Joined April 2019

- Tweets 812

- Following 734

- Followers 11,204

- Likes 1,557

175 Photos and videos

Pinned Tweet

1 May 2024

🚀Big News from Opium Team!🚀

🎊

We're excited to announce that we are evolving! Opium is now pivoting to launch Zero Options (0options), reflecting our renewed focus and adaptation to the market landscape.

🎊

Register for the early access: 0options.finance

⬇️more below⬇️

17

9

39

8,739

14 Apr 2025

🔥It seems that derivatives are back and evolving fast🔥

What is the next innovation 2025?

medium.com/opium-network/def…

9

2

13

2,537

Opium retweeted

2 Mar 2025

Turns out that auditors cannot figure the algorithm from the code (surprise!), so having to write a quick document for them to understand it

29

32

371

34,967

9 Dec 2024

💹Are you actively using basis trading strategy? 💹

0%

yes, onchain!

0%

yes, centralized exchange

0%

no, I dont like it

100%

what is this?

4 votes • Final results

7

11

1,396

Opium retweeted

12 Sep 2024

Exciting innovation in DeFi from the 1inch team: seamless cross-chain swaps for users, powered by sophisticated rocket science behind the scenes! No reliance on bridges—cryptography ensures swap security 🚀🚀🚀

📄 We’ve just released our white paper on intent-based atomic swaps!

This research dives deep into how our technology simplifies cross-chain transactions by automating the process and eliminating off-chain complexities.

Read the full white paper ➡️ 1inch.io/assets/1inch-fusion…

6

1

11

2,388

1 May 2024

🚀Big News from Opium Team!🚀

🎊

We're excited to announce that we are evolving! Opium is now pivoting to launch Zero Options (0options), reflecting our renewed focus and adaptation to the market landscape.

🎊

Register for the early access: 0options.finance

⬇️more below⬇️

17

9

39

8,739

1 May 2024

Will Zero Options impact existing Opium users?

Absolutely not! No changes to decentralized protocol or governance token. We're adding KYC modules and welcome solvers and arbitrageurs. Join Zero Options for a transformative journey in accessible on-chain derivatives! #ZeroOptions

1

7

1,825

Opium retweeted

21 Mar 2024

In the first 10 minutes, we have already raised more than $3 million, about 70% of our offering.

Be fast, it won't last long 😉

realt.co/product/the-realt-r…

#RealT #RealTRaise

29

40

163

41,001

Opium retweeted

20 Mar 2024

As I said on #davos2024: DeFi and CeFi liquidity should be hybrid, as it brings better prices, compliance and less trading costs 🚀🚀🚀

Congrats @native_fi

20 Mar 2024

It's time for Native to shake up the DEX landscape.

For the 1st time, Market Makers (MMs) & Solvers will have access to on-chain credit-based trading through Native’s new product - Aqua #NativeLaunch

Aqua aqua.native.org, will bring 3 main benefits to users:

1. For Liquidity Providers: Sustainable High Yields

2. For Retail Traders: Better Pricing

3. For Market Makers: A Leap in Efficiency and Profitability

But what exactly is Aqua? ->

3

1

3

1,662

24 Jan 2024

73%

YEZZZ!

27%

WTF?

11 votes • Final results

6

2

10

2,114

Opium retweeted

8 Dec 2023

Another 🔥 DeFi opportunity just dropped for $osETH holders 🪂

Park your $osETH in the @Opium_Network Turbo Vault to earn staking rewards and option premia from the sale of covered $ETH calls.

If you’re hunting for pure ETH-based yield then look no further 👀

Details inside 👇

4

4

21

3,711

Opium retweeted

24 Nov 2023

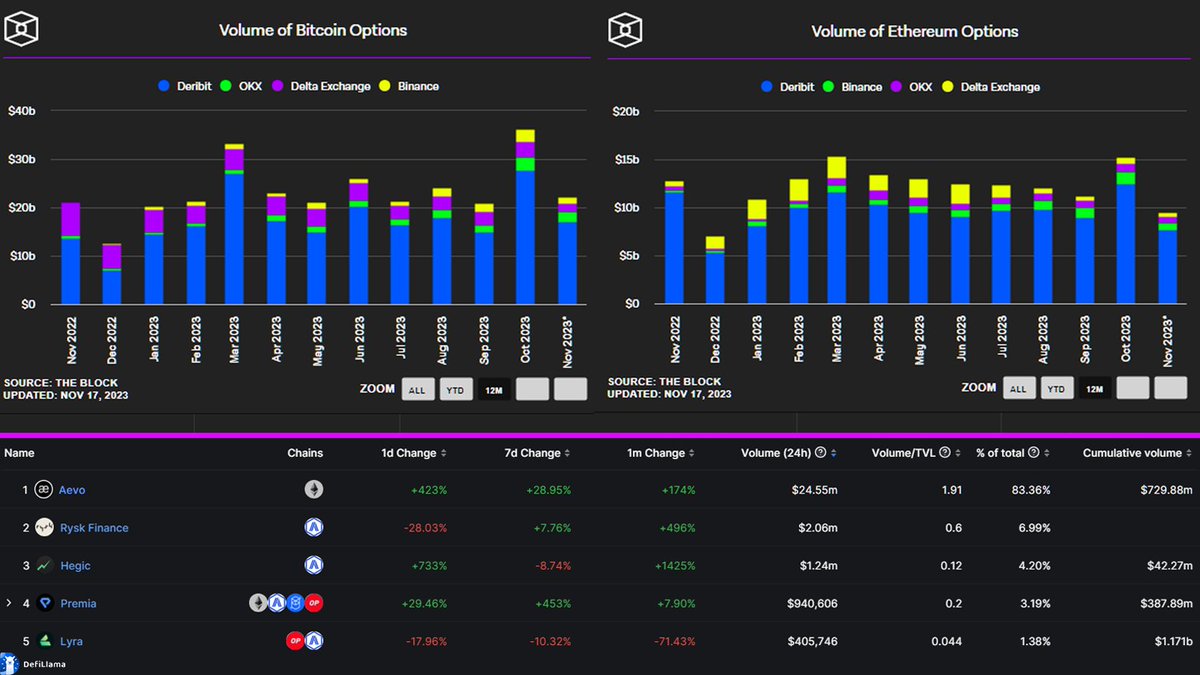

Exploring 9 Decentralized Options Protocols 🌐

Last week, we released our article analysis on the crypto options market and covered CEX vs DEX options in our previous post (Link at end of the post).

This week, we will be taking a look at 9 decentralized options protocols! We believe that TVL is a great metric to determine the strongest players in the decentralized options space, so here are the key contenders shaping the decentralized options landscape:

🔹 @opyn_

TVL: $13.17M

Chains: Ethereum, Avalanche, Polygon

Opyn focuses on developing open finance by leveraging DeFi methodologies and perpetual options and introducing the pioneering perpetual options like Opyn Squeeth.

🔹 @HegicOptions

TVL: $10.94M

Chains: Arbitrum, Ethereum

Hegic simplifies peer-to-pool options with one-click process for various strategies and the cost of an option based solely on premiums, eliminating additional trading or taker fees.

🔹 @aevoxyz / @ribbonfinance

TVL: $15.7M (Combined)

Arbitrum, Ethereum, Optimism

Built by the same team, they are one of the biggest players in the options niche. Aevo is a derivatives L2, offering options & perps trading. As for Ribbon, their first product was the first Decentralized Options Vault (DOV) protocol, offering tokenized structured products and strategies.

🔹 @lyrafinance

TVL: $9.45M

Chains: Optimism, Arbitrum, Ethereum

Innovation: Lyra operates as an automated market maker (AMM) for options, and enhancing capital efficiency and composability with the upcoming V2.

🔹 @PremiaFinance

TVL: $5M

Chains: Arbitrum, Ethereum, Optimism, Fantom, BSC

Premia V3 boasts a Hybrid Orderbook, where each pool equates to a specific strike and liquidity tick, and includes vaults for tokenizing exotic or structured strategies, incentivized by PREMIA and governed by vxPREMIA stakeholders.

🔹 @dopex_io

TVL: $4.28M

Chains: Arbitrum, BSC, Avalanche, Ethereum

Dopex introduces Single Staking Options Vaults (SSOVs) and a dual token system (DPX and rDPX) for governance and liquidity enhancement.

🔹 @ryskfinance

TVL: $3.01M

Chains: Arbitrum

Rysk Finance blends AMM and Request for Quotation (RFQ) systems that offers uncorrelated and delta-hedged yields for its liquidity providers, providing auto-exercising options with efficiency and user-friendliness.

🔹 @Opium_Network

TVL: $2.64M

Chains: Ethereum, Polygon, BSC, Arbitrum

Opium's decentralized escrow system, offering adaptability to various use cases such as sports betting, where participants can place wagers, with the escrow determining payouts based on the event's outcome.

🔹@DualFinance

TVL: $2.5M, including staked $18.17M

Chains: Solana

Dual Finance empowers DAOs with liquid option-based incentives, tools and services. Partner projects can use their Staking Options to sustainably incentivize their communities.

-----

TVL data was taken from @DefiLlama, on 24/11/2023.

For a comprehensive look at these players and their contributions to the decentralized options space, check out our full article here ⬇

blog.impossible.finance/impo…

If you missed it, last week we took a deep dive into the ever-evolving crypto market ⬇

twitter.com/impossiblefi/sta…

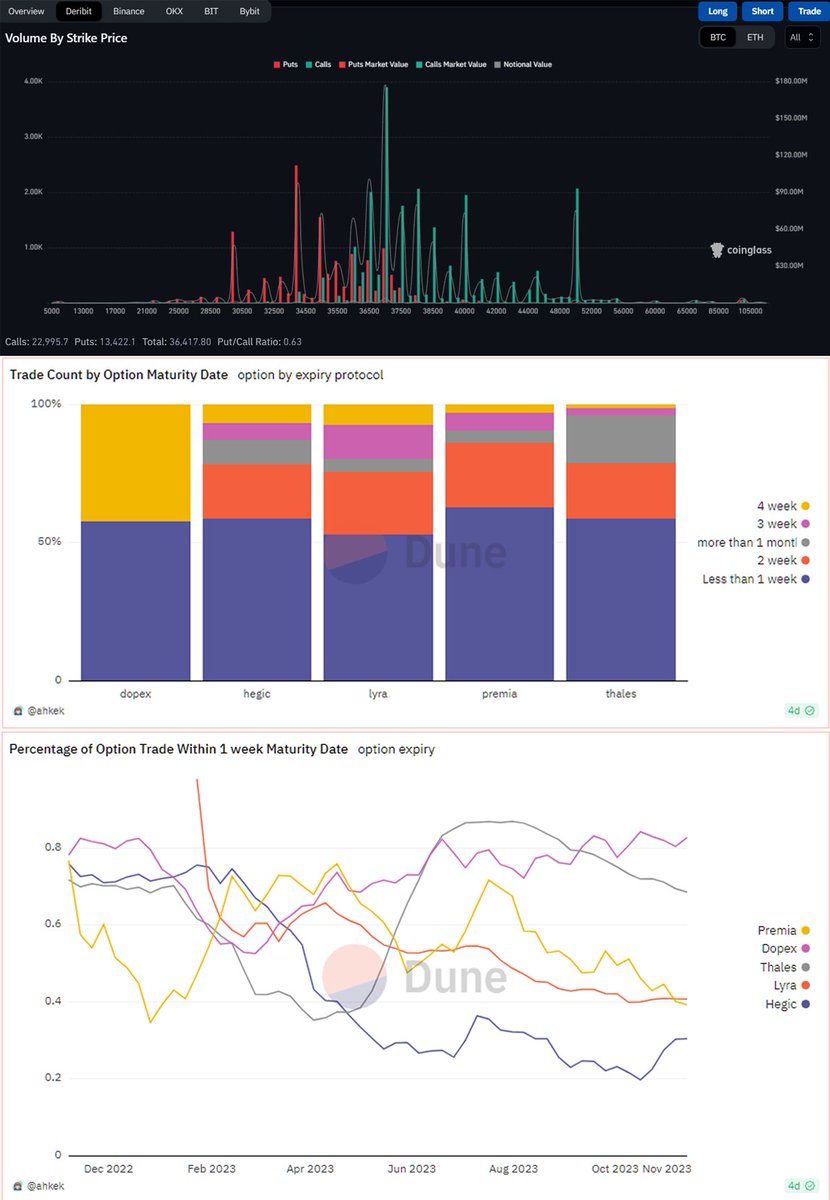

17 Nov 2023

Dive into the dynamic world of crypto options with a glimpse into the current state of the market.

We did the research for you — So, grab a cup of coffee and read up 👇

In the crypto options market CEXs, like @DeribitExchange, dominate in terms of trading volume, offering deep liquidity and competitive pricing, but require custody of user funds and rely heavily on market makers.

DEXs, led by platforms like @aevoxyz, @ryskfinance, @HegicOptions, @PremiaFinance and @lyrafinance. It focuses on self-custody and transparency, utilizing automated market makers (AMMs) and Request for Quote (RFQ) systems to aggregate liquidity but are lagging in terms of volumes.

This disparity underscores the overwhelming prevalence of centralized platforms in the crypto options trading landscape, yet the significant untapped potential for expansion and growth of the decentralized options space.

When we delve into maturity data and strike prices, CEXs offer greater liquidity and flexibility. Users can purchase contracts with expirations extending well into the next year, signifying the market's depth.

In contrast, the decentralized #cryptooptions space exhibits a distinct pattern. Here, the majority of users engage in options with much shorter durations, typically within a one-week timeframe.

When assessing the distribution of options traded by their maturity dates, a notable trend emerges, though:

There is a reduction in the percentage of options traded within a week of maturity.

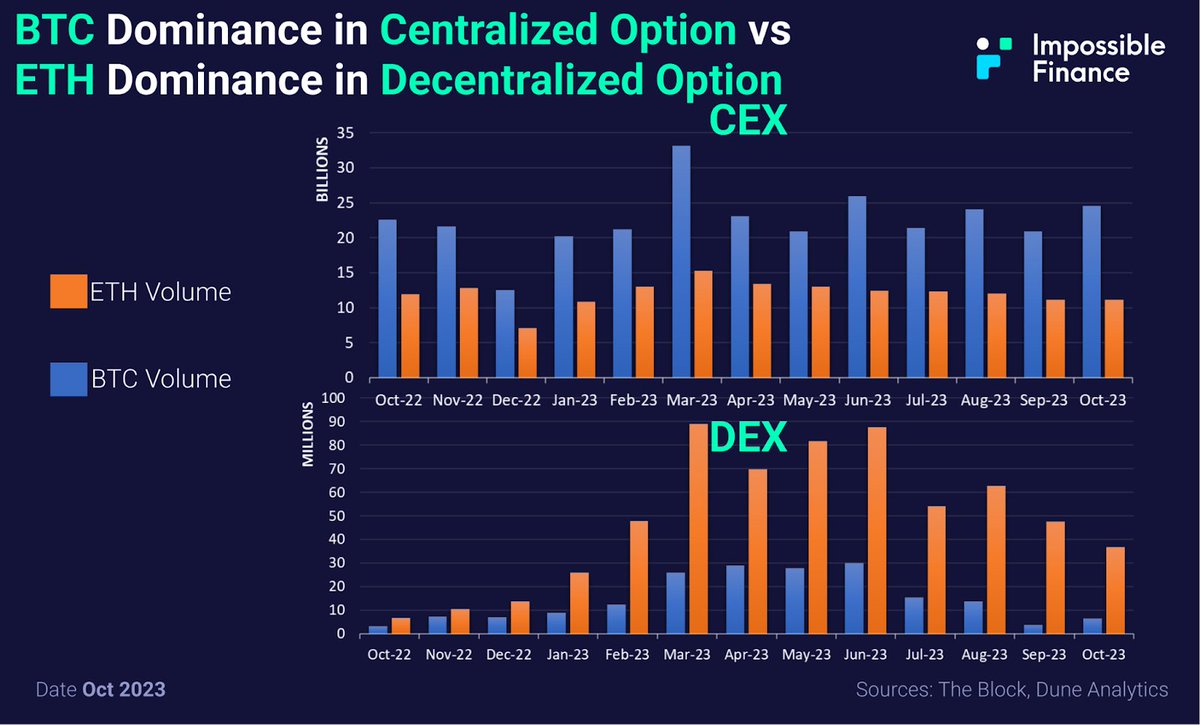

Another significant distinction between centralized and decentralized crypto option exchanges is the distribution of trading volumes between BTC and ETH.

In the centralized crypto option exchange domain, there is a notable skew towards BTC options, with considerably higher trading volumes in comparison to ETH.

Conversely, within the decentralized crypto option exchange landscape, the situation is reversed, with ETH options experiencing higher trading volumes than BTC.

This divergence probably highlights the versatility and variety of options available to cryptocurrency traders across various platforms, together with preference of the options.

----

This is just one part of our deep dive into the crypto options sector 😎

Our full article goes beyond just analyzing the option market statistics. We shine a spotlight on 9 Option projects, the impact of LPDFi in crypto options, and much more!

Read here: blog.impossible.finance/impo…

3

10

31

5,240

Opium retweeted

19 Jul 2023

Meet newest #DeFi primitive: Token Plugins! Let me know what do you think about it! What token plugin can you build? #ETHCC youtube.com/live/a9uCqWmH-HE…

148

70

314

65,058

Opium retweeted

17 Jul 2023

StakeWise V3 gives stakers the power to access liquid staking from any node, prioritizing control, self-custody, yield and decentralization 🌊

Try StakeWise V3 on testnet: pacific.stakewise.io

107

1,825

1,104

103,143

let’s talk about identity

tomorrow 1pm at sozu haus

@0xMantle

@Clique2046

@Knowyourcat_id

@gitcoin

@zkme_

@worldnetwork

yes you may jump in the pool after

rsvp or ngmi

lu.ma/sozuidentity

2

7

31

10,926

15 Jul 2023

💎An amazing development of Know Your Cat idea!🐱

🎊 Congrats and kudos to kyCat team! 🎊

kyCat = soulbound token that can whitelist you and much more 🚀

🎯Mint your cat knowyourcat.id and participate on hackathon #ETHCC #sbt #soulbound

14 Jul 2023

.@sozuhack01 That's fantastic news! we're excited to be sponsoring the event and offering bounties worth $2500! 🎉🐾 we can't wait to see the amazing projects that will come out of the SOZU HACK [01] online hackathon.

Sign up now at sozuhack01.devfolio.co.

Meet our team!

Meow!

4

156

83

3,657

Opium retweeted

2 Jun 2023

With @Opium_Network, you can trade and create customized financial products without intermediaries, and with the integration of Gelato's Web3 Functions, Opium can automate smart contract functions, making scheduled deposits and withdrawals a breeze!

gelato.network/blog/defi-aut…

5

6

19

4,494