Ph.D. Economist & Global Macro veteran (20 yrs). Applying institutional rigor to the under-analyzed microcap space. Focused on Energy, Mining & Infrastructure.

Joined May 2026

- Tweets 36

- Following 60

- Followers 337

- Likes 11

Photos and videos

$GEODF / $GEO.TO is the kind of small-cap setup where one ugly quarter can make the chart look broken while the actual asset value story gets better.

No doubts, Q1 was bad. Margins compressed, EBITDA fell, and the headline numbers looked ugly. But I don’t think this was a demand-collapse quarter. It looks much more like a lumpy execution / labor-cost / contract-timing quarter in a business that is inherently uneven.

The key point: the labor contracts that pressured the quarter have already been renegotiated. If that is right, then Q1 is probably not the new run-rate.

What I care about more:

✅Geodrill owns a hard-asset drilling fleet that is expensive to replace

✅Replacement value is likely well above accounting book value

✅The company trades around/below NAV depending on how you mark the fleet

✅Gold/copper exploration activity remains supportive

✅Management has now announced a buyback

✅Insider alignment is unusually strong

✅A strategic sale is a real possibility over time, not a fantasy

The buyback matters. This is not a SaaS company buying back stock at 40x revenue to manage dilution. This is an asset-heavy drilling business buying stock at what looks like a discount to replacement value. That is exactly when buybacks make sense.

The market seems to be treating $GEODF like a busted earnings story. I think it is more likely a lumpy asset-value story where a bad quarter created a better entry.

The next proof point is simple: Q2 margins and utilization need to rebound. If they do, Q1 was noise. If they don’t, then the labor/timing explanation weakens, and I’ll have to revisit the thesis.

But at today’s valuation, I think the setup is attractive:

Hard assets metals cycle renegotiated labor buyback insider alignment potential strategic value.

Credit to @MoneyMarkStocks for the stellar work here. His replacement-value framing is the reason I spent more time on this instead of treating it like just another bad microcap quarter.

Disclosure: I am long $GEODF / $GEO.TO and may add, reduce, or sell at any time without notice. Not investment advice. Do your own work. Small caps are volatile and can be illiquid.

1

5

661

Jun 12

$KLNG I agree with @realLigerCub's read — grounded in the same public data anyone can pull.

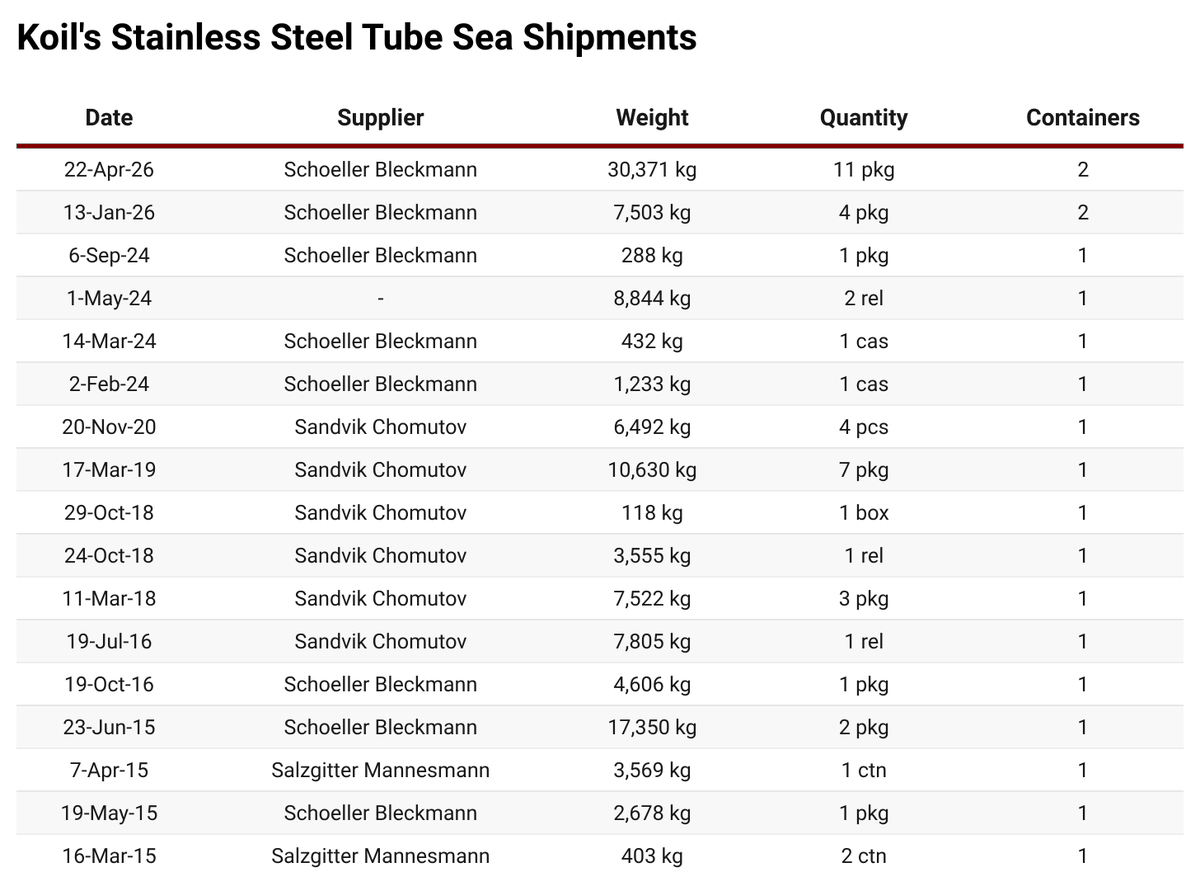

Yesterday, Koil Energy announced a major project award — subsea umbilical handling, spooling & storage — deploying a newly acquired 3,500-MT mobile offshore carousel funded by last month's $5M credit facility, which then won its first contract within weeks. A non-dilutive rental flywheel executing in real time.

The alternative data underneath is the louder signal. Customs / bill-of-lading records show a record 30,371 kg seamless stainless-steel tube shipment landing in Houston on Apr 22, the largest in Koil's 11-year import history, sourced from premium Austrian umbilical-tube maker Schoeller Bleckmann. 2026 YTD tube imports already run ~3.5x all of 2024. You don't import that much subsea-grade tube unless you're building to ship.

That lines up with Q1: revenue 56% YoY, a return to profitability, and fixed-price product revenue doubling as the product cycle turns.

$KLNG remains attractively valued at around 1.3x EV/sales vs a subsea peer set near 6.5x. The market is paying component-supplier prices for a company repositioning as an integrated subsea-systems provider.

A few fair caveats that matter: Koil doesn't disclose contract values, so any dollar figure is third-party inference, not company-confirmed. One strong quarter of margin recovery isn't a trend; Q2 has to back it up. And it's a thin OTC micro-cap; liquidity cuts both ways. Not investment advice.

Jun 12

Yday, $KLNG announced its first major order since Aug 2025. Based on shipping records and third-party supply chain data, the market is likely underestimating the value of the Aug 2025 order by more than 2x.

2

303

Jun 11

My new piece: Shorting Microcaps Without Getting Killed 🐻💀

Most short write-ups are victory laps. The reality is harsher. The sad truth is that in microcaps, spotting the overvalued junk is the easy part, as the market's full of it. The hard part is everything between "this is obviously worth less" and "I actually made money being right."

First, the question everyone asks: can't you just hedge the microcap risks with an inverse ETF? The fans of this thesis have a fair point — when you're wrong, the position shrinks instead of growing: no squeeze, no margin call, capped loss. But that exact feature is the flaw. The daily reset that cushions your loss in a steady drop bleeds you in choppy tape, and small caps are nothing but chop. And any index hedges the wrong risk: what takes your face off in a microcap book is one surprise dilution, not a broad selloff — while shorting the microcap index itself (IWC) is a non-starter, too thin and illiquid to lean on. There's no carry-free way to hold a hedge anyway: everyone charges rent.

That's the warm-up. The real meat — the six kinds of shorts ranked by how tradeable they are, the three gates every trade has to clear, and four of my own shorts (two wins, two losses) are in my guest post for @MSmicrocaps. The sharpest ideas in this one were sharpened in conversation with @majgeoinvesting and @DeepSailCapital — grateful to both. More to follow.

Read it here 👉 mscliffnotes.substack.com/p/…

1

7

1,832

Dr Microcap retweeted

Jun 11

Round Table Skull Session with @DeepSailCapital @Pixelresearch_ @MicrocapDr, Shorting & Squeezes.

"I've had plenty of shorts that have worked out over time, but when I go back and do all the math, I realize I actually lost money because I paid so much borrow on the position."

skullsessions.video/p/why-gr…

1

7

12

5,241

Dr Microcap retweeted

Jun 10

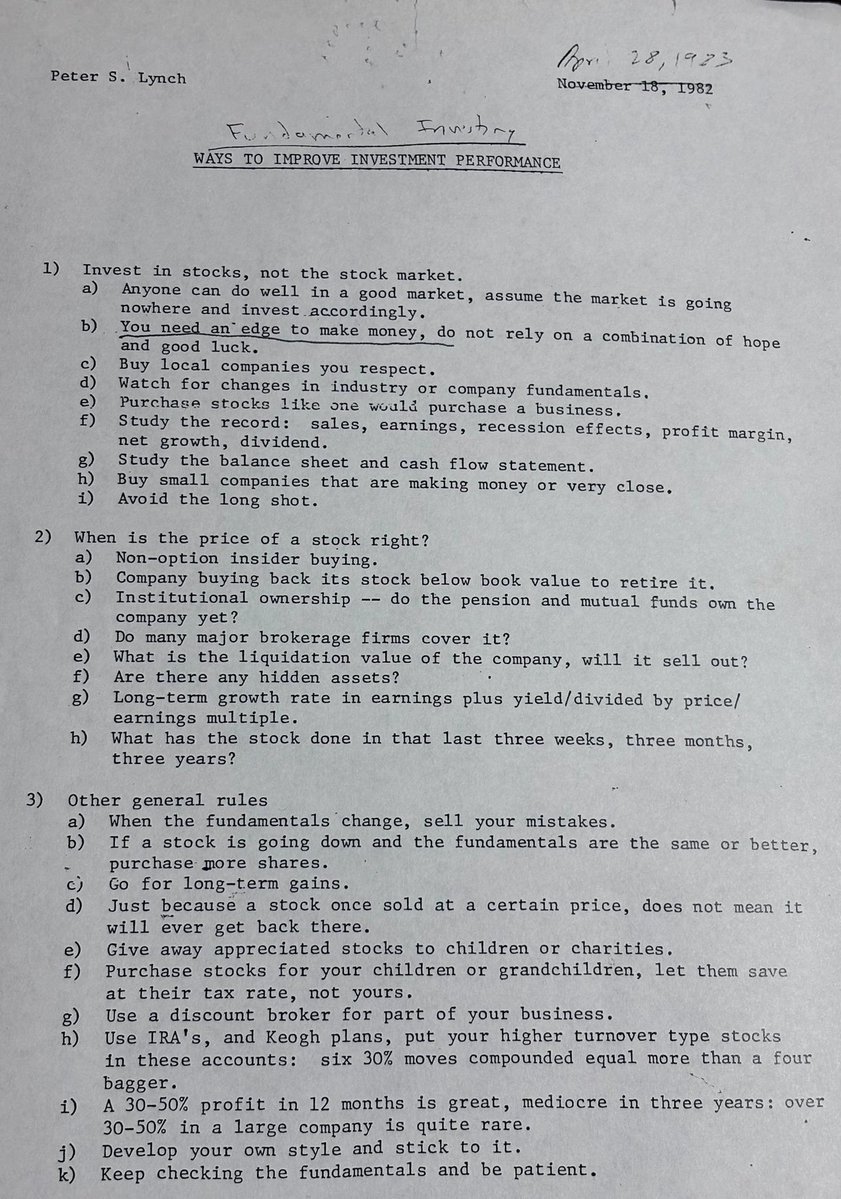

I was 26 years old when Peter Lynch handed me this.

April 28, 1983. I was the auto and retail analyst at Fidelity.

Peter was in his prime, on his way to building the greatest mutual fund track record in history:

29.2% annual returns for 13 YEARS STRAIGHT, growing Magellan from $18 million to $14 billion. The Babe Ruth of investing.

I'm looking at the principles he had typed up on a single sheet of paper that I've kept in my files for 42 years and I believe now is the perfect time to revisit them again.

Let me walk you through a few:

Rule 1B: "You need an edge to make money. Do not rely on a combination of hope and good luck."

Today's retail investor has no edge. He has Reddit, Robinhood, zero-DTE options and a TikTok algorithm pushing him into whatever stock just ripped 200% the day before.

That's hope and good luck wearing a fancy costume.

Rule 1E: "Purchase stocks like one would purchase a business."

Tesla trades at over 360 times earnings on a business deteriorating in real time, Oracle has $206 billion in liabilities against $39 billion in equity, MicroStrategy is a leveraged Bitcoin holding company priced like a software firm, and don't even get me started on SpaceX, that piece of garbage you'll be able to trade tomorrow...

Nobody in their right mind would buy these as actual businesses. They buy them as stories, narratives, and lottery tickets.

Peter would have called it the same way I do - these are not investments. They are speculations. GAMBLING.

Rule 1G: "Study the balance sheet and cash flow statement."

The hyperscalers spent over $380 billion on AI capex in 2025. Goldman says the measurable productivity payoff does not arrive until 2027 at the earliest.

Oracle just reported NEGATIVE $23.7 billion in free cash flow for fiscal 2026 while borrowing at a pace that would make a leveraged buyout firm nervous. The cash flow statements are screaming but nobody is reading them.

Rule 1I: "Avoid the long shot."

This one cuts the deepest.

The entire market has become a long shot.

OpenAI is projected to post roughly $74 billion in operating losses in 2028 ALONE while priced for transformation tomorrow. Bitcoin treasury companies are multiplying off thin air.

The retail investor of 2026 is making one long-shot bet after another and calling it a portfolio.

Rule 3A: "When the fundamentals change, sell your mistakes."

Tesla's fundamentals have changed.

California registrations are down 24% year over year and inventory days went from 10 to 27. Musk himself admitted on the last earnings call that Hardware 3 cannot achieve unsupervised FSD, breaking a promise made to 4 million customers.

The fundamentals have screamed change. But the stock is still at $385.

The mistakes are not being sold. They are literally being doubled down on with leverage.

Rule 3I: "A 30-50% profit in 12 months is great. Mediocre in three years."

Today's retail crowd expects 30-50% in a WEEK. Then they wonder why they get wiped out the second the hype stops.

And my favorite - Rule 3J: "Develop your own style and stick to it."

That is the entire game right there.

I developed mine sitting across the hall from Peter Lynch in 1983, watching him work, reading his notes, getting my own research handed back to me covered in his pencil marks. Then in 1984, my first full year managing money, I ran the #1 mutual fund in America. The Fidelity Overseas Fund was top 2 for the next six years running.

I did not get there by chasing narratives. I got there by following the sheet of paper you are looking at right now.

42 years later, this single page contains more wisdom than every Fintwit thread, CNBC segment, and Wall Street price target combined.

Peter retired in 1990 with the greatest mutual fund record in history. Then he sat down and wrote books explaining exactly how he did it.

Only a few "investors" these days read them.

And almost nobody is reading the balance sheets, the cash flow statements, or studying actual businesses today either.

They are chasing AI, crypto, and whatever pumped yesterday.

The wisdom on this page is timeless and it's more important than ever.

51

302

1,501

231,405

Jun 9

$PPIH is exactly the kind of small-cap selloff I try not to overreact to.

The headline Q1 looked ugly because EPS and net income were down hard, and the market treated it like a thesis break. I don’t think that is the right read.

This was a messy project-timing, mix, and ramp-cost quarter, not a demand problem.

The issues behind this lumpy quarter were specific and anticipated: MENA timing delays, product mix, Canada seasonality, Ohio/Qatar ramp costs, and higher SOX/professional expenses. Annoying, yes. But not the same as customers walking away or the market disappearing.

The key details I care about:

✅Backlog increased to $136.5M

✅Management said no projects were cancelled

✅They still expect FY26 revenue and net income growth vs FY25

✅Backlog includes contributions from AI/data center projects in North America

✅Ohio facility ramp gives them better U.S. capacity at a time when data center, district energy, and engineered infrastructure demand is accelerating

That last point matters. $PPIH is not a generic pipe company. It makes engineered piping, leak detection, insulation, containment, anti-corrosion systems, and district energy infrastructure. Maybe boring but mission-critical stuff.

AI data centers are not just GPUs. They need power, cooling, thermal systems, water, redundancy, and infrastructure that actually works. $PPIH is one of the tiny public ways to get exposure to that physical layer.

The number I’m actually watching now is gross margin.

It went from roughly 36% to 29% this quarter because of ramp costs and mix. If gross margin recovers next quarter, the timing and ramp-cost explanation holds. If it does not, then “timing” quietly becomes “structural margin pressure,” and that, not demand, is what would change my mind.

I’m not pretending this is a smooth quarterly compounder. It is a lumpy project business. You have to underwrite backlog, execution, and margin recovery, not just one quarter’s EPS.

For now, I am treating the selloff as a chance to be patient, not a reason to abandon the thesis.

Disclosure: I am long $PPIH and may add, reduce, or sell at any time without notice. Not investment advice. Do your own work. Small caps are volatile and can be illiquid.

1

2

15

2,240

Jun 6

I see a lot of discussions on what's going on with $RDCM after the wild ride, so here's my take.

Radcom is a small Israeli software company that most people have never heard of. It quietly runs in the background of phone networks, helping carriers catch and fix problems before your calls ever drop. Boring, sticky, mission-critical. This is exactly the kind of infrastructure business that I like.

A couple of weeks ago, a big account on X mentioned it, the crowd piled in, and the stock shot up to ~$17. Then that same crowd got bored, wandered off, and it slid right back to ~$12. But had anything really broken?

I went digging through the actual SEC filings, and there was nothing there. No bad news, no cut to guidance, no insiders heading for the exits. It was just hype inflating and then deflating. The business itself didn't change at all.

Here's what makes it genuinely interesting once you look past the noise. Radcom is sitting on about $108M of cash with zero debt. That's roughly $6.35 a share — call it half the entire share price, just parked in the bank. Strip that cash out and you're paying almost nothing for a company that's profitable and still growing. For years, that pile sat there doing nothing, which is a big reason the stock stayed so cheap.

What changed is the part that matters: activist investors just took control of the board. These are people who want that cash actually put to work — a buyback, a special dividend, or, most interesting of all, selling the whole company. Businesses like this rarely come up, and the few that have sold went for rich prices. I see a material upside from here, and that giant cash cushion limits the downside while we wait.

It's not free money, of course. The company leans heavily on a handful of big customers (one is about half of sales), and there's always the risk the new board blows the cash on a bad acquisition instead of handing it back.

Net: I own a little, and I'd add on a weakness like this.

Huge credit to @FinSkeptic, whose work on Radcom is the best out there — if this interests you, go read him first.

Not investment advice, just me thinking out loud. I own shares and may buy more or sell the position without any warning. Do your own work.

1

3

18

1,363

Jun 4

Great @iancassel piece on letting your losers get smaller. One thing I'd add: shrinking a loser is the right default — but it's a default, not a law.

The Verdun trap Cassel describes — sunk cost, ego, wanting to be right more than wanting to make money — is what happens when you add to a loser on feeling. The cure isn't "never add." It's being brutally honest about whether you're acting on fresh conviction or defending an old decision. You earn the right to override the default only through rigorous research into the company. Sentiment, partial information, and "it should be working by now" don't count.

Two examples from my own book, pulling in opposite directions:

$VEEV: the market wanted to treat it as AI roadkill. My work said the opposite — not a company being disrupted by AI, but one positioned to benefit from it. The financials and independent expert coverage confirmed it. So I added. That's a legitimate override: I wasn't adding to be right, I was adding because the research said the thesis was getting stronger as the price fell.

$SPWR: I had genuine conviction here, anchored in TJ Rodgers' track record of building real businesses. But a deep look at the capital structure — plus conversations with investors I respect — told me to sell at a loss. That doesn't mean $SPWR fails. I just don't believe it works soon, and "eventually" carries an opportunity cost I'm not willing to pay.

The discipline cuts both ways. Sometimes the research tells you to add to the "loser." Sometimes it tells you to exit a name you still believe in. The one input that should never drive the decision is the price you paid.

Let your losers get smaller — unless you've done the work to earn the right not to.

Jun 4

New Article - Letting Your Losers Get Smaller

It takes just as much discipline to hold a winner as it does to not add to a loser.

microcapclub.com/letting-you…

5

704

Jun 3

D-BOX $DBOXF $DBO.TO just reported a milestone year 🎬

The company that makes motion-synced theater seats finally hit escape velocity. Revenue up 35%, profitability up 100% , and the high-margin royalty stream is growing 5x faster than the underlying box office. The writing is on the wall - they're winning share, not just riding a tide.

I'm focused on this latest print since the broader story is already well-covered by independent analysts like @BreakoutInvestr and @WolfOfOakville, so I am pointing you there for the full thesis.

The balance sheet doubled to C$17.6M cash (~US$13M) cash with virtually no debt. At ~11x EV/EBITDA, you're paying a perfectly ordinary multiple for a business in operating-leverage inflection.

The strategic tell: management is openly positioning to bankroll D-BOX installations at cash-strapped chains like AMC and Regal. 7 of the top 10 North American exhibitors are still untapped. That's the runway.

Risks worth owning: half the installed base sits at one customer (Cinemark), the slate cycle is real (last two quarters showed it), and liquidity is thin. The deferred tax recognition flatters reported earnings - normalize for it.

I'm long, sized small, and watching the next two prints.

Not investment advice. I hold a position and may add or trim without notice. Microcaps cut both ways — please do your own work.

2

11

1,042

Jun 3

When @nanalyzetweets speaks, I listen.

Jun 3

$SIVE

This stock is being pumped heavily by accounts that do nothing but pump stocks. The below press release does not reflect any revenue commitments but is basically just a PR piece coming from a firm that's understandably engaging in a money grab off the back of being pumped relentlessly. Buyer beware!

2

439

Jun 2

Very sharp.

My website shows the backbone of my strategy. The last 2 months were an outlier negative event for what I do.

1

1

411

Jun 1

Everyone says space stocks are a bubble. After three weekends rebuilding the models, I think most people are wrong about which ones.

It's not one bubble. It's two completely different things wearing the same costume:

🚀Rocket Lab is a real company priced for near-flawless execution.

🛰️AST SpaceMobile is the purest scarcity bubble in the group - a gorgeous idea that doesn't fully exist yet.

Most of the rest is just expensive growth that normalizes once you do the work. (Quantum stocks at 700x sales are far crazier than anything in space.)

A few things that surprised me:

🌕 Intuitive Machines screens "cheap." But the cheap was bought, not earned — the revenue came attached to an acquisition.

🌌 Sidus Space loses money on its revenue before paying a single salary. Negative gross profit. I literally couldn't plot it on the chart.

✅The kicker: at its rumored ~$1.75T price, @SpaceX would list cheaper - on sales - than @RocketLab, and a fraction of AST. The best house on the block, priced below the fixer-uppers.

That's the whole catalyst. Once you can finally buy the real thing, why keep paying up for the stand-ins?

History rhymes here too. Glencore, Rivian, Coinbase all rang the bell when the category king went public. But it's a pattern, not a law, and I lay out exactly what would prove me wrong.

I also walk through how a careful person would actually play this. Hint: not by shorting these naked into a squeeze but with the real option structures, the borrow data, and the charts.

Full breakdown, free to read:

open.substack.com/pub/microc…

1

360