PR & Communication Strategist| Journalist| Corporate MC & Moderator| Voice Over Artist| Budding Entrepreneur & Actor| Arsenal.

Joined July 2010

- Tweets 33,800

- Following 1,685

- Followers 681,839

- Likes 9,061

1,509 Photos and videos

Pinned Tweet

29 Mar 2024

Grateful to the @avancemedia team for the recognition as Avance Media's 2023 100 Most Influential Young Africans list (8th Edition)!

avancemedia.org/miya100

#100MIYA #AvanceMedia #YoungAfricans

14

75

101

29,435

Mark Masai retweeted

Jun 12

This is how a month of World Cup action began 🔥

3

21

254

9,079

Mark Masai retweeted

Jun 11

The the FIFA World Cup kicks off today. We join millions of fans across Kenya and the world in wishing all participating teams a successful tournament, with a special salute to the African nations carrying our continent’s hopes onto the global stage.

May the competition showcase excellence, unity, resilience and the enduring power of sport to bring people together across borders and cultures.

Let the games begin! ⚽🏆

2

6

13

1,512

Mark Masai retweeted

Jun 11

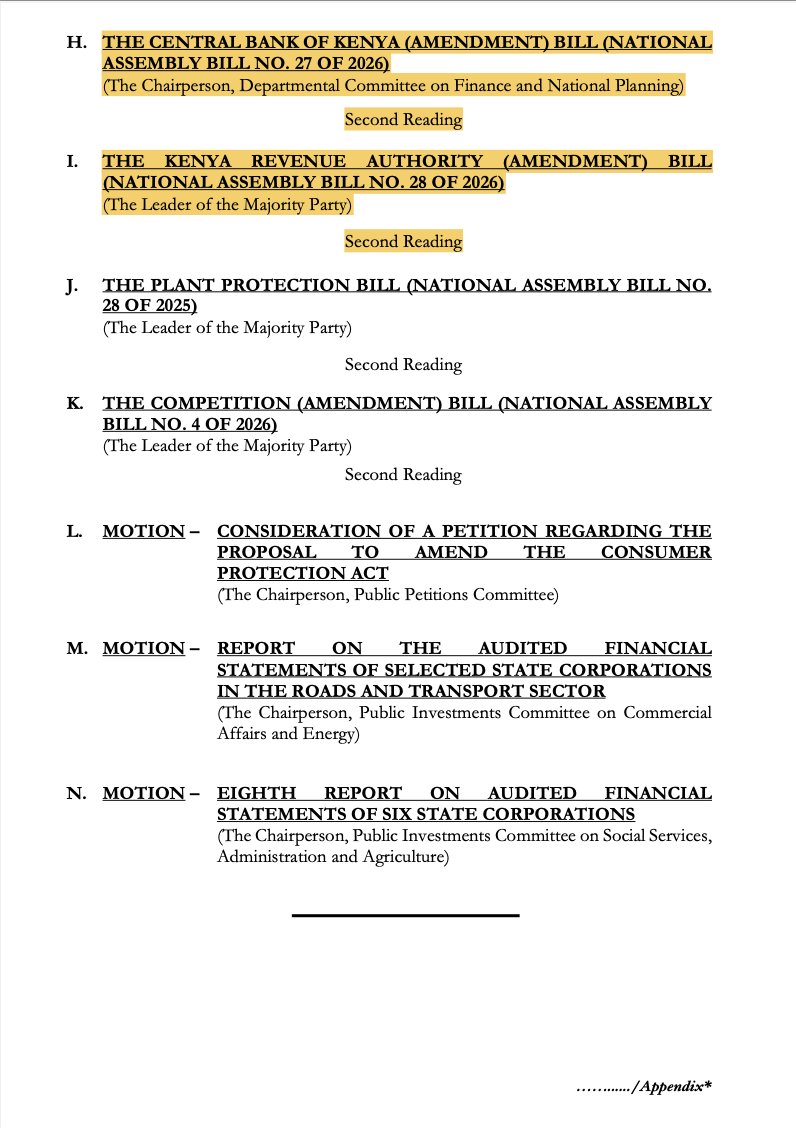

A pretty heavy National Assembly agenda starting this afternoon:

Thursday 11th June, 2026

· Pronouncement of the 2026/27 Budget highlights by National Treasury CS, John Mbadi

Tuesday 16th June, 2026

· Appropriation Bill 2026 goes through the Second Reading & Committee of the Whole House

· Finance Bill 2026 goes through the Second Reading & Committee of the Whole House. This means we should expect the Finance & Planning Committee Report to be tabled

· The Central Bank of Kenya (Amendment) Bill 2026 goes through the Second Reading

· The Kenya Revenue Authority (Amendment) Bill goes through the Second Reading

Jun 10

UPDATE: Kenya's 2026/27 Fiscal Framework

The stalemate on the Equitable Share allocation for 2026/27 has been resolved.

Kes 428.0 billion has been arrived at as the mutually agreed upon allocation for the financial year starting July 1st, 2026.

This 1.9% increase to the planned Equitable Share allocation, considering no adjustment to the revenue numbers, now pushes the 2026/27 budget to Kes 4.857 trillion & the fiscal deficit to Kes 1.23 trillion, 5.9% of GDP.

1

12

29

18,608

Mark Masai retweeted

Jun 11

From Morocco’s Atlas Lions 🇲🇦 and Senegal’s Lions of Teranga 🇸🇳 to South Africa’s Bafana Bafana 🇿🇦, Africa will be well represented at the Fifa World Cup. 🌍⚽

Which team will you be cheering on? 🔥

33

59

235

32,133

Mark Masai retweeted

Jun 10

"We are spending more than twice the global average on elections. And this is primarily because we are living in a very low trust political environment." - @TomMboya

#TSNR

Listen to the full conversation here --->

youtube.com/watch?v=CvjY4hrn…

7

8

1,113

The world has been warned El Nino is returning, so what is it, and should we be worried?

@SeabrookClimate has the details about the natural weather phenomenon

trib.al/KTLSYFP

68

27

51

24,054

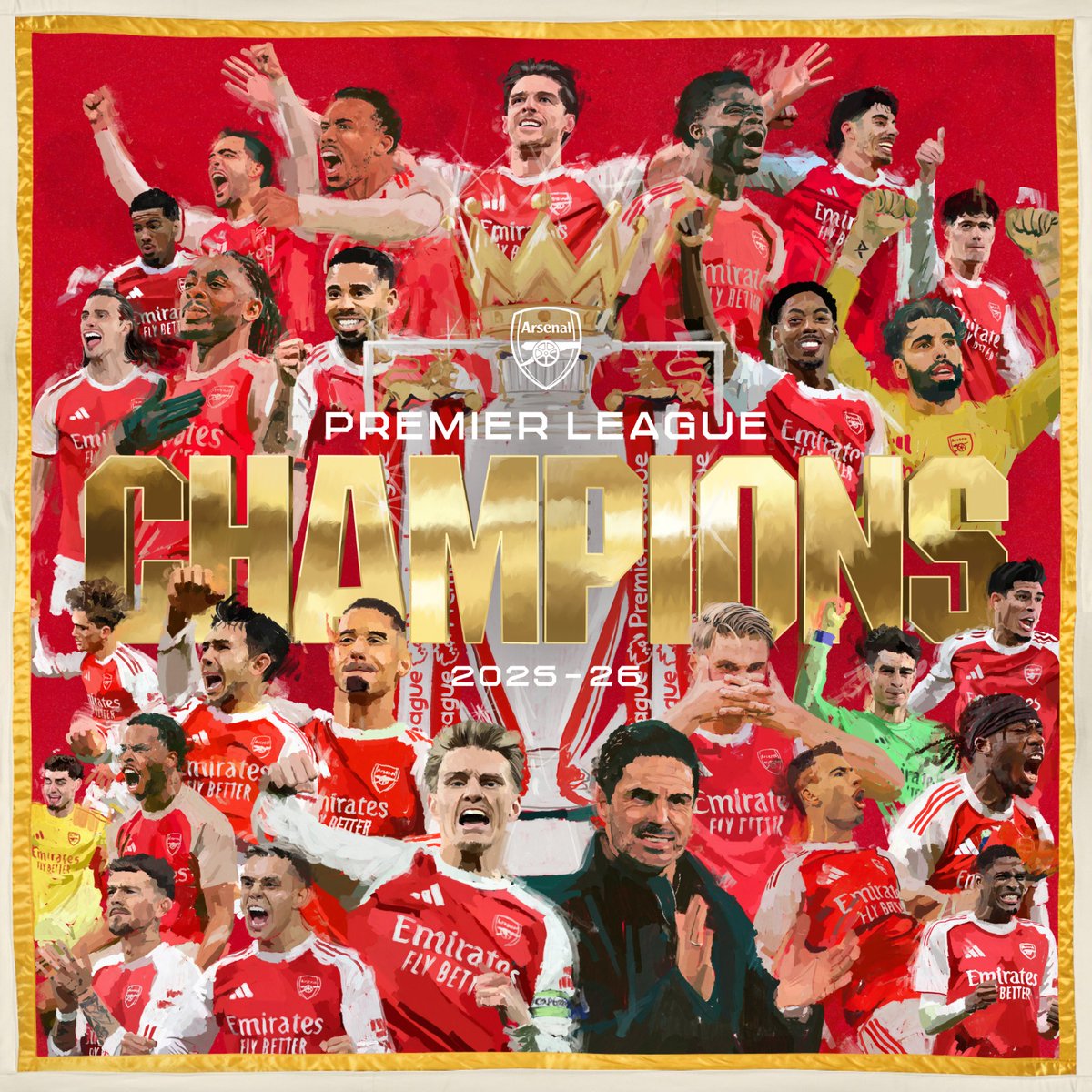

Mark Masai retweeted

May 31

A moment that was 22 years in the making.

This time last week, @Arsenal lifted the Premier League trophy 🏆

308

5,026

32,707

503,755

Here's everything you need to know about today's historic parade 👇

779

3,468

20,484

492,111

A special observer on MD-1 👑

Watch Inside Training from the Puskas Arena, on The Arsenal app ⚡️

193

969

7,887

158,720

Mark Masai retweeted

May 30

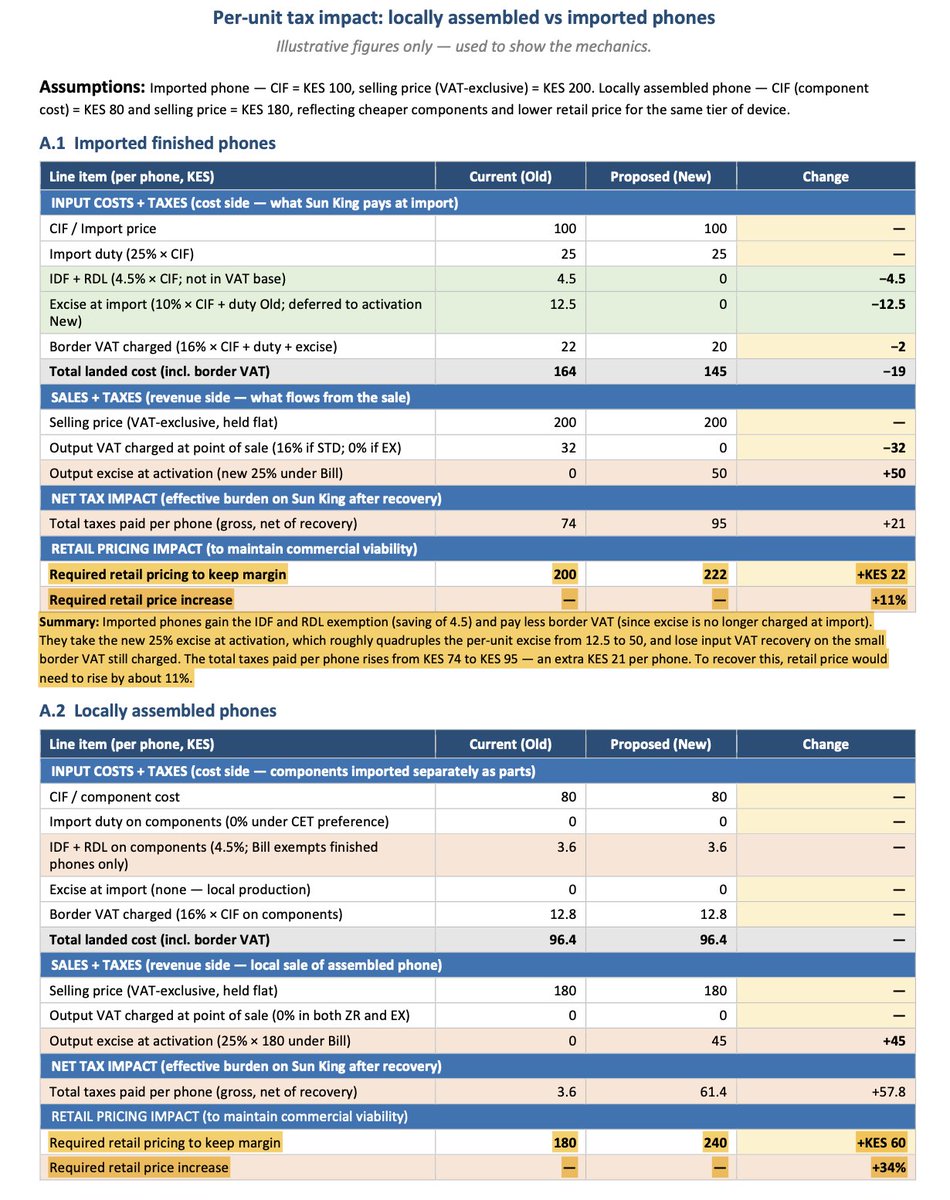

The National Assembly Finance & Planning Committee has been told that the argument by the National Treasury that Finance Bill 2026 will make phones cheaper by consolidating taxes on mobile phones is incorrect.

In case you are lost, here's what Finance Bill 2026 proposes:

· Delete paragraph 29, of the 2nd Schedule to the VAT Act, 2013 which currently provides VAT

zero rate on the supply of locally assembled & manufactured mobile phones

· The Bill proposes to classify as exempt the supply of imported or locally purchased telephones for cellular networks & other wireless networks

· Impose 25.0% excise rate on locally assembled phones (currently 0%) & increase the rate on

imports from 10.0% to 25.0%

· Also, the Bill shifts the excise duty trigger to the point of phone activation

· The Bill proposes to exempt imported finished phones from IDF and RDL

Sun King's core argument is that Finance Bill 2026 means that locally assembled phones will lose 3 protections they currently enjoy simultaneously:

· Input VAT recovery since they are being reclassified from Zero-rated to Exempt status

· Prior excise exemption

· While Finance Bill 2026 exempts imported finished phones from IDF and RDL, it provides no equivalent relief for imported components used in local assembly of phones

Sun King argues that the net effect of Finance Bill 2026 proposals is that:

· There will be ~11.0% retail price increase required to make the current operations for imported finished phones viable under a Finance Bill 2026 tax regime

· There will be a ~34.0% retail price increase required to make the current operations for locally assembled phones viable under a Finance Bill 2026 tax regime

Sun King argues that its Tatu City facility (Kes 25.0 million invested, 50 direct jobs, 80,000 phones produced to date) would face closure under a Finance Bill 2026 arrangement as currently proposed.

7

63

69

7,459

Mark Masai retweeted

May 28

CS Migos Ogamba: Out of 808 girls, 79 were injured. 71 have been treated and discharged while 7 remain admitted. We have 16 fatalities whose identities will be identified. The process of accounting is taking place

24

70

623

93,412

Mark Masai retweeted

May 26

Should the taxpayer still bear the burden of proof in instances where a tax dispute with the Revenue Authority is based in pre-populated & third party data?

In my submission before the National Assembly's Finance & Planning Committee on behalf of the Tax Research Centre at @StrathU, I argue that Finance Bill 2026's proposals seeking to anchor Incomes & Expenses Validation in law will be incomplete if they do not include a proposal for the the Revenue Authority being saddled with the burden of proof in such instances.

Here's why:

· Finance Bill 2026 proposes to amend Sec75 of the Tax Procedures Act to provide that the Revenue Authority may use technology to pre-populate tax returns on behalf of a person required to submit or lodge a tax return

· Finance Bill 2026 further proposes that a person required to submit or lodge a tax return may rely on pre-populated return generated by the Revenue Authority to file their return

· Finance Bill 2026 proposes to amend Sec112 to provide that the Cabinet Secretary of the National Treasury may make Regulations for the procedure for the submission or lodging of returns based on pre-populated tax returns generated by the Revenue Authority

Here's where the problem is:

· In all this, Sec56(1) which provides that "In any proceedings, the burden shall be on the taxpayer to prove that a tax decision is incorrect" remains unchanged

· Sec56(1) is predicated on the fact that Kenya has been running on a self-assessment based regime & the data upon which tax disputes emerges was held by the taxpayer

· With Incomes & Expenses Validation & the onset of a Dual Assessment regime in Kenya, taxpayers are now exposed not just to errors of judgement & data on their part, but also errors of technology & transmission which are out of their control

· Can we really still have the burden of proof lying exclusively with the taxpayer in an environment where tax compliance has shifted from a function of record keeping to one where system integration reliability is now a key factor?

49

1,081

1,789

256,296