Personal finance writer @Thefynprint

Joined February 2019

- Tweets 538

- Following 125

- Followers 3,410

- Likes 2,349

52 Photos and videos

Funny how multi billionaires worry about birth rates.

India doesn’t need lectures from Elon.

It needs better jobs, cleaner cities, stronger institutions, corruption free leaders and higher living standards.

Population size alone isn’t a success metric.

128

49

2,513

279,922

Anil Poste retweeted

May 28

How much do you know about markets outside India? Drop your answers in the comments & tag @thefynprint. We will tell you if you're right!

2

2

23

10,062

May 15

Indian investors: ‘Let’s diversify globally.’

RBI limit: ‘Absolutely not.’ 💀

To make things easier, we built a live feeder fund tracker that shows which funds are open, restricted, or paused for fresh investments. Link in comments @thefynprint

1

3

225

May 15

Feeder fund - thefynprint.com/feeder-funds…

Other live trackers-

World market returns - thefynprint.com/world-index-…

GIFT outbound funds - thefynprint.com/gift-city-ou…

1

1

154

Anil Poste retweeted

Probably @PosteAnil meant, that is the actual yield investor got for the price 1 year ago. It can’t be considered as an yeild for today’s maket price

1

1

1

360

Apr 3

Hi @leading_nowhere

The yield figures in the infographic are based on trailing 12-month distributions (annualised) from disclosed payouts, not just the latest run-rate.

The CAGR includes total return, not just price movement. we also spoke IndiGrid.

2

1

2

1,489

Apr 3

We will still recheck the numbers and will update if needed.

Could you share which source you’re referring to?

1

394

Mar 5

Well captured @partha0799 !

Mar 4

I’ve followed @deepakshenoy for ~4 years.

Read most of his blogs. Also a long-time reader/supporter of @CalmInvestor’s writing.

But one framework he shared today really stuck with me.

I was on a call hosted by @PosteAnil & @ActusDei on asset allocation.

One point stood out.

Deepak said many investors ignore multi-asset funds because in a good year they may slightly lag pure equity returns.

Fair point.

But he added something deeper.

Most investors saying this haven’t built portfolios during brutal drawdowns.

Take something like March 2020.

Markets fell ~38%.

When you start investing, a fall like that doesn’t feel as scary.

Because your portfolio might be ₹2–5L.

But fast forward a few years.

Suppose you earn ₹12L a year and your portfolio grows to ₹30L.

Now a 35–40% drawdown isn’t just “market volatility”.

It’s suddenly ₹10–12L evaporating.

That’s almost a year of your salary.

That’s when you truly start questioning your investment hypothesis.

And that’s also when investors finally appreciate:

• diversification

• asset allocation

• different asset classes doing different jobs

When I started investing, my framework was simple:

Equity Gold.

But as the portfolio grew, so did the need for stability.

So I slowly added:

• corporate debt

• REITs

• InvITs

• diversified exposures

Your asset allocation evolves with your portfolio size and emotional tolerance.

Most people only realise this after their first big drawdown!

If you’re building a long-term portfolio, the allocation matters more than the product.

Learn more: advisoira.com

1

728

Anil Poste retweeted

Feb 1

Had an interesting session with @AashishPS (@WhiteOakCap) and walked away with a completely different way of thinking about diversification, risk, and long-term wealth.

c.c @ActusDei @PosteAnil

Here are some insights on global diversification, silver and more 👇

⸻

1. Why passive worked in the US — but the comparison with India is flawed

The US didn’t outperform because it is “better”.

It outperformed because of market structure:

• Fewer listed companies

• Massive buybacks

• Cross-holdings

• Private equity takeovers

• Rising valuation multiples

In 30 years, US market cap grew 6x, while the number of listed companies fell ~40%.

This concentration and capital discipline is what made passive investing work so well.

India does not share this structure.

Comparing Indian markets to US indices is like comparing two different machines with the same fuel.

⸻

2. REITs & InvITs are true diversifiers — when used correctly

REITs and InvITs hold income-generating assets with long-term lock-ins.

Their key role is not just growth — it is income stability and diversification.

Yes, market prices can move.

Yes, yields can compress when prices rise.

But the underlying cash flows continue to grow, which puts a natural floor under yields.

They are structural stabilisers, not tactical trades.

⸻

3. Global diversification is not about tax or currency only — it’s about purchasing power

Most investors judge global investing by:

• Taxation

• Currency movement

Both matter.

But they are not the real risk.

The real risk is this:

If your country underperforms, your entire wealth base is shrinking in global terms — even if your portfolio is “up” in rupees.

A depreciating rupee and weak domestic returns quietly erode your real purchasing power.

Global investing is about protecting future lifestyle, not chasing returns.

⸻

4. Most Emerging Markets products are not diversified for Indian investors

India is already ~20% of majority EM indices.

So when Indian investors buy EM funds,

they’re often just buying more India.

True diversification today is Ex-India global exposure — where economic cycles are uncorrelated.

@WhiteOakCap’s fund here is Ex-India.

⸻

5. Commodities are macro hedges, not wealth creators

Commodities are country-cycle trades.

They benefit exporting economies, not consuming ones.

For India, they behave like cost inputs, not long-term return engines.

That makes them useful as tactical hedges, not strategic portfolio anchors.

⸻

6. Risk is not volatility — it is permanent loss of capital

Price movement is noise.

True risk is not getting your money back.

If earnings grow, returns may be delayed — not denied.

⸻

7. Equity sits at the top of the value chain

If you understand:

• Business

• Governance

• Capital allocation

And economics :)

Then equity is where long-term wealth is actually created.

But markets are not economies.

⸻

8. Not all strong economies produce strong stock markets

Example:

Samsung is ~27% of the Korean stock market.

So if Samsung underperforms,

Korean indices suffer — even if the economy is doing well.

Index performance is a function of concentration, not just GDP.

⸻

9. Markets move like a sine wave — not a straight line

They are driven by human behaviour, not logic.

That’s why behavioural economics won a Nobel Prize.

Because people are not rational — they are emotional.

⸻

10. Asset allocation is alchemy, not mathematics

1 1 ≠ 2

Correlations change.

Volatility blends.

The right mix can increase returns and reduce risk at the same time.

That is real diversification.

⸻

Final takeaway:

@AashishPS mentioned he’s 50, (I’m almost half his age :)) but here’s what his core philosophy is:

Life, investing, and business are not about maximising one variable.

They are about optimising the entire system.

If you liked this thread, follow @partha0799 for more :)

5

9

34

4,665

Jan 31

Let's goo! 😎

Jan 31

#Budget2026 is almost here, and we are decoding it LIVE tomorrow. 🇮🇳

We’re bringing you live insights from the finest minds—Neil Borate (@ActusDei), Anil Poste (@PosteAnil), Ira Puranik (@PuranikIra), and Vedant Vichare —as we break down how this budget affects your wallet.

Join #BudgetWithThefynprint on our live Twitter threads as we focus exclusively on Personal Finance topics.

Follow @thefynprint and turn on notifications 🔔 to catch every update.

What are you most excited to hear about? Let us know in the comments! 👇

@nsitharaman @FinMinIndia #finance #thefynprint

1,133

Jan 14

Have you ever filed a travel insurance claim for a flight cancellation, delay, lost baggage, or any other issue? Were you successful in receiving the payout? If not, what challenges did you face?

This is for a story, please DM or comment @ActusDei @thefynprint

2

9

5,722

Anil Poste retweeted

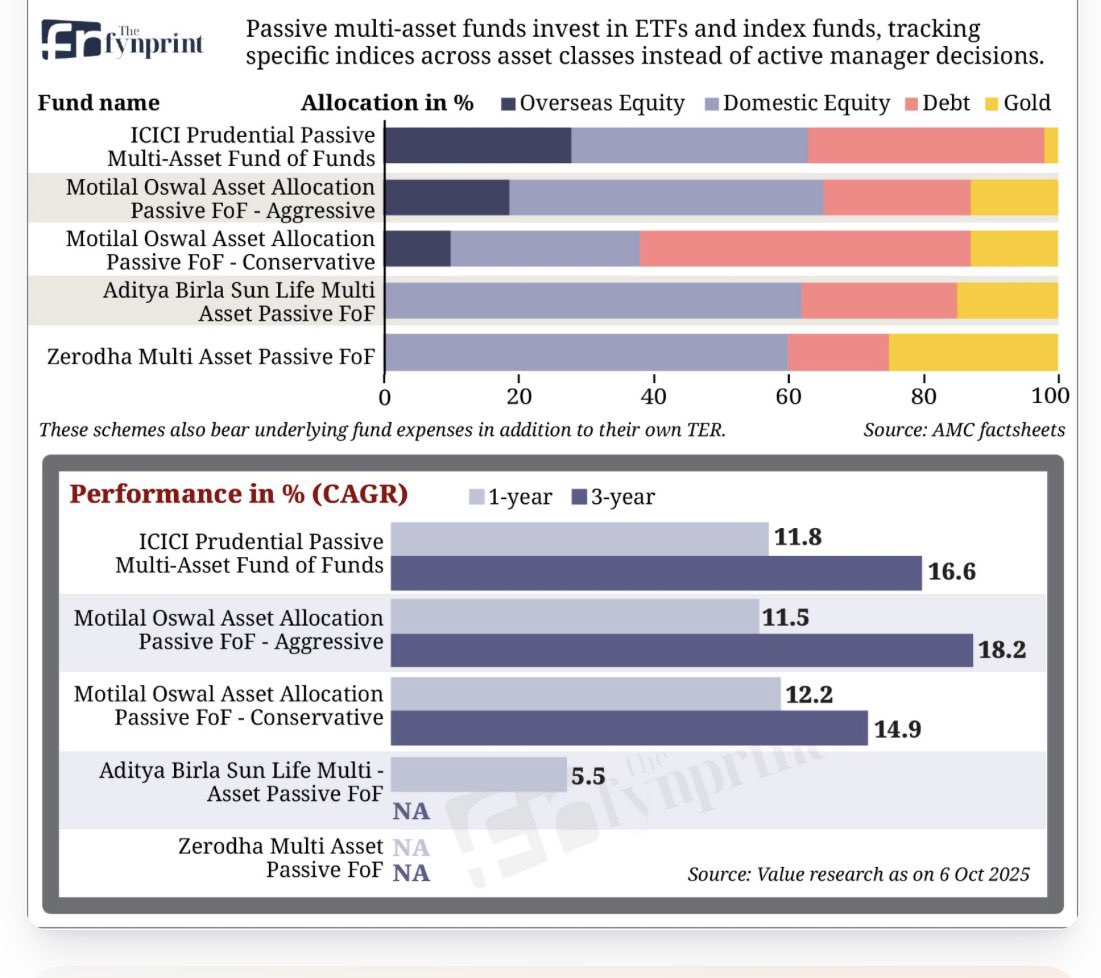

In continuation to my previous learnings on Multi asset allocation fund I came across with a good article in my email by @thefynprint (link attached at last).

Summarising the article by @PosteAnil with good data points below.

1. How Different Schemes Allocate ?

Funds like ICICI Pru, Motilal Oswal, Aditya Birla and Zerodha Passive FoFs follow different models.

ICICI Pru stands out for higher global exposure, Motilal Oswal has both aggressive (equity-heavy) and conservative (debt-tilted) options while ABSL and Zerodha maintain domestic focused allocations.

2. ICICI Pru and Motilal Oswal Highlights

ICICI Pru Passive FoF roughly splits into 28% global equity, 35% domestic equity, 35% debt, 2% gold.

Motilal Oswal’s aggressive variant leans on Indian equities US exposure gold whereas its conservative version is debt focused with mild equity and gold exposure.

3. Tax-Efficient Rebalancing

Rebalancing inside the fund doesn’t trigger capital gains tax.

Investors avoid tax leakage that normally occurs when shifting money between equity, debt, or gold on their own.

To Conclude:

These funds suit longterm investors wanting steady growth with lower volatility.

With global exposure built in diversification and automatic rebalancing at low cost passive multi-asset funds offer a balanced, hassle-free investment journey.

Link to the full article: thefynprint.com/investment/p…

#markets #Nifty50 #learning #wealth

@swing_blaster @Paryan_Sharma @Shantanu10101 @OneWhoNeverSell @TheAlpha10X

I often read about diversification and try to find what could be a suitable option available through mutual fund route.

An option which is well diversified across different asset classes and different regions.

I came across a Multi asset fund which I find interesting to discuss.

This is inline with my previous post on Multi asset funds.

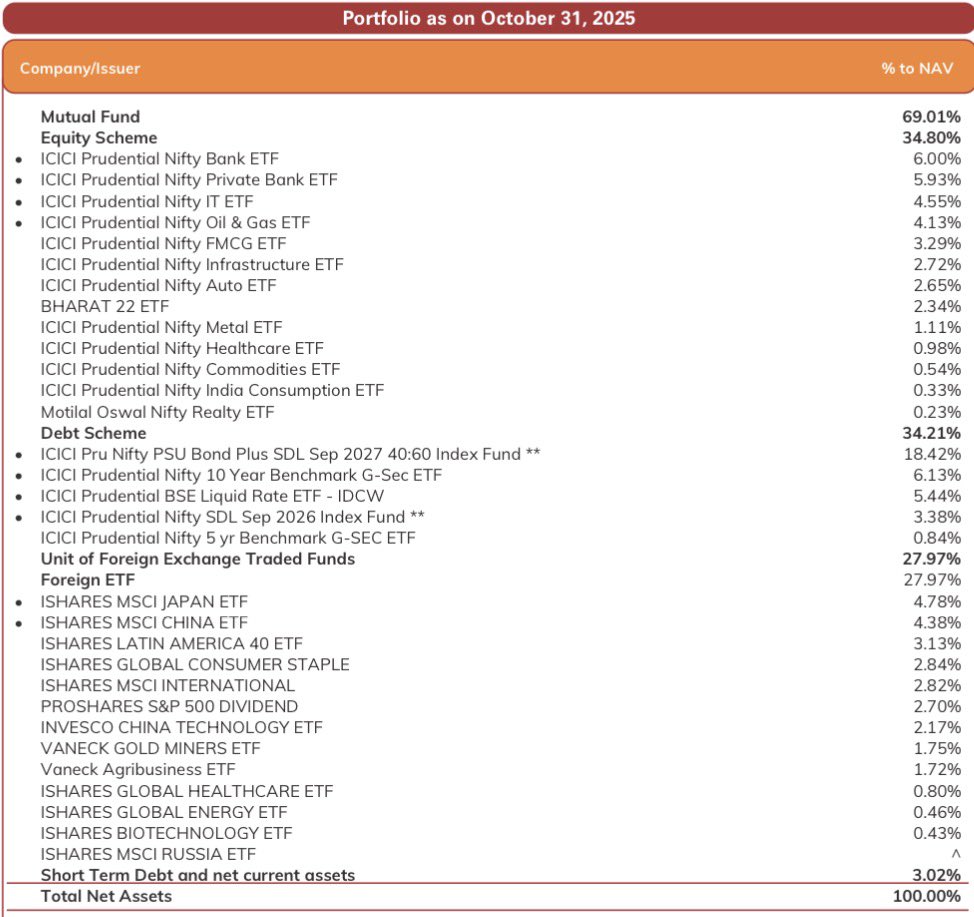

Sharing the details of ICICI Prudential Passive Multi-Asset Fund of Fund.

1. Asset Allocation

- Domestic Equity ETFs: 69% (rounded off to whole number)

- Domestic Debt ETFs: 14%

- Global ETFs: 28%

- Commodities exposure is less than 2%

- A simple spread across India, global markets and debt. This is highest among exposure to global equities in Multi asset category.

2. Portfolio Snapshot

- A basket of ICICI equity ETFs (Banking, IT, Infra, Oil & Gas, Auto, Metals, Healthcare, Consumption, Realty).

- Debt ETFs (PSU Bonds, G-Secs).

- Global ETFs (Japan, China, S&P 500, MSCI USA, EM, Healthcare, Biotech, Robotics, Gold Miners).

- A ready made diversified global portfolio inside one fund.

3. Total Expense Ratio

- Regular is 0.62%

- Direct is 0.22%

- It is low for a multi-asset and global exposure product.

4. Benchmark

CRISIL Hybrid 50 50 - Moderate Index (80%) S&P Global 1200 Index (15%) Domestic Gold Price (5%) (Benchmark)

5. What I do not find suitable ?

Double layer costs as underlying ETFs also have their own TER.

To Conclude:

It is a simple fund of fund with good exposure to global equities managed by experienced fund mangers.

#Nifty50 #sp500 #mutualfundsahihai #WealthManagement

@Anvith_ @suryachaudhary1 @Frontlineflex12 @purshottamxp @viralbshah @rohantantia

4

4

19

2,235

14 Dec 2025

Hi everyone

I’m exploring inbound Portfolio Management Services (PMS) based in GIFT City that accept investments from US citizens.

If anyone in my network knows of such PMS providers, please DM or comment. @ActusDei @thefynprint

2

4

1,148

10 Dec 2025

I’m writing a story on offbeat, budget-friendly New Year destinations.

If you travelled to Oman, Qatar, Egypt, Georgia, Uzbekistan, or Kazakhstan and can share your experience, DM or comment to connect. @ActusDei @thefynprint

2

1

5

3,538

Anil Poste retweeted

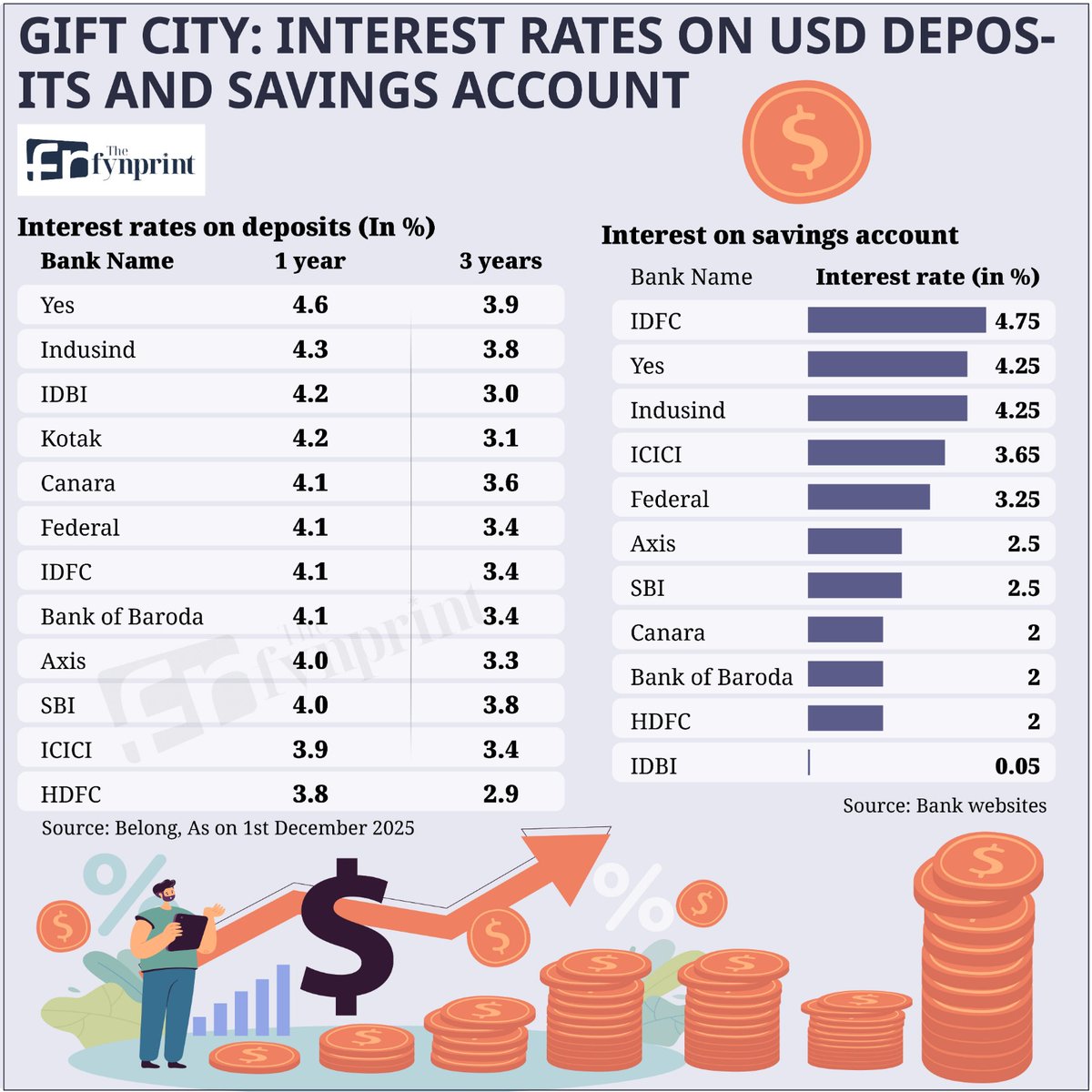

3 Dec 2025

An excellent compilation by @PosteAnil with inputs from @ankurc07 of @GetBelong of GIFT City FDs & savings account rates for NRIs. To learn more about global investing, sign up for my upcoming webinar on Friday at 7 pm payments.cashfree.com/forms/…

8

21

158

12,828

Anil Poste retweeted

26 Nov 2025

How to link NPS with CAS for Kfin and CAMS users. @PosteAnil provides these amazing practical tips. If you like his work, please repost and join our personal finance community docs.google.com/forms/d/e/1F…

26 Nov 2025

For KFIN and CAMS CRA users:

You can opt in for CAS statements by logging into your NPS account

After logging in - go to the "statements" tab

Select the "CAS" option,

Provide your consent for sharing your NPS details with the depository and click "Submit".

4

18

93

26,047

Anil Poste retweeted

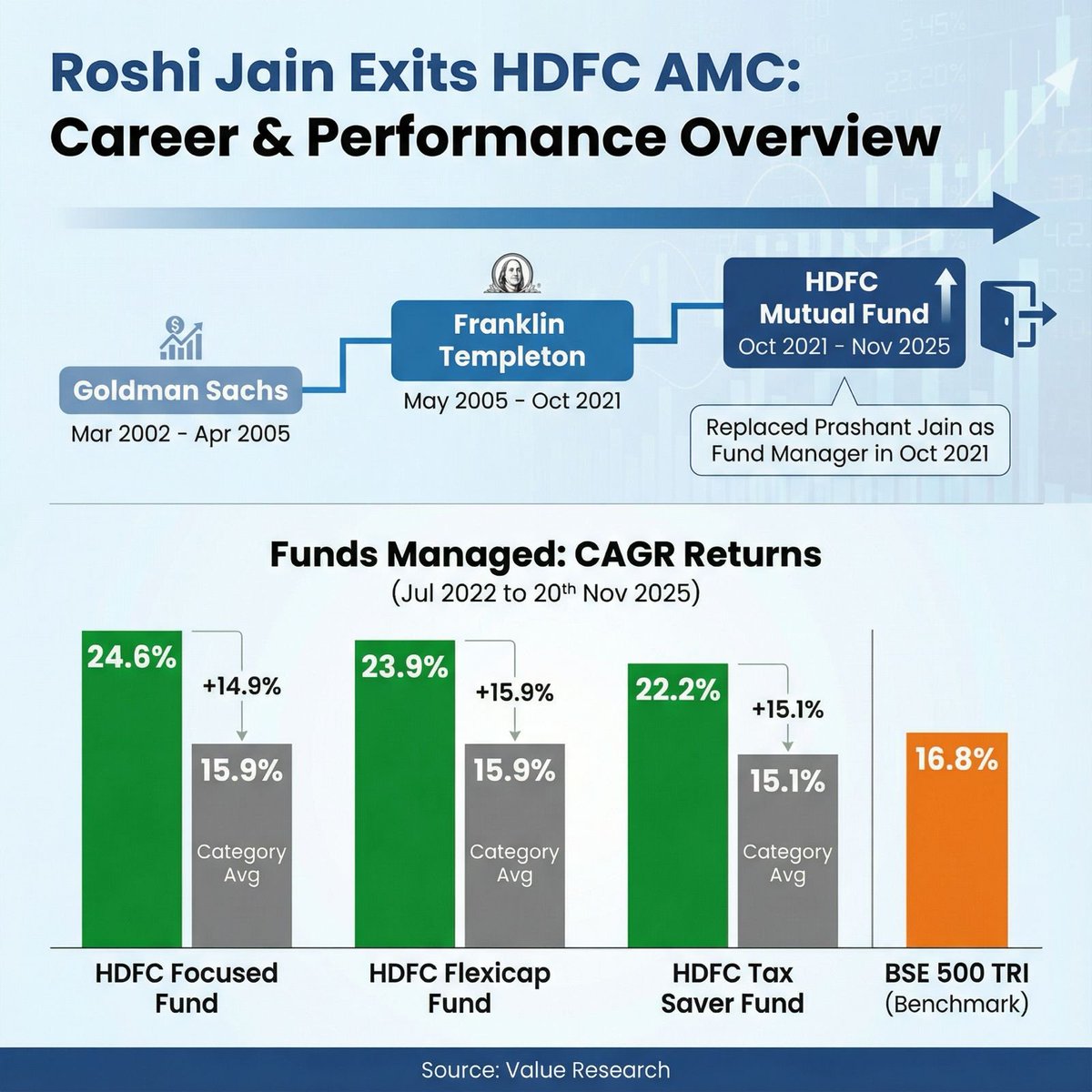

21 Nov 2025

Roshi Jain’s HDFC AMC Journey Ends With a Strong Performance Run; by @PosteAnil in @thefynprint

- Credited for delivering consistent alpha across flagship equity schemes

- Schemes managed; HDFC Focused Fund, Flexi Cap Fund, Tax Saver Fund

- What should an investor do when a fund manager exits?

& My views...

5

6

85

15,372

22 Nov 2025

Parag Parikh AMC Looks to Expand GIFT City Offerings, soon to launch passive outbound funds, Eyes NPS Entry. Read more: thefynprint.com/5ah92KCMO @ActusDei @thefynprint

5

608

Anil Poste retweeted

15 Nov 2025

What influencers DON'T tell you about PMS.

1) You are taxed on churn

2) No tax deduction on PMS fees

3) High & complex costs

Why are PMSes being promoted relentlessly?

92

61

527

76,698

Anil Poste retweeted

15 Oct 2025

Some personal news!

I’ve joined @TheFynprint after a fulfilling stint at ET Wealth. In my new role, I'll be diving deeper into stories that simplify insurance, investing & more. Looking forward to working with @ActusDei

For ideas and concerns, reach me at ira@thefynprint.com

3

2

13

15,818