Law and things @ConsenSys. Card carrying member of team #DoLittle.

Joined October 2016

- Tweets 2,297

- Following 235

- Followers 5,225

- Likes 1,351

72 Photos and videos

Matt Corva retweeted

Jun 8

The MetaMask Agent Wallet is here. 🦊

Early Access is now live - 200 spots available.

👇

90

86

562

120,217

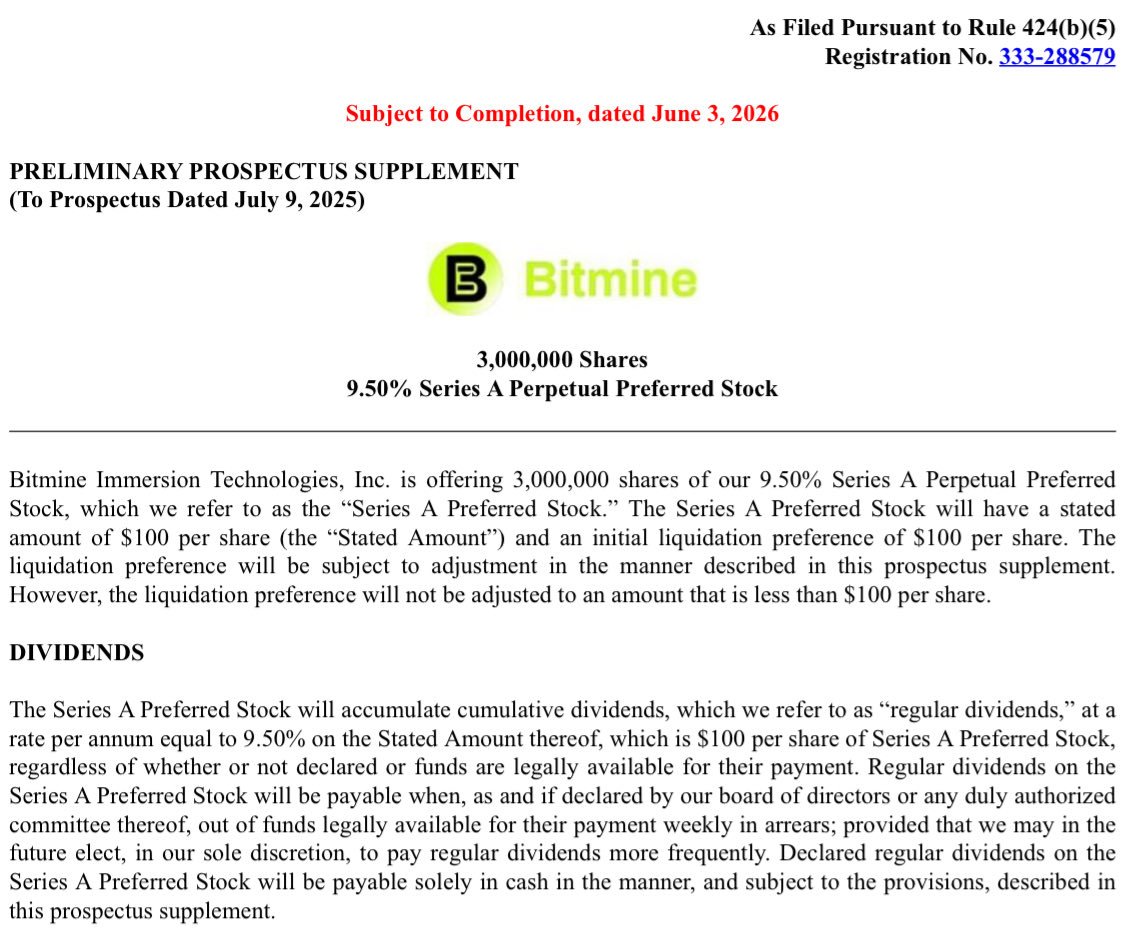

Jun 3

Let me go on record and say that debt in DAT's is dumb, but this could be different than STRC at least in the sense he's paying 9.5% on a much smaller number than what he's earning 3% on. The native ETH yield should safely cover his debt obligations, would be what I assume he's thinking.

192

Jun 1

A reminder to everyone that not all DATs are uber-complex financial engineering debt-driven ticking time bombs. AFAIK, the two biggest ETH dats (BNMR and SBET) remain debt-free "long-term permanent capital." (who are also earning ~3 % on their treasury).

Jun 1

DATs were the worst thing to possibly ever happen to crypto

2

236

May 25

These and most similar takes are drivel. Evaluating prices against momentary “ATH” is a fools errand in crypto with assets being extremely volatile but having little sustained price duration during volatility. ETH and BTC have their troubles but both are mindshare sinks with sustained long term adoption across their purported use cases. Nothing is likely to replace BTC as a store of value. Nothing is likely to replace ETH as the base asset for an actually and meaningfully decentralized global settlement layer.

May 25

3

3

19

2,416

Matt Corva retweeted

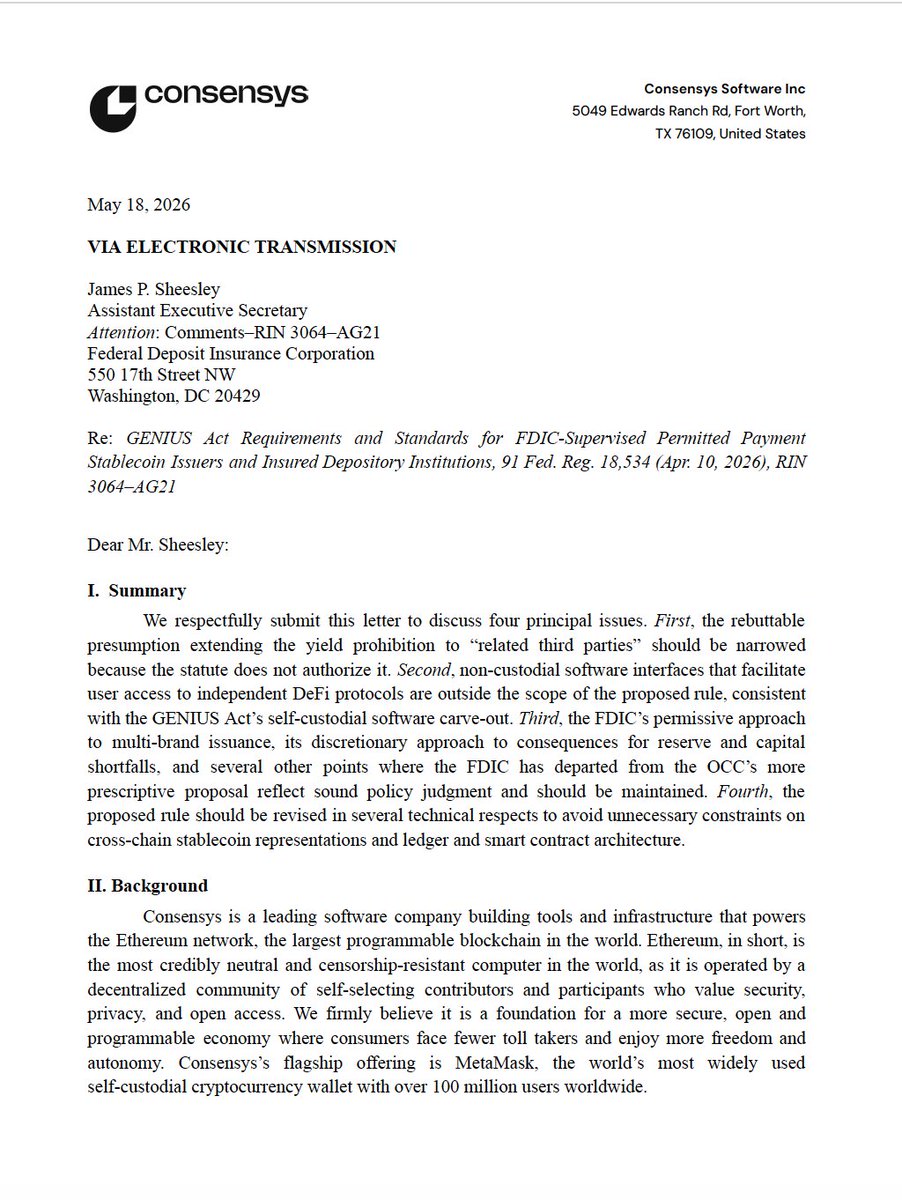

May 19

Following our comment letter to the OCC, this letter responds to the @FDICgov notice of proposed rulemaking relating to GENIUS Act implementation. Our comments track what we told OCC but differ in some material respects.

First, the rebuttable presumption extending the yield prohibition beyond stablecoin issues to “related third parties” should be narrowed because the statute does not authorize it. Companies like @metamask that have branded distribution deals are beyond what the law says is prohibited, are akin to plenty of other commercial arrangements in the financial system, and shouldn't be barred if we want to adopt the best pro-consumer policies.

Second, non-custodial software interfaces that facilitate user access to independent DeFi protocols are outside the scope of the proposed rule, consistent with the GENIUS Act’s self-custodial software carve-out. This seems obvious but we need to say it nonetheless

Third, the FDIC’s permissive approach to multi-brand issuance, its discretionary approach to consequences for reserve and capital shortfalls, and several other points where the FDIC has departed from the OCC’s more prescriptive proposal reflect sound policy judgment and should be maintained. You got it write FDIC so stick to your guns during interagency deconfliction!

Fourth, the proposed rule should be careful to properly conceptualize and categorize cross-chain stablecoin representations and ledger and smart contract architecture. Accuracy here will meaningfully impact the industry.

As always, our sincere gratitude at the work the @USTreasury and its sub agencies are putting into this and the speed with which they are going.

May 19

Consensys has filed a comment on the @FDICgov's GENIUS Act proposal, outlining four areas that need refinement.

This filing, alongside our OCC and Treasury comments, marks the start of a broader conversation with federal banking agencies on getting the GENIUS Act rules right.

Read our full comment letter: consensys.io/blog/fdic-geniu…

1

5

14

2,525

Matt Corva retweeted

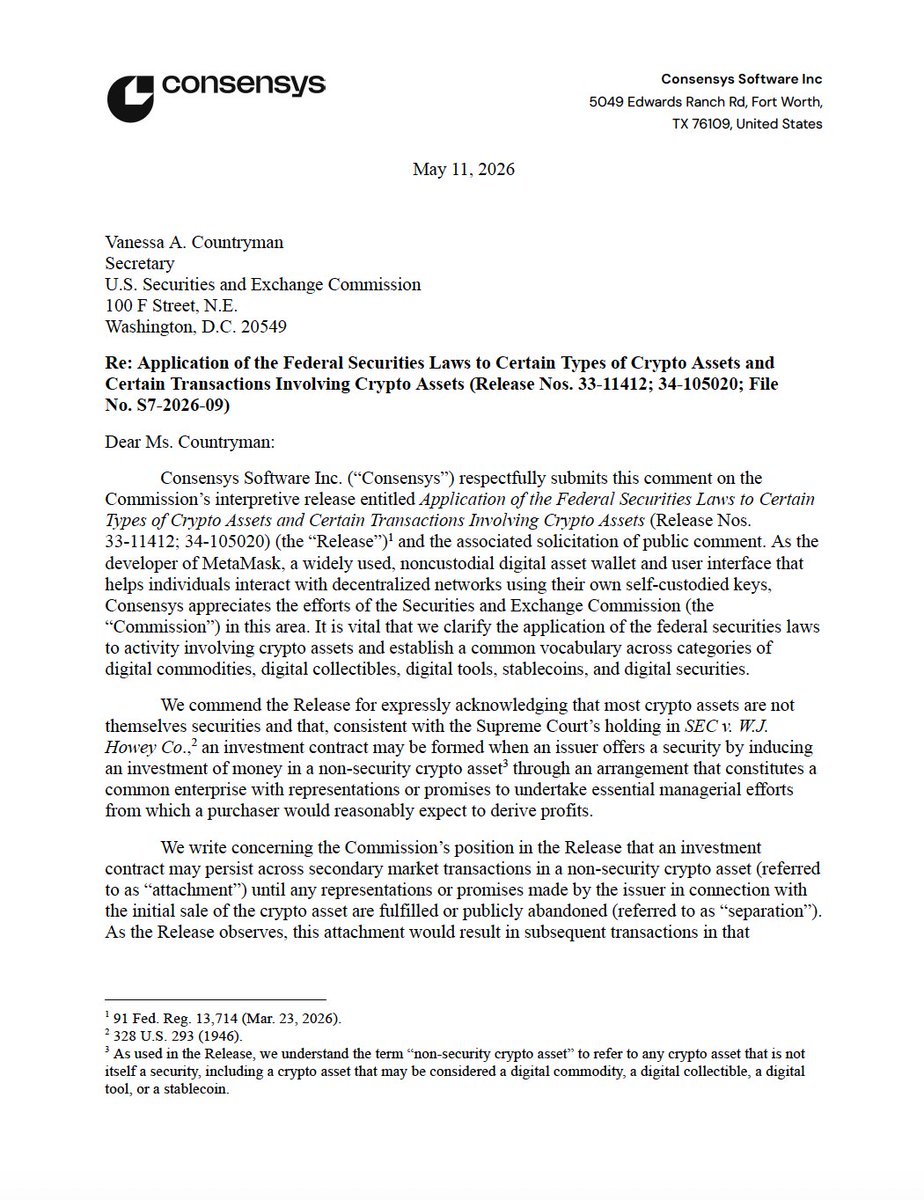

May 12

We have a small securities problem that impacts DeFi but that no one has really been talking about. While we all (rightfully) applaud the @SECGov interpretive guidance on token taxonomy and the Division of Trading & Markets staff guidance on registration of neutral crypto self custody wallets and DeFi interfaces, there is an issue when you read the two side by side.

Did you catch it? If you don't want a spoiler, then stop reading here.

For those who read on . . . you know that digital commodities are outside the SEC's purview. The Interpretive Guidance says it. You know that to avoid registration you need to make your interface very neutral if it is going to allow users to trade tokenized securities. That's what the Staff Statement says. But what about transactions in non-security crypto assets that remain "attached" to an investment contract? Those transactions are securities transactions, says the Interpretive Guidance, but the Staff Statement doesn't say anything about the registration requirements of an interface that users employ to transact in them.

This is a HUGE category of tokens. Like basically all of them. 99% of them.

If we got nothing else from the SEC, what do we, your humble yet tenacious US-based wallet and interface providers, do? Maybe each of us simply figures out which non-security crypto assets are attached to investment contracts and which have "separated", as the Interpretive Guidance lays it out.

I'd love to do that. Really I would. But I'm afraid that just isn't going to work. Not only is the "attached/separated" concept brand new with very little (none?) guidance on how it is to be applied, but also its built on the Howey doctrine which is generally messy and has had very little to say so far on secondary transactions.

Most important, how on earth are we to expect wallets like @MetaMask to look at the universe of tokens - thousands and thousands of tokens which we have nothing whatsoever to do with especially as it relates to issuance - and be able to parse which ones have outstanding representations and promises that make them subject to an active investment contract (and not only a single assessment, mind you, but one that you have to make continuously!)?

Maybe we could do that when artificial super intelligence takes over and I and my colleagues lose our jobs to all-knowing robots, but until then, it's just not possible for us to do. We wave the white flag on it.

So what DO we do? We all come together and work on exemptive relief with the @HesterPeirce-led Crypto Task Force and with the hard working staff of Trading & Markets. (Ed note: These little regulatory wrinkles/snafus/gaps are simply unavoidable, and that is why you get the public's comments and iterate - which is exactly what the SEC is doing.). We get a safe harbor for good faith, transparent interfaces that avoids harsher securities-focused restrictions that put a drag on potential innovation. And wallets and interfaces in the good ol' U.S. of A. will be able to lead the pack instead of struggling to compete with foreign wallets and interfaces which aren't mindful of SEC guidance.

Our letter is available below. The more the merrier in advocating for this important issue.

May 12

Consensys has filed a comment with the SEC on its recent crypto interpretive release.

We're asking the Commission to establish a safe harbor for providers of self-custodial, user-directed interfaces. This would protect US users' access to the open, neutral tools that define the peer-to-peer blockchain economy.

Read our full comment letter:

consensys.io/blog/closing-ga…

5

12

54

11,673

Matt Corva retweeted

May 12

Consensys has filed a comment with the SEC on its recent crypto interpretive release.

We're asking the Commission to establish a safe harbor for providers of self-custodial, user-directed interfaces. This would protect US users' access to the open, neutral tools that define the peer-to-peer blockchain economy.

Read our full comment letter:

consensys.io/blog/closing-ga…

6

14

79

15,272

Matt Corva retweeted

This is absolutely incredible. 💔

138

830

5,996

563,314

Apr 21

Decentralization does not mean immutable. Immutable means immutable. Decentralization may, in some circumstances, mean there is a path to mutability, but it is a path that is controlled by a decentralized set of actors. In broad decentralization, this may mean tens of thousands of actors running independent nodes. In emerging systems, this could just be a security council (who's existence and capabilities have always been plainly disclosed).

This is good. If you want high degree of immutable properties, go use BTC or ETH natively on each chain.

12

3

11

5,987

Apr 20

Off the cuff musings on security keys, always subject to change:

@tayvano_ is 100% correct and everyone else is wrong. In lieu of a more clear regulatory regime, if you have the ability to try to stop illicit actors and have high confidence information, you should take that action. The wait for a court order or law enforcement order thing is a utopian ideal that doesn't work in practice.

"But this isn't the future I was promised with decentralized stablecoins!!!" No one told you that USDC was free from human intervention. Go use BTC or ETH or something else that's decentralized protocol native if that's the only type of instrument you want to use.

"But it's a slippery slope if these people start freezing funds." It's called capitalism. If they do a poor job, they will devalue the utility of their offering, and people will gravitate to other services over time. Similarly, if they are awful at stopping illicit actors, people should gravitate towards other services over time.

Nation state cyberattacks are a global geopolitical issue without a clear solution. I don't believe blaming the citizens for being mugged is the right approach, particularly IF the citizens are doing what they can to protect themselves. I don't know that there's a clear solution in this case (i.e. the equivalent of blowing up the reactors). Right now it appears to me that most of the response is focused on understanding the attack and tracking the attackers, not necessarily putting them out of business entirely.

4

3

19

3,790

Apr 13

The SEC guidance is great not because of what it says, but because of what it means. For decades our system was built upon centralized intermediaries who for some time provided significant value. In the age of technology, specifically auditable smart contracts, the need for reliance on intermediaries who are more or less rent seekers is gone.

The guidance under Atkins' leadership suggests the Staff is recognizing this. That innovation is necessary to do the best by the Staff's constituents - market participants. Not just by the legacy market infrastructure.

Lots more to do, but this is an incredible moment. If decentralized applications meet their promise, you can pencil this down as the day centralized intermediaries were dealt a critical blow by allowing fair competition against them. (in before all the centralized intermediaries run the same playbook as the banks against CLARITY).

3

12

35

5,744

Mar 11

It's amusing to note that the one issue that caused Democrats at large to align with extractive banking practices and the gambling industry, it's crypto. If crypto came out against cigarettes you'd get Gensler aide articles about how big tobacco is the lifeblood of america.

11

586

Jan 3

Insider trading is a feature, not a bug, of prediction markets. They are markets for information and they should remain that way. That’s the absolute benefit of them - the closest and most real time source of truth that others can monitor and react on. Turning them into solely financial markets neuters their benefit and is incredibly misguided.

2

2

304

Jan 3

For example, in 2018 we approached the CFTC for relief on a prediction market built on @gnosis_. The proposed market was for when the L train (which was supposed to close operations for some time and is the only direct subway thoroughfare from North Brooklyn into manhattan) would open. They asked us “what about insiders” and our reaction was that is the whole point. If you worked construction or policy and had direct info we wanted you participating in the markets. If you were a prospective renter in north Brooklyn you could view the market as most informative as to when you would have direct subway access to the city. Excluding insiders means you are relying on indirect speculation for information. Cc: @RitchieTorres. Don’t turn prediction markets into something they are not intended to be.

1

1

172

Jan 3

Don’t view this as endorsing a world without sensible rules, particularly on elected officials, but let’s not lose sight of what the benefit of these markets at scale can be.

1

129

Matt Corva retweeted

22 Oct 2025

Most points from an 18 year old defenseman in a season, salary cap era:

44 — Rasmus Dahlin

29 — Aaron Ekblad

19 — Zach Bogosion

19 — Jakob Chychrun

12 — Cam Fowler

10 — Noah Hanifin

9 — Drew Doughty

9 — Victor Hedman

7 — Matthew Schaefer

Schaefer's played 6 games.

12

32

913

58,322

Matt Corva retweeted

17 Oct 2025

This is not normal behavior for an 18-year old, rookie defenseman. Calder goes through Schaefer.

20

73

535

298,404

Matt Corva retweeted

15 Oct 2025

JUST IN: 🇺🇸🇨🇳 Treasury Secretary Bessent says he's optimistic about China and they're in communication with them.

403

474

5,417

508,659

Matt Corva retweeted

25 Sep 2025

SharpLink will be the first public company that uses Ethereum to record/issue their official shares.

You'll be able to bridge your shares between brokerage accounts, and ERC-20. DeFi integrations and new use-cases ahead.

Proud to partner with $SBET

25 Sep 2025

NEW: SharpLink is partnering with Superstate to issue tokenized $SBET shares directly on the Ethereum blockchain.

SharpLink will become the first public company to do so.

Together, we’ll work to advance how tokenized public equities can one day trade on Automated Market Makers and other DeFi protocols in a fully compliant way.

SharpLink has always been Ethereum-aligned. This step reinforces our mission to advance the Ethereum ecosystem and modernize capital markets.

The asset is $ETH, the ticker is $SBET.

34

63

630

70,696