Discussing all things data center-centric - AI, power, colocation, cloud, and development of the infrastructure that will support it all.

Joined July 2024

- Tweets 1,149

- Following 68

- Followers 180

- Likes 10

406 Photos and videos

Jun 12

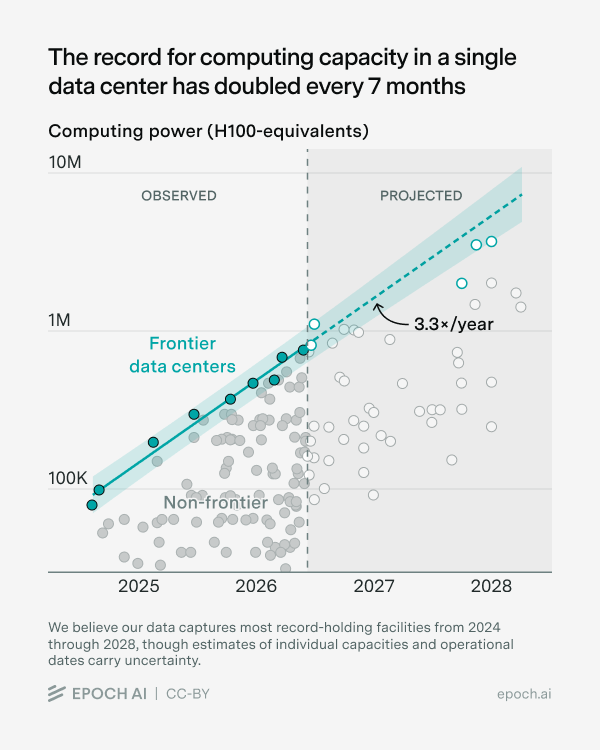

The record for computing capacity in a single data center has doubled every 7 months.

Epoch AI's data shows frontier facilities scaling at 3.3x per year in H100-equivalent compute. The largest facility operating today will look mid-tier by 2028.

The debate about overbuilding misses the point.

Hyperscalers aren't building for today's workloads. They're building for a demand curve that has made every prior estimate look conservative.

A data center designed to 100kW per rack in 2024 may be architecturally inadequate for frontier AI workloads by 2027. The physical decisions being made today have to account for compute density that doesn't exist yet.

The 7-month doubling cycle is the number every developer, investor, and infrastructure architect should have front of mind right now.

34

Jun 10

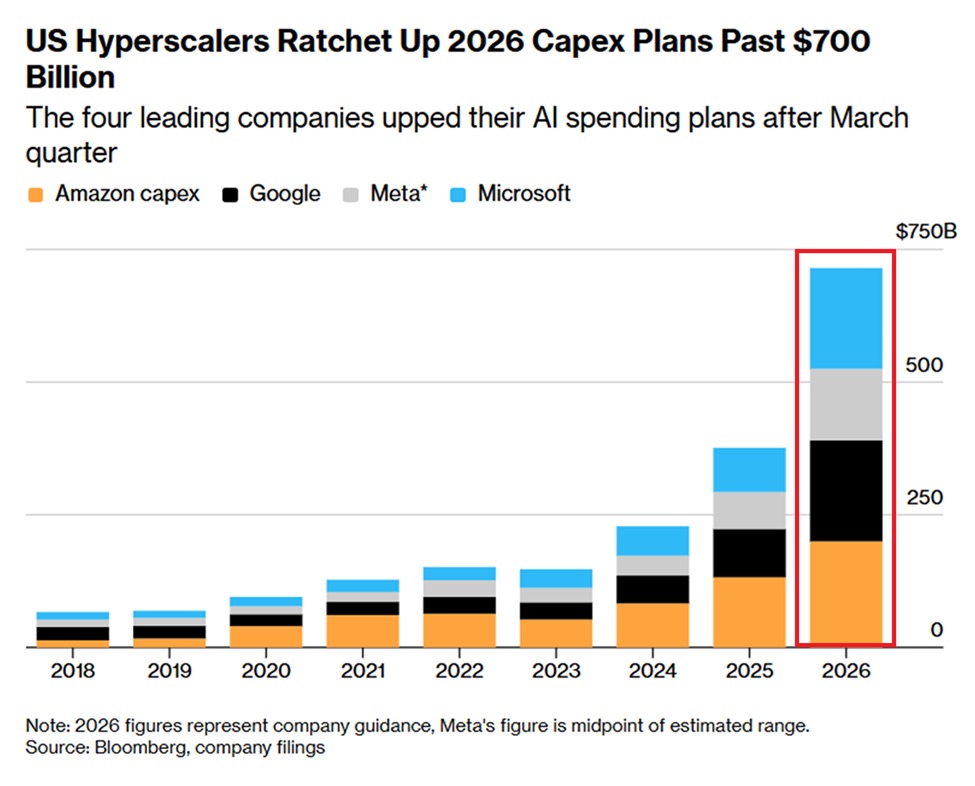

Every quarter analysts call for a pullback, the number goes higher.

The four leading hyperscalers just updated 2026 capex guidance past $700 billion, after already revising it up post-Q1 earnings.

Amazon ~$105B

Google ~$75B

Meta ~$65B

Microsoft ~$200B

Their combined capex in 2018 was ~$50 billion. They are now deploying that in a single month.

All four raised guidance again after Q1. That's a structural commitment decoupled from quarterly revenue performance. The AI infrastructure buildout is being funded as if capex is non-discretionary.

The constraint is execution capacity across every layer of the supply chain.

47

Jun 10

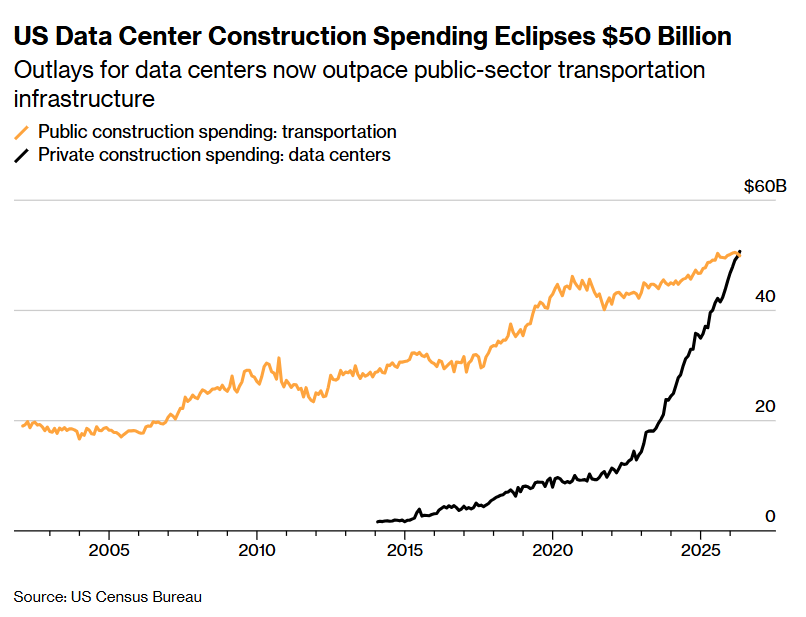

Private data center construction is starting to look less like real estate and more like national infrastructure.

This chart shows private data center construction spending overtaking public transportation construction spending: highways, rail, mass transit, the stuff we normally think of as the backbone of the economy.

A few implications that follow:

→ Permitting has become capacity planning. The limiting factor is whether you can clear interconnects, secure substations, and lock a realistic delivery date.

→ Local winners will be the places that can ship electrons. Grid headroom, fast utility coordination, and transmission access are becoming the new version of being on the interstate.

→ The ripple effects are bigger than the site. More demand for transformers, switchgear, generators, concrete, skilled trades, and a whole new layer of long-term O&M jobs around power and cooling.

We’re watching a shift where digital growth is pulling physical construction, and public systems, along with it. Worth planning for.

1

46

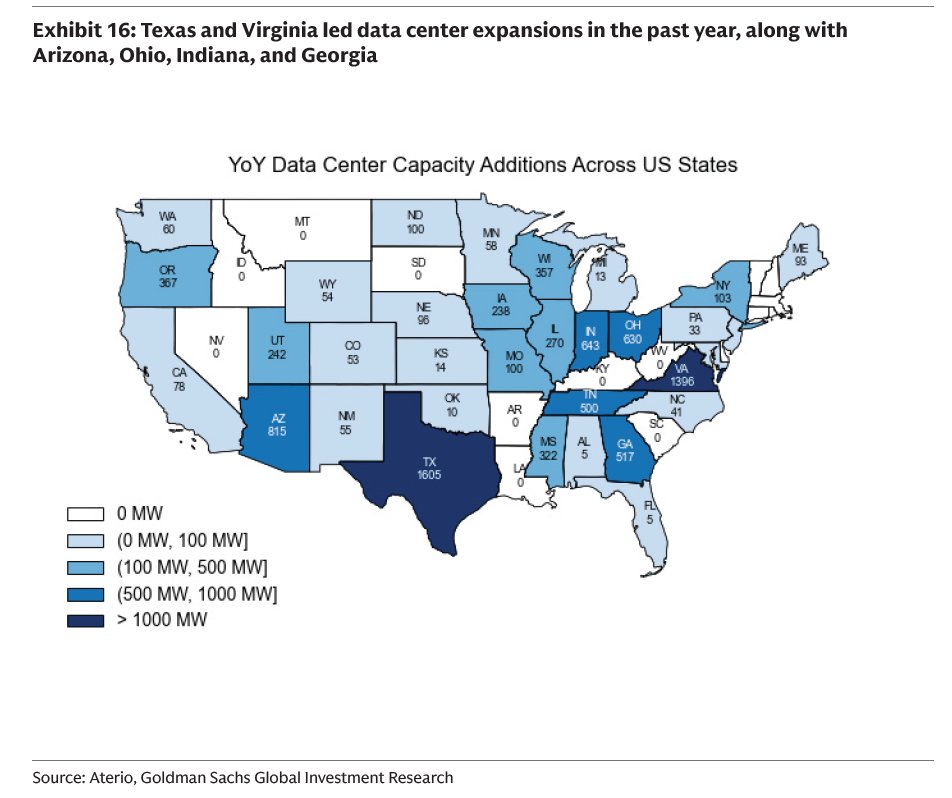

This map tells you exactly where the data center buildout is actually landing, and why.

Texas and Virginia are setting the pace. GW-scale annual capacity additions in both. The constraint is time-to-power and time-to-build. Developers go where interconnection, generation, and delivery timelines can actually pencil.

The next tier is quietly forming: Arizona, Georgia, Indiana, Ohio. Accessible transmission, big sites, improving fiber, fewer surprise bottlenecks than the legacy coastal hubs.

Data centers were ~4% of US electricity use in 2024. Demand is expected to more than double by 2030.

The conversation has shifted from "where's the land?" to "where are the electrons?"

Capacity additions are following grid reality, and that's what's reshaping which secondary markets become first-class.

78

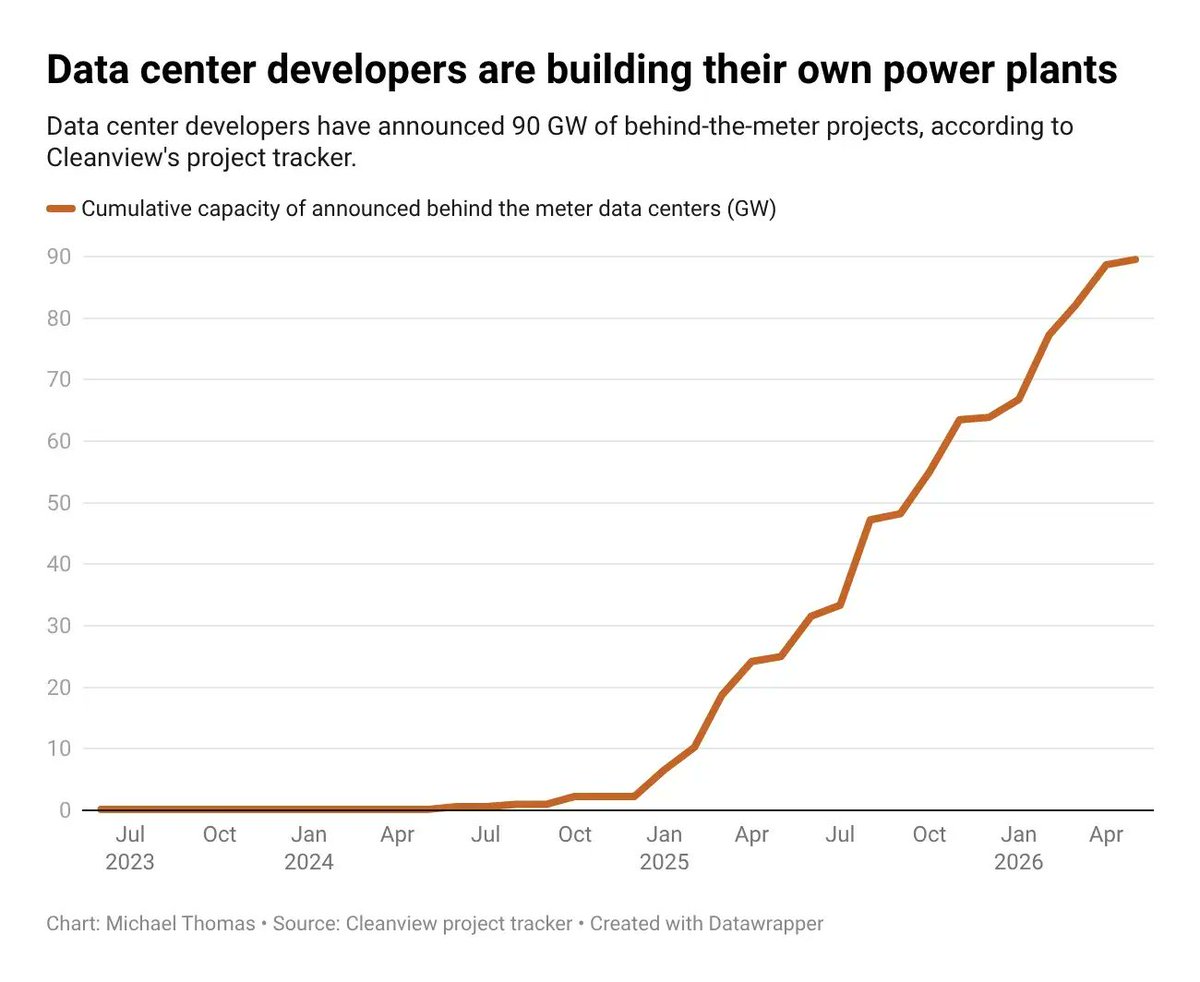

Data center developers just quietly rewrote the power playbook.

~90 GW of announced behind-the-meter projects — meaning data centers showing up with their own generation. For scale, that's roughly the output of 90 utility-scale 1 GW power plants. A parallel buildout.

What this signals:

"Time-to-power" is now a competitive advantage. If you can't get a reliable megawatt on a predictable date, the land, buildings, and GPUs are just a placeholder.

The grid is still central but no longer the only path to scale. BTM is a hedge against queue risk, curtailments, and "we'll study it" timelines.

The next phase iswho can deliver power, predictably, at campus scale.

29

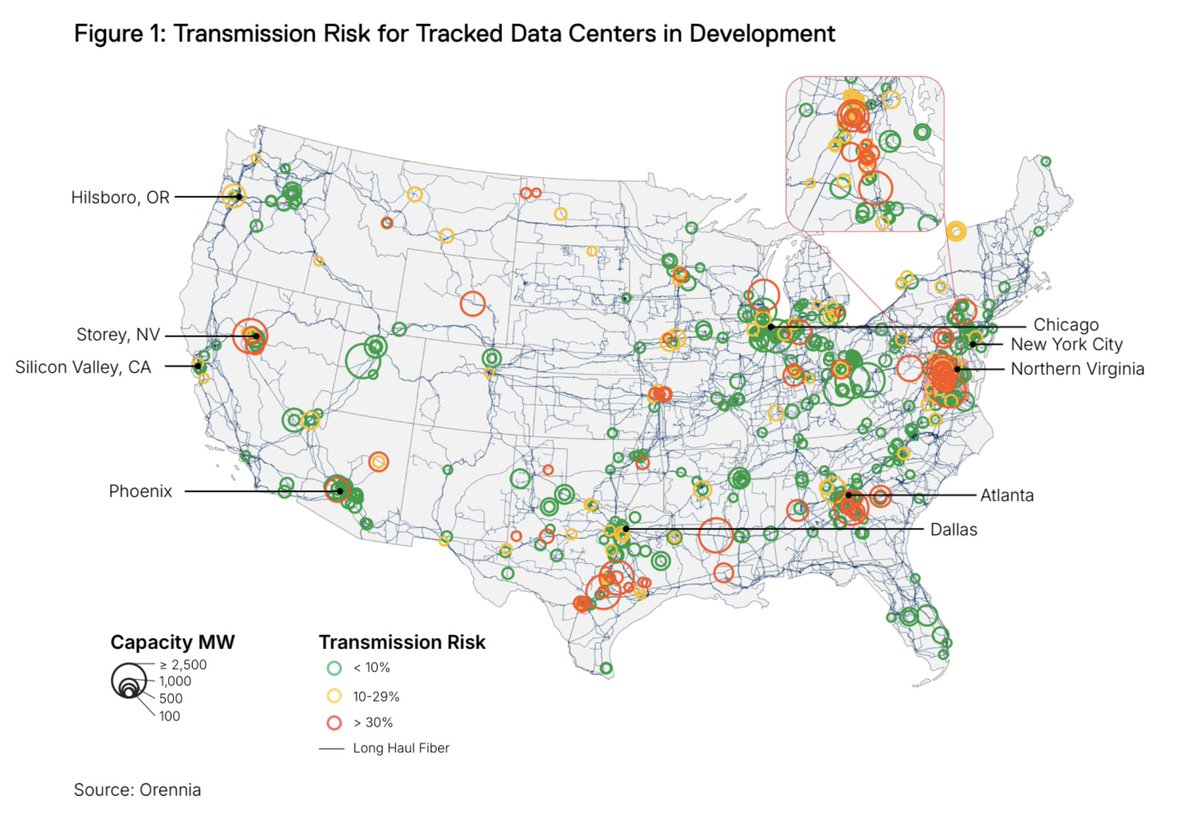

This map should be required reading for anyone making data center site selection decisions right now.

Orennia's transmission risk analysis shows a significant portion of the largest projects in the pipeline sitting at 30% transmission risk.

Northern Virginia, the world's highest concentration of data center capacity, is also carrying some of the highest transmission risk in the country. Phoenix follows the same pattern.

The green circles across the Midwest and Southeast tell the diversification story. Lower risk, growing capacity, markets that got ahead of the grid problem by building where transmission headroom still existed.

Transmission risk is the variable most developers underweight at site selection and overpay for at construction. This map shows exactly where that problem is concentrating.

Source: Orennia

#DataCenters #AIInfrastructure #SiteSelection #PowerGrid #DigitalInfrastructure

77

NVIDIA's 800VDC architecture is becoming the standard for next-generation AI data centers, and the supply chain opportunity goes well beyond the GPU.

800VDC means less conversion loss, less copper, better efficiency at 100kW rack densities. Every serious AI build is having this conversation right now.

The four supply chain layers that follow:

Layer 1 — Wide Bandgap Semiconductors: $STM $WOLF $NVTS $IFNNY

Layer 2 — Power Management & Gate Drivers: $MPWR $TXN $VICR $ADI

Layer 3 — Busbars, Connectors & Power Modules: $APH $TEL $NVT $FLEX

Layer 4 — Industrial Power Infrastructure: $VRT $ETN $GEV $SIEGY

Most investment conversation focuses on Layer 1. The real constraint over the next three years is Layers 3 and 4, long lead times, limited capacity, demand curves that weren't modeled at this scale two years ago.

#DataCenters #AIInfrastructure #NVIDIA #PowerDistribution #SupplyChain #DigitalInfrastructure

1

171

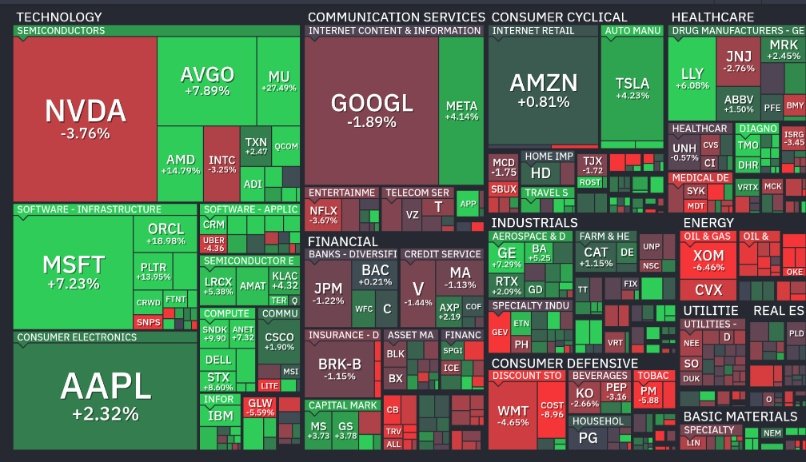

Mixed market day, but the AI infrastructure story is right there in the heat map.

$MU 27.49% — HBM demand running ahead of supply, memory market repricing in real time

$AMD 14.79% — what happens when you double your server CPU market forecast to $120B by 2030 $AVGO 7.89% — custom silicon momentum making everything else look like the side story

$MSFT 7.23% — AI monetization finally showing up in numbers

$NVDA -3.76% — most owned stock in the world, profit-taking happens, demand picture unchanged

Three things I take from this tape:

➡️ Semis aren't moving together anymore, as winners are tied to specific bottlenecks: memory, interconnect, packaging, power.

➡️ Hyperscaler spend is showing up downstream. When the headline GPU name cools off, the suppliers around it are where conviction gets expressed.

➡️ Dispersion is the story. AI exposure is not a single checkbox. Understanding where the constraint sits in the data center stack is what separates the right calls from the wrong ones.

#DataCenters #AIInfrastructure #Semiconductors #NVIDIA #AMD #Micron #DigitalInfrastructure

1

575

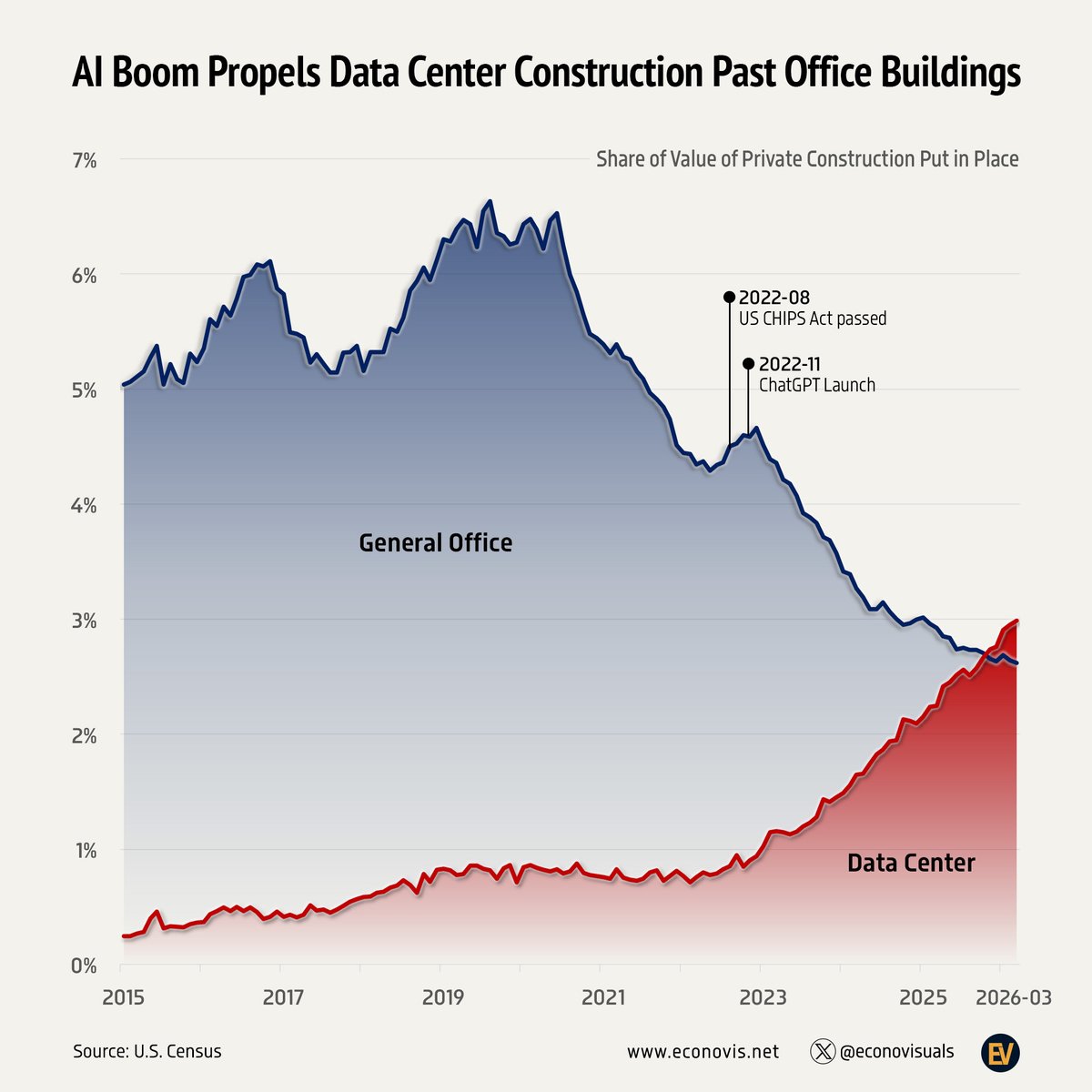

Office construction has collapsed from 6% to under 3% of all US private construction value. Data centers just crossed it at 3%, for the first time in history.

The same shift in how people work that gutted office demand accelerated AI adoption, which drove the compute infrastructure buildout that is now outpacing one of the most established asset classes in commercial construction history.

The buildings that house AI infrastructure have become the dominant force in private construction. The supply chain needs to catch up.

Source: U.S. Census via @econovisuals

1

44

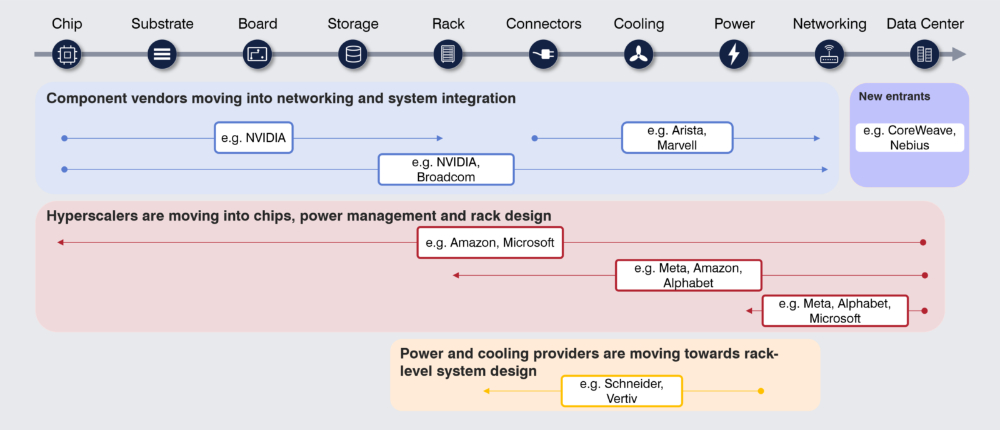

Every major player in the data center stack is expanding into someone else's territory, and it's accelerating.

NVIDIA now spans chip to cooling system design.

Amazon & Microsoft are designing their own chips, power management, and rack architecture, Schneider & Vertiv are pushing into rack-level system integration, and CoreWeave & Nebius are bypassing the traditional colocation model entirely.

The boundaries that defined this industry five years ago are dissolving. The companies that position themselves at the integration points are the ones that will define the next decade of AI infrastructure.

1

134

Google just broke ground on its first data center in Sweden: air-cooled, heat recovery for local homes, €5M community fund, built on 700 MW of renewable energy Google has been adding to Sweden's grid since 2013.

This is what proactive community engagement looks like, which is infrastructure designed from day one to give something back to the place it's built in.

The projects that earn community trust early are the ones that scale.

48

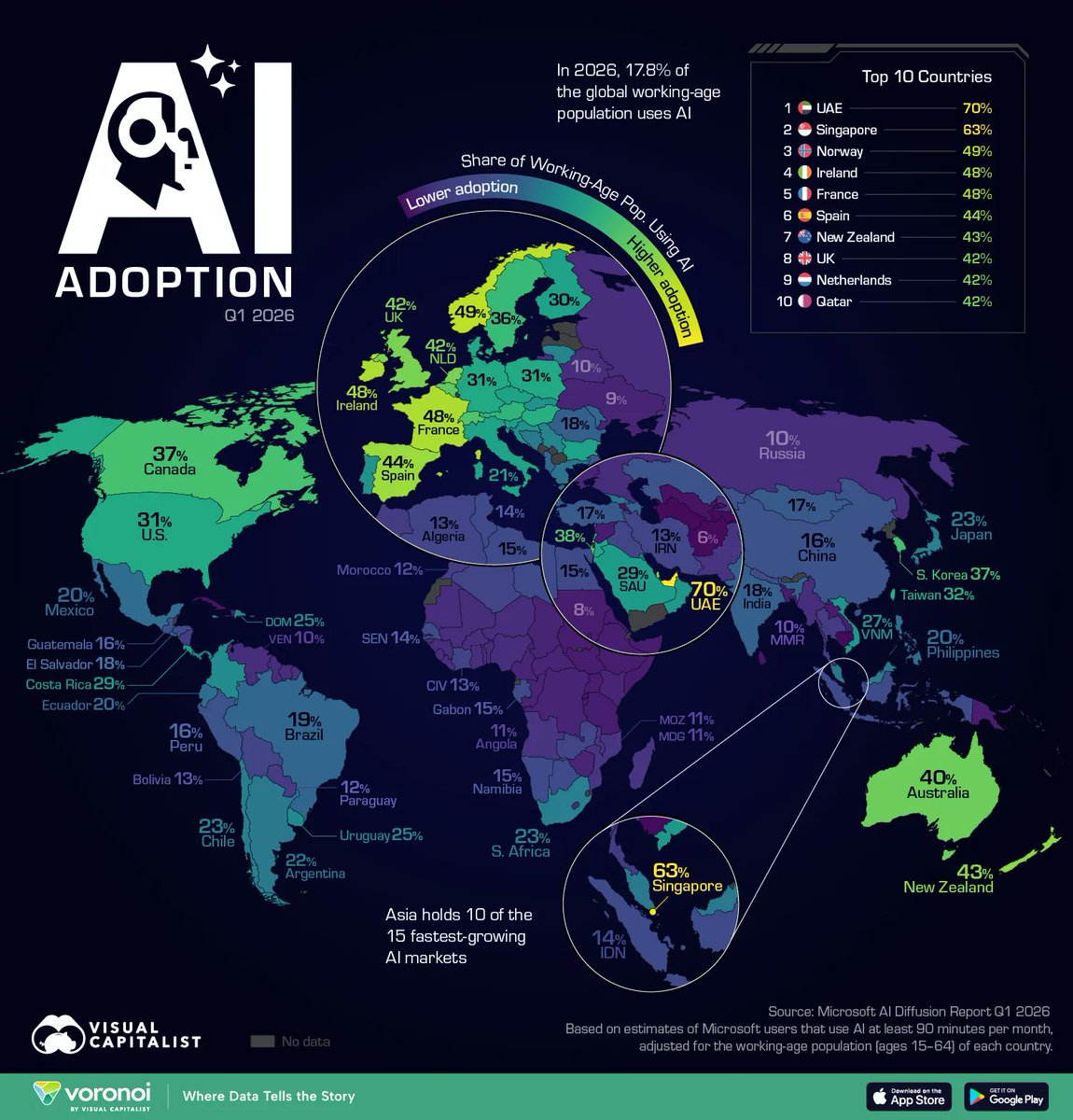

The US builds most of the world's AI infrastructure. It doesn't lead in AI adoption.

UAE: 70%. Singapore: 63%. The US trails more than 20 countries despite leading AI development. South Korea grew adoption 43.2% in the last year alone. Europe accounts for 11 of the world's top 20 AI adoption markets.

China sits at just 16% but at China's scale, even modest increases add hundreds of millions of new AI users overnight.

The demand driving the infrastructure buildout is increasingly global. The countries adopting fastest are creating inference workloads that need to be served closer to where users actually are.

2

2

149

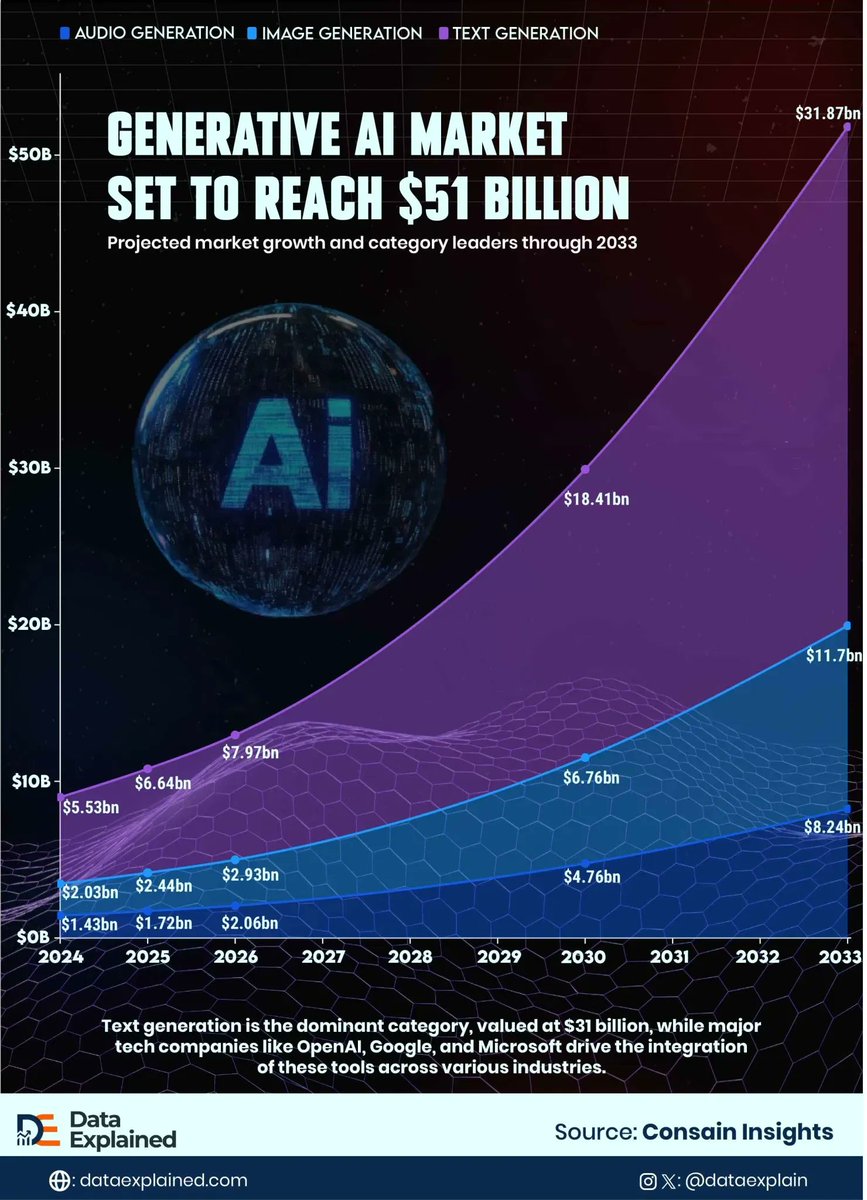

The generative AI market is projected to reach $51 billion by 2033, and every dollar of that number has a physical address.

Text generation alone hits $31.87B. At the inference scale required to serve that volume, the compute demand translates directly into rack density, power draw, and cooling load that data centers are being designed around right now.

The three categories on this chart have different infrastructure profiles:

▪ Text generation = sustained, high-density GPU compute

▪ Image generation = burst-intensive, heavy parallelization per request

▪ Audio = lower footprint today, but real-time voice agents will change that fast

The $51B is what the application layer captures. Data centers are building the foundation that makes that number possible, and that foundation needs to be in the ground years before the revenue arrives.

1

67

SoftBank just committed €75 billion to build AI data centers in France. To put that in context, it's larger than the GDP of Bulgaria.

€45 billion first phase, 3.1 GW in the Hauts-de-France region by 2031, and Schneider Electric partnering on Dunkirk. Total buildout targets 5 GW.

A €75 billion bet from one of the world's most aggressive tech investors is a direct signal that France is being taken seriously as a location for next-generation AI compute.

59

May 29

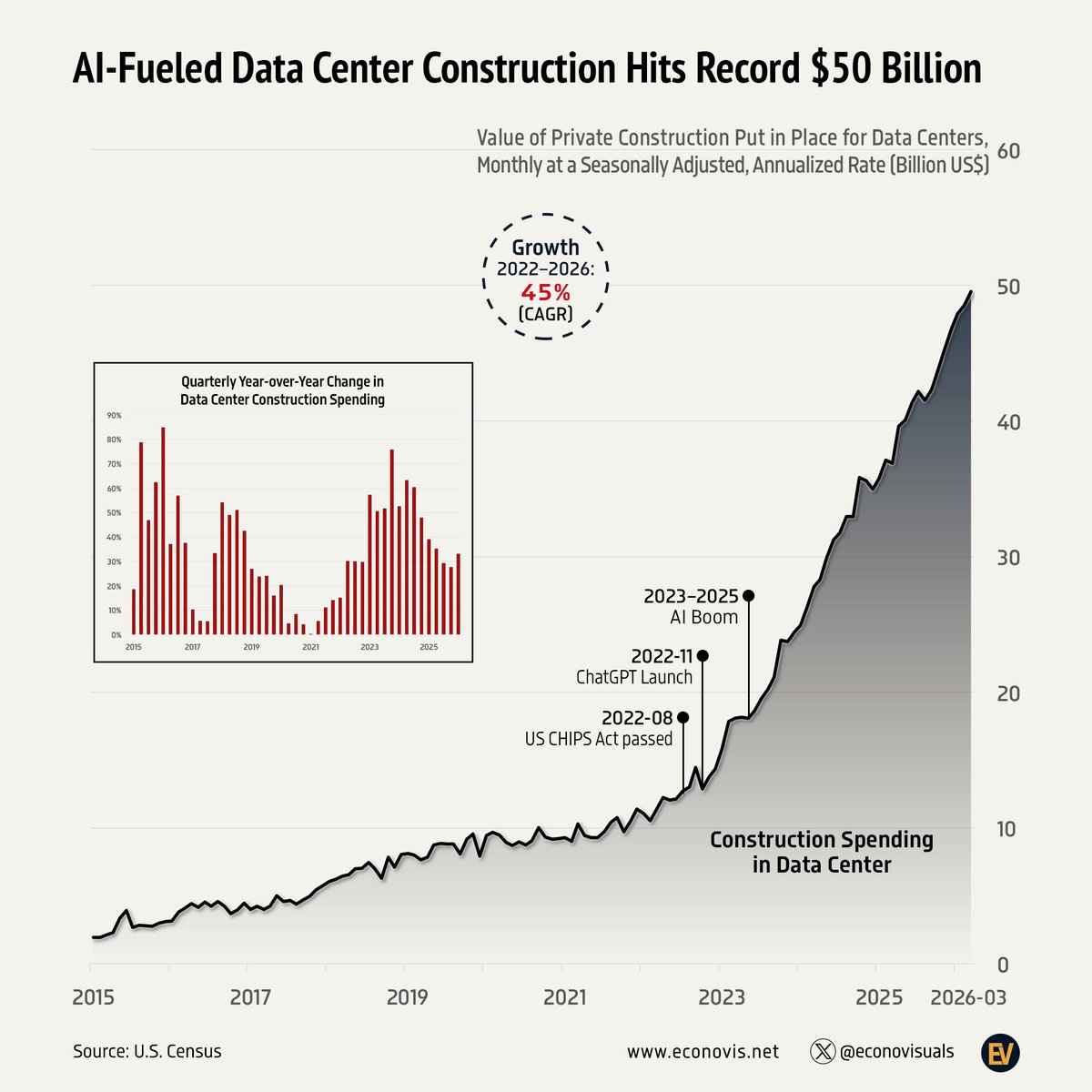

Data center construction spending just hit $50 billion annualized: 45% CAGR since 2022.

Three inflection points that explain the chart:

August 2022: CHIPS Act passed

November 2022: ChatGPT launched

2023–2025: AI boom sustained it

What took the industry decades to build in cumulative spending is now being deployed in a single year and this is construction costs only. It excludes servers, GPUs, cooling, and power infrastructure. The real number is significantly larger.

Source: U.S. Census via @econovisuals

2

86

May 28

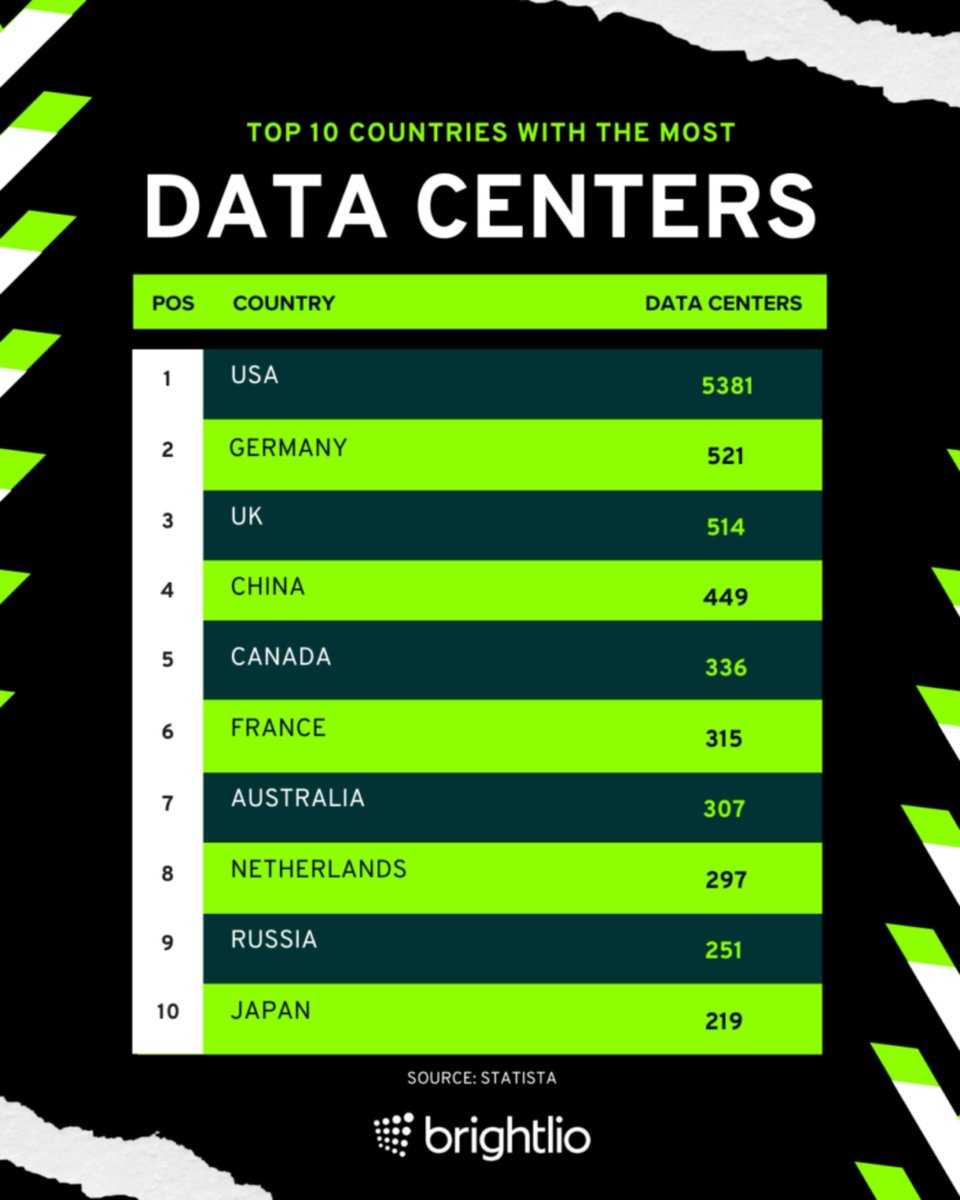

The US has 5,381 data centers. Germany is second at 521. The gap between first and second is larger than the entire count of every other country on this list combined.

That dominance is the result of decades of early investment, deep capital markets, and the world's largest tech companies all pulling in the same direction.

China at 449 is the number worth watching most closely. The count gap is narrowing, and when you account for the scale of individual facilities being built there rather than just the number, the picture gets more competitive fast.

Infrastructure leadership in AI starts with compute infrastructure. This list is a reasonable proxy for where that leadership currently sits.

33

May 27

Five companies are putting $602 billion to work in 2026, and roughly half lands in data center infrastructure.

Amazon $155B

Microsoft $160B

Alphabet $125B

Meta $120B

Oracle $42B

What took the entire industry a decade to build in cumulative capex is now being deployed in a single year. Every quarter analysts have called for a pullback, the numbers have come in higher.

When hyperscalers fund half of all global data center spend, the entire ecosystem downstream (construction, power, cooling, switchgear, fiber) is operating as an extension of five balance sheets. Their capex cycles become everyone else's revenue cycles.

Extraordinary opportunity for companies positioned correctly in the stack. Centralized risk for everyone who isn't.

56

May 27

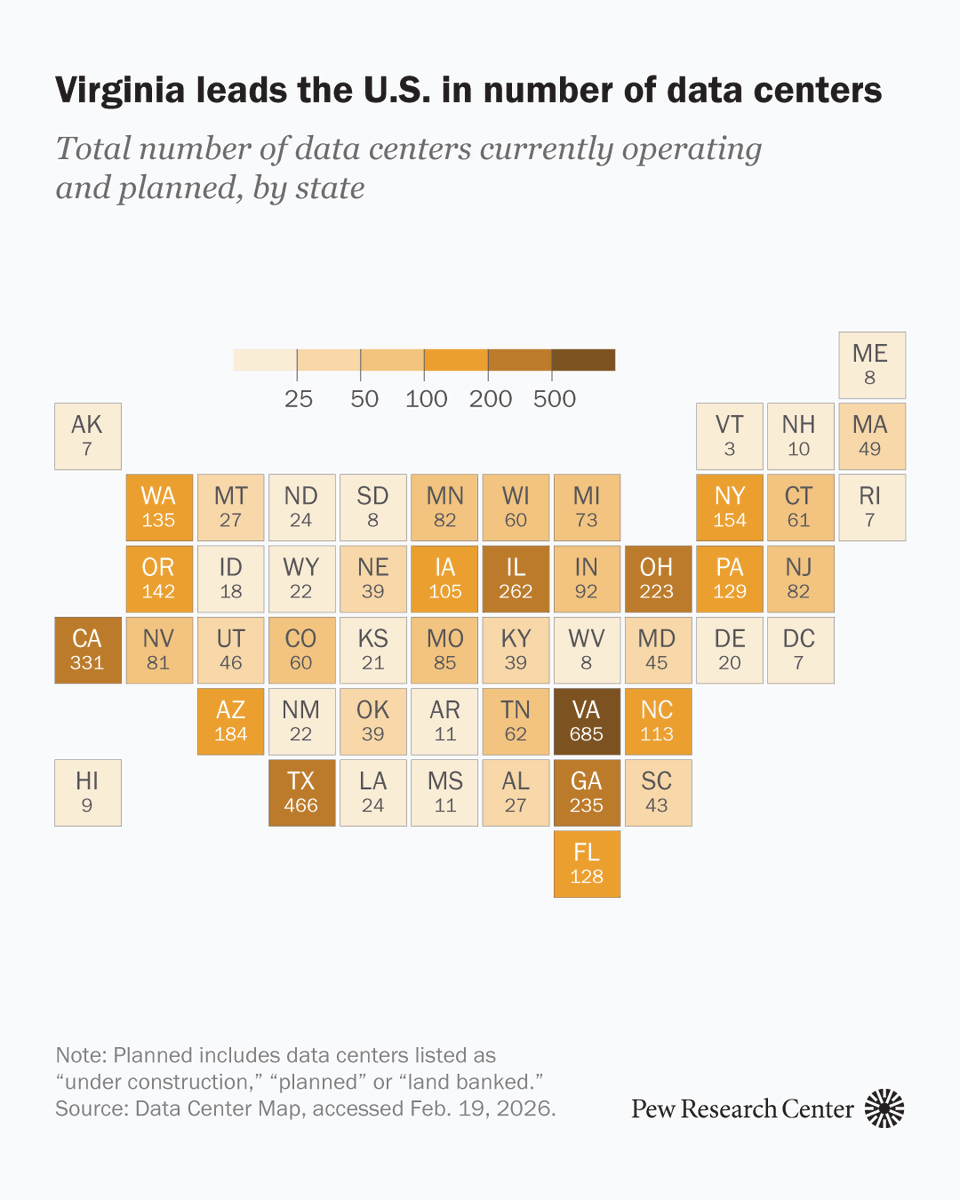

Virginia has 685 data centers, Texas is second at 466, and California third at 331.

The concentration at the top reflects decades of infrastructure investment that incumbents built long before AI made data centers a household conversation.

What's more interesting is the middle of the map. Illinois at 262, Ohio at 223, North Carolina at 113. The Midwest and Southeast are building real scale and attracting the same hyperscale investment that once flowed almost exclusively to Northern Virginia.

67% of planned data centers are going to rural areas. 39% into counties that currently have none. Where compute gets built shapes where AI economic benefits land, and that picture is changing fast.

1

1

61

May 26

Blackstone just committed $5 billion to a joint venture with Google to sell TPUs as a compute-as-a-service offering, giving enterprises a direct route to TPU capacity outside of a traditional Google Cloud contract. First 500 MW targeted for 2027.

This is also a direct move in the GPU vs. TPU battle. Google has long positioned TPUs as its answer to NVIDIA's dominance, and this is how they scale that access without building the infrastructure entirely on their own balance sheet.

The model matters as much as the money. Enterprises with specific AI workloads, capital market firms, research institutions, or buyers who need dedicated compute but don't want a full hyperscale cloud relationship. That's a real market nobody was serving at scale until now.

1

64

May 26

India is quietly becoming one of the most consequential data center markets in the world, and it's moving faster than most people realize.

Schneider Electric's data center business in India is already growing double-digits, currently 15–20% of their India revenue, with the market projected to reach $31.36 billion by 2035 at a 13.37% CAGR.

What makes India different from other emerging markets is the convergence happening simultaneously: domestic AI adoption, government-backed digital infrastructure investment, deep engineering talent, and a manufacturing ecosystem already in place.

The operators and vendors building India relationships now are the ones who will be positioned when this market hits its next gear.

1

61