I am a serial entrepreneur who is committed to corporate social responsibility. I want to leave the world a better place then when I arrived here.

Joined September 2022

- Tweets 4,841

- Following 1,311

- Followers 583

- Likes 37,961

32 Photos and videos

Pinned Tweet

22 Dec 2025

$MMTLP - Pls listen in and share. PIN this on your profiles and bookmark it!

#MMTLPARMY

#MMTLPstrong

#WeAreNotGoingAway

21 Dec 2025

5

488

Kerr 🇨🇦 retweeted

Jun 14

📣📣SAM BANKMAN-FRIED APPEAL DENIED 🚨🚨

Sam Bankman-Fried loses his appeal in his 8 Billion FTX FRAUD case.

He was unable to overturn his 25 year sentence.

Maybe he can be cellmates with Andrew Left in September.

NOT A GOOD WEEK FOR

SAM & ANDREW

22

110

445

5,012

Kerr 🇨🇦 retweeted

I know how Elon Musk became a trillionaire, but I don't know how Bernie Sanders, Elizabeth Warren, and Nancy Pelosi became millionaires.

2,063

18,103

110,180

1,287,041

Kerr 🇨🇦 retweeted

Jun 12

🤔🤔WHY IS THE DTCC DRAGGING THEIF FEET❓️❓️

So why is the DTCC dragging their feet in the MMAT MMTLP Bankruptcy ❓️

Lets just look at their board of directors, shall we.

Citadel

Virtu

FINRA

UBS

JP Morgan

NYSE

Goldman Sachs

NOW YOU KNOW WHY THEY DON'T WANT TO SUPPLY THE SUBPOENAED RECORDS‼️

Jun 12

33

211

411

15,907

Kerr 🇨🇦 retweeted

Jun 12

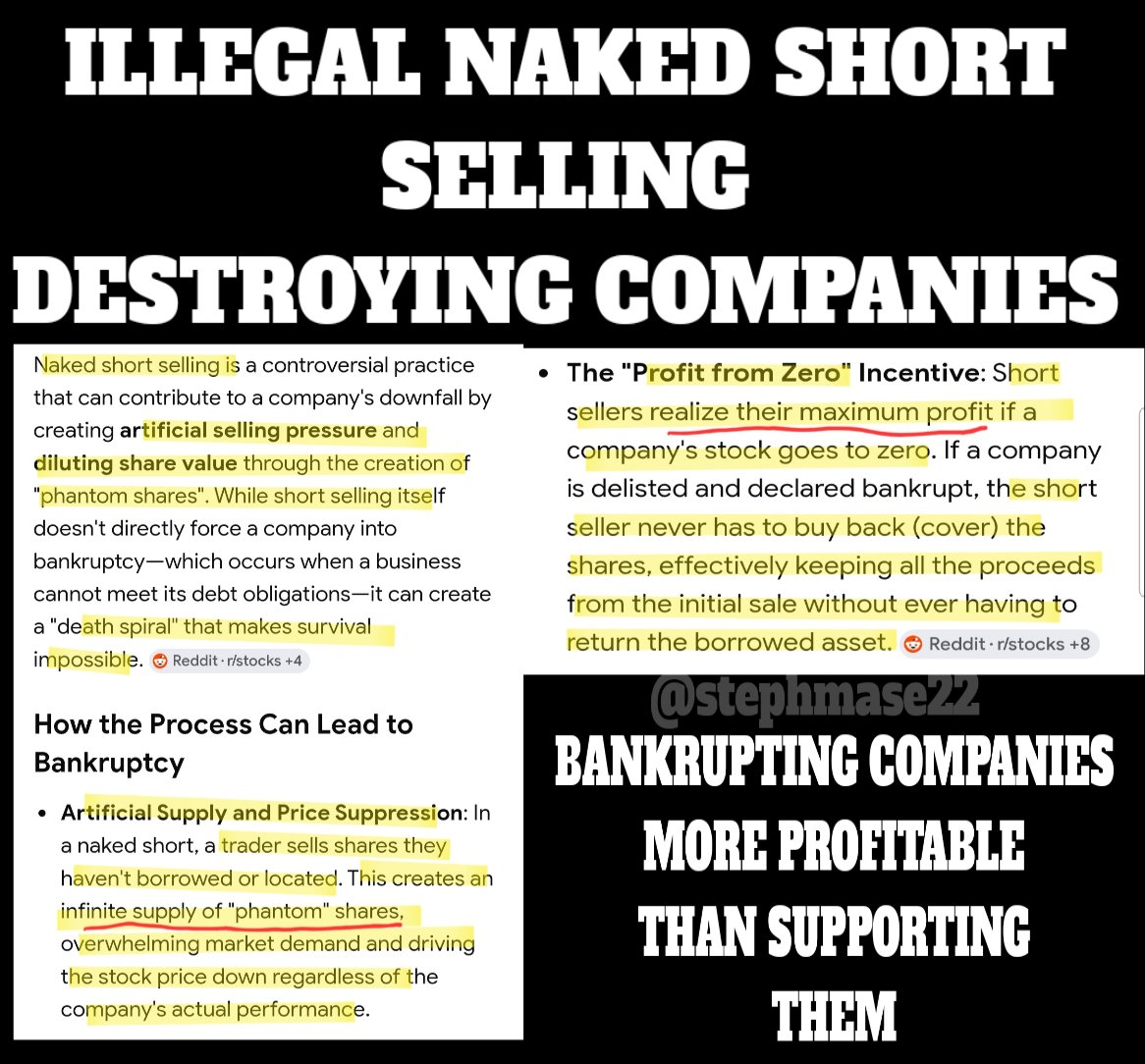

📣📣ILLEGAL NAKED SHORT SELLERS MAIN GOAL IS TO BANKRUPT THE COMPANY

When a company comes under attack from predatory short sellers, their main goal is to bankrupt the company.

WHY❓️

Because they have been selling or shorting something they don't own.

This causes Phantom shares that don't exist.

When they bankrupt a company, they

NEVER HAVE TO COVER‼️

That's why the MMAT MMTLP Bankruptcy case is setting an important precedence.

The Trustees is investigating, and the Judge has issued subpoenas that they are trying their hardest to avoid.

BANKRUPTCY MAY NOT BE THEIR CRIMINAL CRIME CLEAN UP ANYMORE

7

164

385

5,176

Kerr 🇨🇦 retweeted

Jun 11

SpaceX IPO will create 4,400 new Millionaires, from engineers to Cafeteria workers.

God bless Capitalism

Jun 10

JUST IN: SpaceX IPO reportedly expected to mint 4,000 new millionaires — “from engineers to cafeteria workers”

1,116

2,458

13,103

1,708,155

Kerr 🇨🇦 retweeted

Jun 11

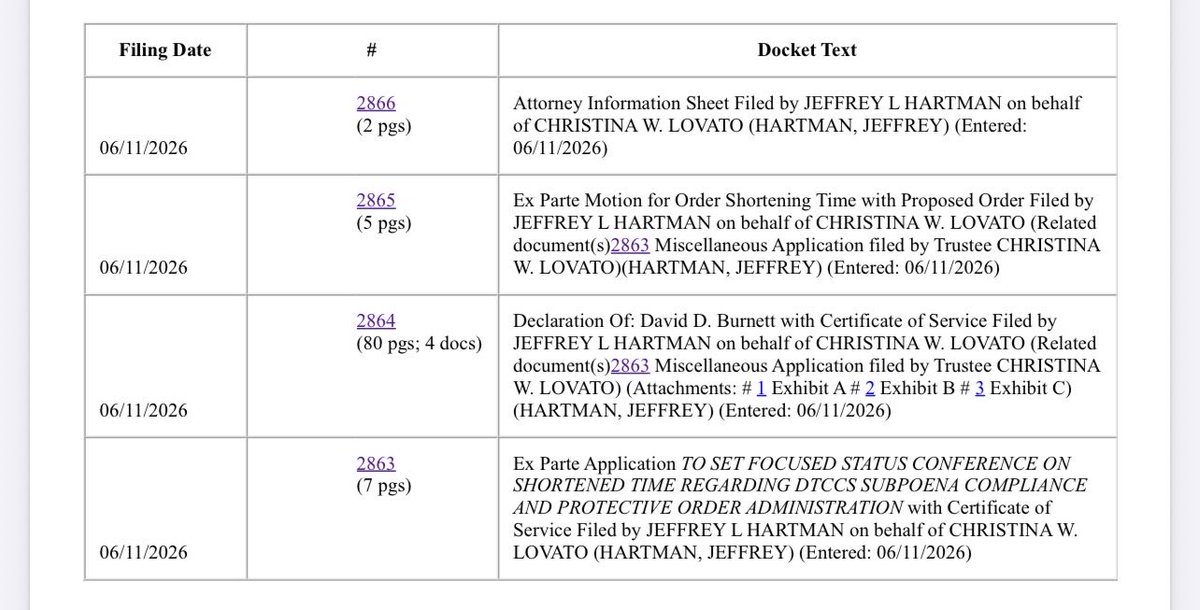

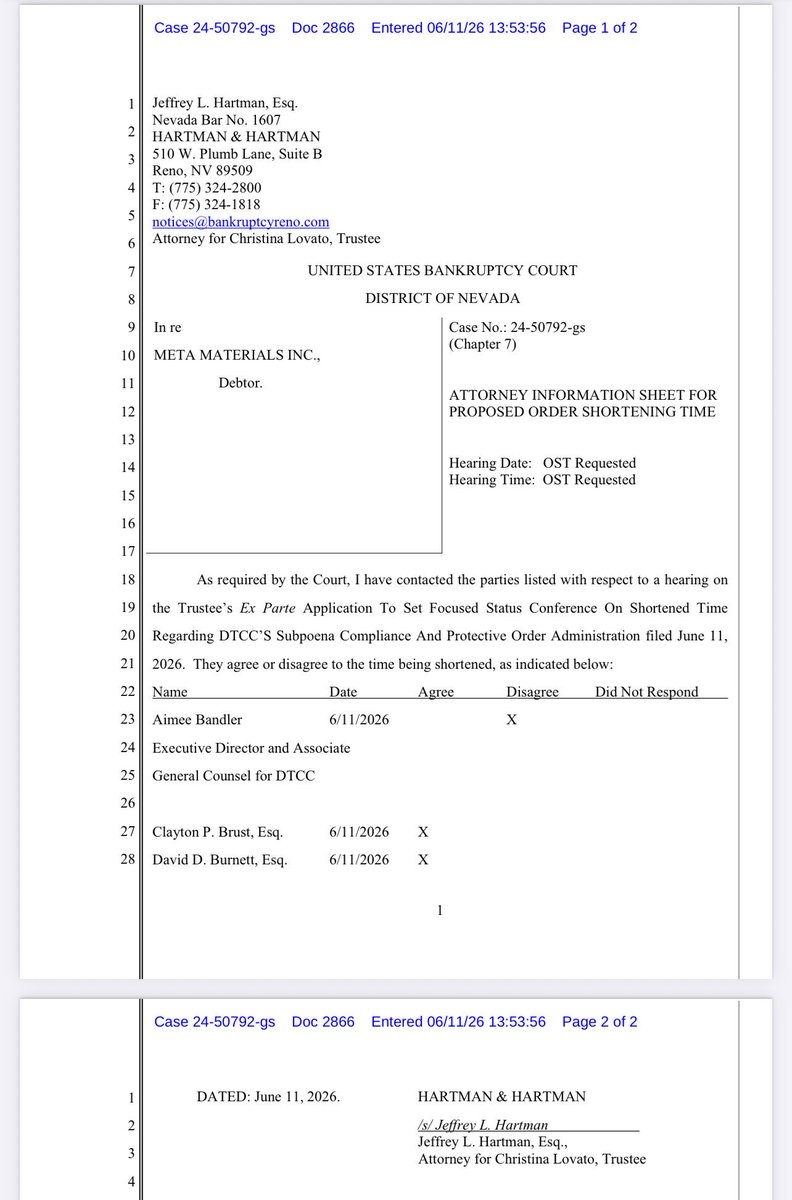

🔥 MMAT Update – June 11, 2026

📄 Docket Nos. 2863, 2864, 2865 & 2866

What happened?

Trustee Christina Lovato filed a series of motions asking Judge Spraker to schedule an expedited status conference regarding DTCC’s subpoena compliance and production delays.

⸻

🎯 The Main Issue

The Trustee says DTCC still has not fully produced certain subpoenaed records, particularly transaction-level Correspondent Clearing Data that has been requested since 2025.

According to Trustee counsel David Burnett:

“That data is very important to our analysis.”

In simple terms, this appears to be data that could help identify who was actually involved in specific trades, not just trading totals.

⸻

⏰ Why The Rush?

This is the biggest takeaway.

The Trustee specifically warned the Court that continued delays could impact potential claims because of statute-of-limitations deadlines.

Burnett also stated:

“Statute of limitations deadlines make DTCC’s immediate production … very time-sensitive.”

🚨 That’s strong language coming directly from Trustee counsel.

⸻

📬 What’s Next?

At this point:

✅ DTCC has not filed a Motion to Quash

✅ Trustee has not filed a Motion to Compel

✅ Trustee wants Judge Spraker to step in and hold a focused conference to address DTCC’s outstanding production and determine next steps.

⸻

👀 What Stands Out

The repeated focus on:

🔹 Correspondent Clearing Data

🔹 Transaction-level records

🔹 Time-sensitive discovery

🔹 Statute-of-limitations concerns

suggests the Trustee believes this remaining DTCC data is important to the ongoing investigation.

📌 Bottom Line: The investigation appears very much alive, DTCC remains an active discovery target, and the Trustee is pushing for answers sooner rather than later.

⚖️ Not Legal Advice • For Discussion & Entertainment Purposes Only ⚖️

dropbox.com/scl/fi/pzyf05xks…

dropbox.com/scl/fi/f5e7strlu…

dropbox.com/scl/fi/n7umzargy…

20

194

352

29,130

Kerr 🇨🇦 retweeted

Jun 11

📣📣KEN GRIFFIN BUYING POLITICIANS AGAIN

This is how Ken Griffin has built an empire.

He makes nothing but is the 35th richest person in the world.

Kenny is one of the largest political doners. Approximately donating over 285 Million since 2015.

Now you know why they investigated Andrew Left and not Ken Griffin.

24

226

513

8,361

Kerr 🇨🇦 retweeted

21 Jan 2025

🚨🚨 FORENSIC AUDIT 🚨🚨

📢🚨 DTCC AND BROKERS 🚨📢

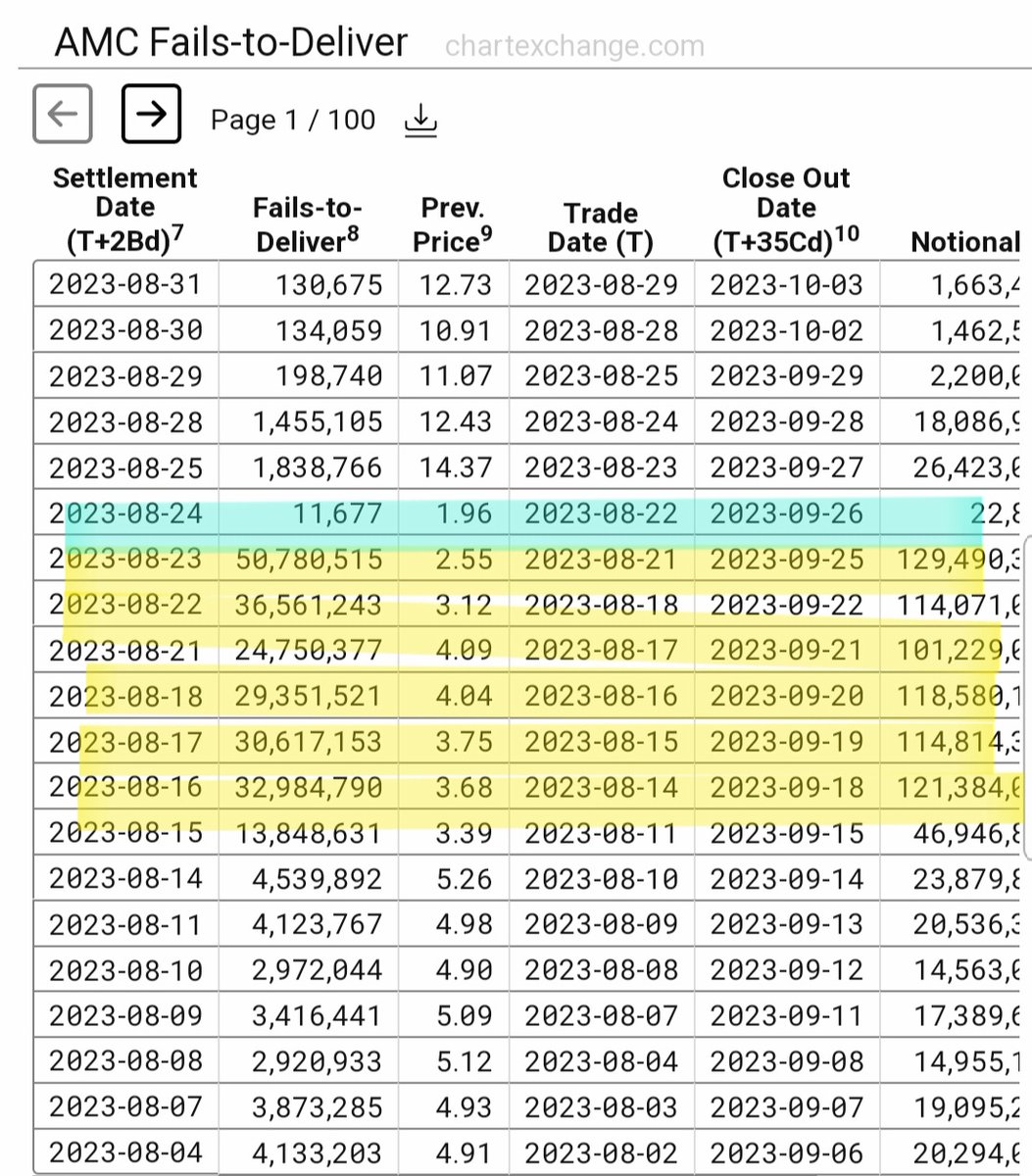

FTD's fails to deliver have become a massive problem that threatens national security and the global financial system

This is the practice where they sell securities they don't own and can't deliver or settle.

This creates synthetic shares way above the legally issued float.

This is facilitated by the @The_DTCC that allow fails to roll over indefinitely.

They don't settle the trades but take payment and don't deliver. Leaving many Retail investors with IOU's.

$AMC has been one of the companies that spent significant time on the Threshold list with over 50 Million FTD's at one point.

Many companies like $MMTLP $GME #DJT have also spent long periods of time on the Threshold list.

All of the companies that have huge short interest encounter fails that are compounding driving the companies market cap and shareholders value down because it artificially dilutes the company.

TRADE SETTLEMENT SHOULDN'T BE A OPTION BUT MANDATORY.

A forensic audit of the brokers and the DTCC is required to uncover the largest ponzi scheme playing out each and everyday.

@realDonaldTrump @MarkUyedaUS @Kash_Patel @DevinNunes @PamBondi

61

560

1,247

31,940

Kerr 🇨🇦 retweeted

Jun 11

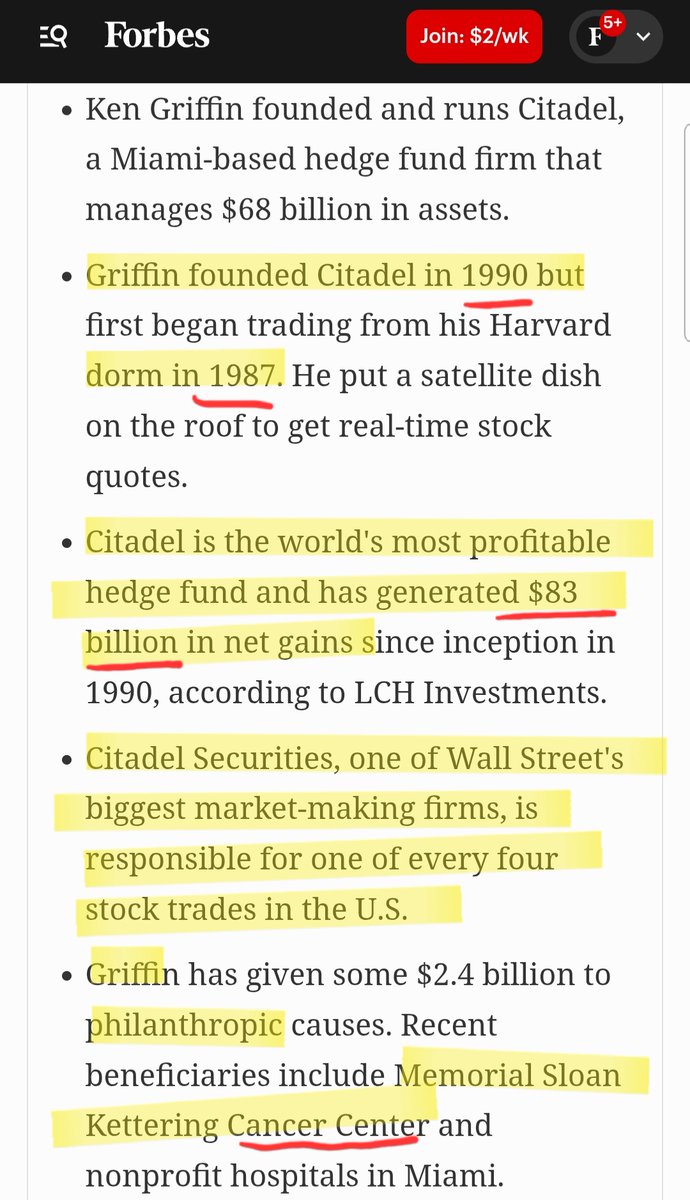

📣📣KEN GRIFFIN PARASITE OF WALL STREET

Ken Griffin's story 🤔

He started his career in his Harvard dorm in 1987.

3 short years later he starts what would become the world's most profitable Hedge Fund.

In 2002 he started Citadel Securities becoming one of the largest Market Makers executes one of every four stock trades in the US.

This is when Citadel became a Global Powerhouse. Could it be the conflicts of interest 🤔

Payment for Order FRAUD and front running.

Ken Griffin portrays himself as a philanthropist. Donation money to charity.

I find it especially interesting that Kenny recently donated to Memorial Sloan Kettering Cancer Center while shorting and trying to destroy NWBO a promising Cancer treatment.

13

139

355

4,080

Kerr 🇨🇦 retweeted

Jun 10

🚨🚨NO MISTRIAL ANDREW LEFT FOUND GUILTY AGAIN 🚨🚨

Left's defense team tried to argue that the trial was tainted and the jury used an outdated verdict form so the Judge should rule a mistrial.

The Judge took a different action sending the jury back with the correct verdict form.

JURY TOOK AN HOUR AND CAME BACK WITH GUILTY VERDICT AGAIN‼️

38

286

835

12,424

Kerr 🇨🇦 retweeted

Jun 8

📣📣WALL STREET 9 TRILLION ILLEGAL NAKED SHORT SELLING

Counterfeiting the Stock Market selling Billions of shares that were not issued by the company and are never delivered to the Shareholders.

THIS IS HAPPENING EVERYDAY‼️

Video credit @rogerhamilton

24

308

808

12,929

Jun 7

#GNS Float Breakdown/#RS Quell - Mechanics First (Early June 2026)

#NumbersOverNarratives.

Real #DD is becoming rarer and rarer in this #community. Not because it doesn’t exist, but because factual, mechanics driven #analysis doesn’t spread like “yes-man” hype, hopium, and superficial shout out farming.

I’m not here to spin #narratives, I’m not here chasing company recognition, or pats on the back. I’m here ONLY to deliver factual, Numbers over Narratives DD. Due diligence that arms #retail investors with real #mechanics so they can fight #TheSwamp on equal footing is my main purpose.

I don’t work for the #suits or #elites. My moral compass, and ethical makeup, are sound. Confusion over right and wrong has never been an issue for me. I only move for #retail.

With that being said…let me scratch that #GNS DD itch, and #quell the #RS Echo Chamber #FUD.

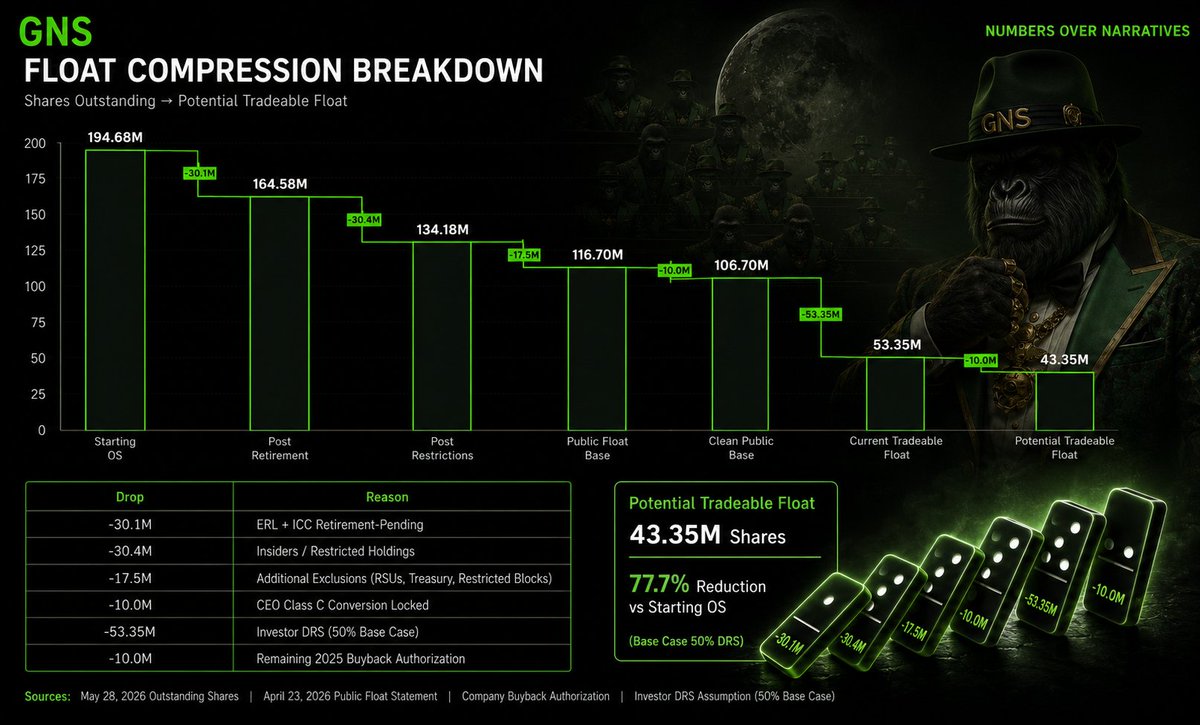

Verifiable Steps (Directly from Filings/Press Releases):

1. Starting #Total Issued/OS.

- 194.68M shares - verified as of May 28, 2026. No new shares issued since.

2. Minus #ERL #ICC Retirement - Pending (30.1M).

- 22.7M unclaimed ERL 5.5M returned 7.4M ICC arbitration award (already at Vstock).

- 194.68M – 30.1M = 164.58M.

3. Minus Insiders/Restricted (30.4M).

- Book entry at Vstock (per April 23, 2026 press release).

- 164.58M – 30.4M = 134.18M.

4. Company Stated Remaining Public Float Base.

- 116.7M shares (explicitly stated April 23, 2026).

- Why the ~17.5M gap exists (134.18M to 116.7M): Additional company defined exclusions include other restricted blocks, unvested RSUs, treasury adjustments, and items classified as non-public.

5. Minus 10M CEO Class C Conversion.

- June 1, 2026 conversion to super voting shares held at Vstock (non-tradable).

- 116.7M – 10M = 106.7M.

Current Tradeable/Broker Lendable Float Post Step 5 (this is now opinion and forward based thinking):

- Base Case (50% Investor DRS on 106.7M base):

- 106.7M × 50% = 53.35M locked and 53.35 million tradeable.

At the current 3 month average daily volume of ~8.7 million shares, the Base Case 53.35M tradeable float already equates to only ~6 days of normal trading supply.

Reported short interest sits at ~6.85M shares. On the Base Case 53.35M tradeable float, this represents a ~12.8% short ratio, and that pressure intensifies significantly as the float compresses further through buybacks, retirements, and DRS.

Continued Compression Levers Remaining 2025:

- Remaining 2025 Buyback Authority: ~10 million shares left (expires July 7, 2026 AGM). Roger can execute fully before then at ~$2.3M cost (@ $0.23).

- If executed: Post buyback tradeable float drops to ~43.35 million (Base Case).

- New 2026 20% Buyback Mandate (to be voted July 7): ~38.936 million shares equivalent. Combined with the remaining 10M, Roger would have potential authority for up to ~49 million shares of buyback firepower.

Combined Post Retirement Post-10M Buyback Scenario (Base Case 50% DRS):

-Tradeable float compresses to the ~38–40 million zone once the 30.1M ERL/ICC shares are finally cancelled. This would represent roughly a 75–80% reduction from the original 194.68M issued OS in effective lendable supply.

Float Compression Roadmap (Base Case 50% DRS):

- Current (early June): 53.35M (~72.6% reduction).

- After remaining 10M Buyback: 43.35M (~77.7% reduction).

- After 30.1M Retirement Buyback: ~38–40M (~79–80% reduction).

***Note on the ~40.1M Shares (30.1M ERL/ICC 10M CEO Class C)***

- These remain technically part of the issued share count pending final actions. The 30.1M ERL/ICC block is already at Vstock and targeted for treasury/permanent cancellation “as soon as practical.” This limbo explains why short pressure can persist until resolved, and why the RS angle is being trolled.

The Conditional 10-for-1 RS Authority - Pure Protective Layer (Trolls are hammering the reverse split language, here is the mechanics reality):

- The proposed 10-for-1 conditional share consolidation is STRICTLY discretionary safety net authority. The Board can use it (or not use it) solely if needed for NYSE American compliance. The trolls framing this as “they’re about to RS next month” are mislabeling the language and framing intentionally. It is insurance, not intention.

- Even if activated, a new 10-for-1 (which I'm absolutely against) would bring the two year cumulative ratio to 100:1. Which is still well below the NYSE American 200:1 limit. The authority is safe to have in the back pocket.

- Having the RS in our back pocket guarantees that GNS will continue trading on the NYSE American no matter what. It addresses the $0.25 hard floor effective October 1, 2026 (any close below $0.25 triggers IMMEDIATE suspension/delisting with no cure period). The RS is a LAST resort insurance IF timelines drag due to Swamp mechanics, but based on the structure above, it should not be needed.

Why the RS Should Not Be Needed:

-Nearly 4 months of runway until the hard floor.

- Ongoing structural compression (DRS retirements buybacks).

- Strong catalyst calendar well before October 1.

- AGI Infinity Portfolio deployments (already started June 1; Phase 1 up to $100M with major pre-IPO AI exposure).

- Legal resolutions 30.1M share retirements.

- ASX dual listing progress.

- Jewel Digital Bank/JUSD stablecoin kickoff (H2 2026). BTC Loyalty Program Round 2 (ongoing DRS incentive).

- Bitcoin treasury growth, AI education revenue ramp, and more.

- No dilution from the recent AGI additions (all funded from existing resources.)

DRS Scenarios (on 106.7M base):

- Bear (40% DRS) → 42.68M DRS → 64.02M tradeable

- Base (50% DRS) → 53.35M DRS → 53.35M tradeable

- Bull (60% DRS) → 64.02M DRS → 42.68M tradeable

Why 50% DRS is Reasonable & Conservative (Base Case):

Pure investor DRS reached ~18.2% mid 2025 and total book entry hit 60.3% by September 2025. The BTC Loyalty Dividend flywheel plus 2 years of consistent push create steady momentum. 50% is balanced and accounts for real world friction.

Bottom line, the mechanics show a tightening supply structure, multiple near term catalysts, and protective tools in reserve. The RS language is being weaponized, but the verifiable math and catalyst timeline tell a much STRONGER story.

Key Takeaways:

- Verifiable tradeable float is already tight at ~53.35M (Base Case).

- Structural tools are actively compressing supply.

- Multiple high conviction catalysts are lined up before the October hard floor.

- The RS is discretionary insurance, not the plan.

The mechanics favor long-term holders. Numbers over Narratives, and #Paytience is the weapon they hate most. I have my #popcorn ready.

OneLove and StayBlessed

DiggerBG

NFA/DYODD

#GNS #DominoThesis #NumbersOverNarratives #FAFO #TickTock #AGI #DiggerBG #SpaceX #Anthropic #OpenAI #IPO #SWAMP @rogerhamilton #DRS #VStock #LockIt @geniusacademyai

1

4

619

Jun 7

RT @rogerhamilton: The $GNS White Paper - Our detailed case for why we believe the AGI Economy will grow 2x-5x in 12 mths and 10x-100x in 3…

44

Kerr 🇨🇦 retweeted

31 May 2024

#KenGriffin is a Financial Terrorist

He has killed American innovation. What company wants to go public knowing they will be attacked as soon as they do. Old Kenny and his band of merry thieves have even tried to kill a cancer treatment. He should have said we have been so good at stealing from families I made 4.1 Billion in 2023

#AMC #MMTLP #DJT #HYMC #MMAT #GNS #MULN #BBBY #GME #NWBO #SCLX #GTII #BBIG #BBBY

47

285

844

29,339

Kerr 🇨🇦 retweeted

11 Jun 2025

8/10 $MMAT and $MMTLP: Lambs to the Slaughter? Not Anymore...

The U3 halt wasn’t a glitch. It was structured negligence in my humble opinion.

Retail watched as phantom shares flooded the system, FTDs and short interest outpaced the laws of physics.

Dartmouth’s Reg SHO at Twenty confirms in p. 29:

"The highest FTD level was $20.3 billion on 23 September 2008. Notably, the second highest FTD level was $19.8 billion on 23 September 2024. Median FTDs were $2.26 billion for this period."

Loopholes designed, not accidental...

(Source: papers.ssrn.com/sol3/papers.…)

🧾 And the FOIA docs?

They expose coordination between FINRA, OTC, DTCC & SEC, timelines, names, silence.

No one blinked when $MMTLP got halted.

They knew. They went silent for months until they could put together a story which was revised at least once almost a year after the halt: finra.org/investors/insights…)

But here’s what they didn’t plan for:

✅ 65,000 relentless/retail shareholders.

✅ A court-appointed Trustee following the paper trail.

✅ Two management teams flagging misconduct, and legal and financial teams, collecting all available trading data to understand the size of the problem.

✅ And a small group of quiet allies in Congress—watching, building the record, preparing the next move.

They thought we’d fold.

They miscalculated.

Welborn’s paper confirms what we all have come to know: Market makers exploited Reg SHO’s “bona fide” exceptions to naked short with impunity.

MMTLP’s over a month on the Threshold List wasn’t a glitch, it was a feature. The SEC’s inaction? A neon sign reading “Come manipulate here!”

10

184

322

8,744

Kerr 🇨🇦 retweeted

Now we can drain the swamp!

#MMTLP found the smoking gun of financial institution collusion with the SEC, and how many of the SEC working complicit are still there?

Well, looks like Trump can now clean house and get them all out of there, and promote good people with in there that can help clean up the mess the corrupt people in the SEC created!

The weaponization of the SEC against the American people is over!🇺🇸

RICO of all RICOs!

I don't have any insider information. I don't know anything other than that there are a lot of bad people that are totally FUKT!!! Justice incoming!

21

185

547

39,680

Kerr 🇨🇦 retweeted

$VIRT

HEADED TO DISCOVERY

Bloomberg Law reports a judge denied Virtu Financial’s motion to dismiss a lawsuit filed by Iron Workers Local No. 55 Pension Fund

They allege owner Vincent Viola rigged a huge stock buyback to funnel more than $400 million to himself and insiders at the expense of regular shareholders.

A few of my previous posts

1)

March 2025

"Pension fund accuses Panthers owner Viola, partner Cifu of stealing $400 million owed to investors in Virtu Financial…

….follows an earlier suit by the pension fund that asked a judge to force Virtu to turn over its books and records for it to investigate suspicions of “apparent wrongdoing.”

x.com/kshaughnessy2/status/1…

2)

December 2024

I had even more questions after $VIRT's CEO attacked my post questioning how many FTD's Virtu Financial has.

x.com/kshaughnessy2/status/1…

3)

December,2024

"Activist Investor, Pulte, Calls for Virtu Financial to Be Sold"

x.com/kshaughnessy2/status/1…

4)

December 2024

“…The devil is in the details as to what asset class of companies are they short?

Even 5-10% of their 6B short book can blow them up in a day if they all have to be covered..”— @FlyEaglesFly529

x.com/kshaughnessy2/status/1…

5)

June 2025

Months before he became SEC Chairman Paul Atkins was an expert witness for Virtu Financial in its court battle with the SEC???

And now as the SEC Chairman he polices Virtu?

x.com/kshaughnessy2/status/1…

6)

May 2026

This Is Big

Major Court Ruling Against

“🏢 Citadel Securities

🏢 Virtu Financial

🏢 Anson Funds

@kimkep4796

x.com/kshaughnessy2/status/2…

23

117

386

13,057

Kerr 🇨🇦 retweeted

May 31

Context and relativity.

Treasury bled $5T/yr and no one commented or cared.

If MMTLP is oversold by 1B, every $1000/share is $1T.

Financial impact is not a legimate concern. Shorts have the money to settle their debts, but even if they didn't, an arrangement (time, etc) could be facilitated.

#ChopChop

May 31

HOLY SH*T 🚨 D.O.G.E. reveals the Department of Treasury was spending around $5 TRILLION a year without any "budget codes"

"They were basically partying on taxpayer money”

I WANT A REFUND IMMEDIATELY

7

66

118

3,885

Kerr 🇨🇦 retweeted

May 29

They have this S1. Memorized they have only been reading it for 3 years and 4 months. The only thing that has changed is the fing financials that they fing requested on 2 different occasions costing the company millions of dollars in accounting and legal fees for a fing company that doesn’t fing trade. I want every shareholder to remember this shit when they consider any settlements well as the lost opportunity cost in the market for the past 3 years and 4 months of waiting on this approval for effectiveness. F the SEC AND F FINRA for this BS. I’ve held this in for over 3 years out of respect for all shareholders and for NBH. ITS OUR TURN TO EAT AT TROUGH AND WE ARE FING HUNGRY!!!

24

142

352

13,818