Joined June 2022

- Tweets 1,711

- Following 244

- Followers 736

- Likes 377

235 Photos and videos

Pinned Tweet

May 15

X-Fab $XFAB continuing its climb toward its right value!

Possibly one of the strongest semiconductors to invest in right now.

1

652

May 29

I just bought more $XFAB.

I started buying in 2024 and continued on drawdowns with an initial average price of around 5€. So, based on the recent move, why did I buy more?

The recent momentum is finally solving one of the main issues of investing in the company: visibility.

X-Fab has always been undervalued but continued to lack any visibility, meaning that despite an increased guidance to around $1.5B in sales by 2030, the stock barely budged.

With @aleabitoreddit shedding a light on this fabulous firm, on all the right metrics of the SiC capabilities and the photonics potential, I believe that the stock can hit my bull target of over €22 a share.

My updated average purchasing price is now €6.930 and I'm willing to buy more if it continues to drop back below €10 a share.

2

17

3,154

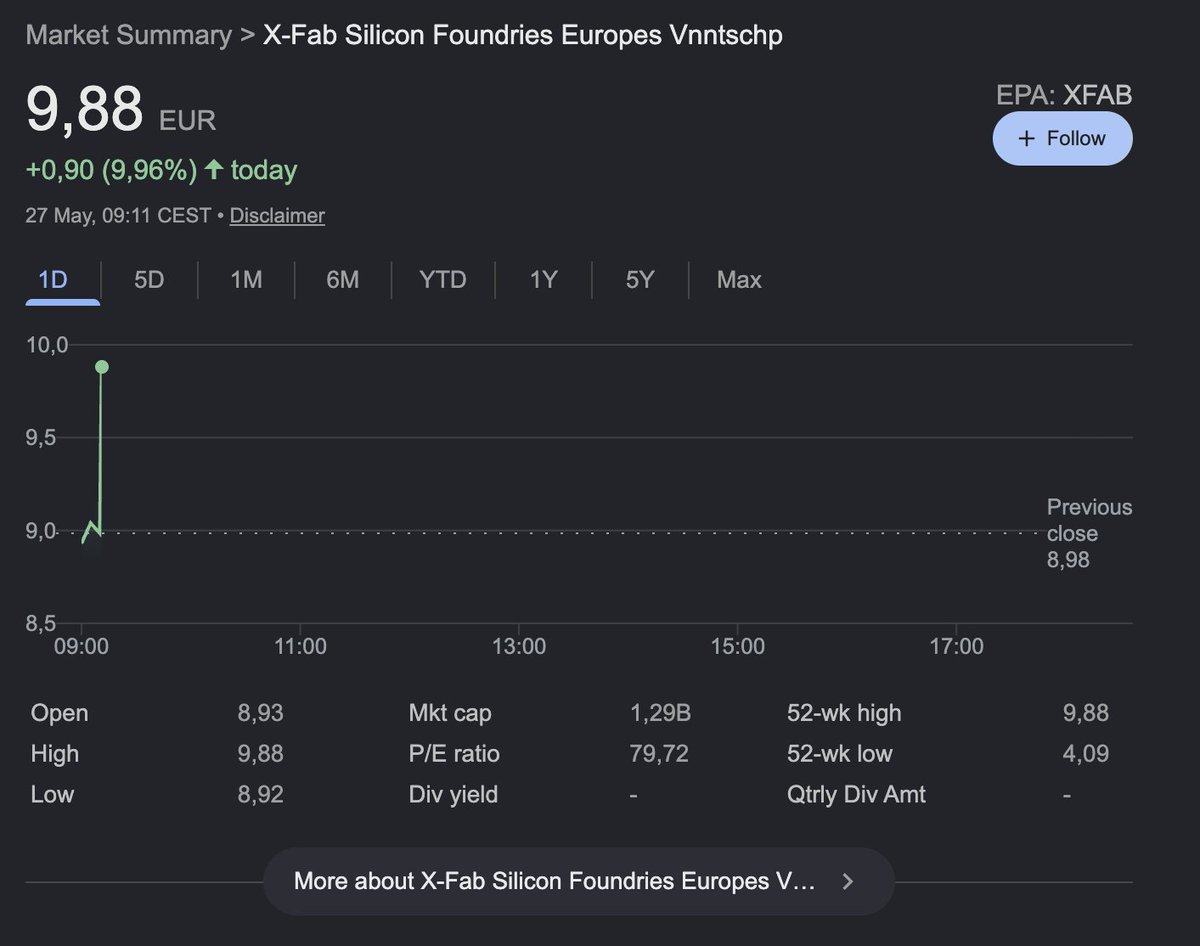

May 27

On $XFAB, don't forget that 50% of the stock is locked in by two families so the buying pressure only applies to half of the float available.

4

7

1,662

May 27

Well, I guess $XFAB is finally getting the love it deserves.

Great company and great management, which is why it pushed me to buy shares back in 2024.

seekingalpha.com/article/474…

1

6

1,160

May 13

X-Fab $XFAB crossing back the €1B market cap on the back of this massive rally!

Simply one of the best semiconductors to own.

More to go.

1

690

May 11

X-FAB $XFAB is one of the lowest valued semiconductor firms on the market and it deserves your attention as it could very well become a 5x bagger in the near future.

3

729

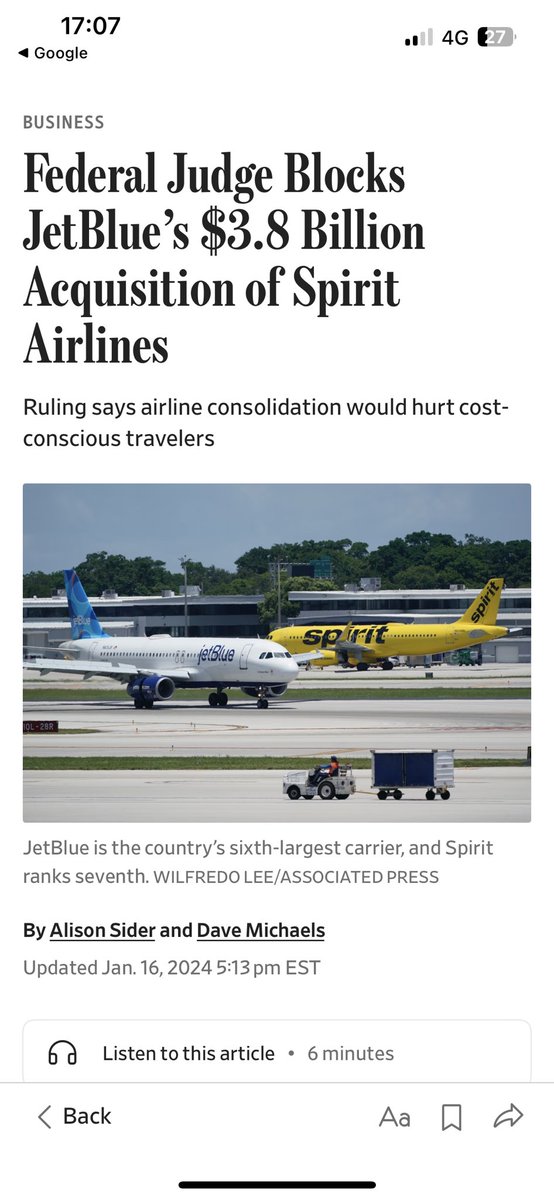

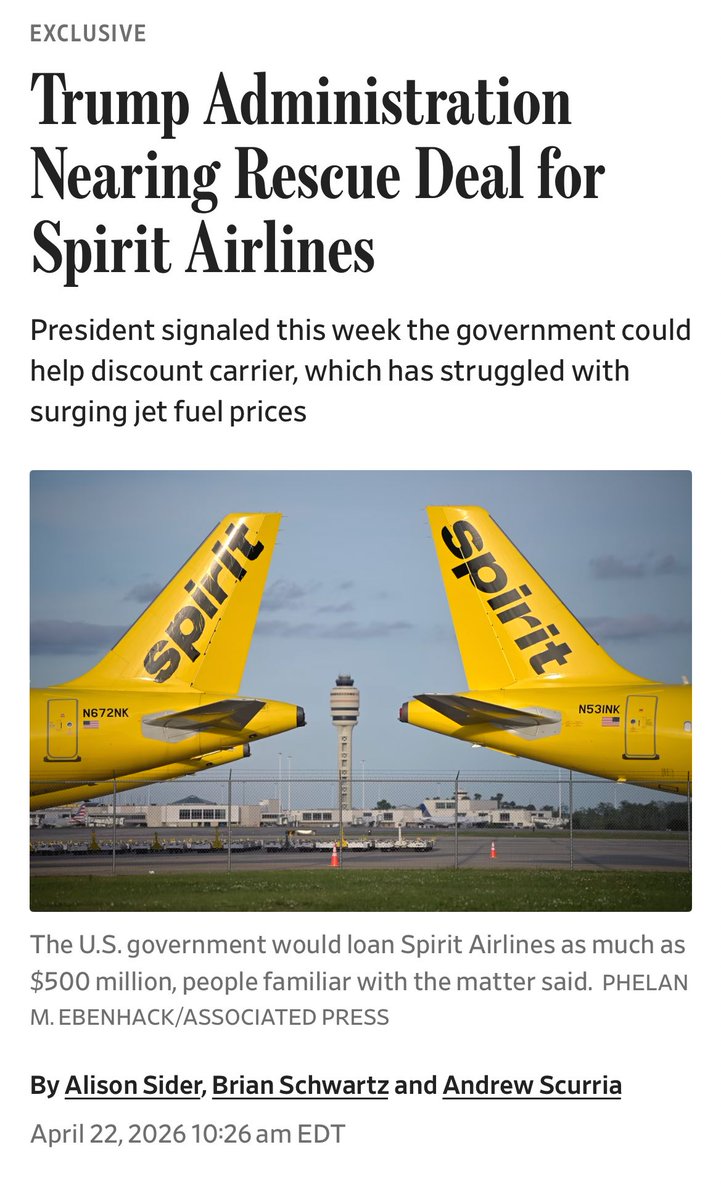

Apr 22

Remember when the JetBlue $JBLU Spirit merger was blocked for antitrust reasons? Guess it was the wrong call.

2

211

Mar 27

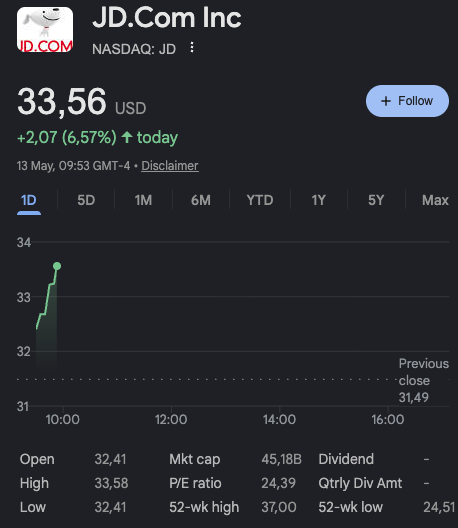

JD.com $JD at 8x earnings is China's most misunderstood stock.

The market sees a money-losing e-commerce company. What it's actually looking at is a profitable retail machine deliberately burning cash to build a food delivery army and invade Amazon's backyard.

Strip out the new businesses, and this is one of the cheapest quality compounders in global e-commerce.

(1/4)

1

2

263

Mar 27

The valuation gap is absurd:

— $JD: ~8x trailing P/E, 0.18x EV/Sales

— Alibaba: 18x P/E, 1.8x EV/Sales

— PDD: 11x P/E, 2.8x EV/Sales

— Coupang: 83x P/E, 1.0x EV/Sales

And JD returned ~10% of its market cap to shareholders in 2025 alone

— $3B in buybacks $1.4B in dividends.

That's not a company in distress. That's a company buying itself back while Wall Street isn't looking.

1

1

225

Mar 27

Even a modest re-rating to 12x forward P/E on normalized earnings gets you to $38, a 38% upside from here.

Yes, China risk is real. Yes, food delivery could stay unprofitable longer.

But at 8x earnings with a 10% capital return yield and a core business that's actually improving, the risk/reward is heavily skewed.

Full model and thesis breakdown here: seekingalpha.com/article/488…

84

Mar 26

More so on Novo Nordisk's $NVO AGM, I want to dive into the newly elected directors:

Jan van de Winkel — Co-founder and CEO of Genmab, Europe's largest biotech. Built it from a 20-person startup to 8 approved antibody therapies including DARZALEX. 30 years in therapeutic antibodies, 300 scientific publications, 150 patents. This is one of the most successful biotech founders in European history, joining the board.

Ramona Sequeira — 30 years in global pharma. Led Takeda's US business through a 3x revenue expansion and was the first woman to chair PhRMA's board. Before that, 20 years at Eli Lilly launching brands across the US and Europe. She knows exactly how to compete in the market Novo is losing ground in.

Helena Saxon — Former CFO of Investor AB (the Wallenberg family's holding company), Goldman Sachs alumna, and 14 years on the board of rare disease specialist Sobi. Deep capital markets and healthcare investing expertise.

The message is clear: the Foundation, which controls the company, saw a business drifting and intervened with force. The new board has biotech R&D depth, global commercial execution experience, and financial discipline, exactly what Novo needs to fight back against Lilly.

At 10x earnings, you're getting a turnaround with A-list governance for free.

2

427

Mar 24

Considering the current situation in Iran, I don't believe that Dubai is over. The charts showcasing the property crash are an opportunity!

Just bought $EMAAR at ~12 AED.

The math is simple:

→ Record FY2025: revenue 40%, EBITDA 33%, net profit 36%

→ AED 155bn backlog = 3 years of revenue locked in → Trading at 5.9x earnings. Peer avg is 6.6x. Industry is 14.8x.

→ 8.5% dividend yield while you wait

The market is pricing in a Dubai crash that S&P, UBS, and every major agency says probably isn't coming.

Fortress balance sheet, 10.7% debt-to-equity, $11.7bn in escrow.

The risk is real, 100K units hitting Dubai in 2026 vs 27K avg. But at sub-6x earnings with this backlog, you're being paid to take that risk.

2

1

407