Joined April 2009

- Tweets 14,206

- Following 2,488

- Followers 2,114

- Likes 1,412

699 Photos and videos

Pinned Tweet

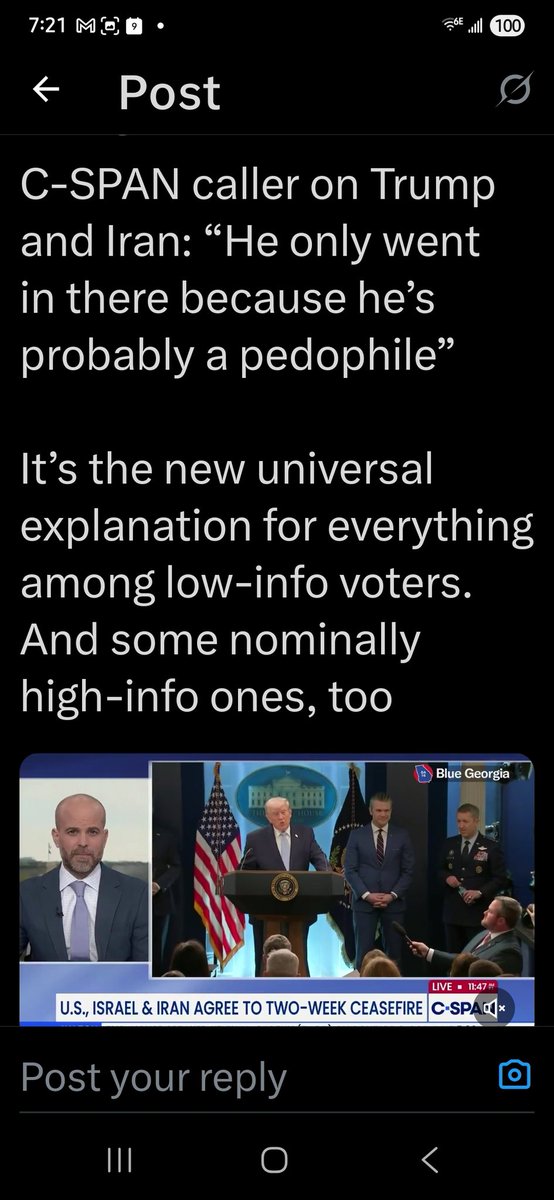

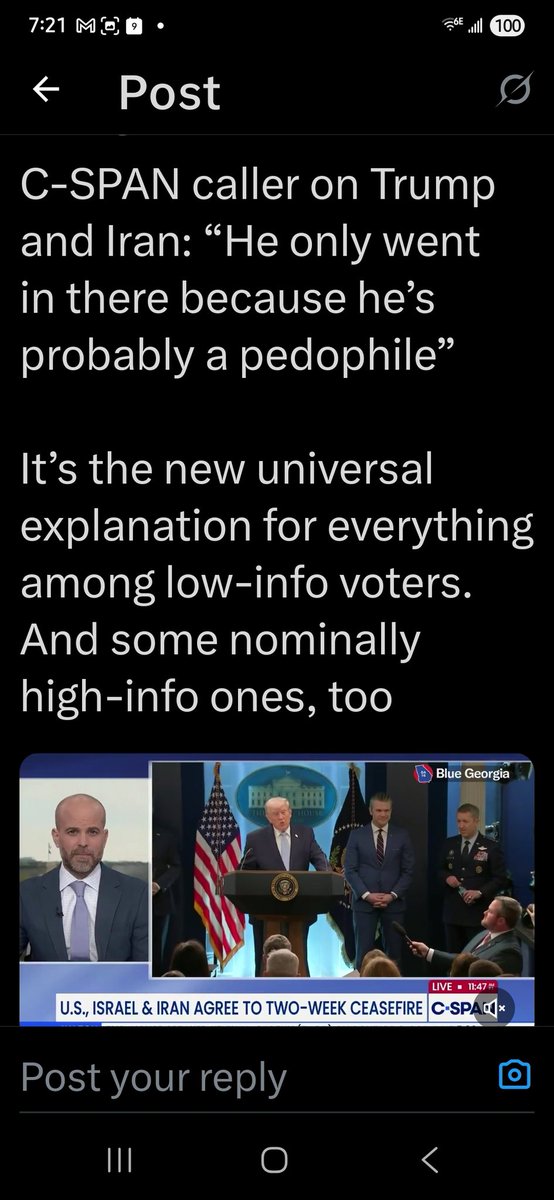

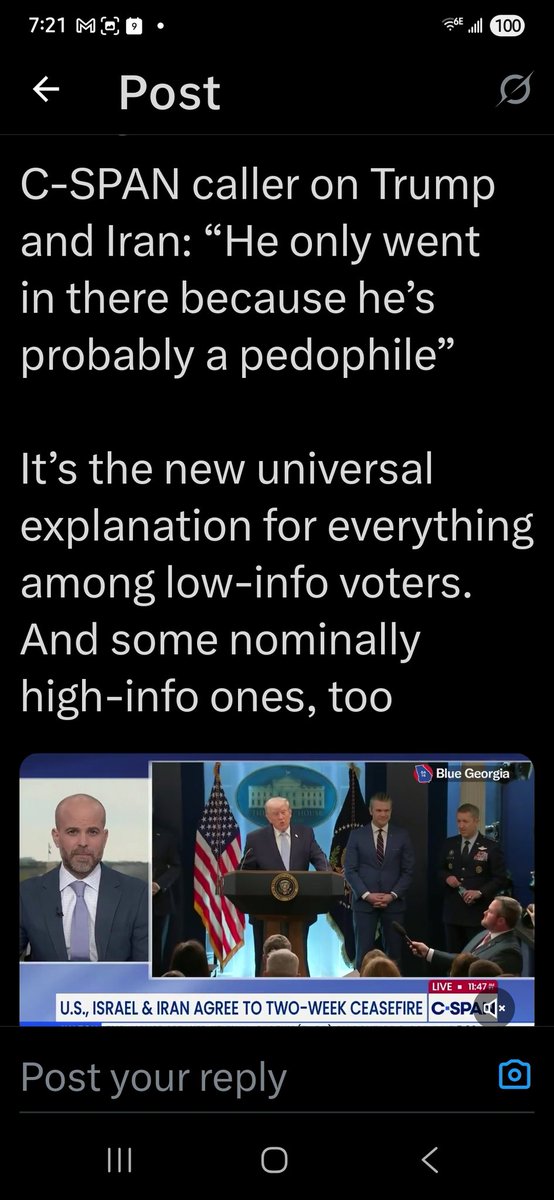

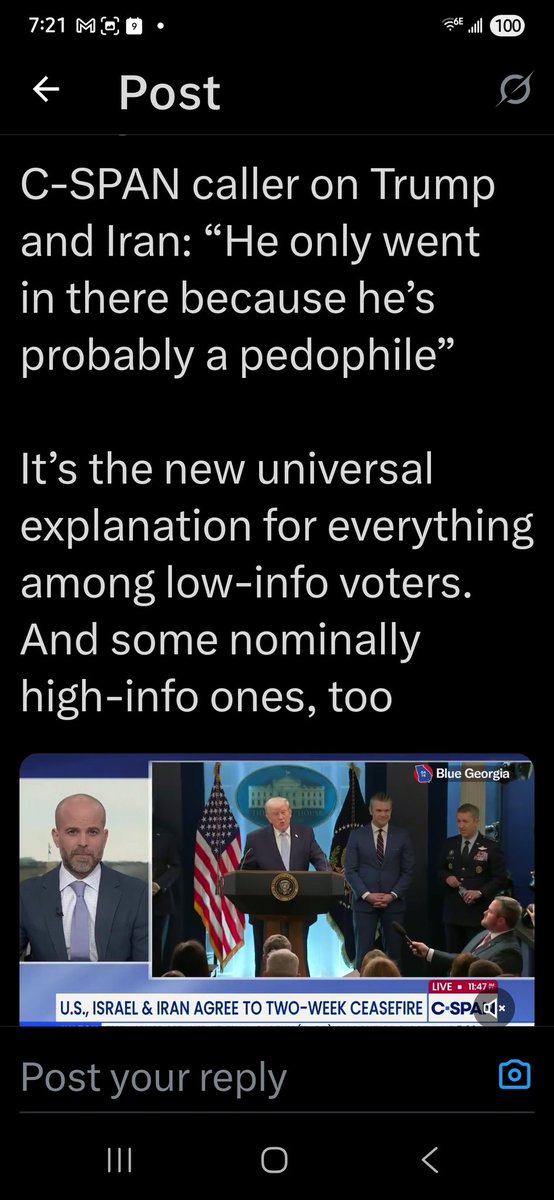

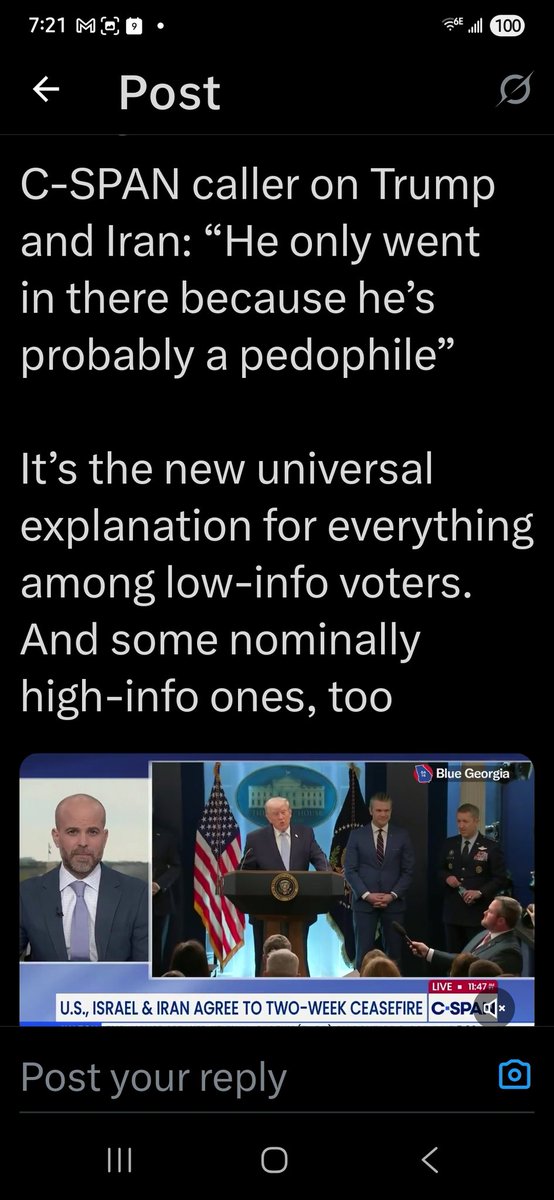

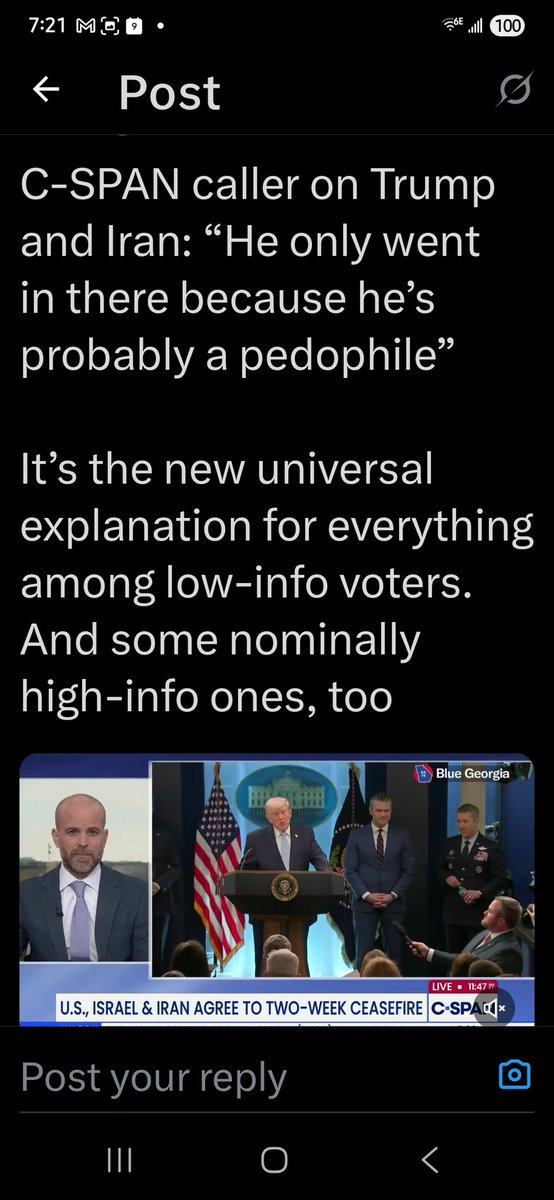

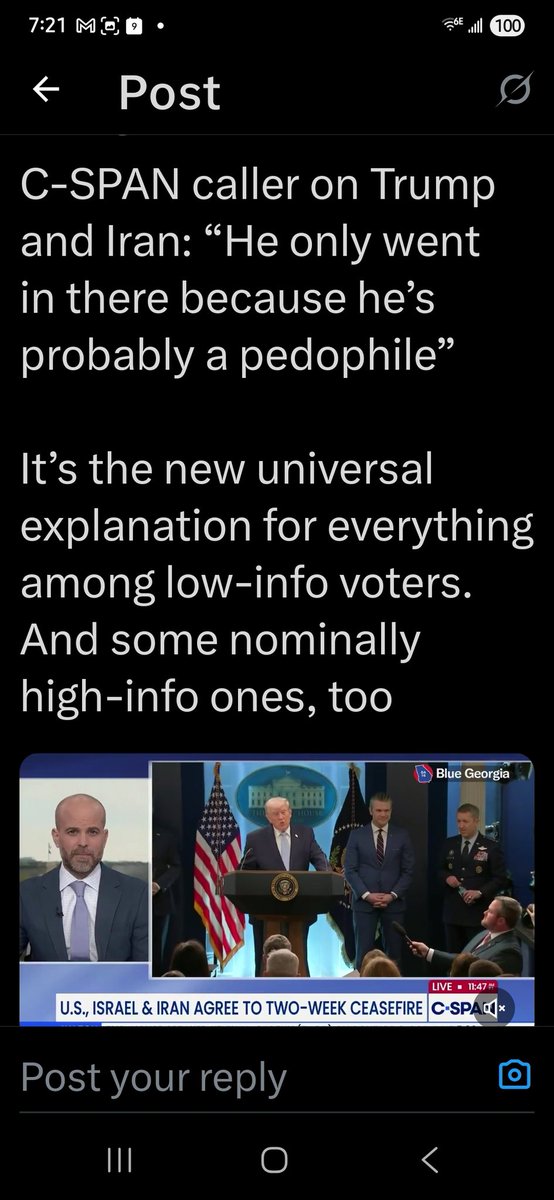

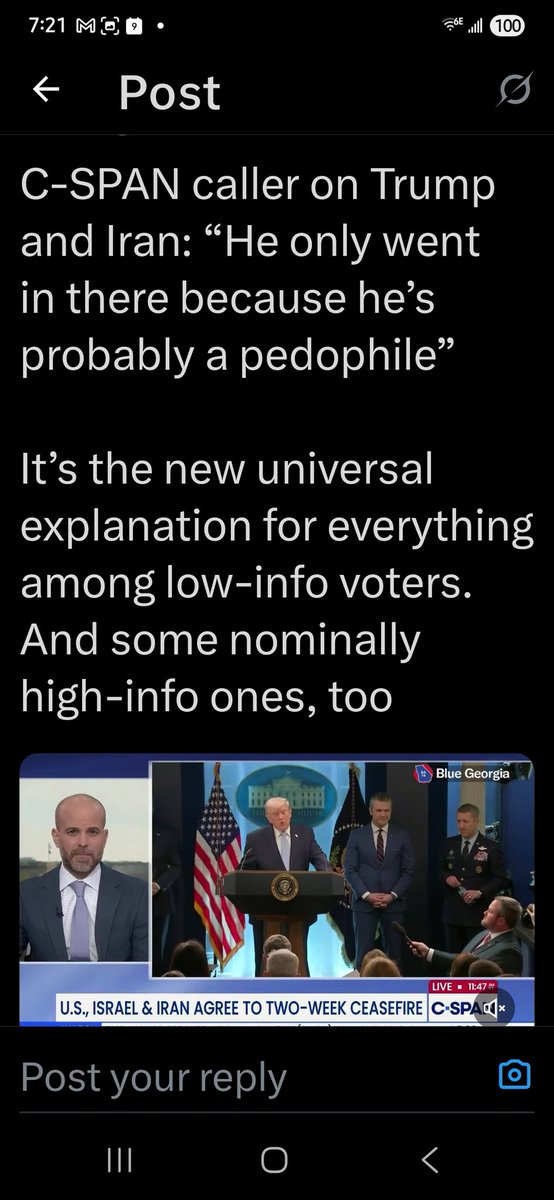

23 Jan 2025

The High Tide Ultimate Frisbee Tournament returns to North Myrtle Beach in March. Book your team to win!

1

2

80

279,931

Jun 11

They'll give you a bond

Jun 10

So if social security goes into insolvency by 2032 what tf happens to all the money that’s been taken out of my check for the past decade????

12

mgb retweeted

Jun 10

Mark it.

“Ladies and gentlemen, you will not hear a better argument for the President of the United States than those five minutes and twenty-five seconds right here:

Cut it. Mark it. Drop it in.

Are you a Leftist?

Are you a Communist?

Are you a Marxist?

Are you super Right-wing? Doesn’t matter.

You can’t disagree with that. That is the best argument you will ever hear—condensed, distilled, like proof alcohol—into why Charlie Kirk believes in this President.”

115

2,387

5,965

129,518

Jun 11

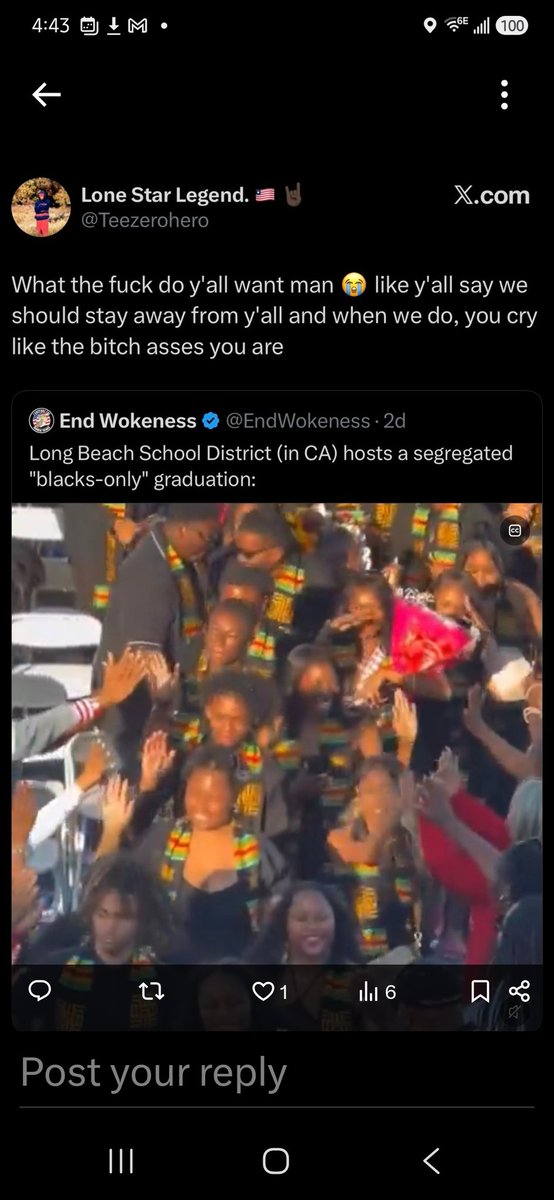

They knew and failed to stop it?! 😆 They built the whole corrupt scheme - IT WAS THEIR BUSINESS MODEL!!

Jun 10

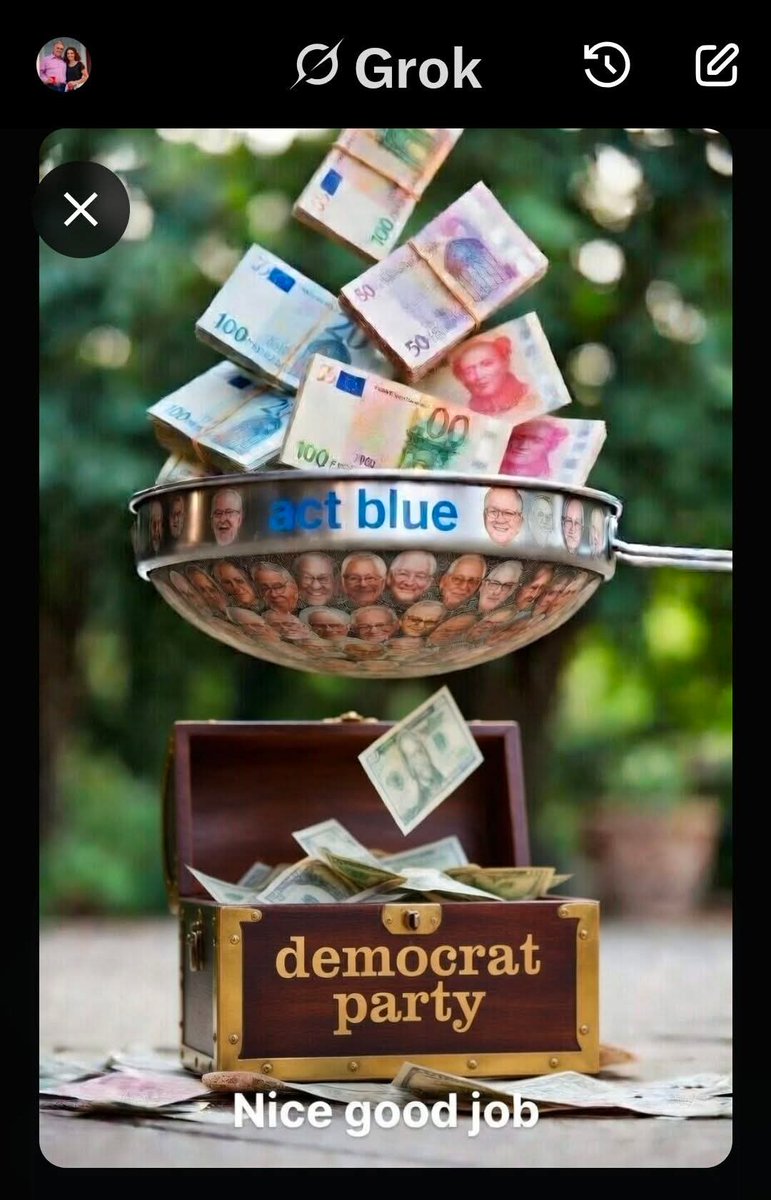

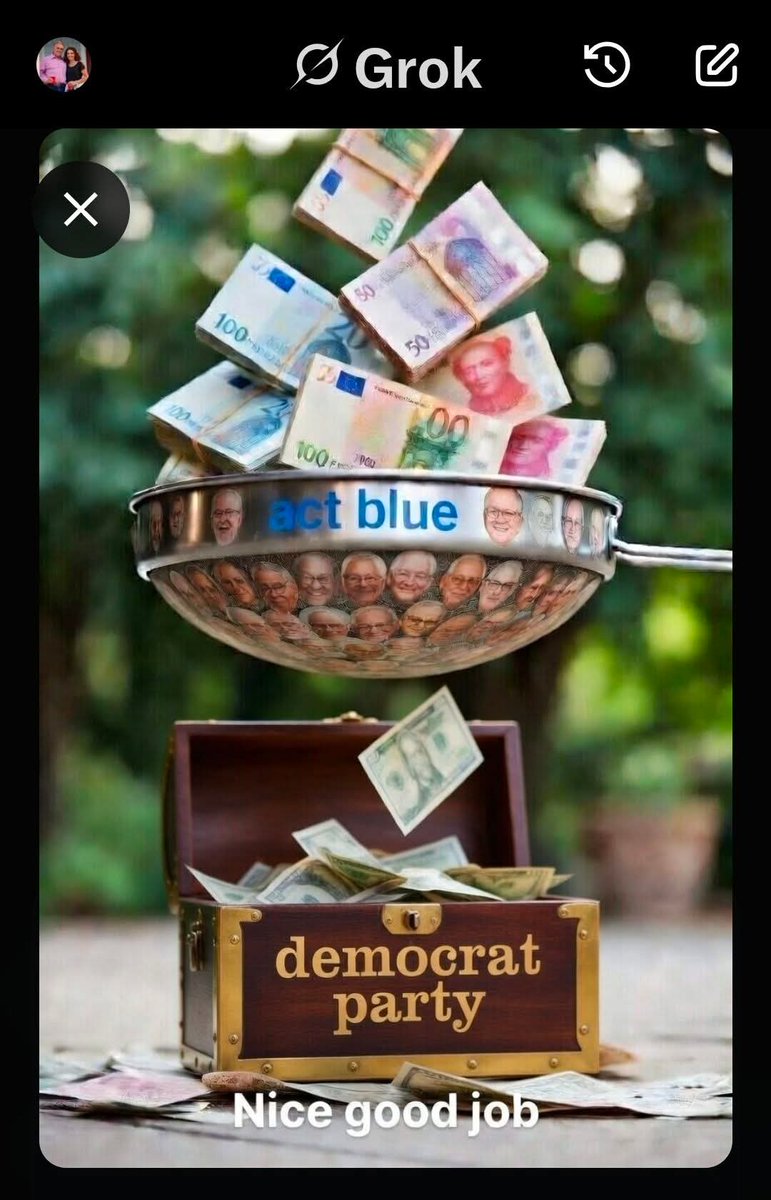

ActBlue accepted foreign money and donations under fake names.

They knew about it and failed to stop it.

And when we asked them about it, they all took the 5th.

6

mgb retweeted

Jun 8

You thought you hated liberal boomers? You don’t hate them nearly enough.

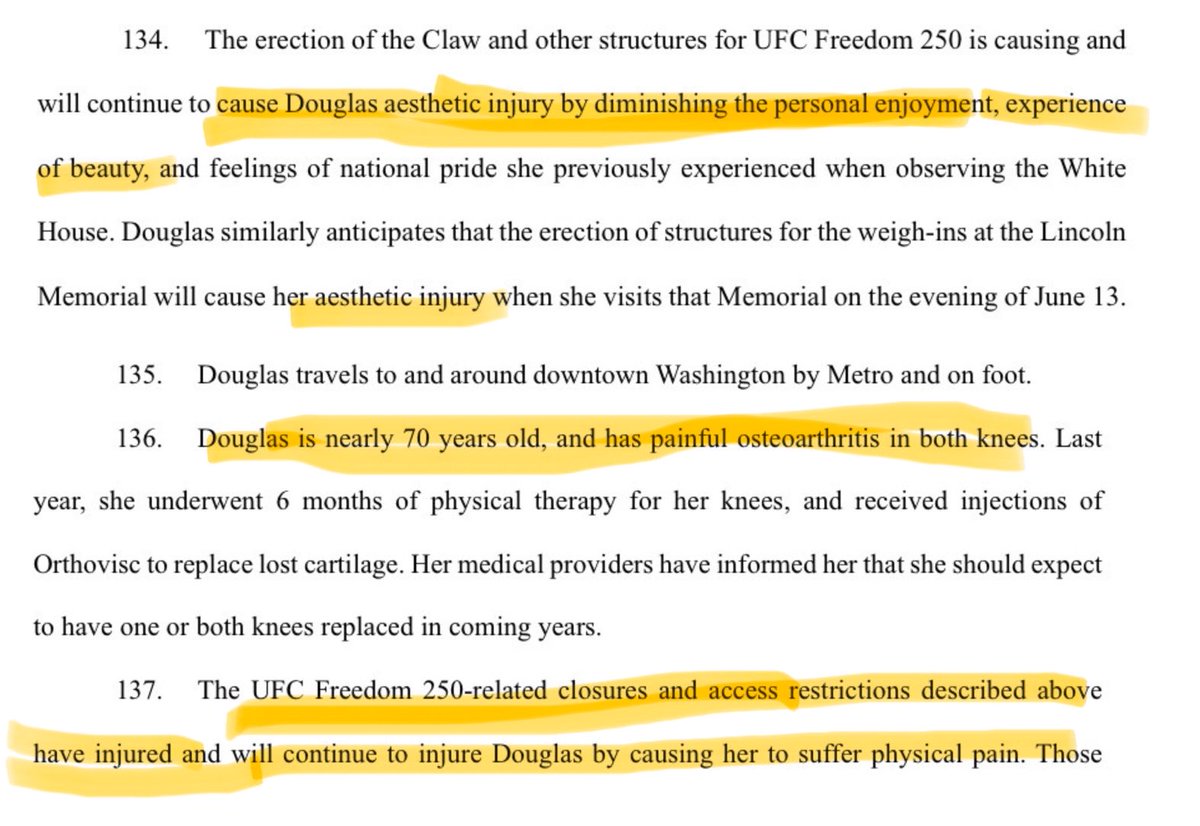

A 69-year-old retired bureaucrat from Alexandria, Virginia, Susan F. Douglas, is suing to stop the planned UFC Freedom 250 event at the White House as part of America’s 250th birthday celebration.

Her argument? The event would cause her “aesthetic injury,” meaning she doesn’t like looking at it. She also claims watching it would worsen the physical pain from her osteoarthritis.

A patriotic celebration featuring Americans enjoying themselves would allegedly cause Susan both emotional distress and physical pain. Think about that.

After spending more than 50 years working in DC, Susan shares that she now devotes her retirement to protesting the White House ballroom and construction of the triumphant arch, opposing renovations like those of reflection pool, and serving as a “safety marshal” at No Kings protests.

Susan is also a prolific donor to the James Talarico for Senate campaign, according to FEC records. Make of that what you will.

Liberal boomers spent decades running the country into the ground, shipping jobs overseas, and opening the floodgates to third worlders. Now that they’re retired, they dedicate themselves to draining the joy out of life for all other Americans.

561

1,998

6,081

115,267

Jun 7

Until the gotcha journalism stops

How much longer are we going to tolerate the way Trump speaks to female reporters?

1

20

mgb retweeted

Jun 6

I DON'T UNDERSTAND WHY MORE PEOPLE DON'T USE GOOGLE GEMINI TO RESEARCH STOCKS.

NOT FOR ADVICE.

NOT FOR PREDICTIONS.

BUT TO THINK CLEARLY BEFORE RISKING MONEY.

HERE ARE 10 DETAILED PROMPTS THAT I ACTUALLY USE 👇

30

93

397

57,453

Jun 1

He's offensively projecting.

Paul Krugman: “We really need to do a thorough purging of the United States."

“We need a deMAGAfication…similar to de-Nazification."

This deranged lunatic was employed by NYT for 20 years.

19

mgb retweeted

May 27

After a Stacey Abrams linked NGO reported $100 in revenue in 2023, the Biden EPA awarded them $2 BILLION in 2024. Thanks to President Trump’s leadership, I canceled that entire grant and that NGO has not had access to any of those funds. In fact, the Trump EPA has canceled over $29 BILLION in grants so far on behalf of the hardworking American taxpayer.

2,632

16,573

82,072

1,141,777

mgb retweeted

May 22

Insane corruption from a homeless project in Los Angeles, California

- The Weingart NGO got a $30 million dollar grant for homeless housing

- A senior citizen home was cleared of elderly residents

- The property was listed on the market for $11.2 million, but it was then sold to Weingart for $27 million (huge gap of money that disappeared)

The city pays the NGO extremely high rates, $400,000 per bed per year for homeless housing on this property

The building sits empty

The NGO has no obligation to put a homeless person in a bed, so they can bill for every room at $400,000 per year with no one in them

It doesn’t stop there. Taxpayers also cover the purchase, operations, upkeep, and problems even if the facility sits empty

The Weingart NGO operates around 10 similar homeless housing facilities

We need prison sentences for every Democrat involved in these deals and every NGO executive

Spencer says he will hand them over to the IRS and DOJ for investigation and prosecution

I saved him some time and looked up who handed the money out

Key Democrats Who Oversaw the Money

- Mayor Karen Bass (Democrat)

- Former Mayor Eric Garcetti (Democrat)

- Key member on the Housing & Homelessness Committee is Nithya Raman (Democrat) who has been involved in oversight and funding decisions

- LA County Board of Supervisors (All Democrats)

I think the problem is clear

376

6,542

17,377

765,407

Elon Musk opened the federal budget and found what both parties spent decades making sure nobody would ever see.

The receipts.

Musk: “Most of the fraudulent government payments, especially to the NGOs, go to the Democrats. Let’s say 80%, maybe 90%. 10 to 20% of it does go to Republicans.”

He didn’t say one side was clean.

He said both sides were eating.

Musk: “The honest answer is the Republicans are partly… they’re receiving some of the fraud too. They’re getting a vig.”

A vig.

That’s the word you use when the house takes a cut of every bet at the table.

That’s not governance. That’s a rake.

And when DOGE shut off the fraudulent payments, the loudest screams didn’t come from Democrats.

They came from Republicans.

Musk: “When we turn off funding to a fraudulent NGO, we’d get complaints from whatever the 10% of Republicans who were receiving the money. And they would very loudly complain.”

You tell someone 90% of the fraud funds their political opponents.

And they still fight you to keep their 10%.

Musk: “I tried telling them, ‘Well, you know, 90% of the money is going to your opponents.’”

Rogan: “They want their piece.”

Musk: “Yeah, they want their piece.”

Rogan: “And they’ve been getting that piece for a long time.”

The uniparty was never a conspiracy theory.

Musk: “The whole uniparty criticism has some validity to it.”

It’s a revenue model.

Left and right aren’t opponents. They’re co-signers on the same account.

The theater is for you. The money is for them.

Every bank on earth runs AI that flags a suspicious $47 charge before you even notice it.

The United States government somehow can’t catch billions in fraudulent payments to shell NGOs.

The technology exists. It has for years.

An algorithm doesn’t care which party you belong to. It doesn’t take a vig. It doesn’t have a donor.

It just follows the money.

And that’s exactly why they’ll never willingly deploy it.

Musk didn’t expose a partisan scandal.

He exposed the operating system of American governance.

And the most dangerous thing he did wasn’t cutting the payments.

It was proving both sides would rather protect the fraud than lose their cut.

The system isn’t broken.

It was built this way.

150

2,809

5,963

122,005

mgb retweeted

BREAKING: Justice Department Veteran Reveals President Obama Prosecution Possible in ‘Grand Conspiracy’ Case Against President Trump; Says James Comey’s “8647” Indictment Will Likely Survive First Amendment Challenges

This week on Straight to the Point, I sat down with former DOJ official and longtime federal prosecutor Jim Trusty for a wide-ranging interview on the expanding investigations into Obama-era intelligence and law enforcement officials dubbed “The Grand Conspiracy."

Asked if the cases were viable, Trusty identified 18 USC 242 as the leading statute for prosecutions in the alleged ‘grand conspiracy’ and discusses how former CIA Director John Brennan’s TV appearances and recently published book may have reset the clock on the statute of limitations. Trusty also addressed James Comey's recent “8647” threat indictment and possible superseding false statements charges.

@thelatmg @latimesstudios_

Responding to the NC indictment, former FBI Director Comey said he is still innocent, not afraid, and believes in the independent judiciary.

John Brennan has called the investigation politically motivated.

Columbia Law School Professor Daniel Richman has not responded to repeated requests for comment.

00:40 Legal Theory Behind “Grand Conspiracy” Against President Trump

01:30 Former CIA Director Brennan Investigation

02:15 Florida Courts Are the Battleground

02:52 What is "Deprivation of Rights Under Color of Law"

04:30 Brennan Alleged “Abuse of Authority” 2017 Intelligence Report About Russia

04:55 Former NSA Director Mike Rogers Critical Witness

05:30 DOJ Can Get Around Statute of Limitations

06:15 Did Brennan’s TV Appearances, Book “Restart the Clock” on Statute of Limitations?

07:45 Brennan Claims Investigation is Politically Motivated

09:00 Attorney General Bondi vs Acting Attorney General Blanche

09:40 Comey “8647 Seashell” Indictment Can Survive First Amendment Challenge

11:32 Comey “Forfeiture of Assets”

13:28 Superseding Indictment Comey Case

14:05 Columbia Law School Professor Was Liaison to Media

15:14 FBI Director Patel Declassified FBI Media Leaks Probe Codenamed “Arctic Haze”

16:00 Potential False Statements to Investigators

16:50 Comey Memos: Trump/Russia Collusion Investigations

18:20 Was Comey the Source of Classified Leak?

18:45 President Obama Not Off The Hook

20:00 Defendants Will Try to Run Out the Clock

21:50 Legitimate Indictments vs. Moral Condemnation

23:10 White House Briefing: Taking the New Media Seat

23:55 Breaking the Legacy Media Hold on Washington

340

3,552

9,607

2,056,727

mgb retweeted

Meeting with British royalty is about the least patriotic way to mark our 250th anniversary. All the more true now, since we’re only beginning to grasp the extent of UK interference in our politics... Steele dossier and all.

Pass the SAVE Act. Don't pretend it doesn't exist.

253

3,070

12,392

76,911

mgb retweeted

Apr 23

Typical liberal. You know how much of a savings it is and you know how much of a grand slam home run this is. But you are just filled with hatred because of words.

78

3

47

6,451

mgb retweeted

Apr 23

Arch Bishop Fulton J. Sheen!! When Bishops were Bishops!! ✝️

43

360

579

16,171

mgb retweeted

Apr 22

The Southern Poverty Law Center is a fire department full of arsonists.

93

506

4,203

34,606

JUSTICE CLARENCE THOMAS: “I think if we don’t stand up and take ownership of our country, and take responsibility for it, we are slowly letting others control how we think and what we think.”

"If you think it's losing confidence, then you get up and you participate. You don't sit on the sidelines."

1,250

10,291

45,259

1,245,056

mgb retweeted

Apr 10

Leading California Governor Candidate Steve Hilton Says He Will Investigate and Prosecute Gavin Newsom over Mass Californai Fraud

California has reportedly blown through at least $180 BILLION in fraud under Newsom. Hilton says most of the stolen money is financing the Democrat political machine.

"It's absolutely SICK! And we need to see prosecutions of the politicians!"

"It’s PATHOLOGICAL! The level of lying and the shamelessness of the lying. there’s something really wrong with someone who’s able to behave like this."

87

527

2,468

44,164

mgb retweeted

Elon Musk: "The whole idea with what Nelson Mandela, who was a great man, proposed was that all races should be on an equal footing in South Africa. That's the right thing to do. Not to replace one set of racist laws with another set of racist laws."

140

329

2,677

52,110

PRESIDENT TRUMP: "I'm proud to join with Christians across the country and around the world to celebrate the most glorious miracle in all of time: The resurrection of our Lord and Savior, Jesus Christ."

"To be a great nation, you must have religion — and you must have God. In churches across the nation on Sunday, the pews will be fuller, younger, and more faithful than they have at any time in many, many years."

"Happy Easter to all, may God bless you, may God bless the United States of America."

4,030

8,887

51,703

1,407,009

Mar 30

2008 had the entire fiasco tied to all of the homes, so a foreclosure avalanche ensued.

Private credit collapse destruction will fall primarily on the now-gated off investors.

How is the Private Credit fund investors' loss more contagious than something like a major market correction with similar size losses?

Mar 30

Subprime Crisis 2.0: Will Private Credit Be The Trigger? | Tyler Durden, Zerohedge

We have recently tackled the rising stress in the Private Credit markets. Here are a few of our previous warnings:

- Fitzpatrick: Soros CEO & CIO Warns of a Reckoning

- Private Credit Stress: Will The Fed Backstop Exuberance Again? – RIA

- Is Private Equity A Wolf In Sheep’s Clothing?

After 30 years of watching credit cycles expand, distort, and collapse, I’ve learned one reliable rule:

“When enough people start drawing comparisons to 2008, it’s worth stopping to check whether the analogy holds up — or whether fear is doing the analytical work for them.”

Right now, judging by the amount of commentary on social media, the stress in the private credit market has everyone’s attention. Most of the commentary being generated makes the immediate jump from private credit firms “gating” exits to the onset of the next subprime crisis in the financial system. Those claims are certainly alarming and generate many clicks and views, but the question is whether those claims are based on facts rather than opinions.

Just recently, Goldman Sachs CEO David Solomon flagged the risk of private credit in his annual shareholder letter. Lloyd Blankfein, who piloted Goldman through the Global Financial Crisis, warned publicly that the financial system appears to be “inching toward another potential catastrophe.” Meanwhile, Goldman’s own research arm published a note concluding that private credit stress is “unlikely to generate large macroeconomic spillovers on its own.”

So which is it? A repeat of the subprime crisis of 2008, or a painful but contained credit cycle? The honest answer most likely sits somewhere in between, and understanding exactly where private credit differs from subprime tells you a great deal about how worried you should actually be.

Let’s revisit 2008.

What Made The Subprime Crisis So Catastrophic

It is hard to believe that we are rapidly approaching the 20-year anniversary of the “Great Financial Crisis” that nearly destroyed the financial system as we knew it. There are many investors and commentators in the markets today who only know about the event from reading history books. Having lived through it, it is a different reality.

Crucially, the 2008 subprime crisis wasn’t simply a mortgage problem. It was a leverage-and-derivatives problem that started in mortgages. That distinction matters enormously when you’re sizing up today’s private credit stress.

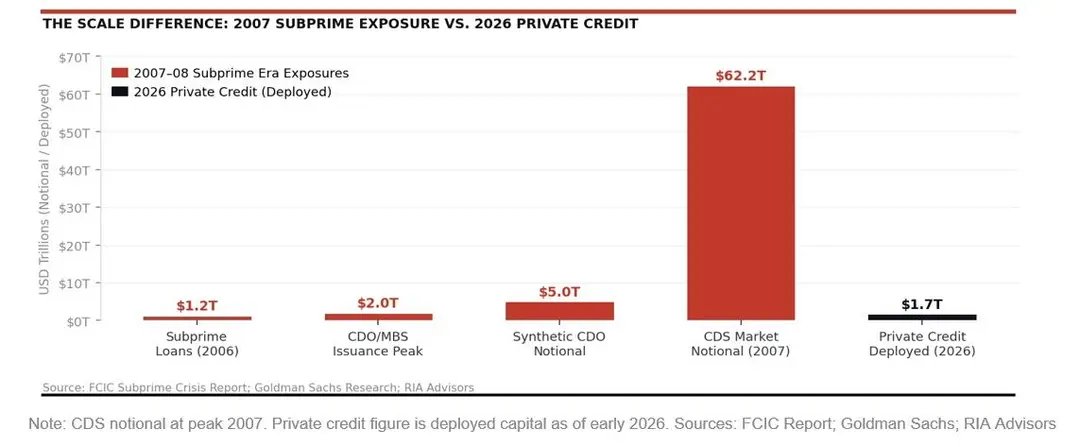

At the heart of the crisis was a product called the collateralized debt obligation, or CDO. Banks packaged pools of subprime mortgages into tranches, which were rated by agencies using flawed models. Those CDOs were then re-sliced into “CDO squared” structures, layering additional complexity and opacity on top of already opaque assets. The real acceleration came when synthetic CDOs entered the picture. Unlike cash CDOs, which required actual mortgages, synthetic CDOs referenced mortgages through credit default swaps. Journalist Gregory Zuckerman found that while roughly $1.2 trillion in subprime loans existed in 2006, synthetic structures created more than $5 trillion in exposure referencing those same loans. The CDS market alone reached a peak notional value of $62.2 trillion by year-end 2007. That is not a typo.

But the derivatives machine required raw material to function, and Wall Street’s insatiable hunger for collateral triggered what historians of the crisis now call the “race to the bottom” in mortgage underwriting. To keep the CDO assembly line running, originators needed volume. That demand for volume led to a collapse in underwriting standards. By 2006, no-money-down mortgages were commonplace.

- NINJA loans, “No Income, No Job, No Assets,” were extended to borrowers who could not remotely service the debt once introductory teaser rates reset.

- Stated-income loans, in which borrowers self-reported earnings with no verification, became the industry norm rather than the exception.

- Adjustable-rate mortgages were sold to buyers who qualified only at the teaser rate and had no capacity to absorb resets of 3 to 4 percentage points two years later.

The Mortgage Bankers Association later estimated that subprime originations reached $600 billion in 2006 alone, up from roughly $160 billion in 2001. Most importantly, the loans were designed to be sold, not held. In other words, the originator of the loan bore no long-term risk and had every incentive to close as many transactions as possible, regardless of quality.

That single misalignment of incentives was the original sin of the entire subprime crisis.

What compounded the damage beyond even that was systematic, institutionalized fraud at the origination and securitization level. The Financial Crisis Inquiry Commission documented widespread “robo-signing,” where bank employees executed thousands of mortgage documents per day without reviewing them. They affixed signatures and notarizations to paperwork they had never read. Countrywide Financial, Washington Mutual, and others were found to have misrepresented loan quality in the representations and warranties they made to investors purchasing MBS tranches, fraudulently inflating the apparent collateral quality of the pools they sold.

Appraisers faced pressure, and in many cases direct financial incentive, to hit predetermined valuations that supported loan amounts the underlying properties could never justify. The FBI reported that mortgage fraud suspicious activity reports increased by more than 1,400% between 2000 and 2007. When losses eventually surfaced, investors discovered they had purchased securities backed not just by bad loans, but by fraudulently documented ones. That distinction made recovery values nearly impossible to model and turned settlement litigation into an industry unto itself for a decade afterward. JPMorgan alone paid $13 billion in 2013 to resolve government claims over mortgage securities, and that figure represented only a fraction of industry-wide settlements.

When housing prices began falling, that entire structure detonated in both directions simultaneously. Banks that held CDO tranches faced mark-to-market losses. Banks that sold CDS protection, AIG being the most famous, faced collateral calls they couldn’t meet. Here is the most crucial point. These instruments traded freely in liquid markets, so price discovery occurred in real time, compressing the panic into a matter of weeks. The interconnection was total. Twelve of the thirteen largest U.S. financial institutions were at risk of failure, according to then-Fed Chair Ben Bernanke.

That’s what systemic risk actually looks like.

Private Credit Stress Is A Different Animal

The private credit market now stands at roughly $1.7 to $2 trillion in deployed capital, a figure that has grown rapidly since banks retreated from middle-market lending after the Global Financial Crisis. That growth is precisely what generated the current stress. Redemption requests have surged across major platforms. Blackstone’s BCRED fund saw record redemptions of $3.8 billion in Q1 2026, exceeding its 5% quarterly buyback limit. Apollo, Blue Owl, and Morgan Stanley’s North Haven fund have all imposed withdrawal restrictions. That gating of withdrawals led to an obvious decline in inflows across retail private credit funds. Those inflows fell to roughly half their 2025 pace, according to Goldman Sachs estimates.

So far, the catalyst is concentrated in software companies, which represent an estimated 15% to 25% of many private credit portfolios. They are under pressure as AI disruption fears potentially erode their earnings power and their ability to service debt. The headline default rate sits around 2% as of 2025, but Goldman Sachs Asset Management’s own research acknowledges that figure understates the true level of stress. When you include liability management exercises and distressed exchanges, the real rate approaches 4% to 5%. That’s meaningful deterioration. It’s not catastrophic, but it’s real.

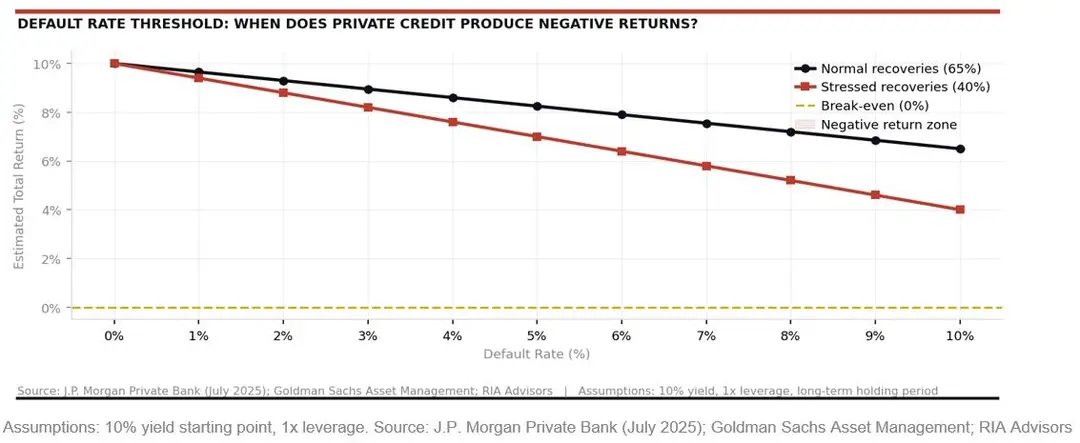

J.P. Morgan’s analysis showed that for senior direct lending to produce negative total returns, default rates would need to exceed 6% while recovery rates would collapse below 40% simultaneously. Those numbers have historically appeared only during COVID and the Global Financial Crisis itself. That’s a high bar — but it’s not an impossible one. However, that would require a deterioration in macroeconomic conditions, a continuation of the Iran conflict oil shocks, and a contraction of consumer spending, which could certainly amplify risks. As shown below, the current structural comparison between the subprime crisis and the private credit sector today is markedly different.

The Importance of the Gating System

The most structurally significant difference between 2008 and today is also the one that generates the most debate. Unlike the subprime crisis, private credit funds can gate their exits. When Blackstone caps BCRED redemptions at 5% per quarter, it’s not a failure of the fund; it’s the mechanism working as designed. In 2008, there was no such circuit breaker. MBS and CDOs traded continuously in secondary markets, meaning every forced seller found a bid at a lower price, triggering more mark-to-market losses, which in turn triggered more forced selling. The feedback loop was instantaneous and brutal.

Gating slows that process considerably. LPL Research noted that while gating makes for terrible headlines, it prevents the forced liquidation that accelerated subprime losses. Goldman Sachs estimates that retail private credit inflows will remain in net outflow throughout 2026 and likely into 2027, a slow bleed, not a cliff. That’s a very different contagion profile.

That said, gating is not a cure. It transfers the problem in time, not away from investors. Those sitting in redemption queues face a multi-year wait to exit positions that may continue to deteriorate. The opacity of private credit portfolios and manager-reported valuations means stress can accumulate invisibly until it can’t.

“The key risk in private credit is not what is visible, but what remains hidden.” – The Daily Economy

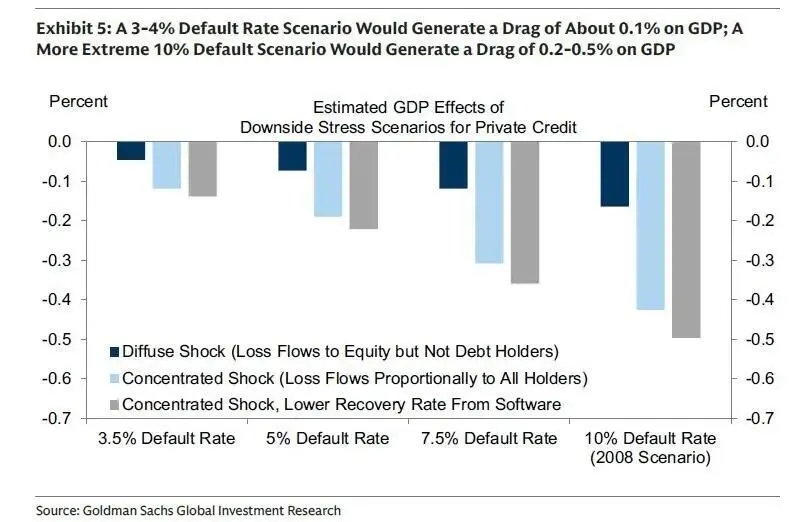

Goldman Sachs economist Manuel Abecasis concluded that, even in an adverse scenario, private credit stress would only drag on GDP by 0.2% to 0.5%. His reasoning is straightforward: the private credit sector holds about $1.7 trillion in levered loans, or roughly 4% of all credit to the private non-financial sector. That’s is not nothing, but it’s not the $62 trillion CDS market either. Goldman also notes that bank lending to businesses has actually accelerated recently, providing a partial offset if private credit tightens.

Blankfein’s view carries different weight precisely because he’s been through the real thing. He warned that private credit assets “can be hard to analyze, may feature hidden leverage, and can become tough to sell.” He’s right that opacity and illiquidity create conditions where problems compound before they surface. The question is whether those conditions, combined with a still-manageable scale, produce systemic contagion or simply painful losses for a subset of investors.

“Private credit stress is unlikely to generate large macroeconomic spillovers on its own.” — Goldman Sachs Economist Manuel Abecasis, March 2026

I’m inclined to side with Goldman’s macro conclusion. However, with a caveat that matters. The base case holds only so long as private credit problems don’t compound with a broader recession, a sustained oil shock from the Iran conflict, and a sharper-than-expected deterioration in software company cash flows. Any two of those three conditions occurring simultaneously change the calculus. Goldman’s own research acknowledges this. The bigger risk isn’t private credit alone. It’s private credit stress coinciding with the wider tightening of financial conditions.

What Investors Should Pay Attention To

The structural differences between today and the subprime crisis are real and important. There’s no synthetic subprime CDO chain multiplying private credit losses to a $5 trillion notional exposure. Most critically, the investor base is primarily institutional, not retail money market funds holding fraudulently rated paper. Fund-level leverage is modest, and the gating mechanism, whatever its imperfections, prevents the instantaneous price cascade that made the subprime crisis so destructive.

What this most closely resembles is a normal credit cycle playing out in an untested asset class. Not a systemic collapse, but not a benign correction either. Goldman Sachs Asset Management’s own European research found that “stress events are likely to remain elevated relative to the last decade,” concentrated in smaller companies and cyclical sectors. That pattern will probably hold in the U.S. as well.

Three things would change my view and warrant genuine alarm.

- First, if default rates push past 8% in tech-heavy private credit portfolios as AI disruption accelerates.

- Second, if bank credit facilities to private credit managers get pulled at scale, triggering forced asset sales.

- Third, retail penetration of private credit grows, as institutional investors sell, leaving less-sophisticated money to hold the bag.

None of those conditions is inevitable. All of them are possible.

The subprime crisis analogy fails on the specifics. But the lesson from the subprime crisis isn’t about CDOs. It’s about what happens when credit markets expand rapidly, underwriting discipline erodes under competitive pressure, and opacity masks deteriorating loan quality. On those broader conditions, the warning is more relevant than the Goldman bulls would like to admit.

That is why we continue to underweight risk for now until we have better clarity about the future.

Key Catalysts Next Week

This is the most structurally loaded week of the quarter. The calendar stacks a Q1 close, a Q2 open, and a full employment gauntlet into five sessions, with markets still metabolizing whatever the Fed just delivered..

Tuesday is the pivot. Consumer Confidence is the marquee release, and it’s the first full-month reading that captures the Iran conflict, the tariff widening, and February’s payroll shock in a single survey. The prior print of 91.2 was already soft. The Expectations component, which the Conference Board flags as a recession signal below 80, is the number to watch. A sharp drop would validate the stagflation fears the Fed just tried to navigate around. Chicago PMI and Case-Shiller Home Prices round out the morning, and then Q1 closes at the bell. Expect elevated volume as pension funds and mutual funds finalize window dressing and mark final positions, totaling roughly $62 billion on the buy side.

Wednesday flips the calendar to Q2 and immediately delivers a triple shot: ADP private payrolls, ISM Manufacturing, and JOLTS. After February’s -92,000 NFP shock, the ADP print will either stabilize the labor narrative or accelerate the deterioration thesis. ISM Manufacturing is the tariff passthrough read, the Prices Paid subindex will tell us whether producers are eating costs or passing them through, while New Orders reveal whether demand is contracting under policy uncertainty. JOLTS completes the picture with the openings-to-unemployed ratio that the Fed uses to assess labor market slack.

Friday is the week’s anchor: March Nonfarm Payrolls. February was distorted by a Kaiser Permanente strike and severe weather, giving bulls a one-month excuse. If March payrolls bounce back above 100,000, the “transitory weakness” camp wins. If they print flat or negative again, the labor market deterioration becomes undeniable, and the pressure on the Fed to act, despite sticky inflation, becomes immense. ISM Services PMI that morning adds the services-sector inflation read alongside Wednesday’s manufacturing data.

zerohedge.com/markets/subpri…

1

54