Taloustiedettä, kamarimusiikkia ja sen sellaista. Yritän pitää mielen avoimena uudelle. Hyviä nauruja ei voita mikään !

Joined October 2015

- Tweets 16,443

- Following 246

- Followers 522

- Likes 32,531

169 Photos and videos

Jun 7

Jos valintoja ei tehdä rationaalisesti, silloinhan lukukausimaksu ei myöskään välttämättä vähennä halua kouluttautua hs.fi/mielipide/art-20000120…

1

2

8

3,189

Jun 5

Jaaha…mitään ei aiota tehdä vaikka alue on kaoottinen ja turvaton. Pistäkää nyt edes vaikka 10 km/h nopeusrajoitus pyöräilijöille ! hs.fi/helsinki/art-200001205…

1

143

Jun 4

Tämä. Alueesta tehtiin ”jalankulkijalähtöinen” minkä vuoksi ei suojateitä vaan pyöräilijöiden haluttiin sopeuttavan vauhtinsa jotta pyörätien voisi ylittää turvallisesti mistä vain. Aika on tunnustaa että tämä idea oli totaalinen aivop… hs.fi/helsinki/art-200001199…

87

May 29

Hei @hsfi onko pakko kirjoittaa tavalla joka lisää vastakkainasettelua ? Miksi ”ekonomisti vaatii” ? Ei ekonomisti tässä vaadi yhtään mitään vaan esittää ehdotuksen. hs.fi/politiikka/art-2000012…

3

3

12

3,080

May 27

Putin leikkii nyt tulella. Lähetystöjen alue on kv. oikeuden mukaan lähetystön kotimaan suvereenia maaperää. Nato-maan ollessa kohteena tämä merkitsisi hyökkäystä Nato-maahan. hs.fi/maailma/art-2000012035…

2

54

May 20

Hei @hsfi jos toimittajalla on huono omatunto siitä ettei ole selvittänyt mistä Sudanin sodassa on kysymys, niin eikö sitä mea culpan sijaan viimeistään tässä olisi voinut avata ? hs.fi/maailma/art-2000012010…

46

May 8

Äly hoi. Nyt jotakin järkeä tähän byrokratiaviidakkoon ! Aivan kafkamaista touhua kertakaikkiaan hs.fi/politiikka/art-2000011…

2

37

Apr 22

Olipa surullinen uutinen 💔 olin seurannut häntä pitkään ja monet suomalaiset erämaat tulivat tutuiksi hänen kauttaan. Hyvää viimeistä vaellusta Ali, aivan liian varhain lähdit. yle.fi/a/74-20222025?utm_sou…

3

261

Mar 20

Tuli kyllä hyvä mieli tästä jutusta. Uskomatonta omistautumista ja kekseliäisyyttä perhepäivähoitajalta! Melkein olisi tehnyt mieli olla ”lomalla” mukana 😄 hs.fi/suomi/art-200001188932…

2

222

mikael thesleff retweeted

Mar 16

This indeed is a sensible response. When DJT has said that Europe (a) is weak and (b) should take care of its own security, logically E can only contribute to security in the Middle East, if the US contribute to that in Europe. And in Europe the key threat is Russian aggression.

Mar 16

A reasonable European reply would be a resolute”yes but”:

- Yes, we are willing to contribute

- but only if the US supports UKR and demands immediate ceasefire by Russia in UKR

- and only if decisions on UKR and the Middle East will be made via a transatlantic Contact Group

1

27

2,249

mikael thesleff retweeted

Feb 26

This is marvellous

This tweet is unavailable

19

106

559

84,269

Feb 19

Mielenkiintoinen lisä eläkekeskusteluun, tällä kertaa optimaalisen eläkejärjestelmän näkökulmasta. Koska kukaan ei voi valita syntymäkohorttiaan, ”omaan pussiin säästäminen” johtaa kohorttien välisiin valtaviin eroihin eläkkeissä samalla panostuksella ja sijoitusstrategialla

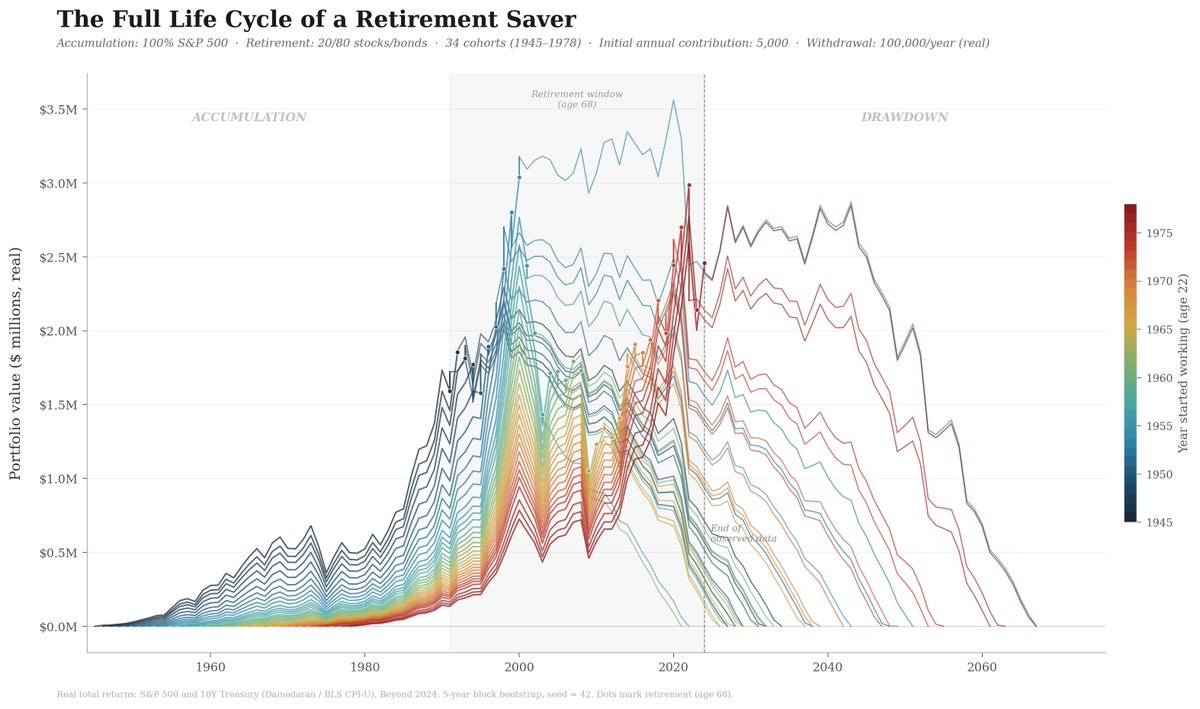

In the first post of this series, I showed that the order in which returns arrive during your working life determines how much wealth you accumulate by retirement. Two workers making identical contributions to the S&P 500 over 46 years ended up with wealth that was 2.9 times different, purely because of when they were born. In the second post, I showed that the problem is worse in retirement.

Today, I stitch the two halves together and ask a simple question: Can you retire comfortably if you save diligently for 46 years? Suppose you want to spend $100,000 a year in retirement and expect to live 30 years (all figures in real term,s). You start saving $5,000 a year at age 22, increasing your contribution by 1% annually in real terms. After 46 years, you have contributed approximately $290,000. Can you get there?

In the figure below, I run the full life cycle (accumulation and drawdown) for 34 cohorts, one for each starting year from 1945 to 1978. The data are the same as in the previous posts: actual annual real total returns on the S&P 500 and 10-year U.S. Treasuries from 1945 to 2024 (Damodaran, deflated by BLS CPI-U). For years beyond 2024, I use a block bootstrap with 5-year blocks from the 1945–2024 sample. Each cohort is run forward until its capital is exhausted. The year of retirement for each cohort is indicated by a dot.

I consider two accumulation strategies. The first invests 100% in the S&P 500 throughout working life. The second follows a glide path: 90% stocks at age 22, declining linearly to 20% at age 68, with the remainder in 10-year Treasuries. At retirement, both switch to the same drawdown portfolio: 20% stocks, 80% bonds, rebalanced annually, with withdrawals of $100,000 per year in real terms.

Start with 100% equities during accumulation. The dispersion in capital at retirement is enormous. The 1954 cohort retires in 2000 with $3.04 million. They rode the postwar expansion and caught the 1990s bull market in their final decade, when their portfolio was largest. The 1963 cohort retires in 2009 with $1.05 million. They accumulated steadily for decades, then the 2008 crisis destroyed over a third of their portfolio in their last working year.

Now run the drawdown. All 34 cohorts are eventually depleted. But how long the money lasts varies enormously. The 1954 cohort sustains $100,000 withdrawals for 67 years. The 1963 cohort reaches zero by 2021, just 12 years into retirement. They did not choose a reckless withdrawal rate. They chose a $100,000 lifestyle and saved for 46 years. The market chose the rest. Their implicit SWR turned out to be 9.5%, which was never going to work. But they had no way of knowing that in 1963.

The cohorts in between illustrate the gradient. The 1957 cohort retires with $1.43 million and lasts 19 years. The 1968 cohort retires with $1.76 million and lasts 23 years. The 1976 cohort retires with $2.99 million and lasts 41 years. The pattern is clear: your retirement outcome is dominated by two draws from the same source of risk — the returns in the last decade of accumulation (which determine how much you retire with) and the returns in the first decade of drawdown (which determine how fast the portfolio erodes).

Now consider the glide path. It does what it is designed to do during accumulation: reduce the dispersion in terminal wealth. Most cohorts retire with between $1.0 million and $1.3 million. The spread is much smaller. But the cost is severe. Because the glide path shifts heavily into bonds during the second half of the working life, when the portfolio is largest and compounding matters most, it sacrifices a large share of expected returns. The median cohort retires with roughly just $1.1 million.

The drawdown consequences are devastating. At $100,000 per year on a $1.1 million portfolio, the effective SWR is approximately 9%. Every single cohort is depleted within 13 to 15 years. The 1954 cohort, the best under equities, retires under the glide path with $1.11 million instead of $3.04 million. It lasts 14 years instead of 67.

The glide path did not fail because of sequencing risk in retirement. It failed because it accumulated too little capital. A $100,000 withdrawal is not sustainable on $1.1 million regardless of the return sequence.

The 100% equity strategy produced enough capital for most cohorts to sustain $100,000 withdrawals for 20 to 40 years. But not all of them. The unlucky cohorts were depleted within two decades. But the lucky ones lasted half a century or more. The equity strategy does not solve the problem. It generates enough expected wealth that the problem becomes survivable for most cohorts. The glide path does not.

This is the central tension. Higher expected returns during accumulation mean more capital at retirement, a lower effective SWR, and a longer-lasting portfolio. But they also mean more variance: some cohorts accumulate far less than others. You can reduce the variance with a glide path, but the cost in expected return is so large that the typical retiree ends up worse off, not better. The insurance is real. It is also ruinously expensive.

I must emphatically highlight that I picked these two strategies because they bracket the range of outcomes, but do not exhaust it. You can adjust the equity share, the glide path slope, the bond allocation in retirement, or the withdrawal amount. You can implement variable withdrawals, add a cash buffer, or use momentum signals. I have run many such variations. The specific numbers change.

But the fundamental result does not: a large share of the variation in retirement outcomes is driven by the sequence of returns, and no portfolio strategy eliminates that variation without a commensurate sacrifice in expected wealth.

So, if you are going to tell me that you have a different strategy than these two, that nobody should follow a $ 100,000 fixed retirement strategy, etc., you are missing the point. The point is that there is a lot of aggregate risk out there, and insuring against it is really costly.

This is why the structure of a retirement system matters. A fully funded system, where each generation saves and invests for its own retirement, exposes every cohort to the sequencing risk I have documented in these three posts. No portfolio strategy eliminates it.

A pay-as-you-go system, by contrast, transfers resources from current workers to current retirees, so the retirement income of the 1963 cohort does not depend on what the S&P 500 did between 1963 and 2009. It depends on the productivity of the workers employed in 2009. That is a different risk, and crucially, it is not the same risk.

A system that combines both components, a funded pillar that captures the equity premium over long horizons and a pay-as-you-go pillar that provides a floor independent of market outcomes, diversifies across two relatively uncorrelated sources of risk.

Neither pillar alone is sufficient. The funded pillar generates higher expected wealth but leaves retirees exposed to bad draws. The pay-as-you-go pillar provides insurance against those draws but cannot deliver the returns needed for a comfortable retirement. A reasonable system has both.

Defenders of full funding point to the superior expected returns and dismiss pay-as-you-go as a Ponzi scheme. Defenders of pay-as-you-go point to the security it provides and dismiss funded systems as a casino. Both are wrong in the same way: they evaluate return and risk separately rather than jointly.

The funded system has higher expected returns and higher risk. The pay-as-you-go system has lower expected returns and lower risk. This is not a puzzle. It is the most basic tradeoff in finance. Anyone who claims one pillar dominates the other on both dimensions is either ignoring the risk or ignoring the return.

And no, pay-as-you-go is not a Ponzi scheme if the system's expenses grow at the same rate as its revenues. This is exactly what notional defined-contribution systems like Sweden’s achieve: benefits are indexed to the growth of the contribution base, so the system remains solvent by construction, even as the population shrinks.

The right question is not which system is better. It is what mix of the two best serves a society that cannot avoid aggregate risk but can choose how to share it across generations.

And that is why modern economics is so incredibly useful and why I love it so much: it gives you the tools to think carefully about these tradeoffs instead of pretending they do not exist.

1

2

245

Feb 15

Kun seuraa maailman menoa joka on tällä hetkellä aika pelottavaa, mieleen tulee myös : demokratiat ovat vahvempia kuin miltä näyttävät kun taas diktatuurit heikompia

84

Jan 26

Tämä NYT juttu ei ole maksumuurin takana. Kahdeksan agenttia Prettin kimpussa jota ensin sprayataan ja pahoinpidellään, sitten ammutaan hänen ollessaan polvillaan maassa ilman asetta.

Jan 26

This New York Times story is not paywalled, and it shows a second-by-second breakdown of what happened. Please scroll through it.

This is not what America, or anywhere, should be

nytimes.com/interactive/2026…

1

262

mikael thesleff retweeted

Jan 24

The Greenland Invasion Scare is over, but Trump may be permanently destroying America's privileged position in the global financial system:

noahpinion.blog/p/what-happe…

50

82

693

201,318

Jan 8

Eurooppalaisena olen monesti ihmetellyt miksi amerikkalaisissa elokuvissa ja tv-sarjoissa (tuoreimpana esimerkkinä Stranger Things) valtionhallinnon edustajat ovat lähes aina pahiksia jotka ovat kansalaisiaan vastaan ja kohtelevat heitä kaltoin. Enää en ihmettele.

3

148

23 Oct 2025

Median suitsiminen ja hiljentäminen on aina kuulunut yksinvaltiaiden pelikirjaan. Nykyään laatumedian voi myös kätevästi korvata kaikenkarvaisilla nettimedioilla jotka toistavat virallista totuutta

22 Oct 2025

The following outlets are no longer credentialed at the Pentagon: NYT, Washington Post, CBS, NBC, ABC, Reuters, Fox

The following outlets are now credentialed instead:

-LindellTV

-Tim Pool

-Jack Posobiec

-TPUSA

-Gateway Pundit

-The National Pulse

-The Post Millennial

3

299

23 Oct 2025

Marssi kohti fasismia jatkuu…

22 Oct 2025

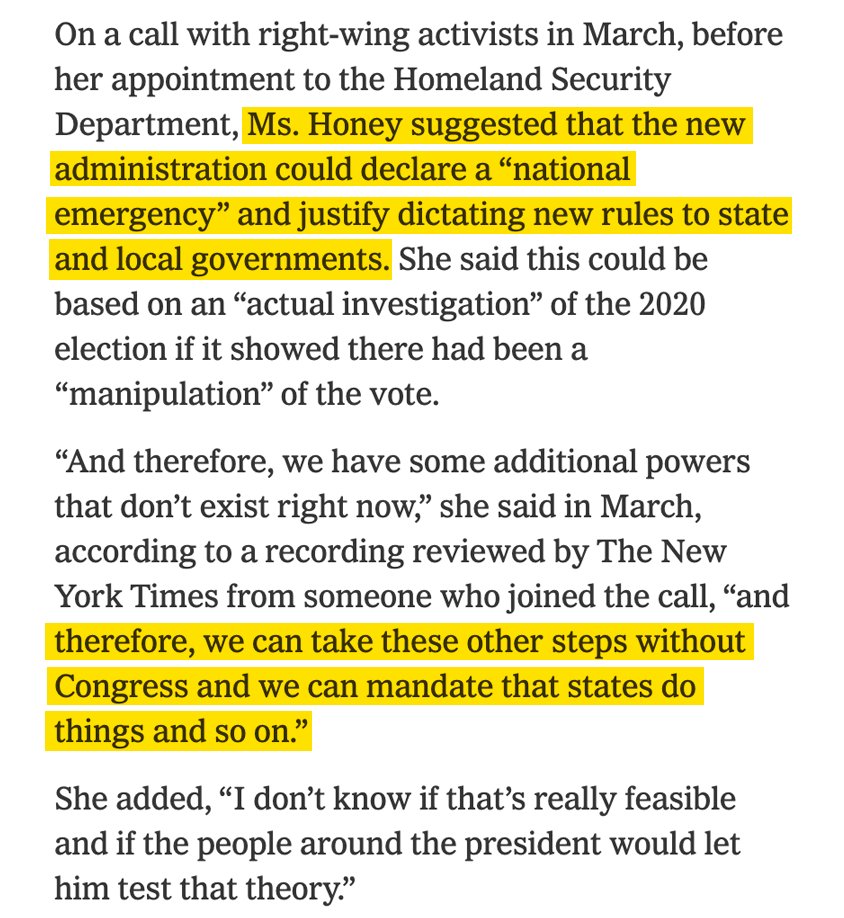

NEW: Trump’s team is plotting to declare a fake national emergency to hijack elections.

One top operative says they can “take steps without Congress” and “mandate" election rules for states.

@NYTimes' investigation exposes the operatives and the takeover already underway. ⬇️

3

150

14 Oct 2025

Congratulations to the fresh Nobel laureates in Economic Sciences ! And also to the legion of their ex-mentees, alumns, advice recipients and sundry coffee acquaintances who have congratulted them while informing us all of their close relationship with the laureates

6

95

mikael thesleff retweeted

13 Oct 2025

Someone less lazy made an excellent thread on the Econ Nobel

13 Oct 2025

🚨 2025 Nobel Prize in Economics goes to Mokyr, Aghion and Howitt 🚨

"for having explained innovation-driven economic growht"

The best prize in years!

2

8

2,731