A platform that democratizes the procurement processes, enhances collaboration among stakeholders (MDAs, Contractors & Citizens) to achieve project deliverables

Joined January 2023

- Tweets 2,435

- Following 19

- Followers 67

- Likes 2,648

47 Photos and videos

Open Projects | Tools | Collaboration | Governance retweeted

Creativity is inventing, experimenting, growing, taking risks, breaking rules, making mistakes and having fun”

- Mary Lou Cook

@TechpointAfrica

@truorganicafric @Proximateagro @MarvelStudios @technextdotng @FAOKnowledge @FAOclimate @FAOForestry @GlobalGoalsUN @vitabridgeinfo

8

1

1

Open Projects | Tools | Collaboration | Governance retweeted

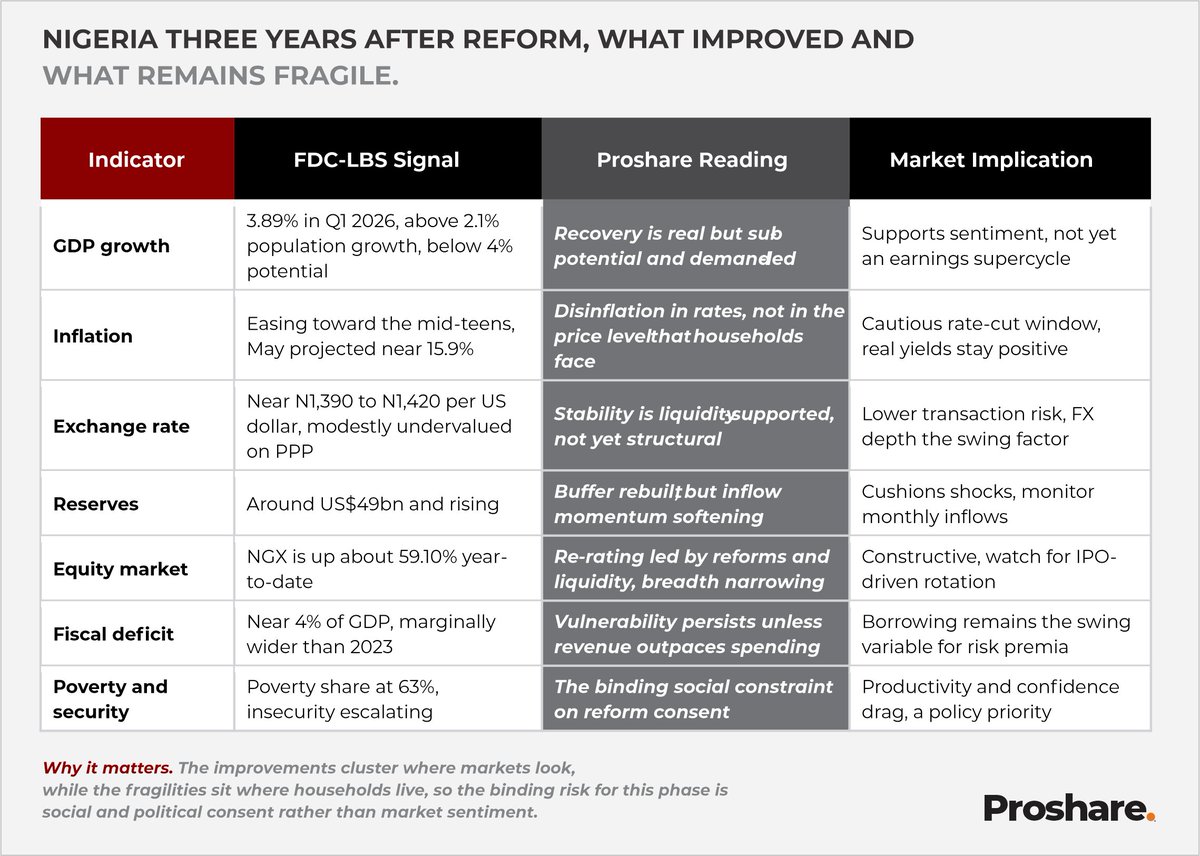

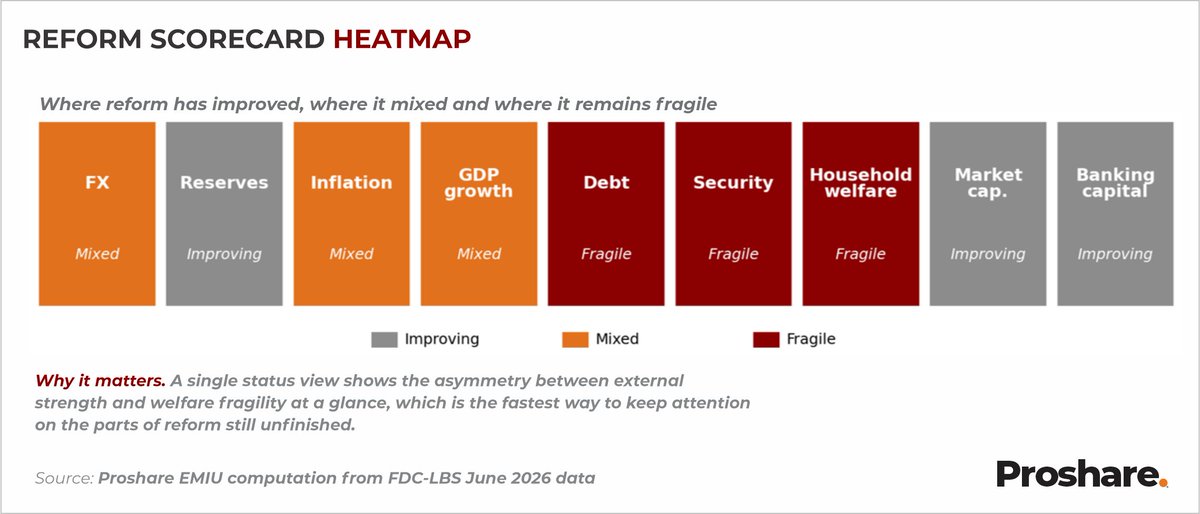

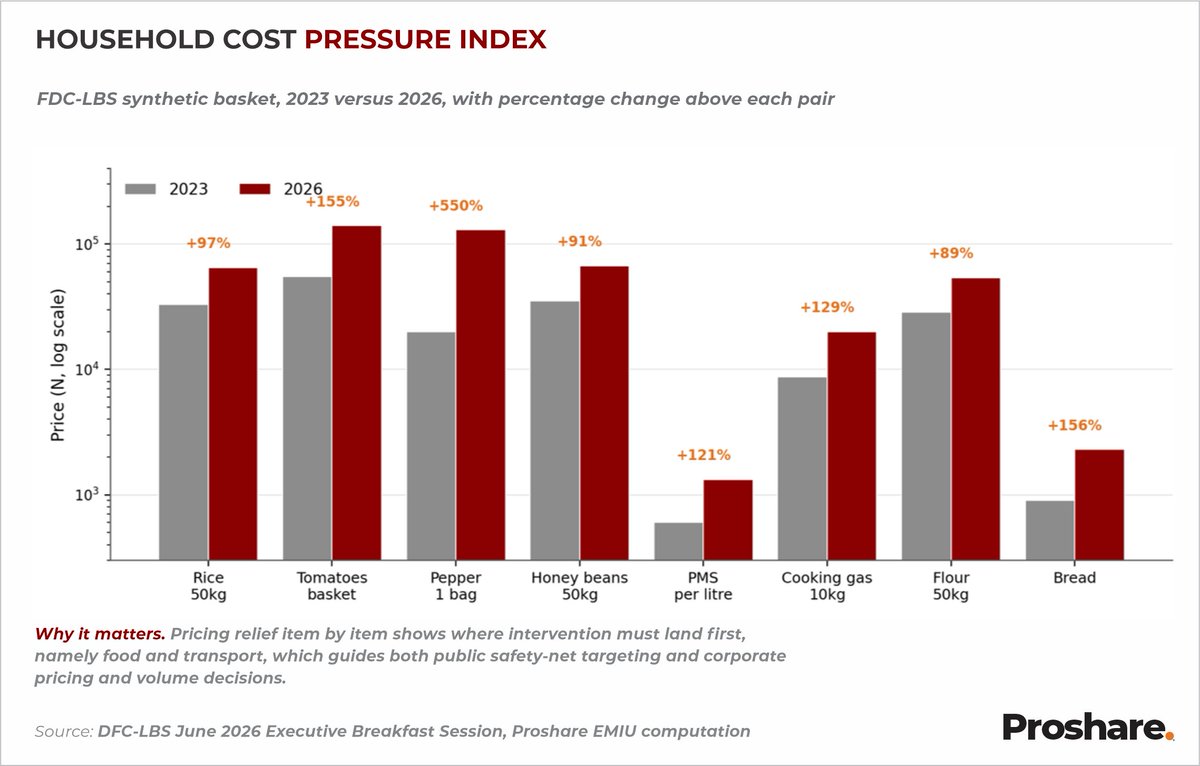

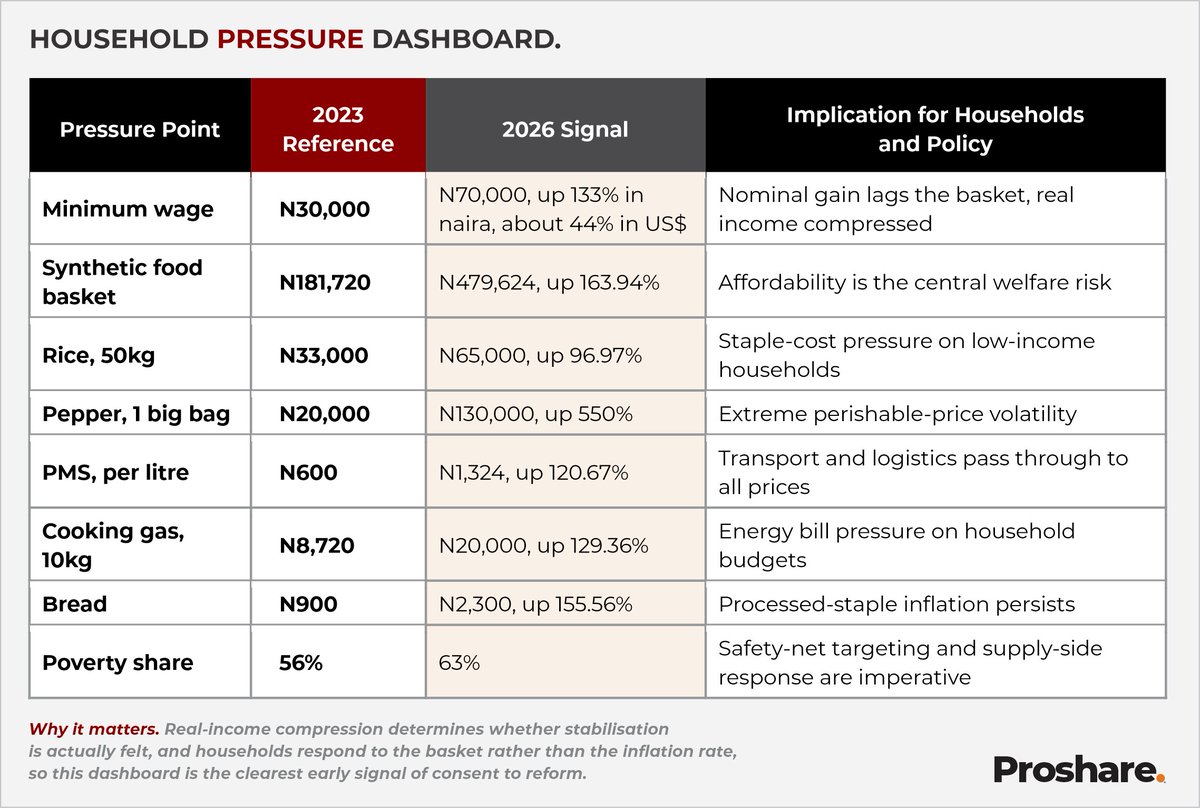

"The gains are real. A more credible exchange rate, rebuilt reserves, sovereign upgrades from S&P and Moody's, the reinstatement of FTSE Russell frontier indices, the FATF grey-list exit, banking recapitalisation, and a re-rating of the equity market all point to restored external confidence. The pain is also real, concentrated in food, fuel, transport, power and rent, with the poverty share higher and insecurity escalating."- @proshare

"Three years into the reform programme that began with subsidy removal, foreign-exchange market liberalisation, tax reform and trade liberalisation, the FDC-LBS reading is deliberately balanced, weighing the period as 15% cheers, 30% tears and 55% fears." - @FDC_ltd in their June 2026 report referenced here proshare.co/articles/june-20…

The FDC-LBS Breakfast Session, presented monthly by @BJRewane of Financial Derivatives Company, functions as a signal document for markets and policymakers. It reads the month through the combined lens of macroeconomic data, household prices, market structure, and global risk, and is closely followed by investors, regulators, corporate planners, and household decision-makers across Nigeria.

The June 2026 edition places Nigeria at the intersection of reform credibility, household stress, public health risk, global geopolitical shocks, fiscal pressure, and capital market repricing, and offers a timely market and policy assessment of Nigeria, three years after reform. It opens with the economic implications of a renewed #Ebolaoutbreak in the Democratic Republic of Congo, moves through the third anniversary of the subsidy, exchange-rate, tax, and trade reforms, and closes with a stock market that has climbed against a difficult backdrop.

The central judgement is that the country has moved from the emergency phase of adjustment into an execution phase, where nominal stabilisation must now translate into real household relief, capital productivity, fiscal discipline, private investment, stronger security outcomes and credible institutional delivery.

The gains are real. A more credible exchange rate, rebuilt reserves, sovereign upgrades from @SPGlobalRatings and @moodysratings's, the @FTSERussell frontier reinstatement, the FATF grey-list exit, banking recapitalisation and a re-rating equity market all point to restored external confidence. The pain is also real, concentrated in food, fuel, transport, power and rent, with the poverty share higher and insecurity escalating. The financial sector is shifting from recapitalisation compliance to capital productivity, which makes governance, asset quality and credit allocation more decisive than headline capital. The Dangote Refinery is a genuine structural change for trade, FX and market depth, yet its prospective listing calls for valuation discipline and market-absorption realism. Ratings and reclassification are credibility, not a substitute for delivery.

In this review, we highlight the key takeaways from the presentation and connect them to Proshare's recent work on banking credit, sovereign ratings, and the household test.

proshare.co/articles/june-20…

7

103

142

14,005

Open Projects | Tools | Collaboration | Governance retweeted

Jun 7

8 days left for Active Citizens Awards nominations.

That person or organisation doing the real work in your community, have you nominated them yet?

Don’t let them go unnoticed. Send in your nomination at awards.civichive.org.

#ACA2026 #ActiveCitizensAwards

8

13

854

Open Projects | Tools | Collaboration | Governance retweeted

Jun 5

✅Stronger digital services,

✅green procurement,

✅smarter IT.

Our Greening GovTech Volume 2 report shows the policies & practices governments need to better align digital & green agendas.

Download the full report: wrld.bg/RArP50Xf5Hz

2

5

228

Open Projects | Tools | Collaboration | Governance retweeted

Jun 11

The pattern is clear. Nigeria earns, then pays debt. It earns more, then pays more debt. By the time anything is left for roads, hospitals, or schools, much of it is already gone. Read that again.

Now, let’s talk about the growing debt. In 2021, Nigeria’s debt stood at N33.1 trillion. By mid-2025, it had climbed to N149.29 trillion. That kind of growth affects how resources are allocated, what gets funded, and what gets left behind.

🎥 Watch the full breakdown of how Nigeria’s debt has grown, what is driving it, and what it means for development going forward.

#FollowTheMoney #AskQuestions

2

26

36

3,679

Open Projects | Tools | Collaboration | Governance retweeted

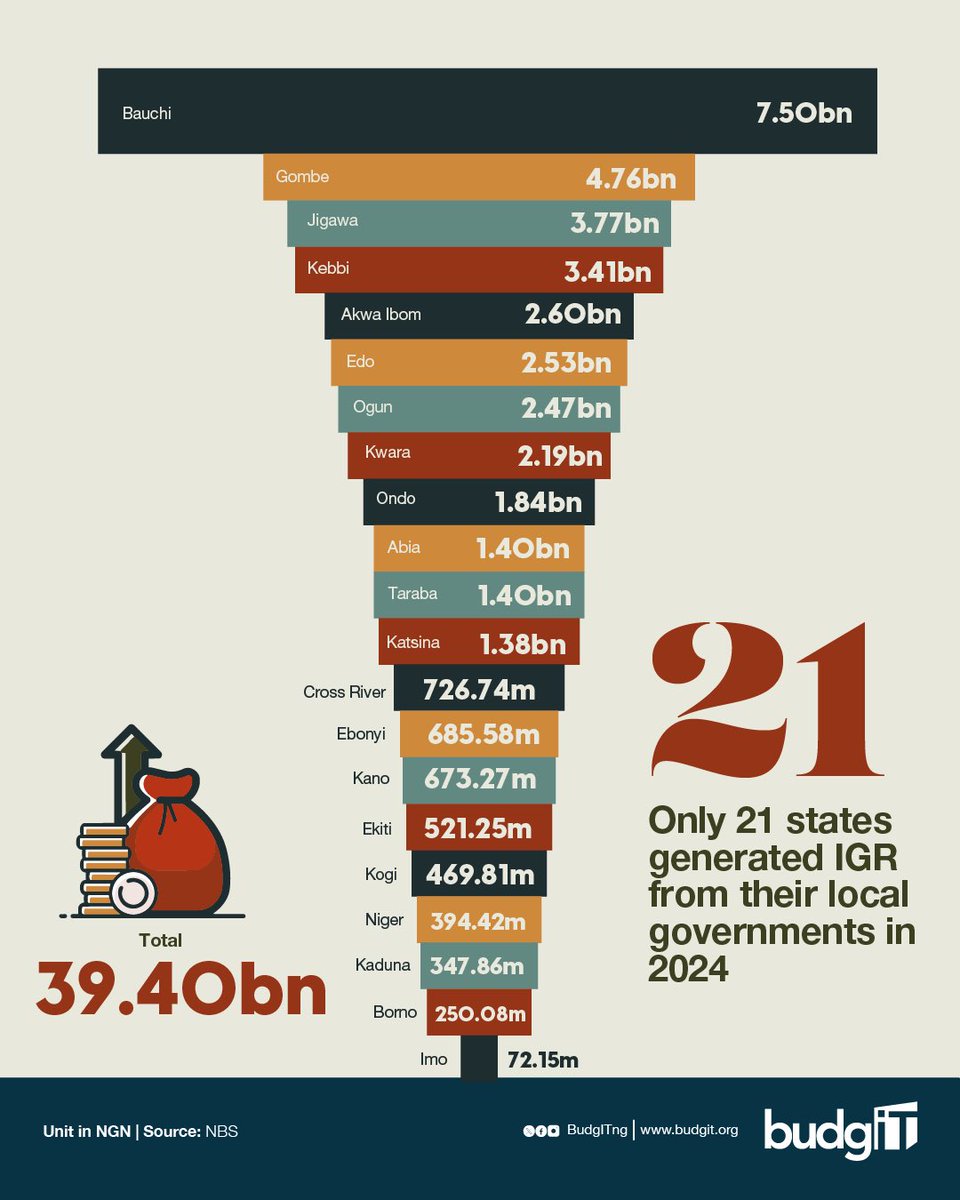

Jun 8

In 2024, only 21 of Nigeria’s 36 states reported any local government internally generated revenue (IGR). According to the National Bureau of Statistics (NBS), no figures were captured for the remaining 15.

Those 21 states accounted for N39.40 billion in total, with Bauchi on top at N7.50 billion and Imo at the bottom with just N72.15 million.

Lagos, which led the year before with N10.49 billion, did not appear on the 2024 list at all.

Local governments were granted financial autonomy in 2024. But if states still cannot account for what their councils generated under the old system, the harder question is whether autonomy will be any more transparent than what it replaced.

#GetInvolved #DataofTheDay

3

35

49

2,635

Open Projects | Tools | Collaboration | Governance retweeted

Jun 6

PUBLIC NOTICE

We have noted the recent clarification issued by the Nigerian Independent System Operator (NISO) regarding affiliation with the “Nigeria National Grid” account.

This platform has always operated independently with the objective of providing timely public information, updates, and conversations around Nigeria’s electricity sector and national developments.

We respect institutional clarifications and remain committed to factual, responsible, and public-interest reporting.

As part of our long-term vision, this platform will be evolving into a broader independent media and public affairs platform covering energy, infrastructure, economy, governance, technology, and major national developments in Nigeria.

We appreciate our community for the continued trust and support.

87

96

661

129,379

Open Projects | Tools | Collaboration | Governance retweeted

Is the Internet a human right?

What is your view?

cbm.akinbo.ng/the-cost-of-si…

@internetsociety

@ShapedInternet @hrw @HRC @HRF @ChinasaTOkolo @ISOC_Foundation @OpenSociety @OpenAllianceNG @gbengasesan @opengovpart @ParadigmHQ @OKFN @_AfricanUnion @NITDANigeria @wef @UNYouthAffairs

1

6

Open Projects | Tools | Collaboration | Governance retweeted

Looking for work-ready graduates?

Meet pre-screened Fellows and recruit at no cost at the NJFP Job fair happening in Abuja on the 4th and 5th of June 2026.

Register: events.njfp.ng/register

61

175

1,224

2,056,998

Open Projects | Tools | Collaboration | Governance retweeted

May 28

Digital government is advancing, but the World Bank’s GovTech Maturity Index shows targeted support is needed to close the digital divide. Difficulties arise where technology meets people. Read the blog for more on this: wrld.bg/iyos50Z2QNQ

4

12

275

Open Projects | Tools | Collaboration | Governance retweeted

Day two of the Observer Orientation and Briefing of the African Union Election Observation Mission (#AUEOM) to the 1 June 2026 General Elections in the Federal Democratic Republic of #Ethiopia 🇪🇹 focused on a briefing on the media landscape and the role of the media in elections, an overview of election administration by the National Election Board of Ethiopia (NEBE), that is;

• Conduct of voter registration, CVE and candidate nominations,

• Perspective on the pre-election context, positives, and challenges

• State of preparedness for the conduct of elections

It also covered election day observation, the deployment plan, the AU-EOM Aide-memoire, introduction to the use of tablets for data collection on E-Day, and observer E-Day reporting: Checklists on tablets.

4

10

28

1,745

Open Projects | Tools | Collaboration | Governance retweeted

May 29

Nigeria belongs to us all, and some people are doing more than saying it. They show up, ask the hard questions, and keep pushing for better even when no one is clapping for them.

This award is for those who speak up, who do not back down until things change, and who keep showing up.

If someone comes to mind, nominate them at awards.civichive.org

Last day to nominate: Sunday, June 14, 2026

#ACA2026 #ActiveCitizensAwards

1

17

18

1,073

Open Projects | Tools | Collaboration | Governance retweeted

📢 The Application to #Cyber4Africa Programme is open. A joint initiative by @AIHub4SD, Cyber 4.0, and @Cisco, it provides African AI start-ups with structured cybersecurity support.

📰 Apply by 8 June: bit.ly/4umyLBm

#AIHub4SD #AfricaAI #CyberResilience

17

44

3,009

Open Projects | Tools | Collaboration | Governance retweeted

Human Rights Advocacy Fellowship

Eligibilty:

• Open to students and recent graduates

• Passion for human rights and advocacy

• Interest in activism and humanitarian action

yandytech.org/fellowship/hum…

22

81

6,695

Open Projects | Tools | Collaboration | Governance retweeted

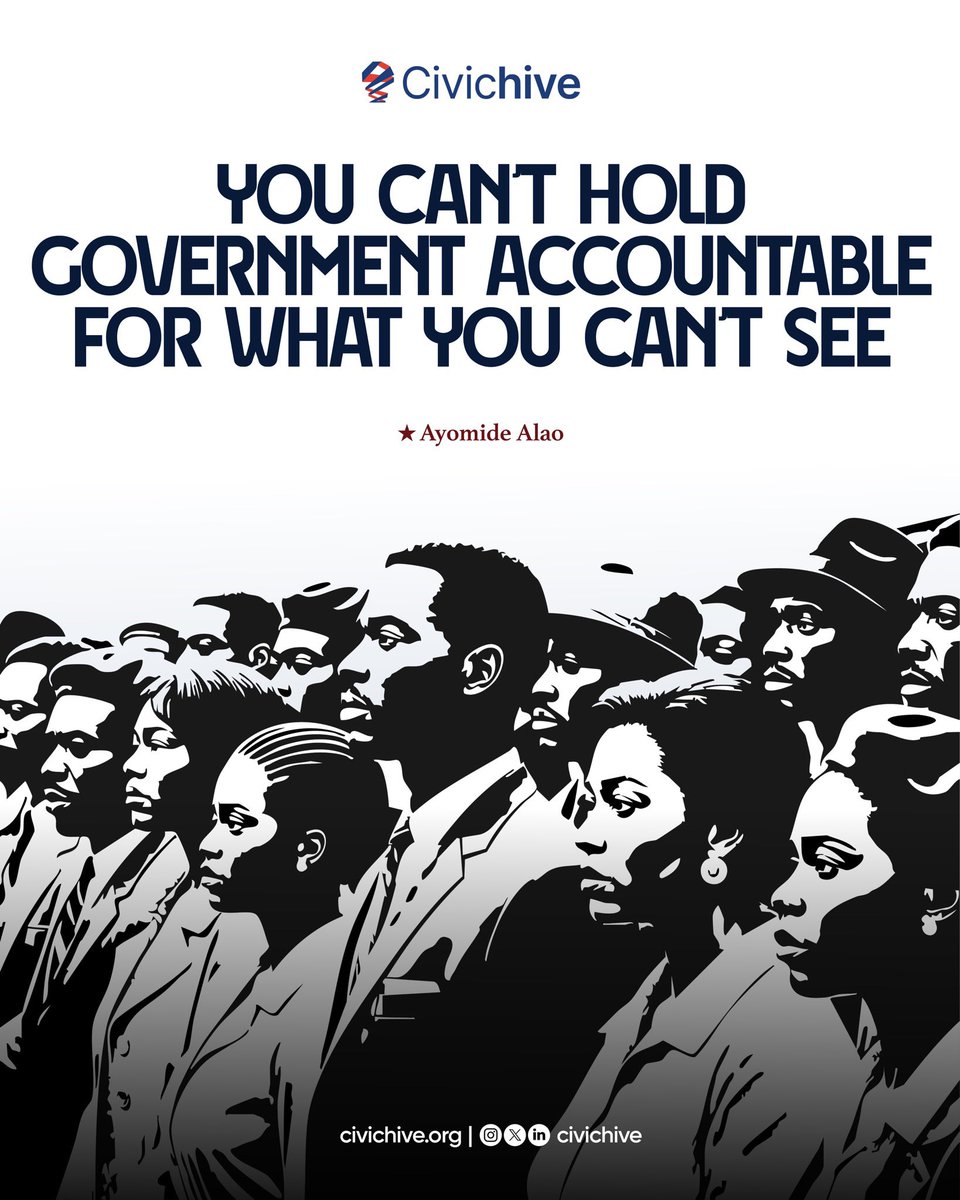

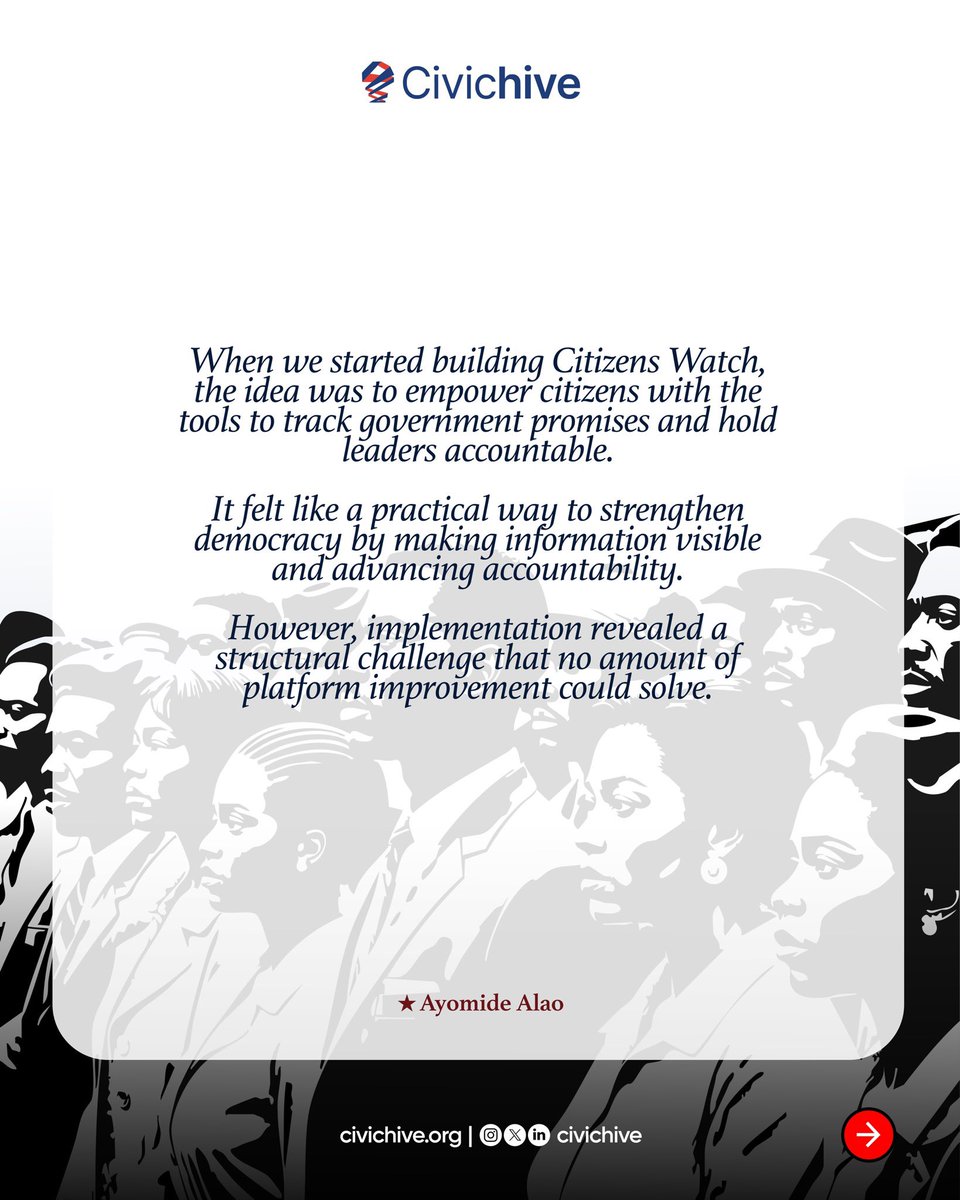

May 29

You cannot hold the government accountable for what cannot be seen or measured.

@alao_ayomide is the founder of @ReformersAfrica and the mind behind Citizens Watch, a digital platform that tracks government promises and holds leaders accountable.

1

10

11

1,023

Open Projects | Tools | Collaboration | Governance retweeted

Artificial intelligence (AI) has the potential to reshape the learning experience. Swipe through to learn more about how education can be enhanced by AI.

1

12

38

1,864

Open Projects | Tools | Collaboration | Governance retweeted

Apply Now!

Flow Fellowship 2026

📆 Deadline: 31 May 2026

🔗 Apply here: buff.ly/nTCWy7z

#Fellowship

10

58

3,736

Open Projects | Tools | Collaboration | Governance retweeted

Application closes tomorrow!🚨

Apply for the Digital Export Acceleration Program Pilot Cohory by NITDA.

Benefits of the program include;

✅Export readiness support

✅Market access guidance

✅Investor readiness support

✅Mentorship & Strategic partnerships

Open to Nigerian Businesses across tech, agribusiness, fashion, healthcare, fintech, manufacturing and much more.

Apply Now 🔗 tinyurl.com/Pilotcohort1

Application closes tomorrow. You don’t want to miss out on this!

2

11

36

2,154

Open Projects | Tools | Collaboration | Governance retweeted

Hey there, changemaker! ✨

You should totally apply for these jobs! 💁 Pick up your computer and send in your application 😉

You've got this! 💪 Don't forget to share this with your network.

1

2

33

2,117

Open Projects | Tools | Collaboration | Governance retweeted

Why attend the Summit?

Exceptional networking • Policy engagement • Skills & leadership dev’t

Early 🦅ends 30 May | Final registration: 10 June

23–25 June 2026 | Accra, 🇬🇭

Theme: “Reimagining Africa through Youth-Driven Solutions”

Register: youthsdgssummit.org

#SDGs

1

8

25

617