A community where pros & traders of all levels team up with one common goal of crushing the markets. Focused, noise-free collaboration. NO BS ALLOWED

Joined July 2021

- Tweets 2,446

- Following 99

- Followers 3,991

- Likes 2,496

600 Photos and videos

“The mistake 98% of money managers and individuals make is they feel like they have got to be playing with a bunch of stuff. And if you really see it, put all your eggs in one basket and watch the basket very carefully.”

Druckenmiller

1

181

Nomura Cross-Asset – “TOUGH SCENE” (Charlie McElligott, ~June 10/11, 2026)

Overall Tone

Pragmatic but clearly more cautious near-term. McElligott is not turning bearish on the AI capex story itself, but he is highlighting that the narrow leadership (Mag7 Semis) is now facing both mechanical downside risks and a new structural headwind from equity supply. The tone is “the reversal we’ve seen is real, and the regime has shifted.”

TL;DR

The recent multi-day reversal in AI leadership was the mechanical inevitability he had been warning about (negative gamma LevETF rebalancing). It is now being compounded by a structural shift: Hyperscalers are moving from being a powerful demand tailwind (via buybacks shrinking float) to a potential supply headwind (equity issuance massive AI IPO calendar). This is pressuring the “Spot Up, Vol Up” regime and making new index highs much harder without Mag7 participation. He remains medium-term constructive on AI capex broadening, but the local setup for equities is tougher.

Key Points Breakdown

1. Tokenomics Pressure Returns

Fresh WSJ headlines on OpenAI considering significant token price cuts.This adds to already “fickle sentiment” around AI scaling economics and projections.2. Hedges & Downside Protection Back in Vogue

Loaded risk window ahead: ORCL AI re-read disappointment (stock -10% post-market on “data center costs overshadowing growth”), SPCX on Friday, and Fed next week.Explicit callout of large SMH put spread buying by Nomura clients over the last two days (Jul 545/525 put spreads in size).3. Negative Gamma is “Spooky Large”

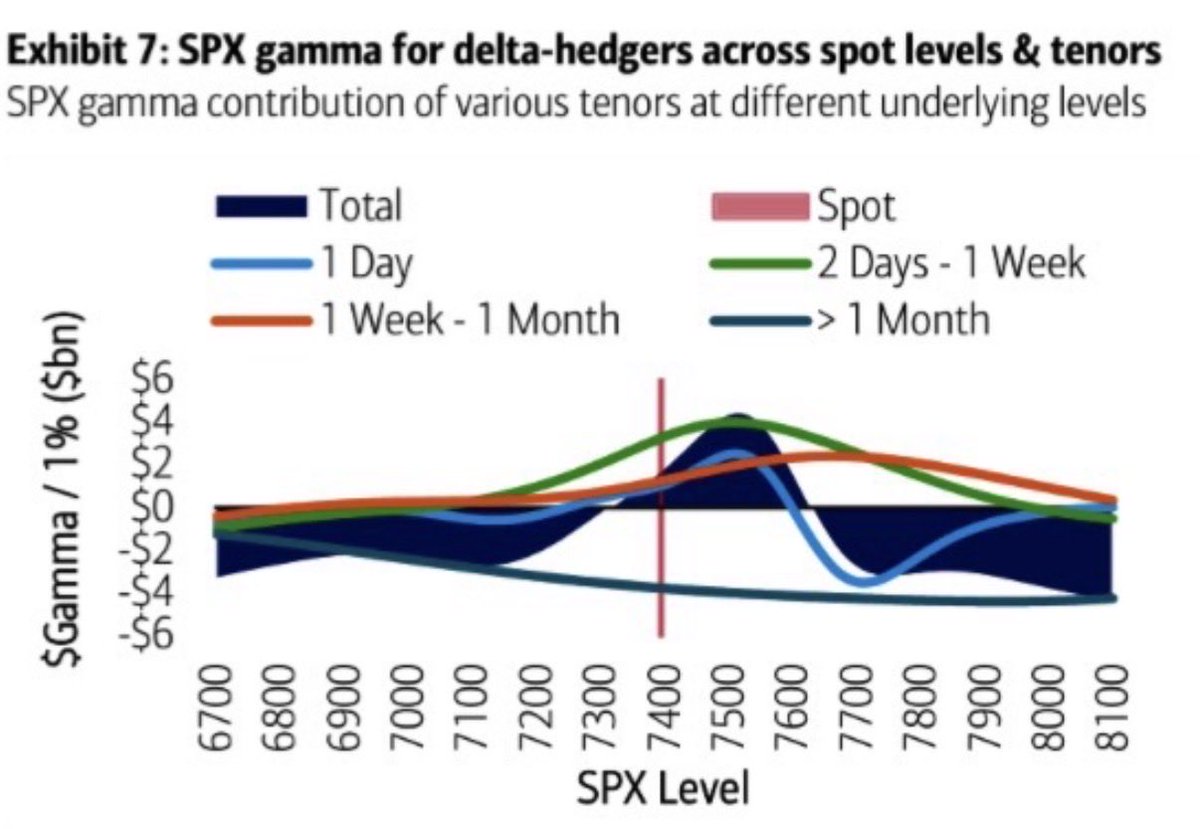

Real gamma (options): ~$5B per 1% on SPX.Synthetic gamma (LevETFs): ~$8B per 1%.These levels will super-charge moves in either direction and feed prevailing market direction.4. Vol Regime Has Shifted (As Anticipated)

Skew is re-steepening in the obvious “Patient Zeroes” (Mag7, Semis, Top 10, QQQ).Return to traditional “Spot Down, Vol Up” correlation with inverted term structure.The anomalous multi-month “Spot Up, Vol Up, Crash Up” regime appears to be over for now.5. The New Structural Thesis: Hyperscalers as Potential Headwind

This is the core new point in the note:

Phase shift in the AI trade: Opportunistic longs have rotated out of first-order winners (Hyperscalers/Semis) and into bottlenecks further down the stack.Hyperscalers are increasingly acting like a “Source of Funds” rather than a perpetual bid.Equity supply shock: GOOGL’s $85B ATM offering META potentially doing the same ~$1.1T AI-linked IPO calendar in a tight window.This acts like de-facto long-dated call overwriting on the biggest stocks and threatens the 15 year post-GFC “De-Equitization” tailwind (buybacks shrinking the float).6. Market-Neutral Pod De-Grossing

Many market-neutral books were forced to be heavily long momentum to survive the 3-Sharpe rally.As the reversal hits, they are de-grossing, adding to the negative feedback loop in the narrow leadership.7. Some Dip-Buying Still Visible

Even in the pullback, there were notable upside expressions in:

DRAM / Memory (Jun12 67 calls)HYG (May 81 calls)IGV / Software (Jun 100 calls)GDX / Gold Miners (Jun26 78/84 call spread)Bottom Line for Your Book

AreaViewImplicationNear-term EquitiesTough scene for narrow AI leadershipRespect mechanical downside riskVol RegimeShifted back to “Spot Down, Vol Up”Skew re-steepening favors long skew on dipsStructural SupplyReal and growing headwindMedium-term pressure on multiplesAI Capex FundamentalsStill constructive (broadening)Medium-term bullish for the themePositioningNegative gamma is large and dangerousStay nimble; hedges are back in play

McElligott’s stance remains medium-horizon constructive on AI capex trickle-down and broadening earnings growth, but he is clearly flagging that the local mechanical supply dynamics make it much harder for indices to resume making new highs without the Mag7 doing the heavy lifting — and that support is now less reliable.

2

344

Charlie McElligott note out this morning:

Nomura Cross-Asset – “POST MORTEM, AND THE END OF THE 'SPOT UP, VOL UP' -RUN” (Charlie McElligott, ~June 6, 2026)

Overall Tone

A post-mortem on Friday’s sharp Nasdaq selloff combined with a new structural thesis. McElligott walks through exactly how the mechanical cascade played out (almost to the minute), then introduces what he sees as a potentially bigger regime shift: the end of the 20-year “shrinking equities float” tailwind due to hyperscaler equity issuance and the coming $1.1T AI IPO wave. He remains pragmatically bullish on the fundamental AI capex story but flags a volatility regime change and higher risk of sharp moves.

TL;DR – The Mechanical Cascade Structural Break

What just happened on Friday:

Started in Korea (Patient Zero = high-spec memory names like SK Hynix). Modest profit-taking turned into retail panic mechanical de-risking.

This triggered US negative gamma flows → Options delta unwind massive EOD LevETF rebalancing to sell.

Result: Nasdaq -5% by close. Asia catching down hard on Sunday night reopen (Kospi circuit breaker, Nikkei -3.5%).

The bigger structural point:

Hyperscalers are now de-facto selling long-dated calls on their own stocks via equity issuance (GOOGL already done, META coming).

Combined with ~$1.1T in upcoming AI-related IPO supply, this risks ending the post-GFC era of net equities demand > supply (buybacks shrinking the float).

This creates a potential “Supply > Demand air-pocket” that should normalize the Spot:Vol correlation and help re-steepen skew.

Key Sections Breakdown

1. The Mechanical Cascade (Exactly as Predicted)McElligott had been warning clients in Asia last week that this was a “mechanical inevitability.” The sequence played out almost perfectly:

Over-leveraged AI trade (especially Korean memory LevETFs) → modest sell-off → reflexivity → US options delta unwind → LevETF “vomit rebalancing” (~$51.6B sell-side notional on Friday, with semis and tech leading).

LevETF AUM is now heavily concentrated in Tech/Animal Spirits (86% of the $167B total).

2. The Structural Break – “Supply > Demand”This is the new big idea in the note:

Post-GFC world = Buybacks M&A > new issuance → shrinking float = powerful tailwind.

New world = Hyperscalers burning cash on capex → forced to issue equity massive AI IPO pipeline.

Hyperscalers are now effectively overwriting long-dated calls on their own stocks. This should bleed out the “Spot Up, Vol Up” regime that dominated the last two months.

3. Vol Regime Shift

Expect normalization of Spot:Vol correlation (less “crash up” behavior).

Skew should re-steepen off the recently extreme flat levels.

Traders will have quicker triggers on the way down.

4. Fundamental Bull Case Remains IntactMcElligott is careful not to turn bearish:

AI capex is broadening beyond Mag 7 into the rest of the ecosystem (INTC, DELL, HPE posting huge beats).

S&P 493 earnings growth is accelerating alongside the hyperscalers.

Real money is still underpositioned and will buy dips ahead of strong earnings quarters.

7

625

The Power Trading Room retweeted

Jun 6

Ken Griffin's ultimate rule for survival is brutally simple

when asked how Citadel survived a near-death experience in 2008 to become a $60 billion empire - he dropped pure reality:

"we lost 50% of our capital and our flagship fund was down $8 billion - that's when you realize your textbook risk models mean absolutely nothing"

"when you are bleeding $500 million a week you don't survive by having conviction - you survive by aggressively protecting cash"

"today we execute 20% of all US volume - we don't hold losers praying for a bounce, if the math breaks, we liquidate immediately"

Griffin didn't build Citadel by predicting the future. He built it by completely removing human emotion and ego from the equation when the market collapses.

bookmark and watch him break down the reality of risk

Jun 5

in a buried interview, Jamie Dimon dropped a brutal truth about wall street that almost everyone completely missed

he operates on one ruthless rule: "people confuse a bull market with their own genius. real risk management isn't predicting the crash,it's having the cash to buy out the guys who didn't prepare"

while modern traders obsess over predicting the exact market bottom, he built his massive edge by simply hoarding liquidity and letting his rivals blow themselves up on leverage. then he buys their assets for pennies

this interview is a rare reality check on true risk management

bookmark & watch a billionaire break down his system

10

64

522

481,350

We identified a 6M sweep in $MSTR 131 puts for June yesterday and many team members took them as a hedge. A dbl and counting.

1

3

2,506

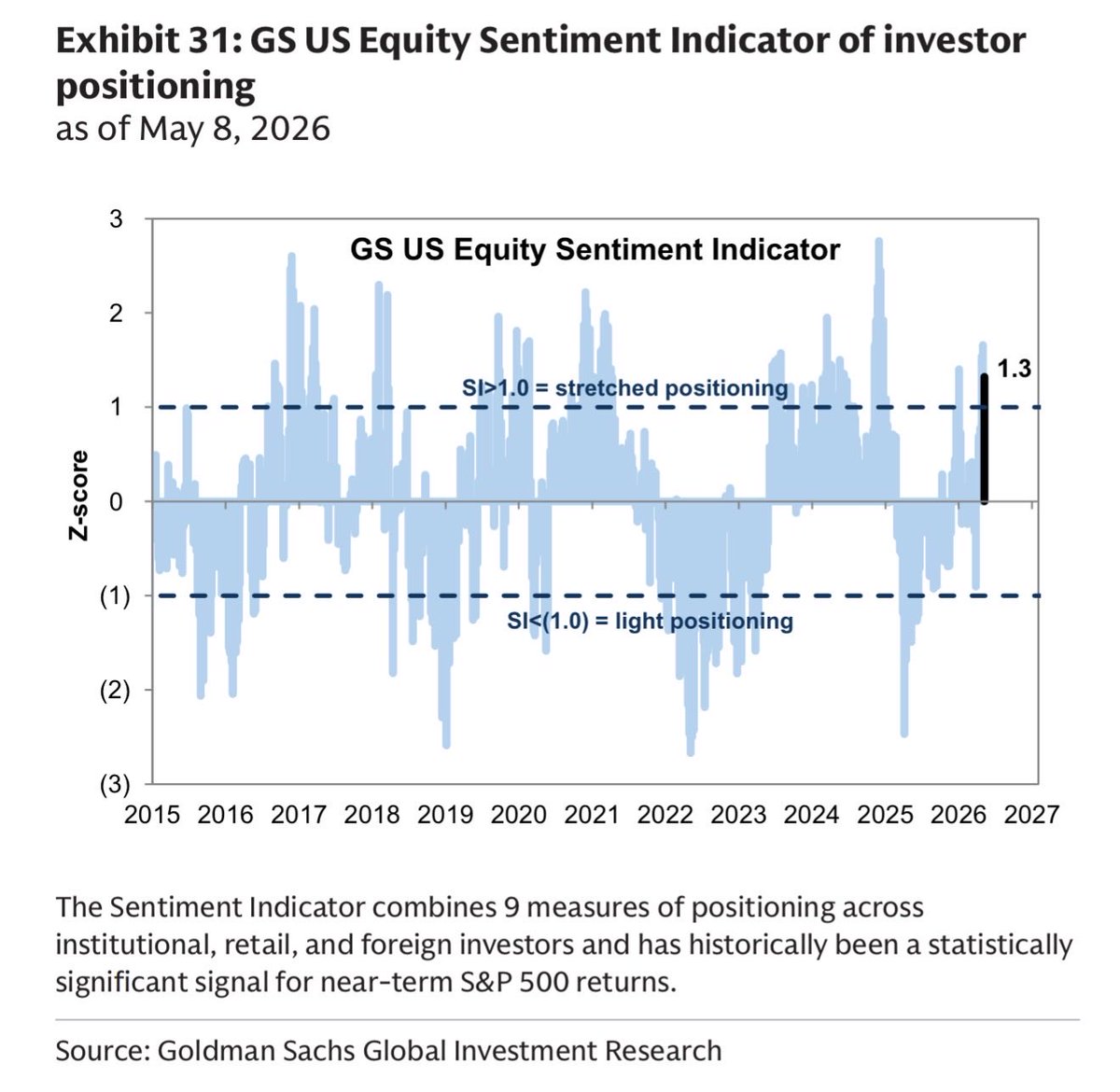

TLDR of Rubner Citadel Roadshow Insights:

• Rally fundamentally justified: No longer debated — driven by strong Q1 earnings (S&P 25.5% YoY, tech 50% YoY) robust AI/hyperscaler capex trends.

• Positioning & flows dominant: Institutions still feel underinvested and are chasing performance; CTA very long, vol-control increasing, corporate buybacks at $865B YTD (accelerating toward $1.5T annualized), retail at records (especially in semis/AI).

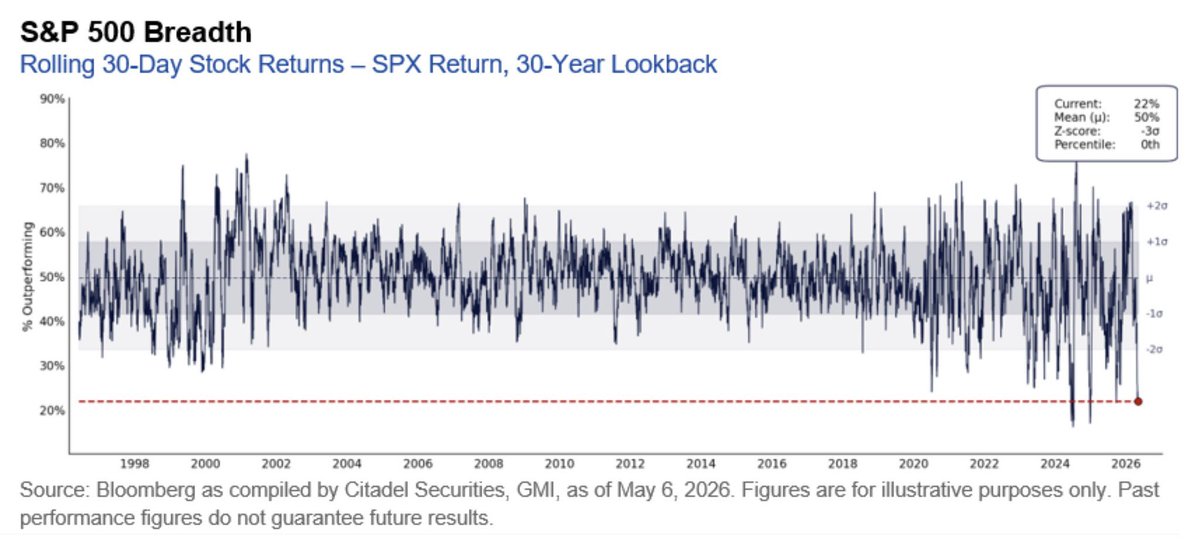

• Extreme narrow leadership: 10 stocks drove 67% of the 19% S&P rally since March 30; only 28% of S&P constituents outperforming (1st percentile); semis now ~18% of a hypothetical $1 S&P ETF allocation (record high), Mag7 ~37% (near-record).

• Market structure theme: “Spot Up, Vol Up” dynamics in AI/MegaCap Tech/semis (retail/options activity setting prices); skew flattened, downside protection cheap.

• Forward view: Nervous bullishness — pain trade is still “higher, then lower” on improving geopolitics/lower vol/mega-cap leadership, but fragility increasing. Debate intensifying on broadening/rotation to laggards (cyclicals, small caps, value) if rates/geopolitics cooperate.

1

4

279

$LLY Llnt term entry of 850 given days before it hit 850…Now go look at chart and prices after. Nice work HY6

3

319

$ARM swing calls up 1300% great work Dersh!

Been rding this one for a while now.....elephant hunting

4

249

OPENAI PREPARING TO FILE FOR IPO VERY SOON, SOURCES SAY: WSJ

1

2

276

RT @InvestingCanons: Stanley Druckenmiller:

“Life goes in streaks. And like a hitter in baseball, sometimes a money manager is seeing the…

146

Taking new members for Monday open.

DM us if interested.

14

23,554

May 15

David Tepper's Appaloosa just filed its latest 13F.

Here are the updated holdings.

1

795

Were you prepared for today? We were.

Member testimonial making us happy to hear folks being unbiased and preparing for possible downside today. Cheers to you this weekend 🍷

2

324

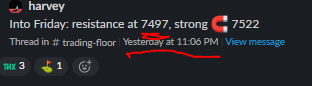

🧲7497 level $SPX given yesterday and here we are.

Kudos to @realharveymark, pretty good that guy

1

3

366

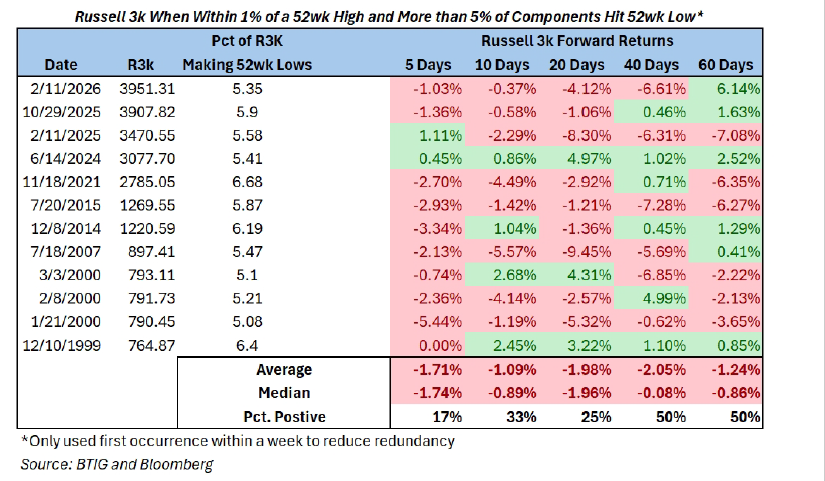

Russel 3000 performance when within1% of 52W high and more than 5% of components hit 52W low:

credit: BTIG

2

3,350

2

313

dump day called this AM, warnings given yday to get defensive

3

271