General Partner @20VCfund. I just love investing & talking about it. 2x Father. Not investment advice.

Joined November 2024

- Tweets 842

- Following 521

- Followers 1,827

- Likes 110,705

93 Photos and videos

So interesting to me how everyone (particularly newspapers) parrots “ $SPCX is on 100x revenues” without acknowledging that:

- they just signed ~$25bn per year compute deals

- are about to add ~$4-5bn of ARR from Cursor.

==> Literally that’s <40x RR revenues at IPO price pro forma (and a bit above that now).

This comes with a total monopoly on potentially one of the largest future markets. and a call option on AI.

Yes it’s still crazy expensive no one knows where future growth exactly comes from going forward, and when (but I suspect mgmt will find a way as they always have).

Do I believe you will be able to buy it cheaper in the future? Certainly. Because doubts will creep back in at some point. But is there a point trying to time it at all? I’m not so sure.

And life is much funnier having an ever so small amount of skin in the game in the most exciting company of our time! 🚀

5

518

I’ve been long $EVC too for a while after reading @Uzocapital’s amazing thesis on it. Just need a bit more patience and it will keep delivering.

Jun 10

$EVC — the most mislabeled stock on the NYSE

The Street covers Entravision as a dying Spanish-language broadcaster. Here’s what’s actually inside it.

Stock: $9.18, roughly $845M market cap, 52-week range $1.95 to $10.12. It trades on the “Hispanic broadcaster” desk, modeled on political ad cycles and a Univision affiliation renewal. But Q1 2026 consolidated revenue was $197M, up 114% year-over-year, and the company swung to a $12.4M net profit ($0.13 EPS). The driver isn’t TV. It’s Smadex, a mobile-game ad DSP buried in the “Advertising Technology & Services” segment.

In Q1 2026 that ATS segment did $154.6M in revenue, up 204% year-over-year, with $34.3M of operating profit, up 427%. It’s now the majority of total company revenue.

The bear says that’s only a 22% margin. But the 22% is on gross revenue. EVC books the media it buys for clients as cost of revenue and grosses it up, while AppLovin and Liftoff report net, after media cost. That comp is apples to oranges, and the filing lets you fix it. Gross revenue of $154.6M minus $96.6M of media cost leaves about $58.0M of net revenue. Against $34.3M of operating profit, that’s a net-basis operating margin near 59 percent, not 22. EVC keeps about 37 cents of every gross dollar, a healthy DSP take rate.

Like-for-like, Smadex runs roughly a 59% operating margin growing 204%. AppLovin runs about 76% growing 24 to 60% and trades near 25x revenue. Liftoff is lossmaking, growing about 32%, and just IPO’d around 6x revenue at a $4.3B valuation. Smadex sits between the lossmaking pure-play and the gold standard on margin, and out-grows both.

On price: net debt is roughly $91M ($162M debt against $71M cash), so enterprise value is about $936M. Against roughly $137M of annualized segment operating profit, the entire company trades at under 7x the ad-tech segment’s EBIT. On net revenue, about a $232M run-rate, that’s near 4x, below Liftoff’s 5.8x.

And the rest comes nearly free. The media business (49 TV and 44 radio stations, retransmission revenue, the largest Univision affiliate footprint) is worth roughly $300 to $400M in a sale. I value the FCC broadcast spectrum at around $500M, with auction-reform optionality on top. A conservative breakup, before Smadex grows another dollar, lands around $25 to $35 a share. The stock is $9.

Why now: app supply just went vertical. Q1 2026 App Store submissions hit 235,800, up 84% year-over-year, with April up 104%, after falling 46% from 2016 to 2024. The cause is vibe coding (Claude Code, Cursor, Replit, Lovable). A weekend-built game has zero organic reach, so the only way it finds players is paid user acquisition, which runs through DSPs, and Smadex is a DSP.

The one risk you can’t wave away: a single advertiser is 36% of revenue. That’s the bear case in one number, and it’s why this is cheap.

5

785

Plot twist: Databricks are waiting for Series Z to IPO.

Jun 9

JUST IN: Databricks is reportedly in talks for a Series M funding round at a valuation of up to $175,000,000,000.00.

1

1

2,084

Must listen on $NBIS.

Personally it continues to make me incredibly excited about the business.

youtube.com/watch?v=aXAH3bdJ…

5

530

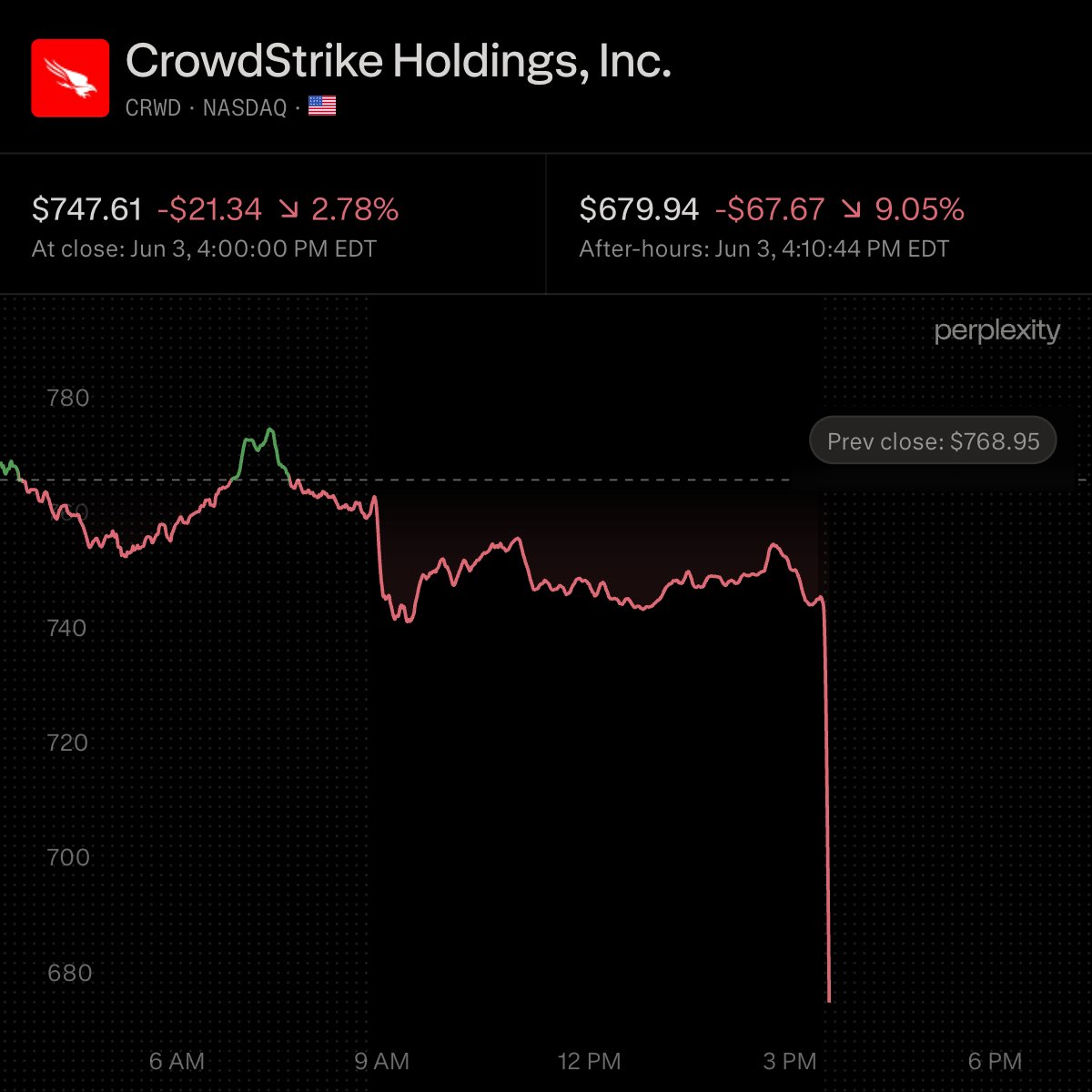

…CRWD AT 34x run-rate revenues growing 26% YoY?

SaaS darlings (now back at nonsensical valuations for the best ones) are about to experience gravity again very soon.

And the gravitational pull should look more like Jupiter’s than the earth frankly.

$CRWD

Jun 3

$CRWD Q1’27 EARNINGS HIGHLIGHTS

🔹 Revenue: $1.39B (Est. $1.38B) 🟡; 26% YoY

🔹 Adj. EPS: $1.10 (Est. $1.07) 🟡

🔹 ARR: $5.51B; 24% YoY

🔹 Net New ARR: $255.8M; 32% YoY

🔸 Stock Split: 4-for-1

FY Guide:

🔹 Revenue: $5.915B-$5.959B (Est. $5.9B) 🟡

🔹 ARR: $6.532B-$6.556B

🔹 Non-GAAP Operating Income: $1.452B-$1.480B

🔹 Adj. EPS: $4.88-$4.96

🔹 Net New ARR Growth: 27.7% at midpoint

Q2 Guide:

🔹 Adj. EPS: $1.16-$1.17 (Est. $1.15) 🟡

🔹 ARR: $5.793B-$5.795B

🔹 Revenue: $1.436B-$1.442B

🔹 Non-GAAP Operating Income: $345.6M-$349.1M

Other Metrics:

🔹 Free Cash Flow: $468.5M

🔹 Subscription Revenue: $1.32B; 26% YoY

🔹 GAAP Subscription Gross Margin: 78%

🔹 Non-GAAP Subscription Gross Margin: 81%

🔹 Module Adoption: 51% for 6 modules, 35% for 7 modules, 25% for 8 modules

🔹 Split Record Date: June 25, 2026

🔹 Split-Adjusted Trading Expected: July 2, 2026

🔹 Cash & Cash Equivalents: $4.55B

Financials:

🔹 Non-GAAP Operating Income: $325.7M

🔹 Non-GAAP Net Income: $283.4M

🔹 Operating Cash Flow: $590.9M

🔹 Free Cash Flow: $468.5M

Commentary:

🔸 “In Q1, the worlds of cybersecurity and frontier AI collided: this was the Mythos moment.”

🔸 “CrowdStrike is AI security infrastructure, critical to successful AI adoption.”

🔸 “Our record Q1 net new ARR, QuiltWorks coalition, and AIDR innovation are indicators of our own AI inflection point.”

🔸 “We are raising our full-year net new ARR growth expectations to 27.7%, at the midpoint, now an acceleration over the prior fiscal year.”

1

2

1,095

The speed at which Corgi move is lowkey redefining insurance in a way no one has done before.

Power of focus, hardwork, and smart use of AI - in an otherwise antiquated industry.

Just the beginning. Congrats @UseCorgi @nico_laqua @emily_yuan_ and the whole team!

Proud angel.

May 28

We raised another $106M at a $2.6B valuation since announcing our last round three weeks ago.

Corgi has grown exponentially in the past couple of months, but we're only just getting started transforming one of the largest sectors in the US economy: insurance.

4

27

4,626

If you missed it - @ClickHouseDB revs expected to hit ~1bn ARR by EoY (4x from today) according to founder in Techcrunch today.

$NBIS owns 28%. More important in terms of the fundamentals than Situational Awareness buying.

Compute bound thesis still holds too. Demand > Supply.

5

935

This neocloud trade is starting to massively pay-off and it feels great.

World is compute bound. How long for, I do not know. But this is directionally correct for now.

May 27

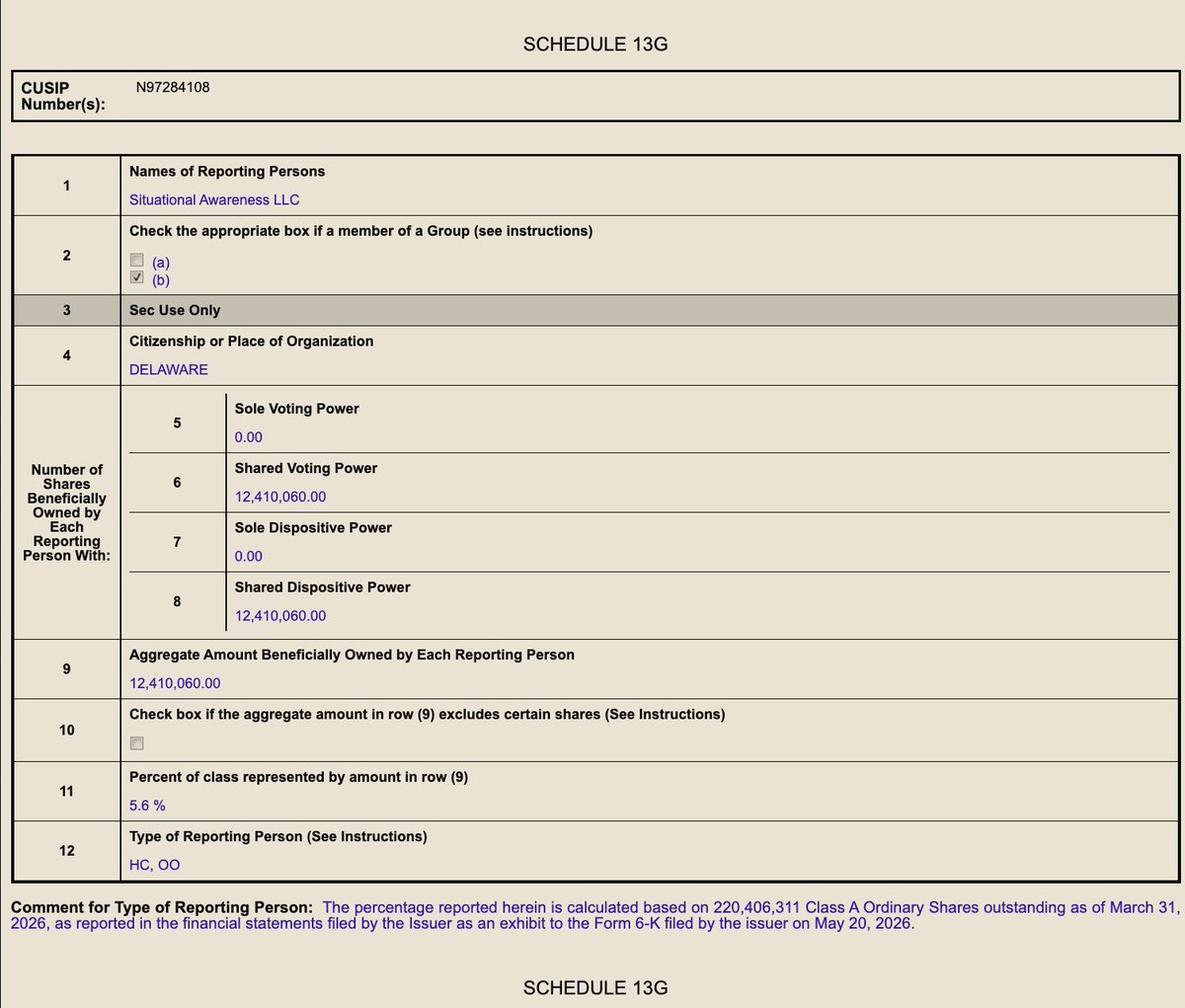

Leopold Aschenbrenner's Situational Awareness LP disclosed beneficial ownership of 12.41M Class A shares of Nebius $NBIS, representing a 5.6% stake.

3

756

Only wrinkle is that @RequestyAI is coming for them!

Slowly at first...

Currently not so slowly.

Then all of a sudden.

Go @ThibaultJaigu! 🚀

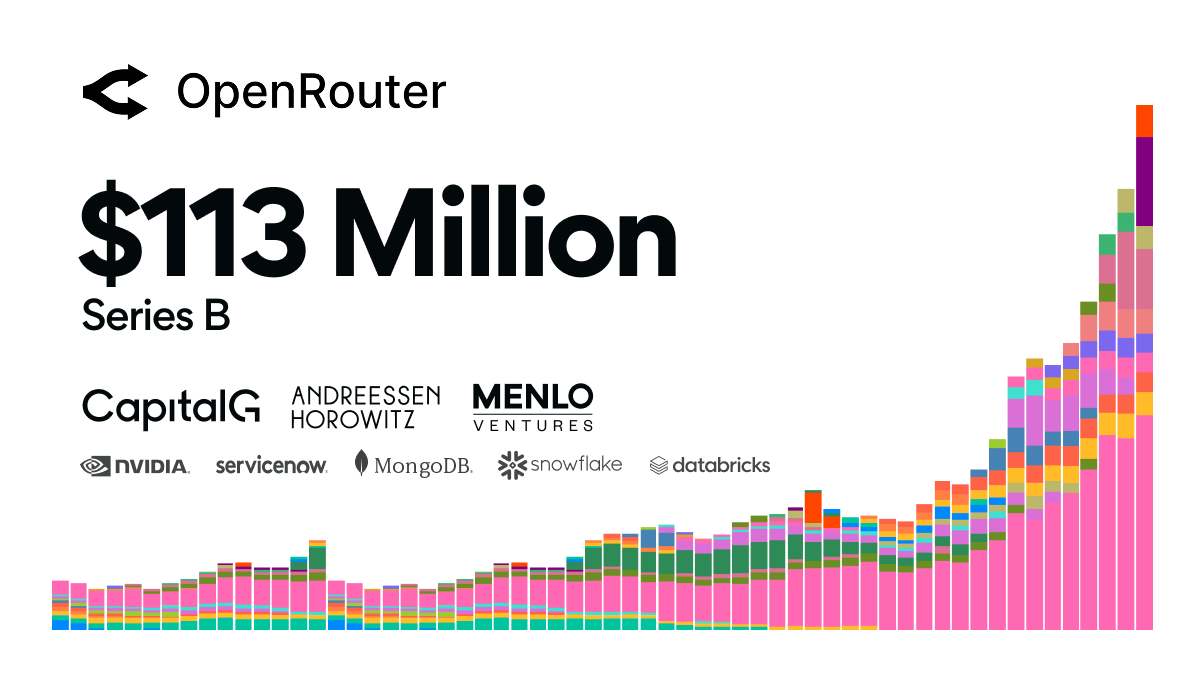

May 26

Today we’re announcing our $113M Series B led by @CapitalGVC.

Over the last 6 months, weekly volume on OpenRouter grew from 5T to 25T tokens as AI rapidly shifts from experimentation into production.

We’re excited for what comes next.

6

754

Turns out @MoodyWriter13 was pretty legendary in his thesis (at least short term!)

This is smart @MoodyWriter13.

I went long $2GB after 30 minutes of looking into it.

Also seems to be a very well managed business based on historical trends and reports.

1

10

4,672

This is smart @MoodyWriter13.

I went long $2GB after 30 minutes of looking into it.

Also seems to be a very well managed business based on historical trends and reports.

May 25

Decentralized power supply for AI data centers is currently one of the hottest themes in the market, and the relevant stocks have been moving rapidly higher. In fuel cells, $BE is the clear market leader, while $FCEL and Ceres Power are trying to position themselves as alternatives.

On the combustion side, the situation is different: the major gas turbine manufacturers such as GE Vernova, Siemens Energy, and Mitsubishi Power are effectively sold out, with multi year backlogs extending well into the second half of the 2020s.

The obvious alternative is gas engines, where several established players are active, including $CAT, Wärtsilä, INNIO and its Jenbacher platform, Cummins, and 2G Energy.

One advantage of gas engine solutions over fuel cells receives far too little attention in the current debate: they are dispatchable and therefore combine naturally with solar power. The engine ramps up when solar generation falls away. Fuel cells cannot do this. They are fundamentally baseload assets and do not tolerate rapid load changes or frequent start stop cycles.

This matters more for AI workloads than many investors realize.

Pure baseload power is primarily needed during full scale training runs, and even there, workloads create second by second load transients. Inference is even more dynamic because it follows user demand and therefore exhibits a clear daily utilization profile. This is exactly where dispatchable gas engines excel, especially when paired with a modest battery energy storage system.

Some of these engines can already operate on hydrogen, further strengthening their long term relevance.

The downside relative to fuel cells is clear: lower efficiency and higher emissions because fuel is combusted.

There is one particularly interesting German company in this space that already has a strong position in decentralized energy infrastructure for the energy transition through combined heat and power systems, biogas solutions, and large scale heat pumps: 2G Energy $2GB.DE

According to management, the company is currently close to signing several US data center contracts in the high double digit to low triple digit megawatt range, with each individual order potentially worth up to €100 million.

That is highly meaningful for a company currently guiding for €440-490 million in annual revenue. For larger competitors, deals of this size would barely move the needle.

The stock is already up roughly 50% ytd. That is not insignificant, and on absolute numbers it is not cheap. But relative to peers it still looks highly attractive:

P/S 2026e of approximately 2.1x

EV/EBIT 2026e of roughly 22x

EV/EBIT 2027e of roughly 18x

Compare that to $BE at roughly 11 to 13x forward sales, or GE Vernova with a market cap near $293 billion and a forward earnings multiple around 32x.

Based on its current business alone, 2G is not cheap.

But the data center optionality is still not reflected in the valuation.

The concrete advantages of 2G’s solutions include:

Standardized modular units manufactured in house and deliverable within roughly 9 to 18 months. This is the critical advantage while turbine supply remains constrained.

The Gas2Power platform covers backup power, prime power, and grid services, with full load step capability within 10 seconds. This makes it ideal for pairing with solar generation.

The waste heat can be used for absorption cooling, directly supporting data center thermal management.

Approximately 55 dB(A) at 10 meters, which materially improves permitting prospects for sensitive sites.

What makes the business model especially compelling is its focus on high margin recurring service revenue.

A triple digit megawatt installed base generates maintenance and service revenue over more than a decade. That recurring stream is the real compounding engine behind what initially appears to be a one time equipment sale.

For investors looking at decentralized AI infrastructure power, this company is worth a look.

1

7

6,181

So SpaceX's S1 indicates being a Neocloud is very profitable? $NBIS $IREN

• Colossus I completed 2024 & Colossus II online Jan-26

• = D&A related to AI CAPEX is essentially reflected Q1 loss (bar 1/3rd of C2 D&A)

• @AnthropicAI pays $1.25B p.m = c.$3.75B per quarter extra revenues at no extra cost

• Q1 net loss for AI c.$2.5bn

• => Add back c.$3.75bn per quarter and segment turns profitable on 5-6y depreciation (again per S1 and assuming this hold)

• AI produces c.$1bn of net income then once rev fully reflected?

4

946

No one is talking enough about interest rates and their potential effects on the AI build-out right now.

Higher debt cost may be a massive spanner in the debt fuelled CAPEX spree - regardless of end-user consumption.

Rates need to go down or could be 2022 all over again.

1

3

589