Mortgage Space/ Tech/ Value/ GARP

Joined January 2022

- Tweets 3,918

- Following 665

- Followers 411

- Likes 17,083

153 Photos and videos

“I think that’s a key component of this, and you know we have done some work within our own health system within one EMR, and that’s exciting but really limited. And what Tempus was able to do is they really have created something that can go across multiple EMRs.” – Dr. Melina E. Marmarelis

From an interview published by @ASCO AI in Oncology on the #ASCO26 study, "Multi-center prospective study evaluating an AI-enabled clinical decision support tool to improve biomarker testing in early-stage NSCLC." The study demonstrated clinically meaningful improvements in biomarker testing rates following the implementation of Tempus Next.

bit.ly/4uByg5X

3

5

23

1,972

NerdcapKTD retweeted

Jun 12

Yeah. We should do a better job and we’ve made big improvements to our UX. But they are designed to help well intentioned users make good decisions about their home. We make fair offers on homes. That’s why 6X more people are selling us their homes this week than they did at this time last year. We need to 6X again. But that will take time and work.

12

27

229

26,730

Jun 10

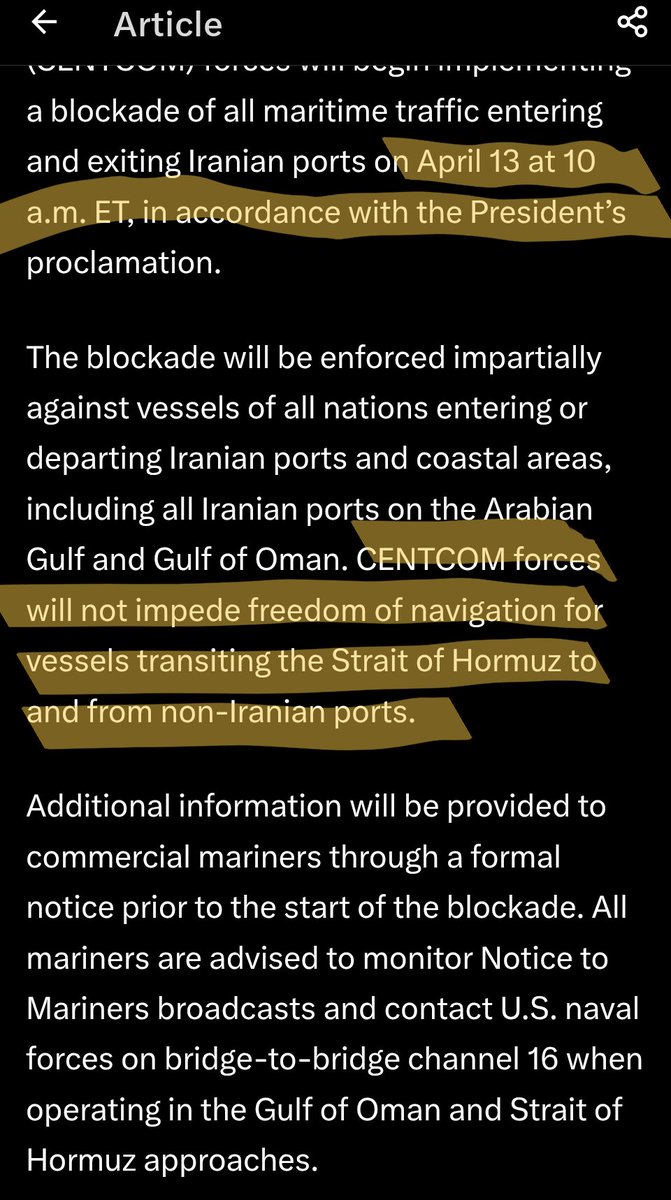

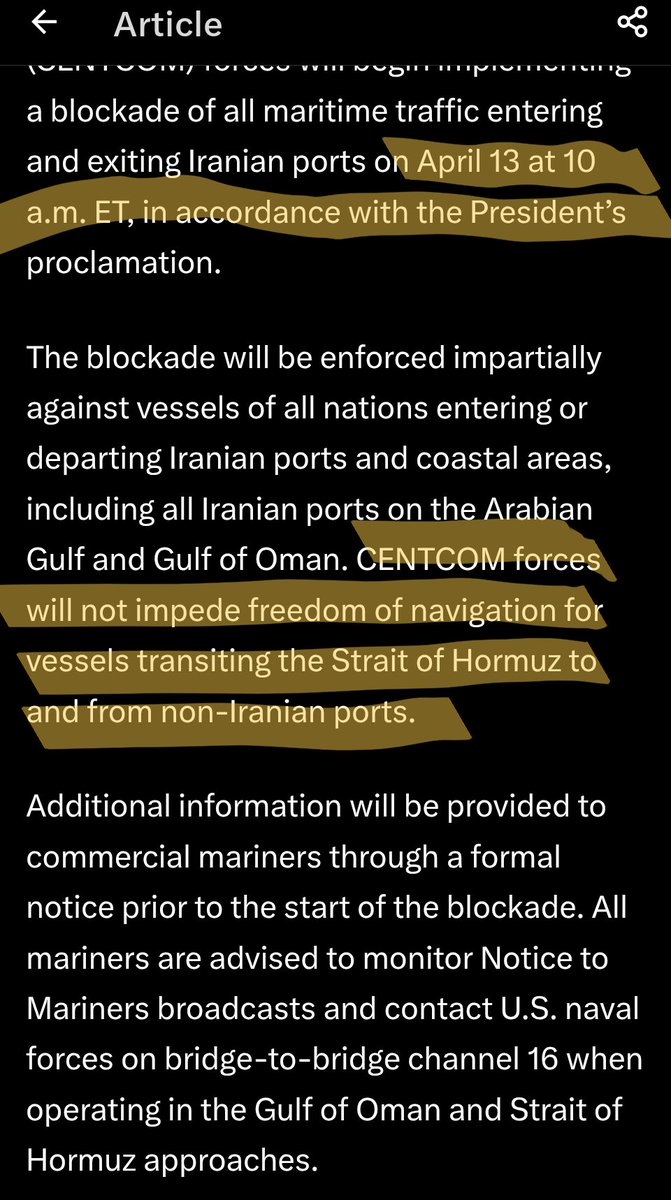

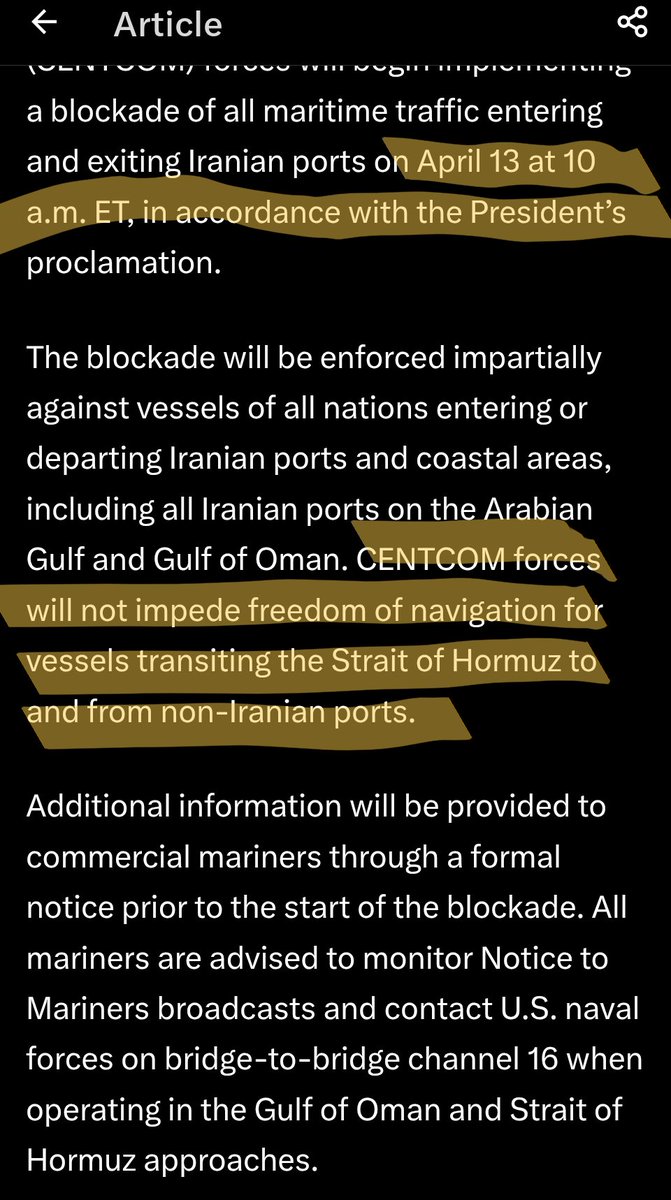

New low. Data center deal not closing on time? Final short push? Unwillingness of 2027 note holders to support refi?

$CCOI

1

2

802

Jun 10

Jun 10

✅ Major regulatory milestone!

Personalis specimen collection kits now have CE-IVD Class A marking in compliance with the EU's In Vitro Diagnostic Regulation.

The Personalis EDTA Blood Collection Kit & cfDNA Blood Collection Kit can now be used across EU & Great Britain for interventional studies.

This enables global deployment of ultrasensitive MRD testing for drug development programs. 💪

Full details: bit.ly/4ofHX8F.

#PrecisionOncology #IVDR #DrugDevelopment #RegulatoryAffairs #ClinicalResearch #ClinicalTrials #Pharma #MRD

185

Jun 10

Could go faster with additional data center sales. Leverage sub 4x is clear line of site and I'd prefer to see additional balance sheet strength prior to dividend restoration. $CCOI

Jun 9

It's going to take until 2028 for the stock to recover back to $50 and that assumes that they get to $300 million in wave revenue and they bring back most of the dividend payout. Remember that the stock was mainly supported by the dividend in prior years.

3

3

1,258

NerdcapKTD retweeted

Jun 9

🚨 BREAKING: $OPEN acquisition contracts surge again

🏠 564 contracts this week

📈 31% WoW

📅 78 contracts same week last year

That’s a 623% YoY increase.

Meanwhile:

• Agent partnerships are scaling

• Seller offers are more competitive

• New products are rolling out weekly

• AI is driving operational efficiency

• Russell 3000 inclusion is just days away

17

56

368

32,276

NerdcapKTD retweeted

Jun 8

3

3

73

7,718

NerdcapKTD retweeted

Jun 8

Incredible to see two of the top pharmaceutical CEOs in the world, Pascal Soriot, CEO of AstraZeneca, and Rob Davis, CEO of Merck, highlight their strategic partnerships with Tempus to bring the power and promise of artificial intelligence to oncology:

cnbc.com/2026/06/05/astrazen…

merck.com/wp-content/uploads…

7

9

77

8,774

Jun 8

Worth a read if you are interested in $PL. I personally trimmed at $44 and $51 and rebought everything I trimmed plus some at $33 on the atm fear. They have the daily scan data set for real time AI modeling on geospatial intelligence.

2

263

NerdcapKTD retweeted

Jun 4

@planet Q1 earnings recap! Record revenue, third consecutive quarter achieving Rule of 40 and most of all, 42% YoY growth, which every HHGTTG listener knows is the answer to life, the universe, and everything 📖👽!

Check it! investors.planet.com/news/ne…

18

20

139

15,713

Jun 4

Jun 4

This was our 10th year at ASCO and it's incredible to think about how much we’ve grown since our first. This year marked our largest collection of accepted research to date, with record attendance at our industry expert theater and lines at our demo stations. All of that momentum channels into one goal: bringing the promise of technology to precision medicine to help patients live longer and healthier lives.

1

205

NerdcapKTD retweeted

Jun 3

I think I said the best way to judge the company is across three management objectives. I said that a few weeks after I took over. Those where 1) can we scale acquisitions 2) can we improve unit economics and resale velocity while reducing aged inventory and 3) can we build operating leverage (i.e. make sure our contribution margin could cover our fixed cost by increasing former and holding latter steady).

on 1) 500%ish YoY, and Q1 2026 was the highest acq since 2022 and double Q4 2025.

on 2) % of homes on the market over 120 Days declined from 51% when I took over to ~10% last quarter, over the same period the market went the other direction and went from like 20%ish to 33% ish. Contribution Margin has improved every single month since my first day and March was the highest contribution margin in any quarter for some time. October, November, December, and January cohorts are each selling faster than any corresponding cohort since COVID.

on 3) Fixed opex was down both QoQ and YoY. And trailing 12 moth opex as a % of revenue is steady at 1.3% QoQ and since CM is up we are going in the right direction.

Those are the financial numbers, but also if you look at the people who are coming into Opendoor - they are exceptional and I'd put them up against any tech company. If you look at our shipping velocity, it is higher than it is has been in years (possibly ever?). We went from 35% of the market to 95% market in coverage. Our capital light product went from 0 to a third of our volume. etc. etc.

48

117

845

85,047

May 29

Boomers destroyed the economy for everyone coming up under them and younger generations are absolutely sick of subsidizing their lifestyle.

May 28

Property taxes are unrealized capital gains. It’s a wealth tax. They hurt seniors and those on fixed incomes the most. There are those who think that it’s good public policy to get seniors out of their family homes in order to “churn the market,” and make room for new home buyers. Those who advocate such a position place less importance on private property rights, and family stability.

1

79

May 29

💯

May 28

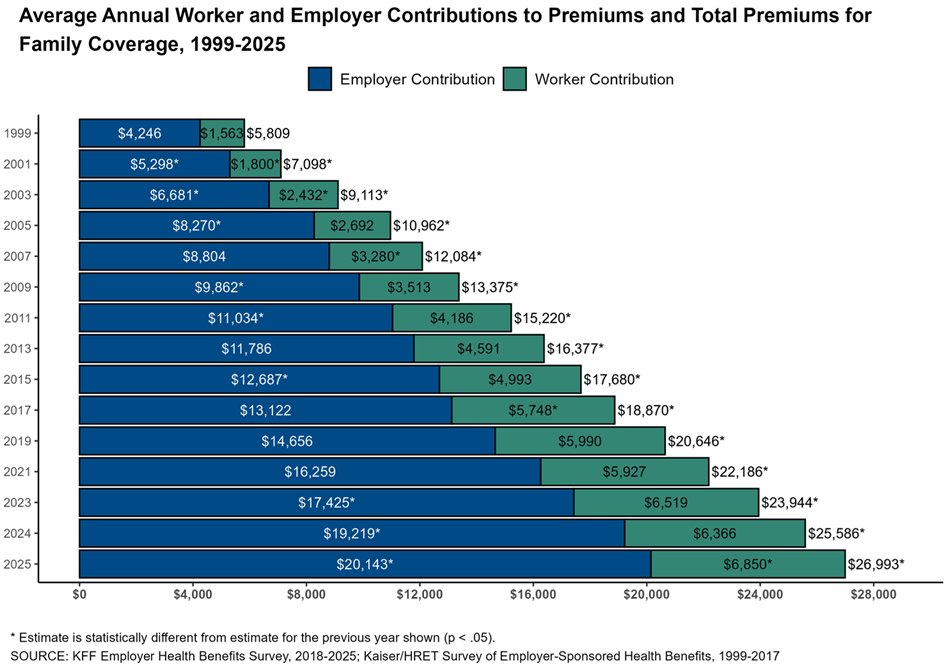

Nearly $27,000 a year for family health insurance premiums, up from $6,000 in 1999.

And that’s before deductibles, copays, and surprise bills.

The system is fundamentally broken.

1

92

May 29

A lot of the boomers also have inflation adjusted pensions the younger generations continue to pay for and are not offered.

May 28

Social security is inflation adjusted.

Medicare is taxpayer provided

The mortgage is paid off.

You're not raising kids.

You can afford a property tax bill which averages out to 1% of the equity you could withdraw from the house.

1

66