Joined August 2022

- Tweets 30,011

- Following 1,290

- Followers 5,699

- Likes 37,284

931 Photos and videos

Pinned Tweet

Apr 14

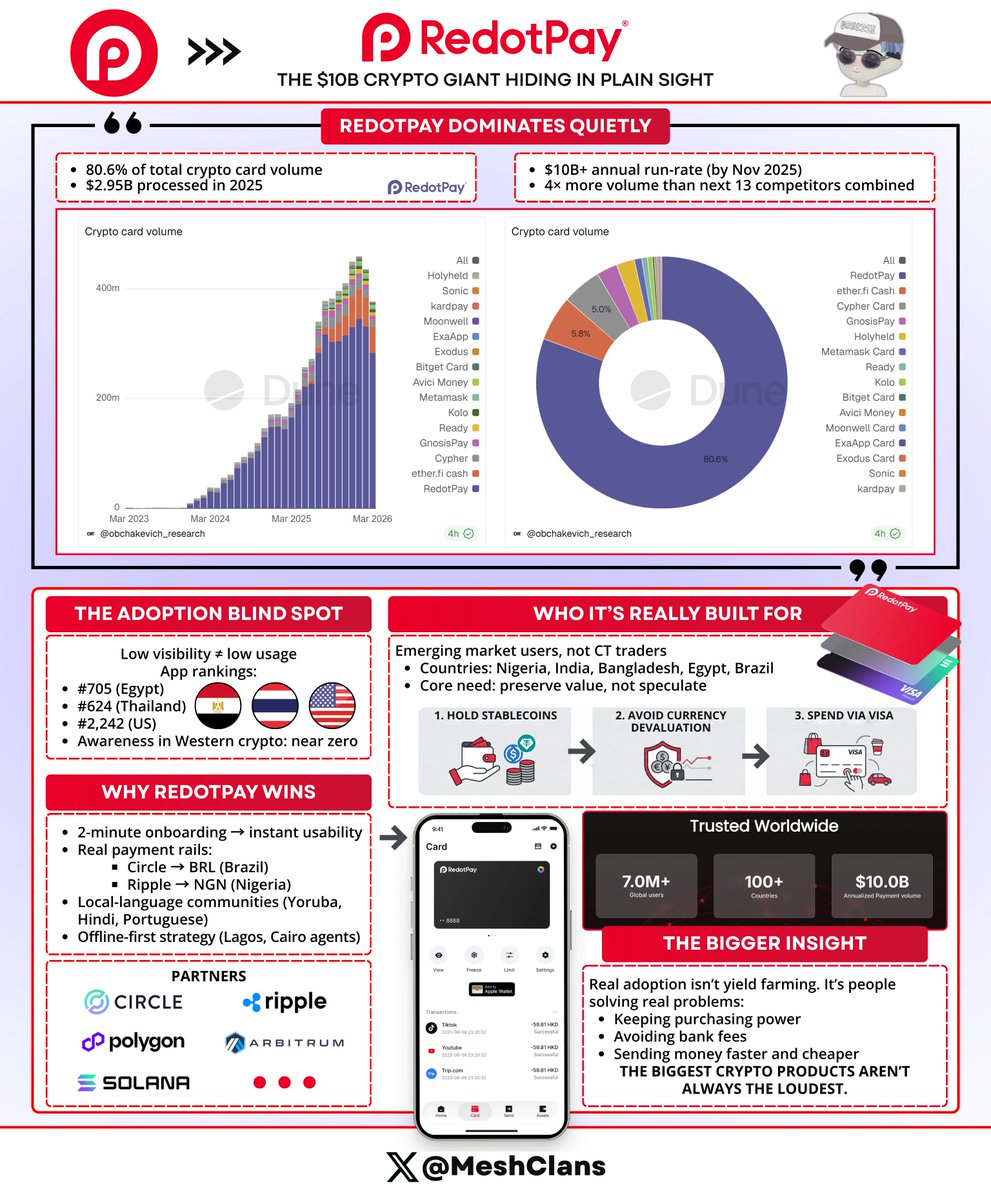

RedotPay controls 80.6% of crypto card volume. Ask 100 people in crypto if they've used it, maybe 2 have even heard of it. I hadn't either until I saw this chart.

I spent some time digging into this anomaly, and what I found changed how I think about crypto adoption.

The data from @obchakevich_ 's Dune dashboard shows @RedotPay processed $2.95B in card transactions during 2025, over 4x what its next 13 competitors did combined, and they hit a $10B annualized run-rate by November 2025.

But here's the weird part the app ranks #705 in Egypt's Finance category and #624 in Thailand, while sitting at #2,242 in the US. I asked 30 people in Western crypto circles about RedotPay. Two had heard the name. Zero had actually used it.

So how does a platform almost nobody on crypto Twitter knows about hit $10B in annual run-rate?

Turns out we've been looking at the wrong map.

RedotPay built for people in Bangladesh, India, Egypt, Nigeria, and Brazil who don't have reliable banking, and the actual use case is straightforward: hold USDT so your savings don't get destroyed when your local currency tanks, then spend it via Visa card for everyday stuff like groceries and bills.

They're not chasing airdrops or staking yields. They just want their money to hold value.

Instead of burning cash on Facebook ads, RedotPay recruited local crypto traders, community leaders, and OTC merchants as agents who earn up to 40% commissions when someone activates a card. The $100 physical card fee and $10 virtual card fee fund the whole thing, and most of their 2025 growth came from people searching for them organically through pure word of mouth in communities we never see.

Getting started takes two minutes: download app, send some USDT, spend anywhere Visa works.

Why is RedotPay so far ahead?

- Two-minute onboarding from download to spending, versus hours learning DeFi protocols

- Real infrastructure through partnerships with Circle (June 2025) for instant BRL payments to Brazil and Ripple (December 2025) for NGN to Nigeria, moving money in minutes instead of days

- Local communities built on Telegram groups in Yoruba, Hindi, and Portuguese, generating massive engagement in languages most of CT doesn't read

- Offline-first distribution with agents on the ground in Lagos and Cairo beating online ads every time

What people actually do with it:

- Deposits are 98% stablecoins (USDT/USDC)

- Spending happens in small amounts multiple times per week

- Real uses include buying food in Cairo, sending money to family in Lagos, and protecting savings from currency collapse in Nigeria

The numbers back it up: they hit 5 million users by August 2024, got to 6M users by November 2025 while adding 3M just last year, tripled their volume in 2025, and they're profitable.

They built it for specific people with specific problems we don't face, and actual adoption looks like a guy in Nigeria making sure his paycheck still buys groceries next month, a family in Egypt paying bills without bank fees, or someone in Bangladesh sending money home without losing 8% to Western Union.

Utility beats speculation when it comes to real volume. Needs drive actual scale. Sometimes the biggest things happen where we're not looking.

Makes me wonder what else is out there that we're completely missing.

73

40

274

50,446

Mesh retweeted

7 GUD READS 📚 (Edition No. 93)

A chain trading 94% below its high while five asset managers quietly pick it.

A token that erased 17.6% of its own supply with real revenue.

A robot that does nothing useful and still has a waitlist.

Catch up on the moments you've missed👇

25

7

54

1,879

Jun 13

Lighter processed $15B in notional volume last week, up 75% week over week.

On the surface, that looks like a clean recovery. But I think the more important question is not whether volume is back.

It is whether the quality of that volume has changed.

This matters because Lighter's previous volume cycle was clearly incentive distorted.

According to Token Terminal data, weekly volume peaked around ~$75B in late November 2025. After the Dec 30 airdrop, incentives faded and volume fell by roughly 70 to 80% .

That was not organic demand disappearing temporarily.

That was a post-airdrop farming unwind.

This is why I care more about open interest than notional volume here. Volume can be manufactured through short-term incentives, wash-like behavior, and mercenary flow. OI is harder to fake because it reflects capital willing to stay exposed on the venue.

At the peak, Lighter's Volume/OI ratio was running in the high 20x range. For context, Hyperliquid sits closer to ~0.76x, while healthier derivatives venues usually operate much lower, often around ≤5x.

So the November spike was not the signal.

The current recovery is more interesting because the underlying drivers look different.

Three things stand out:

- Telegram Wallet went live in April 2026, with Lighter serving as the perps backend across crypto, stocks, metals, and oil

- RWA perps such as SpaceX pre-IPO, Dell, and IBM are expanding the market beyond standard crypto pairs

- LIT listings on Binance and Bybit, alongside Insilico Terminal routing systematic flow natively, are broadening both access and trader composition

Access does not equal adoption, so I would not overstate the Telegram point yet. But distribution of that scale is still meaningful. Most perp DEXs are fighting for the same small pool of crypto-native traders. Lighter now has a path into a much wider retail funnel.

The cleaner metric is Volume/OI.

During this recovery, Volume/OI has normalized around 2 to 5x based on DefiLlama and Artemis data. That tells me the current activity is less dependent on pure incentive churn and more connected to actual market usage.

The architecture is also worth taking seriously.

Lighter uses ZK-SNARK proofs for matched orders, with no mempool and no MEV. In practice, that means execution fairness is verifiable instead of being purely trust-based.

That is a meaningful difference from Hyperliquid's validator-set model.

My view is that this becomes more important as larger and more sophisticated flow enters onchain derivatives. Retail may care most about liquidity and UX today, but institutions will care about execution guarantees, transparency, and market structure risk.

Still, the market has not fully priced that architecture advantage.

Lighter's OI is around ~$766M, while Hyperliquid operates at multi-billion-dollar OI. So the technical argument is real, but conviction capital has not rotated in size yet.

That gap is the real setup.

The post-airdrop collapse proved the old volume base was fragile. The next test is whether Telegram distribution, RWA markets, and systematic flow can turn Lighter into a venue with durable open interest rather than episodic volume spikes.

There are also clear risks:

- Team and investor tokens unlock in December 2026

- OI already exceeds TVL, with TVL around ~$487M

- The LLP is therefore running elevated leverage into a future unlock window where market conditions may become more sensitive

So I would not frame this as a clean breakout yet.

But I do think the current setup is materially stronger than it was six months ago.

The right metric to track is not headline volume.

It is whether OI keeps growing without the Volume/OI ratio breaking again.

31

55

1,598

Mesh retweeted

Jun 12

1/ Crypto adoption is entering a new phase.

For years, digital assets were largely viewed as experimental, speculative, or institutionally inaccessible.

But that narrative has changed meaningfully. BTC and particularly ETH, are increasingly being integrated into the product suites of major financial platforms, treasury companies, funds, and institutional trading venues.

As $ETH adoption deepens, the next question becomes less about whether institutions want ETH exposure, and more about how they should manage it.

Holding $ETH passively gives investors exposure to its long-term upside. But ETH is also a productive asset via PoS yield. For treasuries, funds, and sophisticated users, this creates an obvious opportunity: ETH should not simply sit idle.

The challenge is that native staking is not always operationally simple.

The rabbit hole goes deep → Validator management, withdrawal queues, liquidity constraints, custody requirements & exchange collateral limitations all create friction.

This is esp. true for institutions, where operational resilience, risk management, and liquidity access matter as much as headline yield.

This is where liquid staking becomes increasingly important.

And in 2026, @mETHProtocol $mETH is positioning itself as one of the key yield layers for ETH 🧵

Jun 11

ETH staking is moving beyond yield alone.

“The next phase is about stronger security, deeper liquidity, and better distribution.” - @Defi_Maestro

Read more below on how mETH Protocol is building for 2026.

35

18

84

4,356

Mesh retweeted

Jun 11

I keep coming back to one thing on this chart.

Not the headline number.

The widening gap between Zcash and Monero.

Total Private Value across Monero, Zcash, and Tornado Cash went from $8.31B to $11.17B, a 34% YoY jump according to @MessariCrypto .

That's strong, but the aggregate number almost hides the more interesting story underneath.

@Zcash is up dramatically YoY and is basically driving the sector's growth. Monero is sitting at -5.9%.

Same sector. Same chart. Completely different outcomes.

And imo, that split says more about where privacy in crypto is heading than any price line does.

Zcash's move wasn't just a random privacy coin pump either. There were actual drivers behind it.

Shielded transactions hit highs near 60% of network activity in early 2026, up massively YoY. So people weren't just holding ZEC because privacy was trending again. They were actually using the privacy layer.

Over 30% of circulating ZEC is now sitting inside shielded pools too, which matters because it shows privacy usage becoming sticky, not just speculative.

Then you add the late 2024 halving, @Grayscale's ZCSH trust crossing $196M AUM, and an ETF filing shortly after. The picture gets clearer.

Zcash suddenly has something Monero doesn't have: a regulated-looking path for capital that wants privacy, but can't touch full black-box privacy.

That's the real difference.

@monero's story is more complicated than -5.9% makes it look. On-chain volume still held above pre-2022 levels even after 73 exchange delistings in 2025.

So the demand didn't disappear.

The access did.

I went back and forth on whether that's bullish for Monero or just a sign of where it's stuck. I landed somewhere in the middle.

The protocol is still strong. The demand is clearly real. But a privacy coin you can't easily buy, sell, or route through compliant venues starts losing part of what makes it useful.

Strong privacy. Shrinking on-ramps.

That's not a great combo.

What the market is pricing here isn't just privacy.

It's compliance optionality.

Zcash's viewing keys let users reveal selected transaction data to auditors, counterparties, or regulators while staying private to everyone else. Monero can't really do that by design.

And that's the paradox at the center of all this.

Monero's greatest strength as actual privacy is also the exact thing that makes it almost impossible for institutions to touch in 2026.

Zcash sits in the middle. Private enough to matter. Selective enough to fit into the compliance world.

The same shift is starting to show up outside privacy coins too.

@Paxos launched USAD, a fully encrypted USD-backed stablecoin on @AleoHQ , built for confidential payroll and B2B settlement. That's not just anons hiding transaction history.

That's businesses and institutions that legally can't expose treasury flows, trading activity, payroll data, or counterparty relationships on a fully transparent ledger.

Privacy stopped being an ideology and started becoming infrastructure.

None of this is fully locked in yet.

The Tornado Cash delisting in March 2025 was a real shift, but institutional adoption still depends on regulation becoming clearer. Frameworks like the CLARITY Act still need to move from guidance and political noise into actual law.

So yeah, there's still risk here.

But imo, privacy as a base layer for onchain finance is here to stay. The infra being built around it is too useful to write off as just another cycle trade.

The open question is which protocols actually capture that value.

Two things I'm watching closer than price:

- Shielded transaction share, not ZEC spot price

- Whether the Grayscale ETF clears review

That's when institutional interest stops looking like a trade and starts looking structural.

For now, the market has already made its short-term call:

Compliant privacy beats absolute privacy.

cc: @mert @zooko @_tm3k

34

3

72

2,112

Jun 10

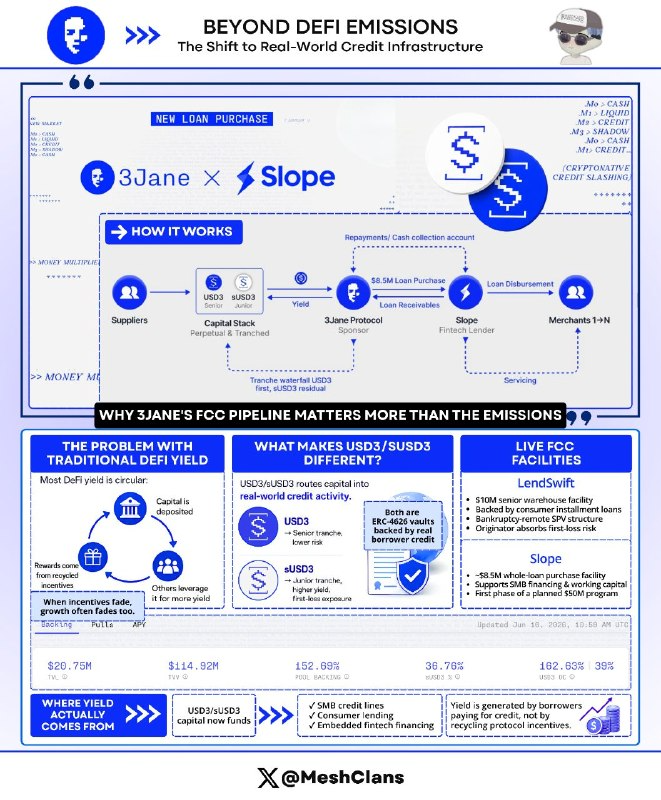

USD3/sUSD3 public deposits are now live.

The emissions will probably get most of the attention today. Fair enough.

But imo, the more important story is where the capital is actually going.

A lot of DeFi yield still runs in circles. You deposit, someone levers up, and the yield comes from the next person doing the same thing. Nothing new really enters the system, so value just moves around until incentives weaken.

We’ve watched this play out enough times that it shouldn’t need explaining, but here we are.

@3janexyz is trying to route that capital into something external: real credit activity.

USD3/sUSD3 is a tranched credit pool. USD3 sits senior in the waterfall, while sUSD3 is the junior, higher-yield tranche with first-loss exposure and a cooldown period before redemptions.

Both are ERC-4626 vaults backed by credit extended to real borrowers, not liquidity incentives recycled through the same protocol.

3Jane’s V1 proved the model with direct credit to U.S. yield farmers. Seven months. Zero defaults.

But V2 is where the more interesting work is happening.

The Fintech Credit Conduit architecture routes USD3/sUSD3 deposits into asset-backed facilities with fintech originators that may have difficulty accessing larger ABS-style markets on their own.

LendSwift was the first clear example: a $10M senior warehouse backed by short-duration consumer installment loans, with a bankruptcy-remote SPV structure and originator first-loss equity.

Now Slope makes the direction even easier to see.

Slope provides embedded business financing and working-capital infrastructure for SMBs and enterprise platforms. 3Jane executed an ~$8.5M whole-loan purchase with Slope, Phase 0 of a broader $50M forward-flow program.

So USD3/sUSD3 capital is now funding SMB credit lines originated through embedded fintech rails.

That’s a meaningfully different borrower profile from V1.

And this is the part I care about: the yield source.

The yield is tied to borrowers paying for actual credit. Most DeFi deposit products can’t really say that, and I think that distinction gets lost in most launch coverage.

The liquidity mining layer runs through non-transferable $JANE emissions, with weekly epochs and TWAB daily snapshots used to reward active deposits over time.

No points system, just a program designed around sustained participation.

Tbh, the FCC pipeline is the real thing to pay attention to.

3Jane is now open to the public

Mint USD3 to earn $JANE

Liquidity mining details below

44

1

78

3,166

Mesh retweeted

Jun 10

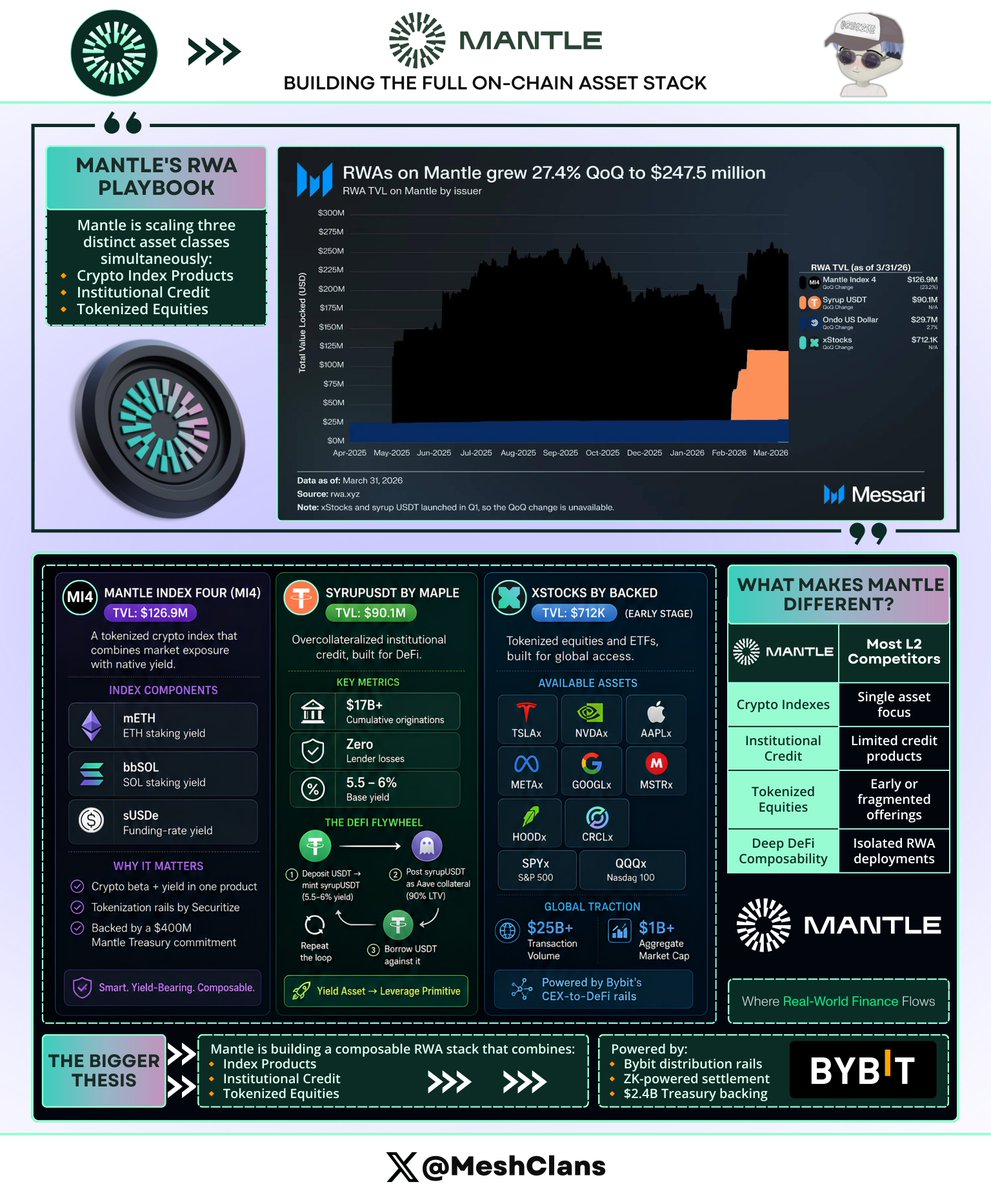

Mantle's RWA ecosystem is doing something most chains aren't, and very few people tracking this space have noticed yet.

The $247.5M TVL with 27.4% qoq growth is only half the story. The more interesting part is how it's built.

Most RWA plays on L2s look like this: one dominant issuer, one asset class, one narrative.

@Mantle_Official 's running three simultaneously across three completely different real-world asset categories, and that architectural decision is what makes this worth paying attention to.

Mantle Index 4 ($126.9M TVL): think crypto S&P 500, except smarter than what TradFi would build. Instead of just holding spot BTC/ETH, MI4 wraps the yield-bearing versions:

- mETH: ETH staking yield

- bbSOL: SOL staking yield

- sUSDe: funding rate arbitrage

So you're getting crypto beta and native DeFi yield inside a traditional fund structure. That combination doesn't exist in TradFi, and that's kind of the whole point.

Securitize built the tokenization rails, Mantle Treasury put up $400M as anchor. This wasn't a small commitment.

syrupUSDT by @maplefinance ($90.1M TVL): overcollateralized institutional credit, over $17B in cumulative originations, zero lender losses. The ERC-4626 structure means it plugs into any DeFi protocol without custom work, which is exactly why it spread so fast.

When Aave listed it as collateral at 90% LTV, the $50M cap filled in hours. I honestly didn't expect it to move that fast. The loop people are running:

- Deposit USDT → mint syrupUSDT (5.5-6% base yield)

- Post syrupUSDT as Aave collateral at 90% LTV

- Borrow USDT against it and repeat

It went from yield instrument to leverage primitive overnight. That's a proven composability story, not just a promising one.

@xStocksFi by @BackedFi ($712K TVL on Mantle, early): tokenized equities on Mantle, structured across Jersey and Switzerland under the Swiss DLT Act, with Kraken's December acquisition making the long-term infrastructure picture a lot cleaner.

The current lineup:

- Single stocks: TSLAx, NVDAx, AAPLx, METAx, GOOGLx, MSTRx, HOODx, CRCLx

- ETFs: SPYx (S&P 500), QQQx (Nasdaq 100)

Bybit's CEX-to-chain rails are what most people are sleeping on here. That distribution flywheel between the world's second largest exchange and Mantle's DeFi ecosystem isn't something most L2s can replicate.

xStocks crossed $25B in transaction volume and $1B aggregate market cap globally by March 2026. The product has proven itself, it's just early on Mantle specifically.

Here's what's overlooked in most RWA coverage. No other Ethereum L2 has institutional credit, a tokenized crypto index, and tokenized equities all live simultaneously at meaningful scale.

The competition isn't really doing the same thing:

- Arbitrum: 2,000 RWA assets but fragmented across dozens of small issuers with no coherent single-chain narrative

- Base: growing retail distribution via Coinbase rails, not DeFi composability

- Stellar: going deep on TradFi compliance, a fundamentally different model altogether

Mantle's building the full stack and betting that composability does the rest.

The Bybit rails, ZK settlement for compliance-sensitive issuers, and a $2.4B treasury that actually convinces institutional issuers to show up rather than deploy elsewhere.

Blockstreet's integration should deepen xStocks liquidity meaningfully, more tokenized funds are coming, and the AI agent angle is genuinely underrated.

As agents need programmable yield-bearing collateral to operate autonomously, this stack starts looking less like a financial product and more like critical infrastructure.

Most chains are building one asset class. Mantle's building the venue.

h/t: @MessariCrypto for the Q1 2026 snapshot.

46

7

75

3,788

Mesh retweeted

Jun 9

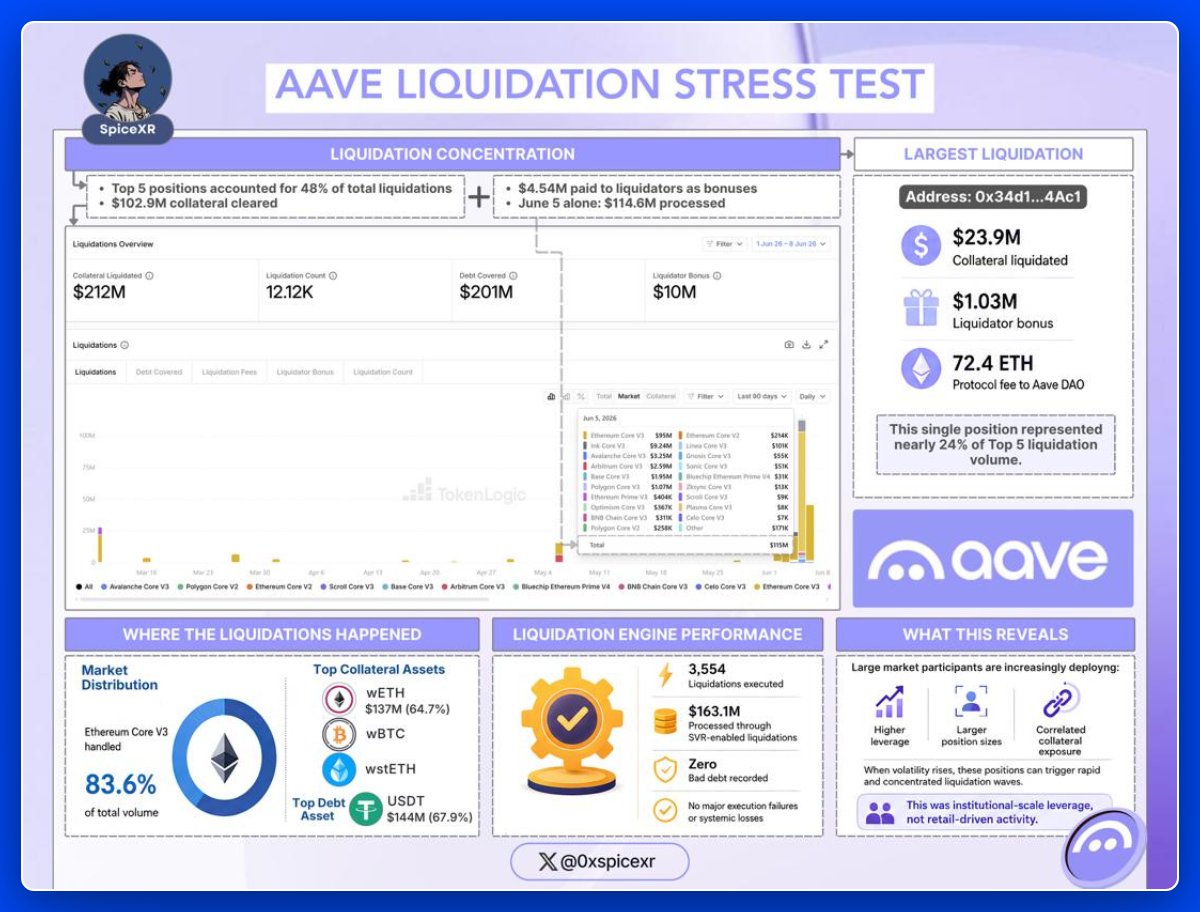

Over the past week, @aave processed $212.3 million in liquidations following a 20-30% market drawdown

The distribution of these liquidations reveals important details about current positioning. The top 5 positions alone accounted for 48% of total volume, clearing $102.9 million in collateral and generating $4.54 million in liquidation bonuses. June 5 stood out with $114.6 million processed in one day

This concentration points to a market where larger, more leveraged positions have become common

Breakdown Below 🧵↓↓

12

13

64

5,786

Mesh retweeted

Jun 8

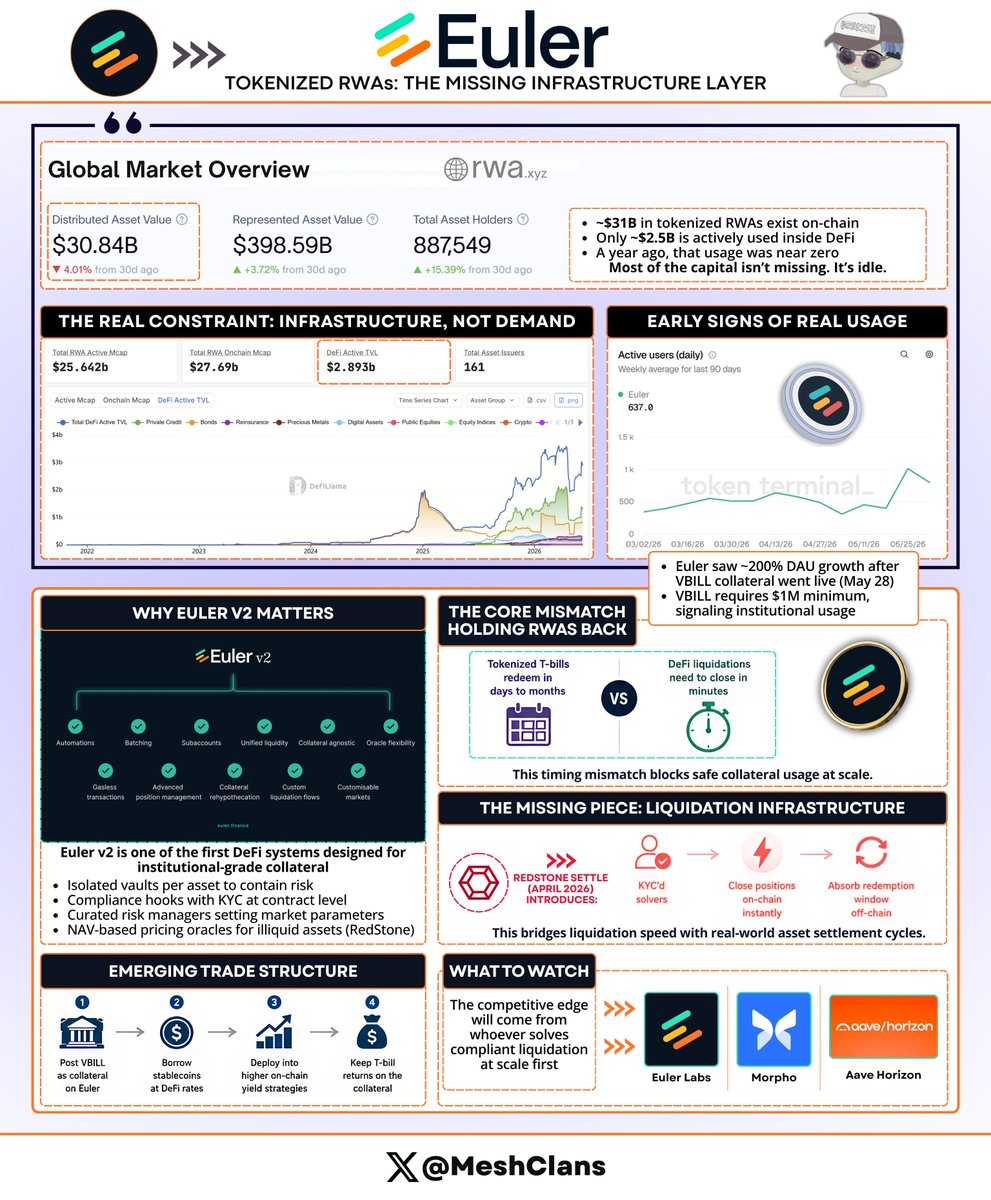

Everyone's tracking tokenized RWA numbers. Nobody's asking why ~$28B of it is just sitting there doing nothing.

~$31B in tokenized RWAs exist on-chain. Only ~$2.5B is actually working inside DeFi. A year ago that number was near zero.

The gap isn't demand. It's plumbing.

@eulerfinance's daily active users more than doubled in the weeks after VBILL went live as collateral on May 28 - roughly 200% growth per @tokenterminal's 90-day chart.

Not every new address is automatically an institution, but this is clearly not a retail-native setup either. VBILL has a $1M minimum ticket on Ethereum, so the user growth around that market points to institutional capital finally finding useful DeFi rails.

Euler v2 was quietly built for exactly this. A lot of DeFi infrastructure couldn't handle it until now:

- Isolated vaults per asset so one bad market can't touch the rest

- Compliance hooks enforcing KYC access at the contract level

- Curated risk managers (KPK) setting parameters per market

- Daily NAV oracles from RedStone pricing illiquid collateral

→ Here's the part that should bother you.

Tokenized T-bills carry redemption windows ranging from days to months. DeFi liquidations need to close in minutes.

That mismatch quietly limited every serious attempt at RWA collateral before this cycle, and almost nobody talked about it.

@redstone_defi Settle launched in April 2026 to fix it. KYC'd solvers close positions on-chain instantly and absorb the redemption window themselves off-chain.

Unglamorous work. Without it none of this holds together.

Tokenization didn't solve the collateral problem by itself. The liquidation layer is what starts making it usable.

The trade structure worth understanding:

- Post VBILL as collateral on Euler

- Borrow stablecoins at DeFi rates against it

- Deploy into higher on-chain yield strategies

- Keep T-bill returns on the collateral the whole time

Positive carry as long as your DeFi yield clears T-bill rate plus borrow cost. When that spread starts closing, the DAU chart moves before anyone writes about it.

RWAs were supposed to be a yield story. They're becoming the collateral layer for institutional DeFi and most people still haven't clocked the difference.

The $28B sitting idle isn't a tokenization failure. It's an infra gap that's barely started closing.

Euler, Morpho, and Aave Horizon are the three setups worth watching. Which one figures out compliant liquidation at scale first?

47

7

93

5,749

Mesh retweeted

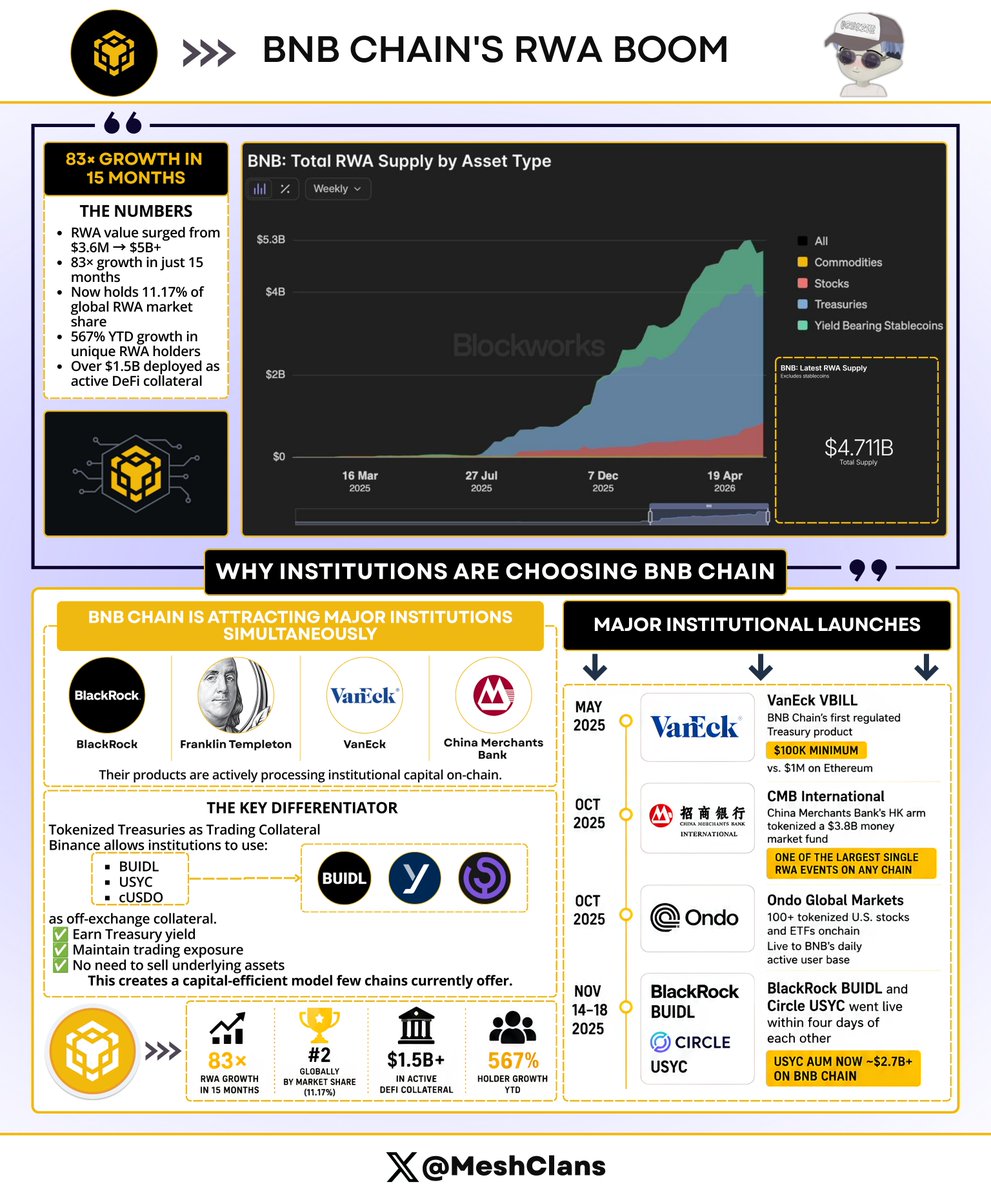

Jun 7

I've been tracking the RWA space for a while now, and BNB Chain's numbers just broke something I thought I understood about how institutional capital picks infrastructure. $60M to peaks over $5B in roughly a year. 83x.

BlackRock, Franklin Templeton, VanEck, and China Merchants Bank are all processing institutional capital on BNB Chain simultaneously right now, and most of the crypto space is still sleeping on why.

@binance started accepting tokenized Treasuries (BUIDL, USYC, cUSDO) as off-exchange collateral for institutional clients. An institution can now hold a Treasury product, earn yield on it, and keep trading positions fully active without touching the underlying asset.

Nothing on Ethereum or Solana combines the Binance distribution, off-exchange collateral rail, and RWA liquidity loop at this scale.

Imo that single mechanic is more consequential than anything else happening in RWAs right now, and the market hasn't priced it correctly yet.

Six months of institutional launches completed the picture:

- VanEck VBILL (May 2025), BNB Chain's first regulated Treasury product, $100K minimum vs. $1M on Ethereum

- CMB International (October 2025), China Merchants Bank's HK arm tokenized a $3.8B money market fund, one of the biggest single RWA events on any public blockchain

- Ondo Global Markets (October 2025), 100 U.S. stocks and ETFs onchain, live to BNB's daily active user base

- BlackRock BUIDL and Circle USYC both went live November 14–18, within four days of each other; USYC alone has since grown to ~$2.7B in AUM on BNB Chain

Here's the interesting part

11.17% global RWA market share, 567% YTD growth in unique holders, fastest of any tracked chain this year.

Over $1.5B of those RWAs sitting inside DeFi protocols as active collateral, with hundreds of millions borrowed against them. Everyone obsesses over TVL but holder growth is also the number that separates a real ecosystem from a concentrated bet.

567% YTD means the adoption base is widening, not just getting deeper with the same whales.

Millions of daily active users (2.4M–3.4M), sub-second finality, fees at 0.05 gwei. Institutional-grade products at price points that don't shut out the geographies tradfi spent decades ignoring.

Redemption liquidity at scale and cross-jurisdictional regulatory clarity are still open questions, but the capital flowing into @BNBCHAIN right now is not speculative - it's structured institutional money that's compounding.

BNB went from a trading chain to an institutional on-ramp for geographies that U.S. markets never reached. Two years ago that sentence would've sounded ridiculous.

Now BlackRock and China Merchants Bank are both live on it.

TL;DR: 83x growth, #2 globally, $1.5B in active DeFi collateral. Track the holder growth, not the TVL numnerss.

That's where this story goes next.

cc: @cz_binance @nina_rong

27

1

61

1,202

Mesh retweeted

Jun 5

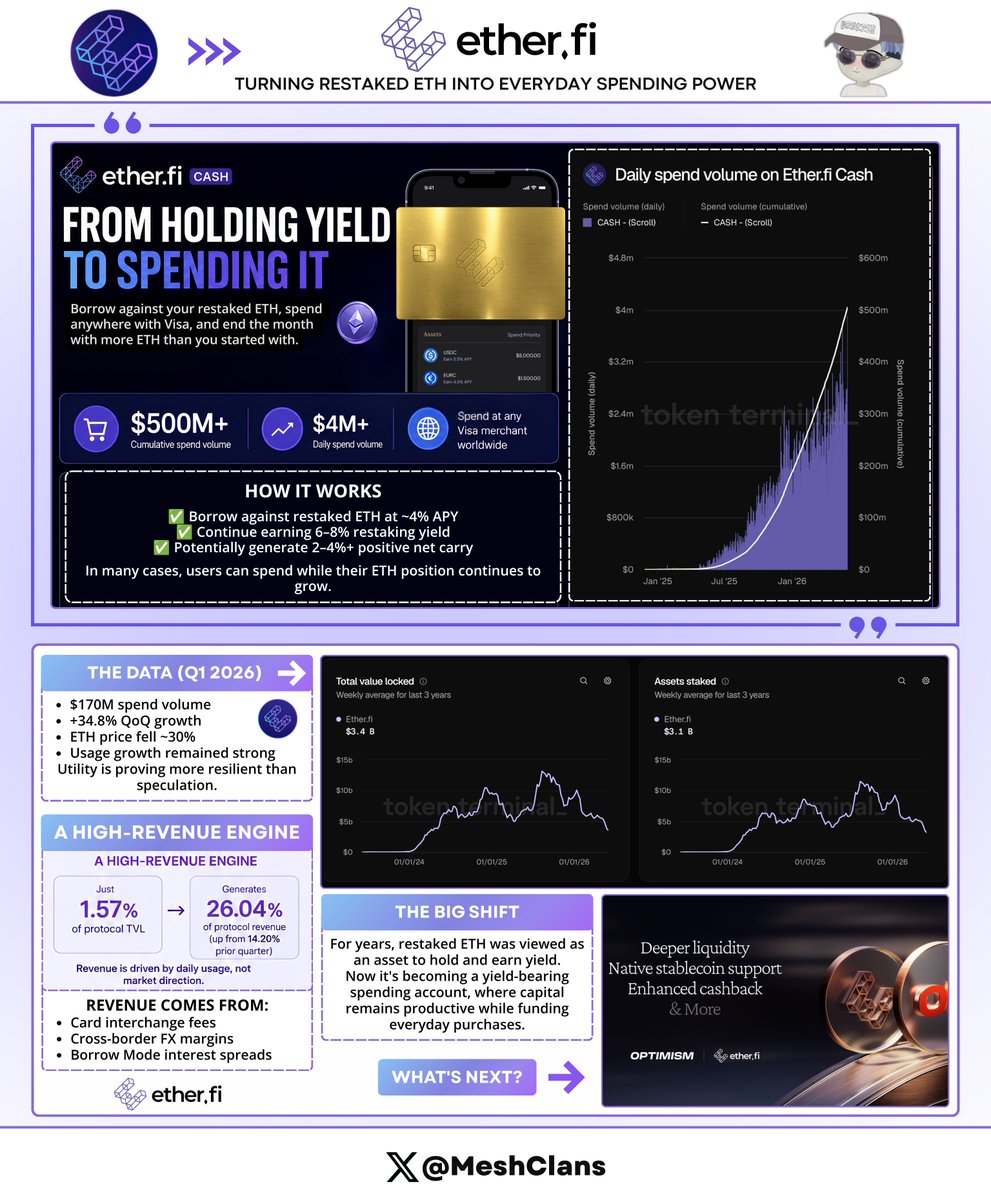

You can now borrow against your restaked ETH, spend it at any Visa merchant worldwide, and end the month with more ETH than you started with.

Etherfi Cash just crossed $500M in cumulative spend volume, with daily spend hitting $4M . But the real story isn't the volume, it's the behavioral shift underneath it.

People aren't selling their ETH to spend. They're borrowing against restaked ETH at 4% APY while the collateral keeps earning 6–8% restaking yield.

Depending on strategy and market conditions, that's often 2–4% in positive net carry, meaning you're effectively being paid to spend. Most people haven't clocked how significant that is.

DeFi has been theorizing about this moment for years. It's now showing up in the data.

Per @tokenterminal Q1 2026 data:

- $170M in spend, up 34.83% QoQ

- ETH price down ~30% that same quarter

- Growth fully decoupled from price action

Products built on speculation collapse when price does and the ones built on genuine utility keep compounding. Spend volume hit a quarterly record during one of ETH's worst quarters, and the product has found real traction.

The revenue structure underneath tells the same story. Cash holds just 1.57% of etherfi's total TVL but generates 26.04% of total protocol revenue, up from 14.20% the prior quarter.

A tiny slice of the capital base producing more than a quarter of all protocol revenue, through daily transaction frequency, not passive yield spread:

- Every swipe earns interchange for the protocol

- Every cross-border transaction earns FX margin

- Every Borrow Mode purchase earns interest spread for the protocol on the user's credit balance

None of that requires ETH to go up. The revenue is tied to how often people spend, not where markets close.

TradFi lived through this exact transition when money market funds evolved from institutional instruments into mass-market products. Fidelity layered a spending interface on top of a yield instrument and made the yield invisible, a checking account with yield running in the background.

It opened an entirely new market. @ether_fi Cash is the same playbook for restaked ETH, except the yield layer is onchain, non-custodial, and composable in ways Fidelity's infrastructure never was.

For three years, weETH and eETH were assets you held and watched compound. The mental model was fixed: yield is income, not spending power.

That mental model is breaking down in real time.

The OP Mainnet migration signals the next phase:

- Sub-cent transaction fees

- Deeper liquidity

- Travel and lounge perks across card tiers

- Native stables and higher-tier rewards already in motion

Restaked ETH functioning as a yield-bearing checking account was always the thesis. $500M in cumulative spend is what the thesis looks like when it starts working.

The shift from holding yield to spending it isn't a product update. It's a new financial primitive.

cc: @KoppKnows @MikeSilagadze @crypto_linn

28

2

51

1,677

Jun 4

What happens when governance shifts from digital protocols to living cultural assets?

Traditionally, collectors faced a binary choice:

> Own the collectible outright

> Or don’t own it at all

Almost no middle ground existed.

@MarketCardsHQ introduces a powerful third path: collectively govern the collectible

Suddenly, ownership isn’t just about economic exposure. It becomes real participation in shaping the destiny of a tangible cultural asset.

Decisions that once sat solely with one wealthy collector now belong to the community

➵ Should the card get graded?

➵ Is it time to sell?

➵ Is this offer actually attractive?

➵ How do we manage and preserve its long term value?

This creates a fascinating convergence of three worlds that rarely intersect so cleanly:

🔸 RWAs ➾ because a physical asset sits at the foundation.

🔸 Collectibles ➾ where value flows from rarity, cultural weight, player legacy, and pure collector heat.

🔸 Onchain Governance ➾ where holders actually coordinate and vote instead of deferring to a single owner

Imo, what makes this truly compelling is that governance is no longer stuck governing protocols. For years, crypto governance has mostly revolved around treasury, token emissions, and parameter tweaks

Here, it’s governing culture

That changes the emotional dynamic completely. Tbh, people aren’t voting for yield farming or token incentives. They’re voting because they care:

🔸 This card deserves to be graded.

🔸 The player’s trajectory is about to explode.

🔸 This offer undervalues its historical significance.

🔸 This piece of culture matters

The decision making becomes equal parts financial discipline and cultural intuition. It feels more human

And the timing couldn’t be better. With the World Cup in full swing, @MarketCardsHQ is launching its first batch of soccer cards. This is your moment to put your football knowledge where your mouth is

If you have a favorite player or strongly believe a certain national team will win it all, you can actually back that conviction on the platform

When a player lights up the tournament, their card’s value tends to rise with them. You can trade tokens backed by real, physical assets instead, no need chasing meme coins

The crown jewel in this drop is something special: a true one-of-one card featuring three Argentinian football legends together, each with original autographs

This is the level of rarity we’re talking about. The first phase includes 68 football cards, and every single one is a one-of-one, the only example of its kind in the world

Many serious collectors refuse to let pieces of this caliber go, which is exactly why fractionalization and collective governance feel so powerful here

Personally, I love this approach. It opens up ultra-rare cultural assets to more people while letting the community steer their future

At that scale, you’re not just building another collectibles marketplace. you’re building governance infrastructure for cultural assets themselves

That’s the part worth exploring most deeply. It doesn’t feel like another tokenization play. It feels like a genuinely fresh idea with real legs

32

1

67

2,788

Jun 3

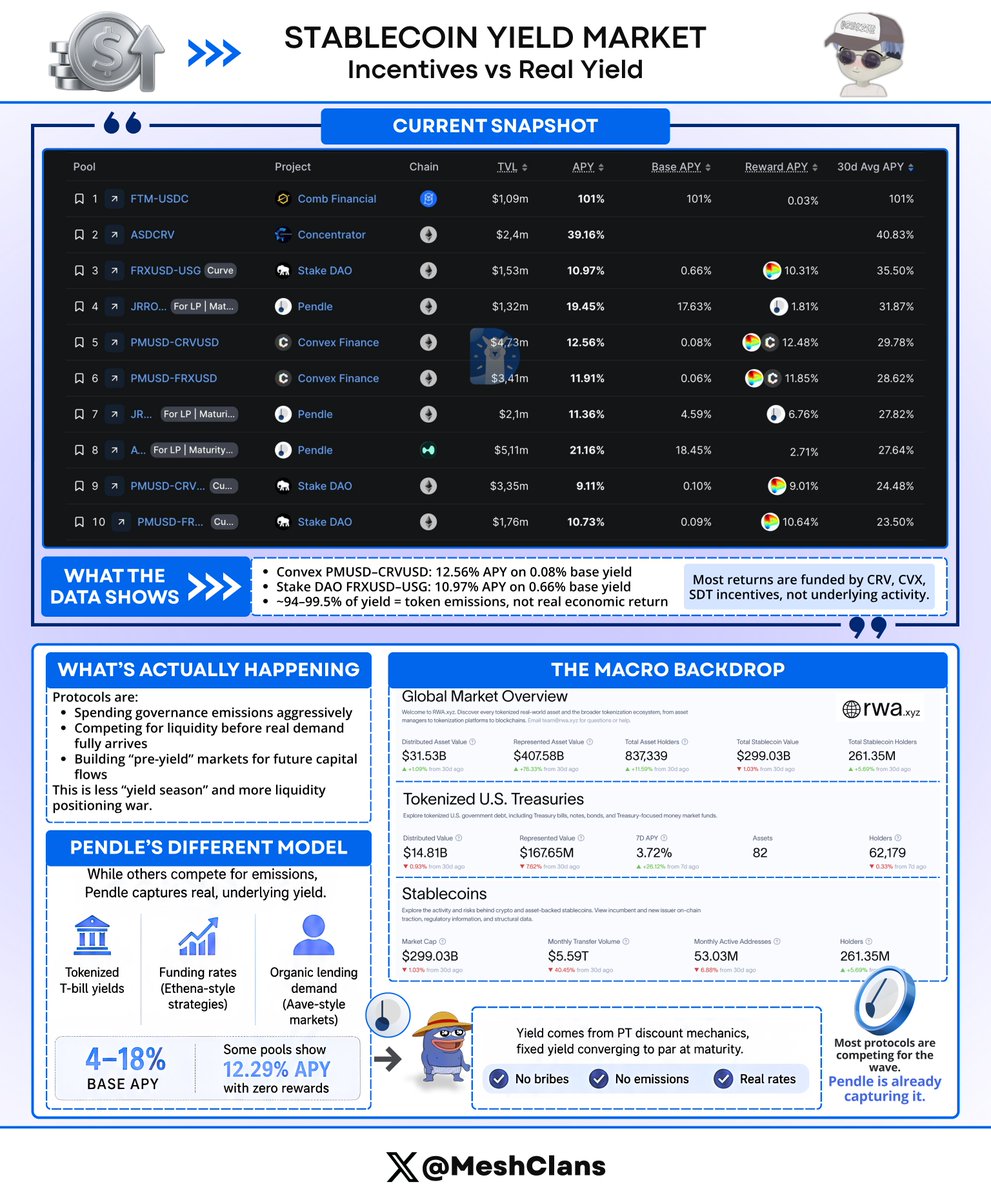

Stablecoin yield is heating up again, with Pendle, Convex, and Stake DAO all pushing 20-40% APY across their pools. Most people are taking the numbers at face value.

I think that's the wrong read.When you actually pull the data apart, the picture looks very different.

As of recent data, Convex's PMUSD-CRVUSD pool is at 12.56% APY on a base yield of 0.08%, and Stake DAO's FRXUSD-USG pool shows 10.97% APY on a base yield of 0.66%. So 94–99.5% of what's being advertised isn't yield from real economic activity.

It's CRV, CVX, and SDT emissions being pumped into pools to attract capital that protocols don't yet have organically.

Not yield season. Protocols making a forward bet, spending aggressively today on demand they believe is coming tomorrow.

And honestly? I think they're right. Just look at what's building underneath.

- RWA tokenization just crossed $30B, with tokenized US Treasuries now in the $8.7B–$14B range. In Q1 2026, they grew faster than stablecoins in absolute dollar terms for the first time ever.

- Yield-bearing stablecoins like sUSDe, USDY, and sUSDS are expanding fast, creating real organic yield floors inside DeFi pools that simply didn't exist during the last incentive cycle

- The stablecoin market is at $299B–$320B with holder count up 5.86% in just 30 days, with more capital looking for a productive home every week

- The veToken bribe economy is running full throttle. Convex controls roughly 50% of all veCRV, Votium has distributed $100M in cumulative bribes, and weekly CRV emissions are at approximately 5M CRV, with real directed capital competing for the same pools

These protocols aren't guessing. They're putting serious money behind a bet most people haven't fully priced in yet.

The bet only pays off if the demand wave arrives at scale. Right now, it hasn't. Not fully.

That's where @pendle_fi is doing something most people are missing.

While everyone else is fighting over emissions and bribe market positioning, Pendle's LP pools are generating 4-18% base APY from actual underlying rates. T-bill yields from tokenized treasury instruments.

Ethena funding premiums from delta-neutral positions. Aave lending rates, real borrowing, real demand and real fees.

There's one live pool rn carrying 12.29% APY with literally zero reward component. No governance token or bribe market. Just real yield.

That comes entirely from the PT discount mechanism, fixed yield locked in at purchase and accruing toward par at maturity. PT pools do expire and capital rotates into new ones, but that's just how fixed income works, not a weakness.

And yes, as with anything in DeFi, smart contract and market risks are real.

Pendle's own metrics make the case:

- $5.8B average TVL in 2025, up 79% year over year

- $47.8B in trading volume, up 36.5% year over year

- $40M in annualized revenue from actual swap fees, not token inflation

Most protocols right now are competing for the wave. Pendle is already capturing it.

Here's the lens worth keeping: next time you see a pool flashing 20% , the first question isn't "how do I get in." It's "what's the base yield?" That number tells you whether you're looking at real yield or a protocol's bet on future demand.

One of them already built the infrastructure that wins.

37

1

55

1,551

Mesh retweeted

Jun 1

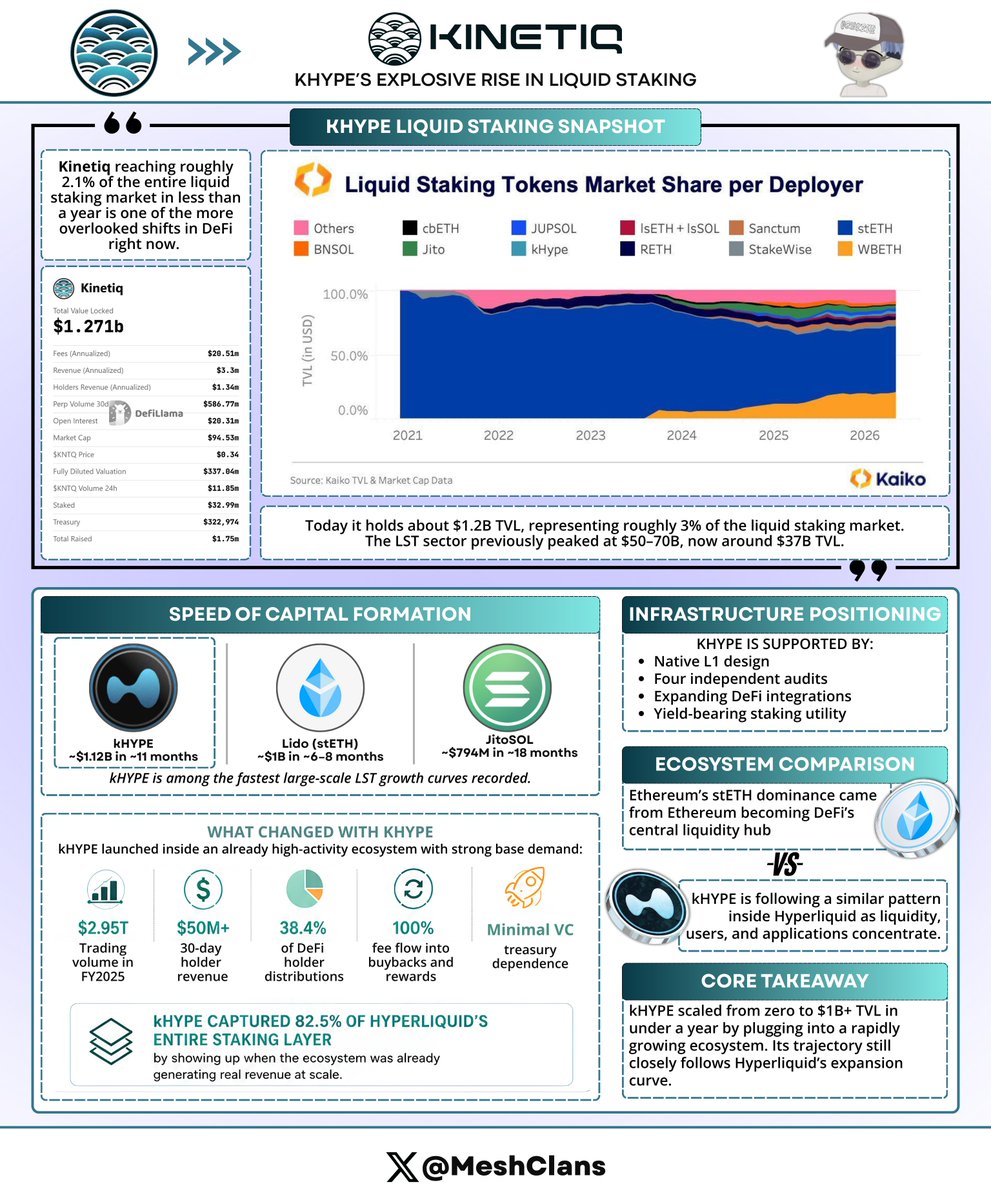

Eleven months ago, kHYPE didn't exist. Today it holds ~3% of the entire liquid staking market.

a market that recently exceeded $50-70B at peak, now sitting at ~$37B after market cycles, with kHYPE at $1.12B TVL throughout.

Per the @Kaiko chart, that teal slice appearing in the 2025-2026 frame isn't noise. It's TVL built faster than any LST in history, and most people still aren't talking about it.

Here's the thing though, that number is genuinely hard to earn. Lido took 6-8 months to hit $1B TVL from a cold start, and Jito took ~18 months to approach comparable numbers on Solana.

LST dominance doesn't get handed out. You earn it through:

- Liquidity depth

- DeFi integrations

- User trust compounded over years

stETH ran through Aave, Curve, and MakerDAO before it ever looked inevitable, and that moat still defines the market today.

In absolute dollar terms, kHYPE (~$1.12B TVL) already holds more than JitoSOL (~$794M), a protocol live since late 2022. The speed differential isn't marginal.

kHYPE compressed years of trust-building into months by launching directly into Hyperliquid's existing momentum.

So what actually happened? Honestly, this isn't really a story about @Kinetiq_xyz . It's a story about what happens when a protocol launches on top of one of the fastest compounding machines in on chain finance:

- $2.95 trillion in trading volume in FY2025

- Recent 30d holder revenue exceeding $50M, 38.4% of all DeFi holder distributions, highest of any protocol

- Bootstrapped with minimal strategic funding and no large VC treasury, with 100% of protocol fees going back to buybacks and community rewards

kHYPE captured 82.5% of Hyperliquid's entire staking layer by showing up when the ecosystem was already generating real revenue at scale.

Of course, as with any LST, smart contract and ecosystem concentration risks exist, but Kinetiq's native L1 design and four independent audits give it a credible base to build from. It continues to deliver strong yields and deep integrations, making it a serious option for both retail and institutional participants.

The LST market reflects the ecosystem behind it, always has. stETH didn't win on product alone.

It won because Ethereum DeFi became the center of gravity for the entire industry, pulling in capital, developers, and composability that no other chain could match at the time.

What's playing out with kHYPE rhymes with that story in ways I don't think most people have priced in yet.

Ethereum sits at ~47% LST penetration of all staked ETH. Hyperliquid isn't anywhere close to that. If it scales toward $20-50B TVL at even 15-20% penetration, kHYPE's addressable market moves to $3-10B from ecosystem growth alone, before any HYPE price appreciation.

Two vectors that haven't meaningfully contributed to those numbers yet:

- The institutional pathway through iHYPE, backed by IMC Trading and Flowdesk

- The full composability buildout on HyperEVM

Eleven months ago this protocol didn't exist. Today it's sitting on a compounding curve that hasn't found its ceiling, and I genuinely think this is the most underread chart in DeFi right now.

At what point does kHYPE start mattering to the ETH liquid staking narrative?

cc:@0xOmnia @0xmagnus @mektigboy @smartestmoney @chiefkeith1000

40

2

56

1,841