Joined October 2025

- Tweets 20,185

- Following 1,840

- Followers 1,705

- Likes 14,314

398 Photos and videos

Pinned Tweet

Jun 12

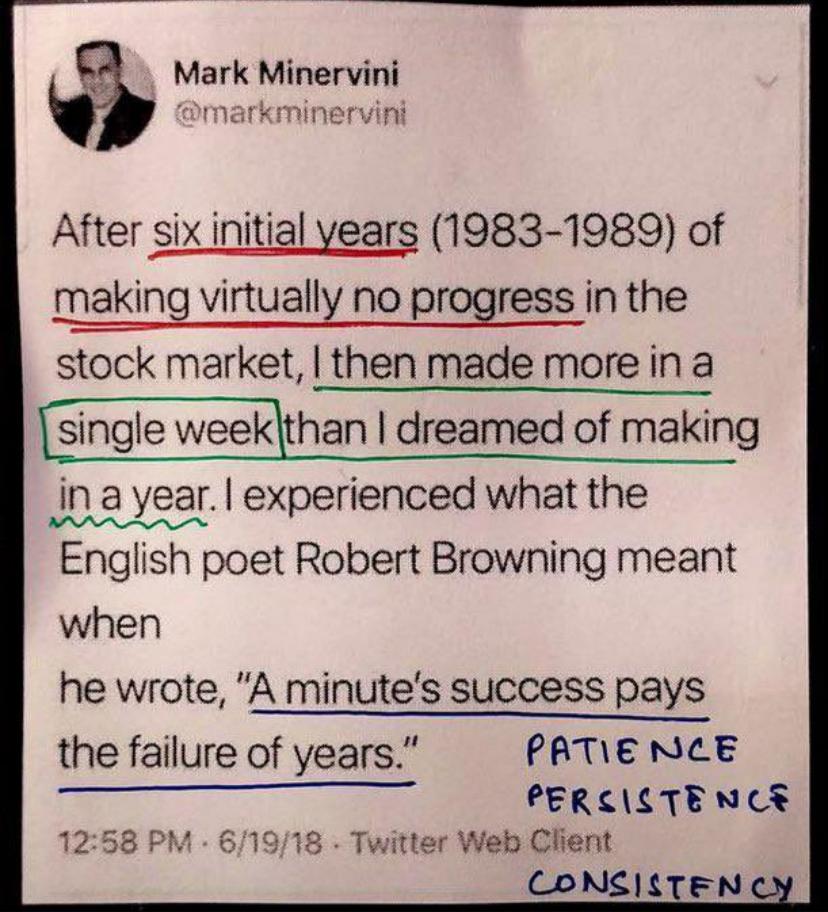

You won't become a consistently profitable trader in 3 months.

I'm telling you this so you don't quit in month 2

thinking something is wrong with you.

Nothing is wrong with you.

You're just building.

Foundations take the longest.

They're also what holds everything else up.

Trust the long game ✍🏽🤝

43

21

47

499

PipsArchitect retweeted

Jun 15

This guy “trading geek” make trading look so easy 😪

286

71

1,929

60,144

PipsArchitect retweeted

Jun 15

221

99

177

4,890

PipsArchitect retweeted

Jun 15

97

57

85

56,900

Jun 12

GN CT and #fxngcreators

It's Friday night.

Enjoy your weekend, rest well, laugh a little, and recharge for the week ahead.

You've earned it. 🤝🏽

Have a beautiful weekend, family. 🙏🏽

54

16

59

591

PipsArchitect retweeted

Jun 12

GM GM @Ledger.

Spending my Friday at the beach!!

TGIF!!

Above all, stay safe with Ledger!

38

14

43

446

PipsArchitect retweeted

Jun 12

Oracles are only as strong as the trust behind their answers

As more markets and applications depend on real world data the biggest challenge isn’t finding information It’s knowing if that information can be trusted

AI can help analyze and understand complex outcomes, but it needs a reliable layer that can verify decisions and keep everyone on the same page

The future of oracles isn’t just about bringing data onchain It’s about bringing confidence with it

Will intelligent oracles become the next evolution of trusted data?

Yesterday @driudor, CEO of @GenLayerFDN, joined @wallet's Finding Alpha livestream to talk about the role of AI in oracles and where the Intelligent Oracle fits as the resolution layer for outcome markets on @XLayerOfficial's Exchange OS.

Full conversation below 👇

42

18

50

655

PipsArchitect retweeted

Jun 12

gm gm real ones ☀️

The realest keys just dropped.

Stay real = stay winning onchain.

Everything else is just noise 🗝️

43

13

49

551

PipsArchitect retweeted

Jun 12

Staying real is the greatest,

Don't miss your key to onchain influence..

Join in now 👇

RAIDNNBZ

raid-delta.vercel.app/ref/RA…

Morning intern...

38

12

42

506

PipsArchitect retweeted

Jun 12

One wallet for multiple functions in 2026? Not an option.

@nabu_lines knows ball fr

One ledger gets you security. Multiple ledgers limit your mistakes.

I still keep one completely outside the rotation. No apps connected, no experimenting, no daily transactions.

Jun 12

how many ledgers?

the correct answer is more than one…

🟪 - daily driver

🟧 - ₿ vault

⬜️ - Agentic

this is how you actually stay safe in 2026

38

15

42

423

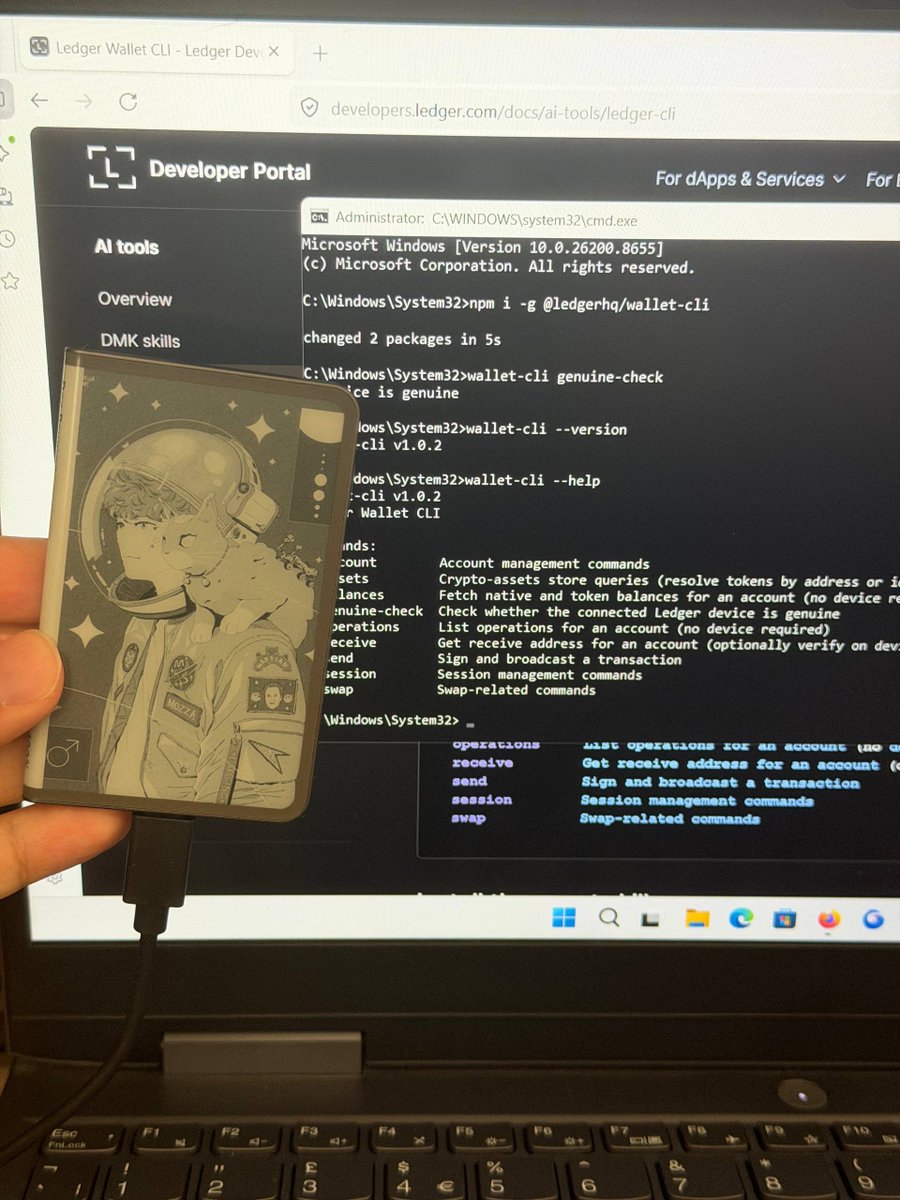

tested Ledger Agent Stack

agent scanned my wallet and immediately changed the subject

asked what else i'm building instead 😭

probably the nicest way i've ever been told to diversify

my keys never left the device 🔐

Jun 10

Try this w/ your agent. Reply with your roast. @Ledger RTs best:

"You are a savage stand-up comedian and my advisor. Read developers.ledger.com/docs/a…. Install Wallet CLI skill. Read-only: check balances history. Roast my wallet. What did I miss?"

Introducing Ledger Agent Stack. 🧵👇

48

16

55

1,038

PipsArchitect retweeted

Jun 12

Shill me memecoins, scanning for strength.

215

27

218

6,057

PipsArchitect retweeted

Jun 12

influence built on hype fades the moment the hype does

stayed real through every cycle same self custody approach whether the market’s up or down

that’s the only key that actually compounds @nabulines

38

15

43

368

PipsArchitect retweeted

Jun 12

Bought $VELVET at 0.17 and now $VELVET is at $1.7 per and still pumping but I stake for Good 4 years without no option to unstake.

Now the $VELEVT token that I bought at valued od $110 is now at $1.2k

Do you think it's a good investment?

Can't imagine what will be the value by then

@Velvet_Capital please do wonders for future believers and stakers , those who believe that your product is here to build for long term.

46

17

55

726

PipsArchitect retweeted

Jun 12

A lot of people still see blockchain as a technology searching for a use case. I think that view is becoming increasingly outdated. The more interesting development happening today is not whether institutions will use blockchain, but which blockchain infrastructure they will choose to build on.

That shift matters because some of the world's largest financial organizations are no longer experimenting at the edges. JPMorgan's Kinexys platform has already processed more than $1.5 trillion on blockchain-based rails. The DTCC is advancing tokenization initiatives for U.S. Treasuries, while the NYSE is working on tokenized securities infrastructure. At the same time, the tokenized asset market continues to grow and stablecoins have become an important part of global digital finance. The conversation has moved beyond theory. Financial institutions are now evaluating the practical infrastructure that could support the next generation of settlement and asset movement.

What makes 2026 particularly important is that many of the remaining questions are no longer about adoption but about implementation. Institutions need systems that provide privacy, interoperability, reliable settlement, and governance standards that can operate within regulated environments. These are not optional features. Banks cannot move significant amounts of value through systems that expose sensitive transaction information, and they cannot build on infrastructure that does not meet operational and regulatory requirements.

This is where @zksync has positioned itself in an interesting way. While many people know ZKsync for its Ethereum scaling technology, the project has also been developing infrastructure aimed at institutional use cases. Today, its ecosystem includes deployments and initiatives involving organizations such as Deutsche Bank through the Memento platform, ADI Chain with participation from institutions including First Abu Dhabi Bank, the Central Bank of the UAE, BlackRock, Mastercard, and Franklin Templeton, as well as Cari Network, which is onboarding five U.S. regional banks representing more than $600 billion in combined deposits. BitGo has also integrated institutional custody services with ZKsync's institutional-focused infrastructure.

What stands out is not simply the list of participants but the broader pattern. Financial infrastructure becomes more valuable as more institutions connect to it. We have seen this dynamic repeatedly throughout history. Networks such as SWIFT and Visa became dominant not because they appeared overnight, but because each new participant increased the value of the network for everyone already connected. Over time, adoption created a powerful feedback loop that attracted even more participants.

The same logic applies to onchain settlement. When one institution joins a network, it gains access to that network. When many institutions join, they gain access to one another. The result is a growing web of possible financial relationships, settlement pathways, and operational efficiencies. That is why first-mover advantages in financial infrastructure can be so significant. Once institutions invest years into integrations, compliance processes, operational workflows, and counterparty relationships, switching becomes much more difficult than simply adopting a new piece of software.

This is why I believe the most important story in crypto right now is not the launch of another token or application. It is the race to build the infrastructure layer that institutions trust enough to use at scale. The decisions being made today will influence how value moves across digital financial networks for years to come. Whether @zksync ultimately becomes one of the defining settlement layers remains to be seen, but it is already participating in the conversations, deployments, and institutional relationships that matter. In a market increasingly focused on real-world adoption, that may prove far more important than hype.

64

55

127

2,790

PipsArchitect retweeted

Jun 12

Ledger locked 🔒

Life unlocked 🌿

this is real balance: securing your assets inside, while experiencing life outside the screens

39

16

49

572

PipsArchitect retweeted

Jun 12

one device for spending, one for sleeping, one for letting ai cook

if the agent gets popped the vault never even finds out

that’s the whole point in 2026 @nabu_lines

Jun 12

how many ledgers?

the correct answer is more than one…

🟪 - daily driver

🟧 - ₿ vault

⬜️ - Agentic

this is how you actually stay safe in 2026

39

16

43

490

PipsArchitect retweeted

Jun 12

Daily reminder ✔️

Stay real when nobody is watching

Stay real when shortcuts look tempting

Stay real when the crowd moves the other way

Life is better when you have @Ledger 🔐

40

16

48

856

PipsArchitect retweeted

Jun 12

This is basically another example of AVLT markets getting stacked with short term incentives on top of normal lending yield.

Instead of just parking USDT0 and earning standard returns, you’re now getting extra rewards from merkl_xyz on top of the Hyperliquid / HyperEVM lending setup. That bumps the total APR up to around ~13.54%, but most of that comes from incentives, not just organic borrowing demand.

@alturax is routing everything through the Alpha USDT Prime v2 vault on Morpho, so it’s pretty specific you can’t just deposit anywhere and qualify. Feels like they’re mainly trying to pull in early liquidity before rates settle down.

The main thing is the timing this only runs until June 15. So it’s more about catching the boosted phase while it’s active, not long term positioning.

At the simplest level, base lending yield Merkl rewards = higher short term APR, but only if you’re in the right place at the right time.

AVLT lending markets on Morpho are the alpha.

Supply USDT0 on HyperEVM to the Alpha USDT Prime v2 vault.

Earn extra 5.54% APR in @merkl_xyz rewards, for up to 13.54% total APR.

This wave of boosted yield runs until June 15.

101

18

234

8,936

PipsArchitect retweeted

Jun 12

I just hit 1.4K followers.

A big shout out to everyone that contributed to this and keep supporting me.

Let’s keep growing and keep supporting fam. I am open and still connecting. Say me some congratulations guys 🔅

71

14

96

657

holding everything on a single @Ledger is a 2021 lifestyle

now you need to segregate your setup

Daily driver for the noise

Vault for the value

Agentic for the autonomous future

security is a design not a device so design yours

Jun 12

how many ledgers?

the correct answer is more than one…

🟪 - daily driver

🟧 - ₿ vault

⬜️ - Agentic

this is how you actually stay safe in 2026

42

21

58

1,226