Digital infrastructure for product provenance, traceability, and verified sustainability reporting. Build on @Hedera. @GoogleCloud sustainability partner.

Joined March 2016

- Tweets 2,666

- Following 27

- Followers 1,423

- Likes 800

367 Photos and videos

NoviqTech retweeted

May 28

$NVQ NoviqTech starts harvesting and pyrolysis trial at Great Barrier Reef Biochar Project tinyurl.com/29kpk3mg @noviqtech_ #NVQ #63Q0 #NVQLF #ASX #ASXNews

2

2

529

May 28

Coralia begins harvesting invasive Chinese Apple trees for @NoviqTech_ Great Barrier Reef Biochar Trial targeting Puro.earth certification by Sep 2026 $NVQ

stockwirex.com/asx-stock-new…

2

3

725

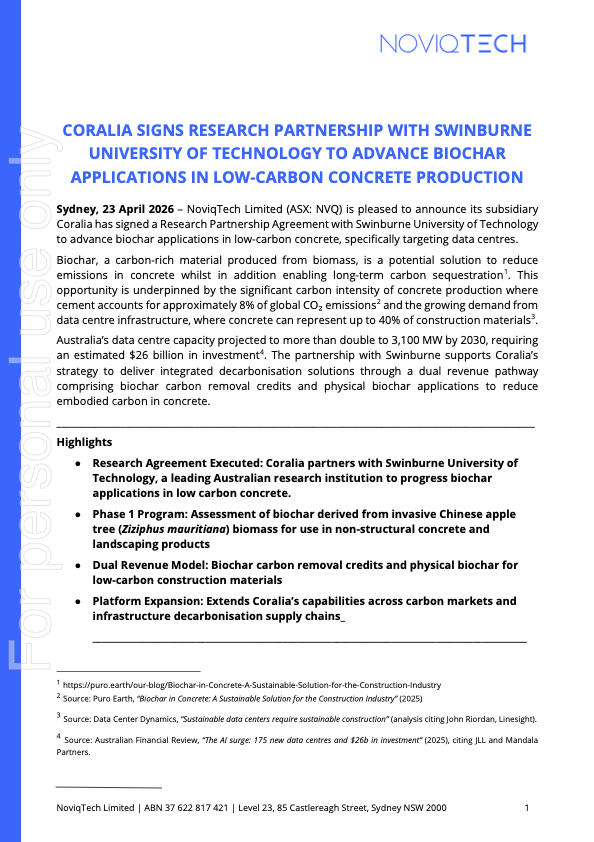

Apr 23

Apr 23

$NVQ Coralia teams with Swinburne to advance biochar concrete push for data centres tinyurl.com/2a4x5b5g @noviqtech_ #NVQ #63Q0 #NVQLF #ASX #ASXNews

2

329

Apr 23

Apr 22

NoviqTech’s $NVQ subsidiary Coralia inks Swinburne deal to test invasive-apple biochar in low-carbon concrete for data centres, targeting…

smallcaps.com.au/article/nov…

2

280

Apr 22

$NVQ subsidiary Coralia has signed a Research Partnership Agreement with @Swinburne to advance biochar in low-carbon concrete for data centre construction. Cement accounts for ~8% of global CO₂ emissions. Data centres rely heavily on concrete.

Biochar offers a pathway to reduce emissions while enabling long-term carbon sequestration. Full ASX announcement here: cdn-api.markitdigital.com/ap…

5

204

Apr 22

8% of global CO₂ from cement as @NoviqTech_ partners with Swinburne to develop biochar low-carbon concrete for data centres $NVQ

stockwirex.com/asx-stock-new…

1

4

254

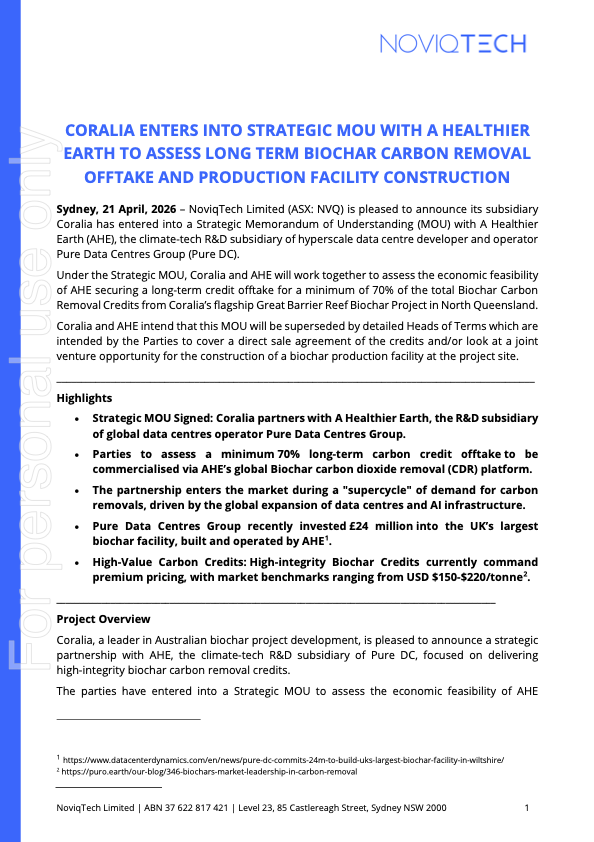

NoviqTech retweeted

📈 $NVQ NoviqTech shares soared 58% after its subsidiary Coralia entered into a MOU with 'A Healthier Earth' to assess long-term biochar carbon removal offtake & production facility construction at the Great Barrier Reef Biochar Project 🤝

@NoviqTech_

🔗 cdn-api.markitdigital.com/ap…

1

3

10

747

Apr 21

$NVQ Our subsidiary Coralia has entered into a Strategic Memorandum of Understanding (MOU) with A Healthier Earth (AHE), the climate-tech R&D subsidiary of Pure Data Centres Group.

The agreement focuses on assessing long-term biochar carbon removal offtake and production infrastructure.

Full details in the announcement: cdn-api.markitdigital.com/ap…

1

1

9

319

NoviqTech retweeted

70% offtake assessed as @NoviqTech_ signs biochar carbon removal MOU with Pure Data Centres' climate-tech arm $NVQ

stockwirex.com/asx-stock-new…

2

5

234

Apr 6

$NVQ A leading chemical recycling facility in Northern Territory chose Carbon Central to structure and verify its sustainability data. In this video, we show how Global Resource Recovery NT tracks emissions, tokenises each recycled batch and provides auditable proof across its value chain, all within one coherent system. Watch here: youtu.be/0l9kbAEdNfw

#CircularEconomy #ResourceRecovery #CarbonReporting

1

1

312

Mar 30

Singapore’s climate framework combines ambition with enforcement.

The Green Plan 2030 sets direction. The carbon tax creates a price signal that escalates quickly. Mandatory climate reporting aligns companies with recognised standards and introduces external assurance on emissions data.

This article breaks down how Singapore’s climate commitments translate into concrete obligations, including carbon pricing, reporting timelines and the role of SAF as aviation decarbonisation scales.

Read the full analysis: noviqtech.com/articles/singa…

62

Mar 23

$NVQ Every credible carbon claim begins with one question: how strong is the data behind it? In this video, we explore how #MRV operates in practice and why it anchors trust across carbon markets. Carbon Central supports this structure by capturing operational data directly, aligning calculations with recognised methodologies and securing records through tamper-evident systems that preserve provenance over time. Watch the full video here: youtu.be/1NeEJ5BiT5g

#CarbonMarkets #SustainabilityData

1

2

294

Mar 16

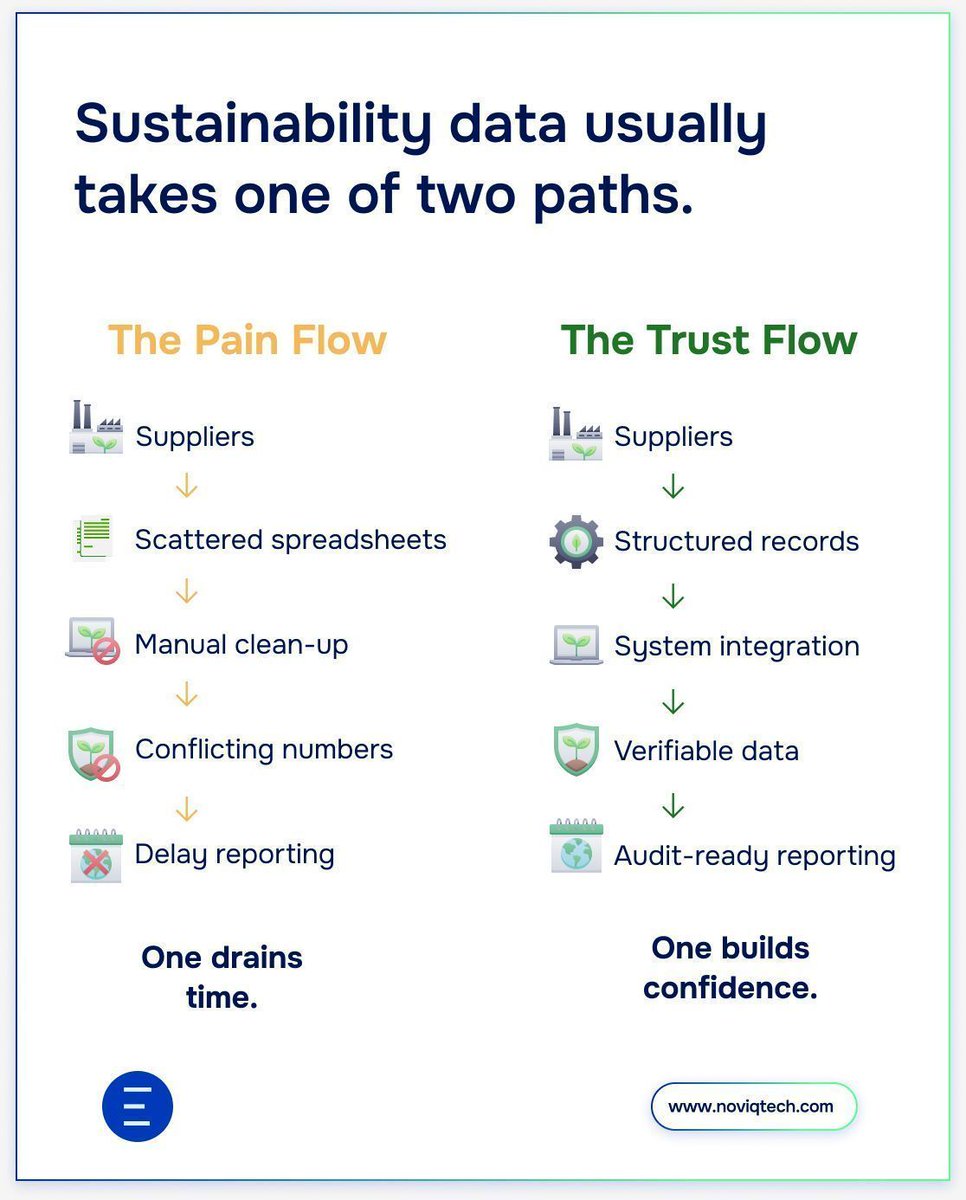

Carbon reporting influences how a business is evaluated and the expectation is clear: emissions data must be structured, traceable, and supported by verifiable records. This short video looks at the data infrastructure that helps sustainability, finance, and operations teams manage reporting with greater clarity and control. Watch the full video:

youtu.be/UovLK_fBXWk

$NVQ #CarbonReporting

1

103

Mar 11

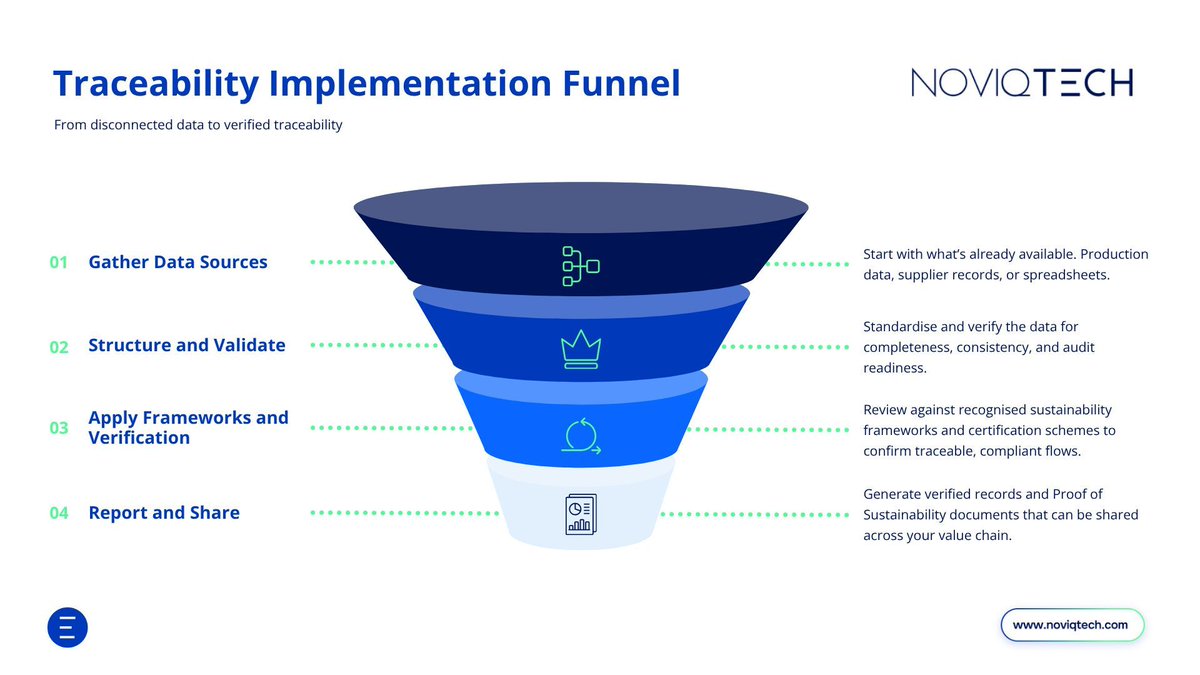

The challenge in proving sustainability performance across complex supply chains usually begins long before verification. It starts with internal systems. Our new article outlines the operational issues that shape sustainability data inside these supply chains. These conditions shape the reliability of the final sustainability information and determine whether teams spend more time analysing insights or assembling inputs. Read it here:

noviqtech.com/articles/provi…

#SustainabilityData #SupplyChain #CarbonReporting $NVQ

1

76

Mar 9

$NVQ Carbon data becomes powerful when it reflects operations. Our video explores the Carbon Central Digital Twin and how it creates a structured model of physical operations. Emissions, renewable energy production and sustainability metrics are recorded against actual activity, giving teams clarity across the full lifecycle. Watch the full video here: youtu.be/-D4YzRV5irU

3

255

Mar 8

Most SAF traceability gaps come from mismatched data and disconnected systems across producers, verifiers and buyers. Real traceability happens when everyone works within the same framework; using recognised standards, integrated systems, and clear accountability across the chain. If you’re building or scaling your SAF verification processes and want to make alignment easier, reach out to our team.

$NVQ #SAF #ChainOfCustody

1

57

NoviqTech retweeted

Coralia secures Data Centres Australia membership as @NoviqTech_ targets low-carbon cement for AI infrastructure and CDR credits for hyperscalers. $NVQ

stockwirex.com/asx-stock-new…

1

1

144

Mar 3

Europe’s aviation sector now has a clear flight path for decarbonisation. The ReFuelEU Aviation Regulation sets binding Sustainable Aviation Fuel (SAF) targets for fuel suppliers and aircraft operators; with reporting, verification, and penalties built in. This article walks through how the regulation works in practice. Read the full breakdown: noviqtech.com/articles/refue…

$NVQ #RefuelEu #SAF

2

65

Mar 2

You’ve probably seen the emissions number on your flight and thought… “ok but how?”

There is a real method behind it, and the new video walks through it step by step.

Clear, simple, no jargon. Watch it here: youtu.be/LLqdSdj22JA

$NVQ

182

Mar 1

At scale, SAF claims might stand or fall on three things:

• Documented inputs entering the system.

• Controlled allocation of sustainability attributes.

• Clear records of when claims are issued and retired.

These mechanics sit behind mass balance and book and claim models, and they shape how regulators, buyers, and certification schemes assess SAF claims in practice.

This is the point where traceability moves beyond a technical consideration and becomes a condition for market participation.

We support SAF traceability across production data, allocation logic, and reporting, so records remain consistent as volumes increase.

How are SAF claims structured and tracked in your current setup?

1

69