#Metals & #MiningStocks News & Analysis. #Gold, #Silver, #Copper, Lithium, Uranium and pretty much all the #Commodities from Aluminum to Zinc.

Joined April 2011

- Tweets 139,742

- Following 2,321

- Followers 4,916

- Likes 25,444

15,369 Photos and videos

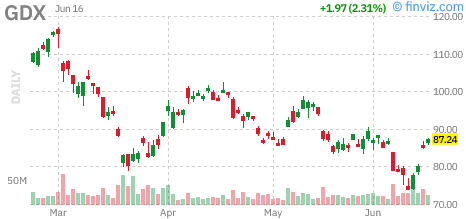

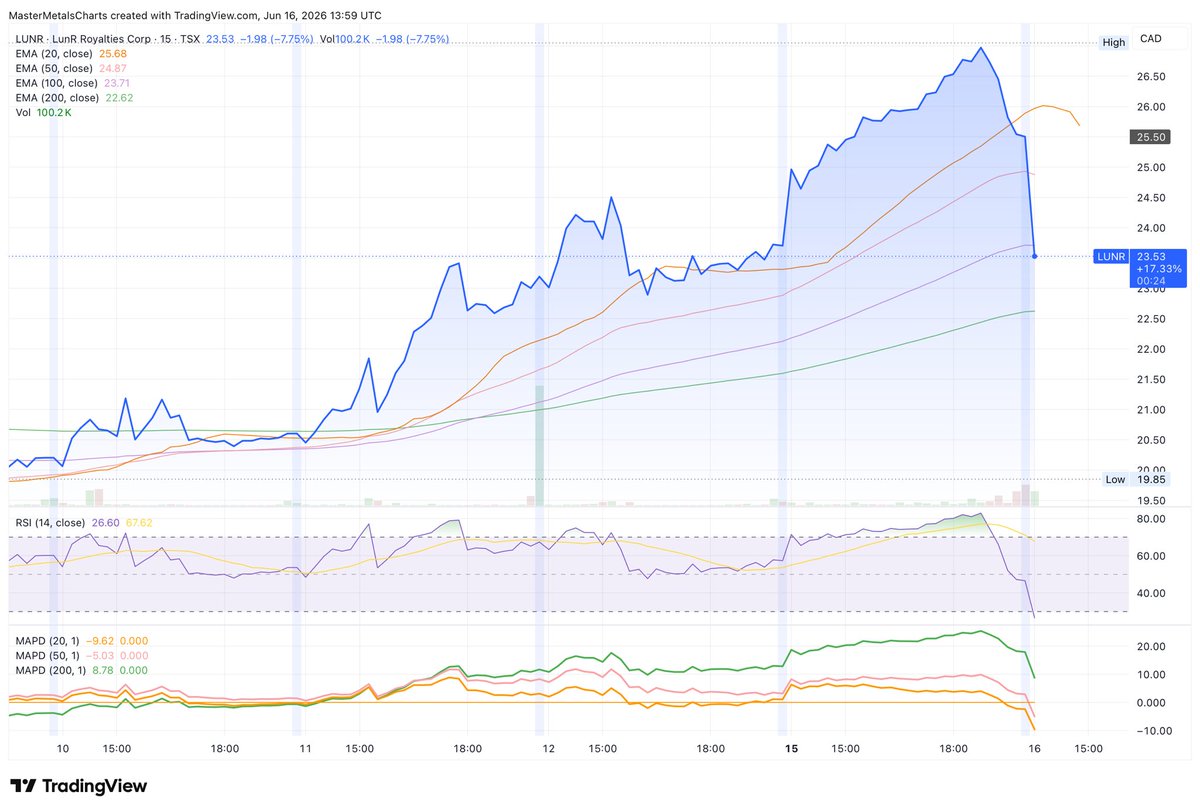

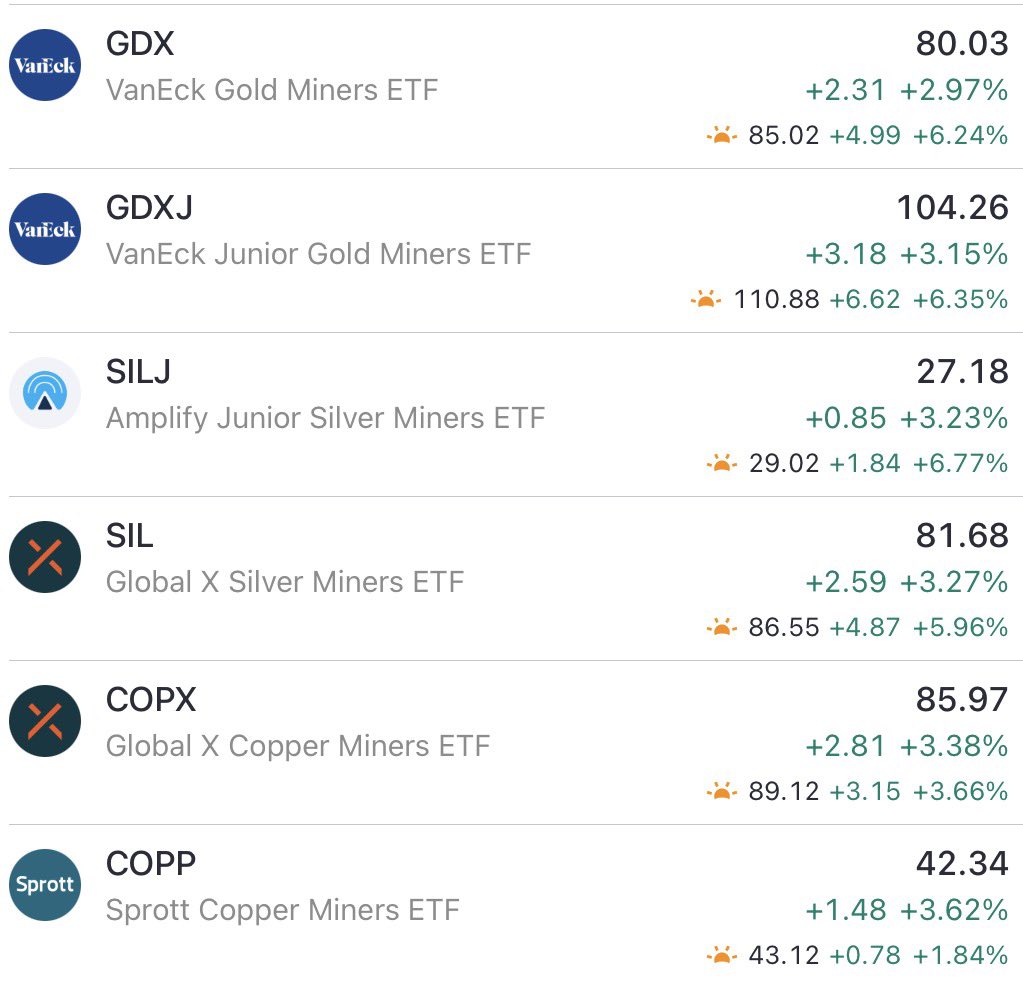

$GDX: VANECK GOLD MINERS ETF UP 2.2869%, last at $87.22 on June 16, 2026 at 02:00AM.

bit.ly/MasterMetalsETF #MasterMetals

1

88

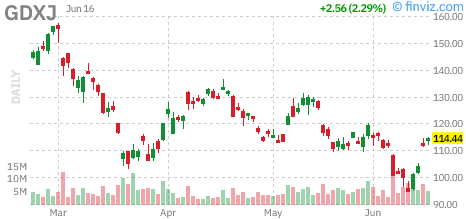

$GDXJ: VANECK JUNIOR GOLD MINERS ETF UP 2.2167%! Last at $114.36 on June 16, 2026 at 02:00AM bit.ly/MasterMetalsETF #MasterMetals #GDXJ

1

93

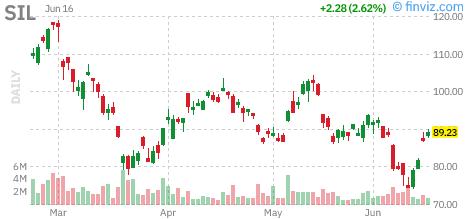

Global X Silver Miners ETF $SIL UP 2.5992%! Last at 89.21

bit.ly/MasterMetalsETF #Silver #SIL #MasterMetals #charts

1

90

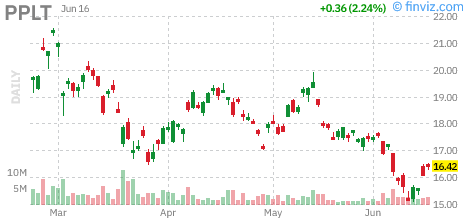

#Platinum $PPLT UP 2.2416%! abrdn Physical Platinum Shares ETF Last at $16.42 on June 16, 2026 at 02:00AM. #MasterMetals bit.ly/MasterMetalsETF

91

It’s great Venezuela’s Gold Mining areas are finally being cleaned up. Just not sure bombing illegal miners’ sites is the way to go about it….Don’t forget all these criminals are there with the full backing of those in power in Venezuela today, helping them to 🧺 their 💰…

Lots of metals in Venezuelan..

Venezuelan crime boss’s demise creates opening for mining boost ⛏️🇻🇪

mining.com/web/venezuelan-cr…

2

160

Jun 16

102

Jun 15

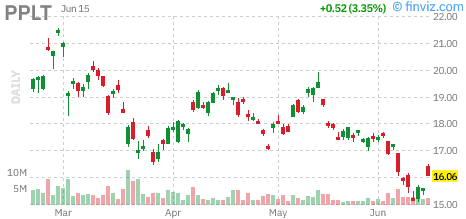

#Platinum $PPLT UP 3.3462%! abrdn Physical Platinum Shares ETF Last at $16.06 on June 15, 2026 at 02:00AM. #MasterMetals bit.ly/MasterMetalsETF

125

Jun 15

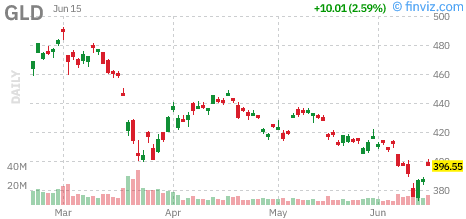

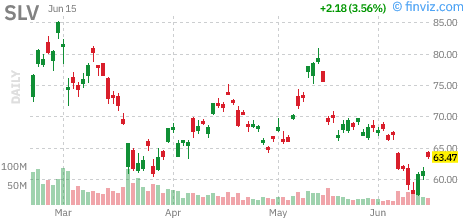

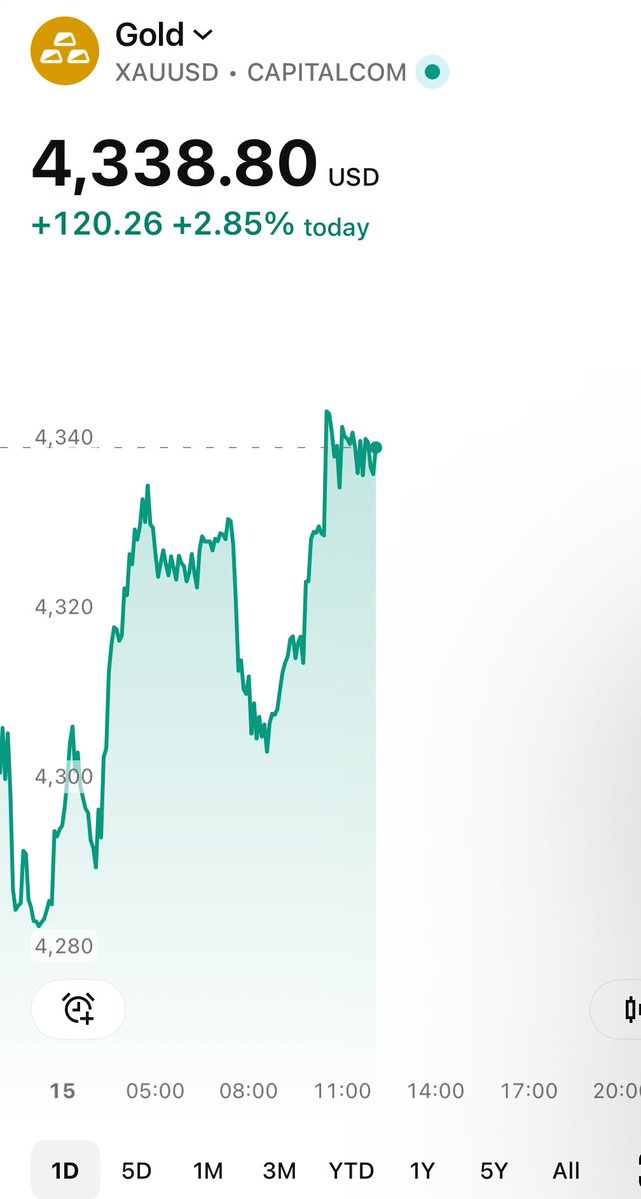

#Silver $SLV ( iShares Silver Trust) up by 3.5569%! Last at 63.47 https:bit.ly/MasterMetalsCharts #MasterMetals

1

167

Jun 15

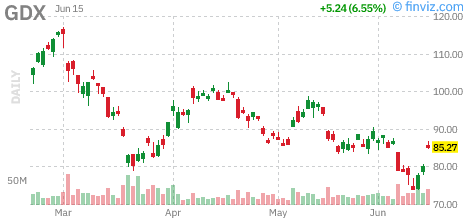

$GDX: VANECK GOLD MINERS ETF UP 6.4851%, last at $85.22 on June 15, 2026 at 02:00AM.

bit.ly/MasterMetalsETF #MasterMetals

2

142

Jun 15

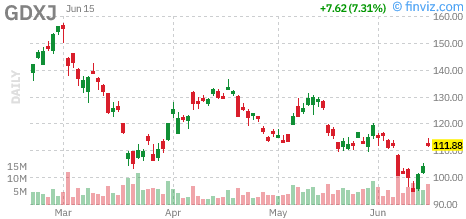

$GDXJ: VANECK JUNIOR GOLD MINERS ETF UP 7.2607%! Last at $111.83 on June 15, 2026 at 02:00AM bit.ly/MasterMetalsETF #MasterMetals #GDXJ

5

133

Jun 15

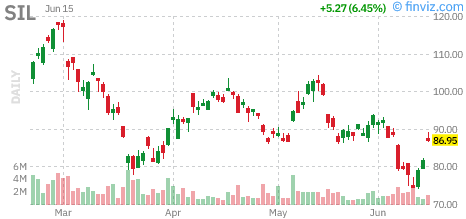

Global X Silver Miners ETF $SIL UP 6.5867%! Last at 87.06

bit.ly/MasterMetalsETF #Silver #SIL #MasterMetals #charts

1

144

Jun 15

Now that’s an embarrassing stat…

And to think they didn’t put Lamine Yamal until the 70th minute… I know he was recovering from injury, but would’ve been better to let him play the first 30 minutes than the last 20 as a desperate measure…

Jun 15

🚨 𝗕𝗥𝗘𝗔𝗞𝗜𝗡𝗚: Mikel Oyarzabal has become the first player since 1966 to spend 30 minutes in a World Cup match without touching the ball once.

— @OptaJoe

270

Jun 15

😅😂🤣

Jun 15

Nos va a hacer portería a cero un tipo que vale lo mismo que un Renault Kangoo. Estoy devastado

1

141

Jun 15

Jun 15

AURION COMPLETES ARRANGEMENT WITH AGNICO EAGLE MINES LIMITED $AIRRF.US | CEOCA Breaking News

ceo.ca/@newswire/aurion-comp…

1

1

256

Jun 15

Jun 15

$SURG.NE 🎯 @YellowLabLife

“If we double the share price to c$1.50 where the warrants are accelerated, it’s only ~c$650mm

“So it’s a double just to get to 0.1x P/NAV

“When looking at comparable projects, why shouldn’t this trade at 0.2-0.3x P/NAV?”

133

Jun 15

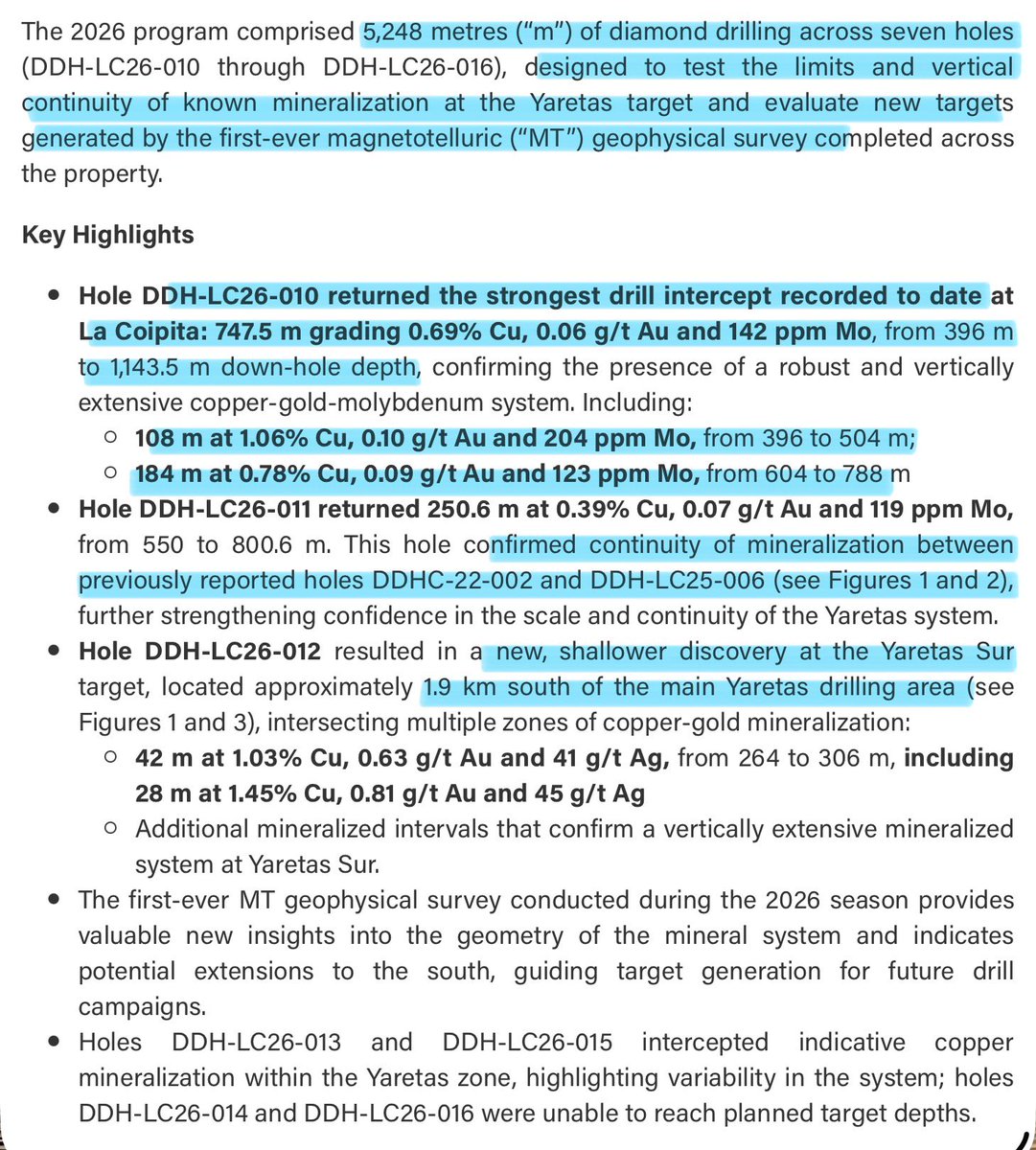

$ABRA.TO Results from 5,248 metres of drilling across 7 holes to test limits & vertical continuity of known mineralization at Yaretas target.

Hole DDH-LC26-010: 747.5 m @ 0.69% Cu, 0.06 g/t Au and 142 ppm Mo, from 396 m to 1,143.5 m down-hole depth; strongest drill intercept recorded to date at La Coipita:

Jun 15

📣 PRESS RELEASE!

AbraSilver Reports 2026 La Coipita Project Drill Results; Best Hole Returns 748 Metres of 0.69% Copper, 0.06 g/t Gold and 142 ppm Molybdenum

Drilling Confirms Continuity of Large-Scale Mineralized System & Delivers New Discovery

“The 2026 drill program delivered several important milestones at La Coipita. Most notably, hole DDH-LC26-010 returned the strongest intercept drilled on the property to date, while hole DDH-LC26-011 confirmed the continuity of mineralization across the core Yaretas system.”

Read more: abrasilver.com/news-releases…

$abra $ABRA.TO #silver #preciousmetals #commodities #argentina

1

259

Jun 15

$SURG.NE 🎯 @YellowLabLife

“If we double the share price to c$1.50 where the warrants are accelerated, it’s only ~c$650mm

“So it’s a double just to get to 0.1x P/NAV

“When looking at comparable projects, why shouldn’t this trade at 0.2-0.3x P/NAV?”

There is a lot of detail to go though here but the main takeaway for the Koala is Berg is a multi-decade ~140kt CuEq copper project with a 24-36% after-tax IRR and 2-3 yr payback assuming:

2Q 2026 costs

Prices somewhere between $4.75/lb and spot (~$6 /lb) on copper

In a consensus first world jurisdiction

With quotes provided by two First Nations groups relevant to Berg and the Premier of BC (who isn’t exactly considered Mr “I love mining”)

With an after-tax NAV of C$4.6-9.4 billion, today the market cap is <c$300mm

In the koala’s opinion, true NAV somewhere in the middle of that range (no major copper producer is being priced like it’s going below $5/lb)

If we double the share price to c$1.50 where the warrants are accelerated, it’s only ~c$650mm

So it’s a double just to get to 0.1x P/NAV

When looking at comparable projects, why shouldn’t this trade at 0.2-0.3x P/NAV?

Now you see why Surge Copper $SURG.V has been the benchmark for every copper developer and producer in the eucalyptus tree for the past 13 months since the updated metallurgical work was released

Biggest mistake this year so far was not taking more of that February financing

1/2

1

1

272