649 Photos and videos

Beyond the Models Everyone Else Still Uses

The models are not wrong because nobody noticed. They are wrong because replacing foundations is harder than adding parameters.

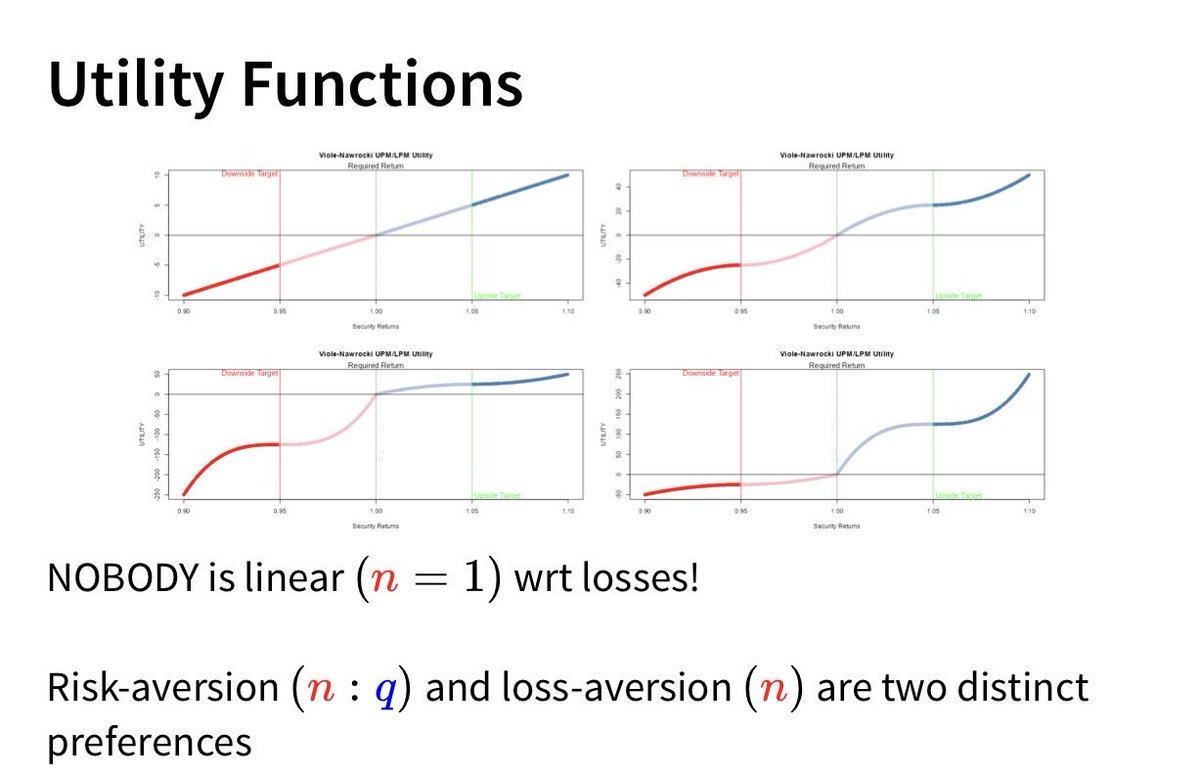

❌ Mean-variance assumes quadratic utility.

❌ Pearson correlation reduces all dependence to a single linear number.

❌ Parametric distributions impose structure markets do not naturally satisfy.

At OVVO Labs, we asked a different question:

What if quantitative finance were rebuilt without forcing markets into assumptions they do not naturally satisfy?

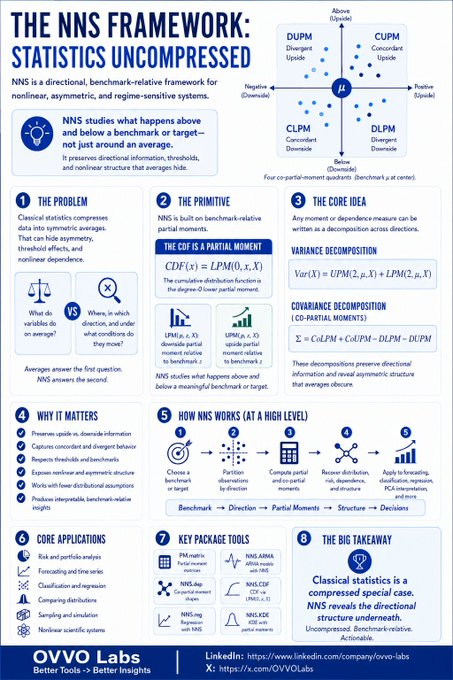

The result is a unified framework built on partial moments and nonlinear nonparametric statistics. Mean, variance, skewness, kurtosis, covariance, and even the empirical CDF are all special cases of one broader mathematical structure. Not a collection of tools. A coherent alternative to the parametric foundations the entire industry inherited by default.

That single foundation powers three production-grade applications.

✳️ Options Pricing

Call = upper partial moment.

Put = lower partial moment.

No lognormality assumption. No dependence on a calibrated volatility surface. Honest confidence intervals from the actual empirical distribution tested live against real market prices, including on the days when assumptions matter most.

✳️ Portfolio Optimizer

Embeds your utility preferences directly into the covariance structure using four directional quadrants of dependence. Captures crash dependence and asymmetric tail behavior that Pearson correlation was never designed to see. Two assets can show zero correlation and still crash together every time. Standard optimization misses it. This one does not.

✳️ MacroNow

Nonparametric vector autoregression across 30 Federal Reserve variables. No arbitrary lag selection. No stationarity assumptions imposed on data that does not satisfy them. Built for live nowcasting, not retrospective fit.

Harry Markowitz reviewed this work over multiple years of correspondence and wrote:

"I agree that your approach is more general than old-fashioned mean variance... I wish you the best in getting your ideas out."

That is not a marketing slogan.

That is the founder of modern portfolio theory acknowledging that mean-variance (the framework every institution on Earth still uses) is a special case of something more general.

The full suite is priced at a fraction of a single Bloomberg terminal. A fundamentally different way to approach pricing, portfolio construction, and macro forecasting, built on decades of original research, unified under one mathematical framework, and available today.

Try the live tools here → ovvolabs.com

Markets don’t care about your assumptions. Neither do we.

3

2

916

OVVO Labs retweeted

Jalen Brunson joins Kareem, Magic, MJ, Bill Walton as the only players to win:

🔸NCAA title

🔸Naismith college player of year

🔸NBA title

🔸NBA finals MVP

Community note

Magic Johnson did not win the Naismith College Player of the Year award; Larry Bird won it in 1979. en.wikipedia.org/wiki/Naismith_… naismithtrophy.com/winners espn.com/mens-college-b…

176

3,768

19,209

816,784

OVVO Labs retweeted

From Nova to Nueva York 🤝

Jalen Brunson, Mikal Bridges, & Josh Hart are the 1st teammate trio to win both an NCAA title (2016 Villanova) & an NBA title (2026 Knicks),

59

2,357

12,043

309,470

If YOU can launch an AI trading agent and YOU bring NOTHING to the table, then neither does your AI trading agent. Slop in. Slop out.

#shortthemall #nonstationaritymeteor

16

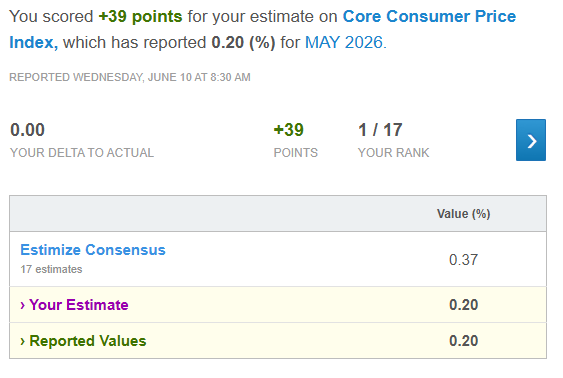

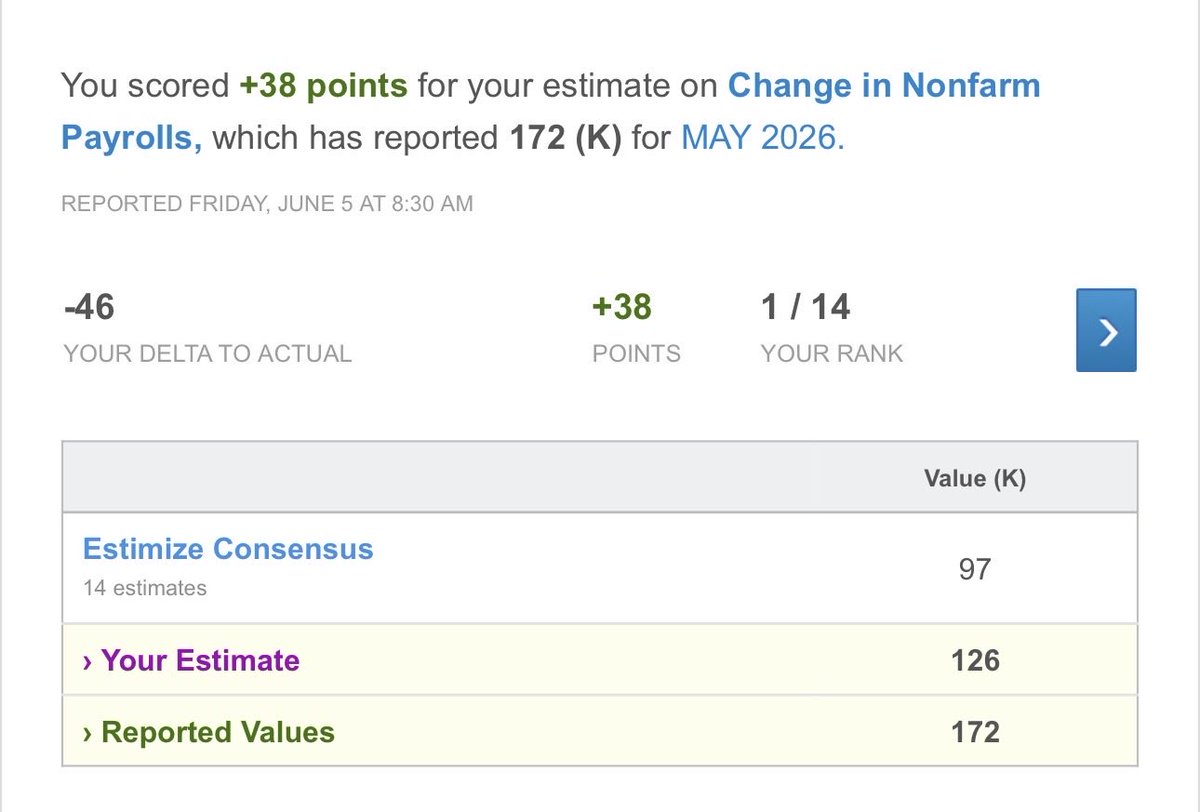

Stronger than consensus #NFP. (lnkd.in/eKyYkENR)

Weaker than consensus #CPI. (lnkd.in/ezrhYuwr)

Both non-consensus.

Both right. ✅

That is exactly what #MacroNow from OVVO Labs was showing.

With 30 macro variables updating twice daily, #MacroNow is built for traders & allocators who need more than consensus, headlines, or generic AI summaries.

You won’t get this from a Bloomberg terminal alone.

And you’re definitely not getting it from a vibe-coded knockoff.

Give your AI a brain for a fraction of the cost.

#Nowcasting #Quant #Macro

1

1

98

Huge unlock for NNS v13.0 🚀

I figured out a tensorized partial moment architecture that makes the core NNS routines dramatically faster while preserving the package’s nonlinear, nonparametric foundations.

This release brings major speedups across partial moments, PM matrices, CDFs, VaR routines, multivariate regression internals, and numerical moment calculations.

Install it from GitHub and let me know what you think:

github.com/OVVO-Financial/NN…

21

Great point that helped me resolve Prospect Theory within Expected Utility Theory!

See following summary:

github.com/OVVO-Financial/Fi…

Jun 6

The great @UOTMENTOR Mickey Hoffman taught 6500 traders in his career at the University of Trading in the floor of the CME pit the most important parts of a trade are your outs, or know your “last trade first”. Before you take a trade, you must know where you will get out for a loss, where you will take profit. Age old wisdom from a man i love and who has been lile a father to me.

1

1

124

40

Seeing upside where others did not...🎯 🥇

With 30 plus macro variables updating twice daily, #MacroNow is built for regimes like this. Standalone or as an ensemble input, the value add is obvious.

Macro is important for trading, see how ovvolabs.com can augment your trading toolkit!

119

1

1

704

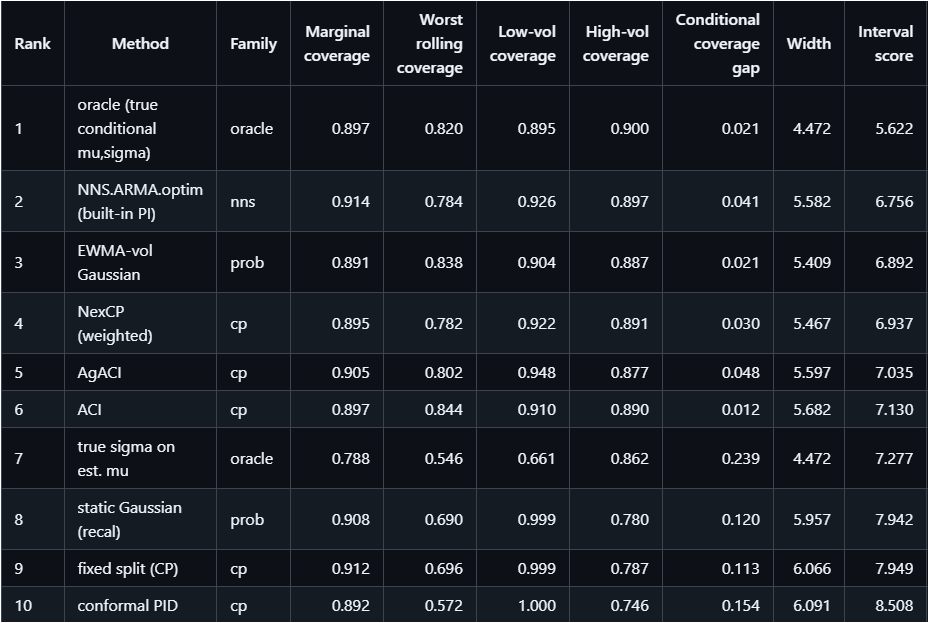

NNS Time-Series Prediction Interval Benchmark

Final Verdict:

If the computational overhead is acceptable, especially with parallelized cores, NNS.ARMA.optim is an elite choice for time-series uncertainty quantification. In this experiment, it delivered the best non-oracle interval score while maintaining near-target marginal coverage and strong high-volatility coverage.

The main advantage is that NNS does not require a separate two-layer architecture of “base model plus conformal wrapper” to obtain adaptive prediction intervals. Its native time-series procedure estimates seasonal structure with NNS.seas(), updates through walk-forward training, and produces prediction intervals directly from the fitted NNS forecasting process.

Adaptive conformal methods such as ACI and NexCP remain valuable calibration tools, and ACI achieved the tightest volatility-stratified coverage in this benchmark. But NNS achieved the strongest overall efficiency among empirical methods, with sharper intervals than the conformal alternatives and coverage behavior that remained competitive across volatility regimes.

The practical conclusion is that NNS is not merely an alternative point forecaster requiring post-hoc calibration. It is a native nonlinear, nonparametric forecasting framework that can produce highly efficient, naturally adaptive prediction intervals directly.

Full experiment: github.com/OVVO-Financial/NN…

78

I recently saw examples of AI cracking long-standing Erdős-style problems, and it made me revisit something I’ve been thinking about for over a decade.

Ten years ago, I wrote a paper titled “Beyond Correlation: Using the Elements of Variance for Conditional Means and Probabilities.”

The core idea was simple but powerful: instead of treating correlation as the fundamental primitive, partition the joint distribution into the four partial-moment quadrants (CUPM, CLPM, DLPM, and DUPM). Each quadrant has its own conditional mean. Those means, I showed, generate exact conditional expectations without ever assuming a correlation structure.

But I always suspected something deeper was hiding there. I felt the quadrant conditional means had to be directly connected to eigenvalues and eigenvectors.

That connection just became explicit, and it goes even further than I imagined.

The result:

Centered, probability-weighted quadrant means form rank-one spectral primitives.

The full covariance matrix then decomposes exactly as: between-quadrant conditional-mean displacement within-quadrant residual covariance.

In other words: PCA can be recovered perfectly from the NNS quadrant decomposition.

PCA diagonalizes covariance. NNS explains where the covariance came from.

And the bonus?

Once you index those same quadrants through time, the identical structure produces a fully observable analogue to a Hidden Markov Model, except the regimes are not hidden. They are directly observed directional states (CUPM → CUPM, CLPM → CUPM, CLPM → CLPM, etc.). You get the full transition matrix and dynamic spectral attribution for free.

So instead of inferring latent regimes and then trying to interpret them (classic HMM), the directional framework defines interpretable regimes first, then measures their dynamics and their exact contribution to every eigenvalue.

This is why partial moments matter!

PCA identifies the dominant axis. Directional decomposition identifies the regimes that created it.

Full technical note is here: github.com/OVVO-Financial/NN…

102

20 Jul 2023

What’s your edge?

2

91