Passionately psycho about understanding business models

Joined July 2021

- Tweets 1,355

- Following 85

- Followers 393

- Likes 249

756 Photos and videos

Feb 26

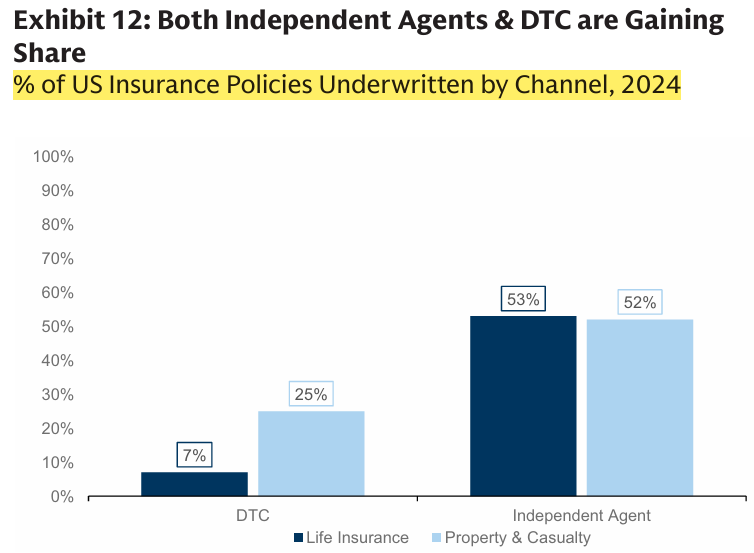

Hello @CedarStResearch , are there any listed players in life insurance which are riding this wave of independent agents/MGAs?

1

218

Jan 16

1

1

697

9 Dec 2025

If common shares of $OPITQ are going to be cancelled at the end of the bankruptcy process, why are they still trade on pink sheets and have some value? The NPV of zero is zero.

Is there a scenario where there could be some equity in the new entity for current shareholders?

116

5 Dec 2025

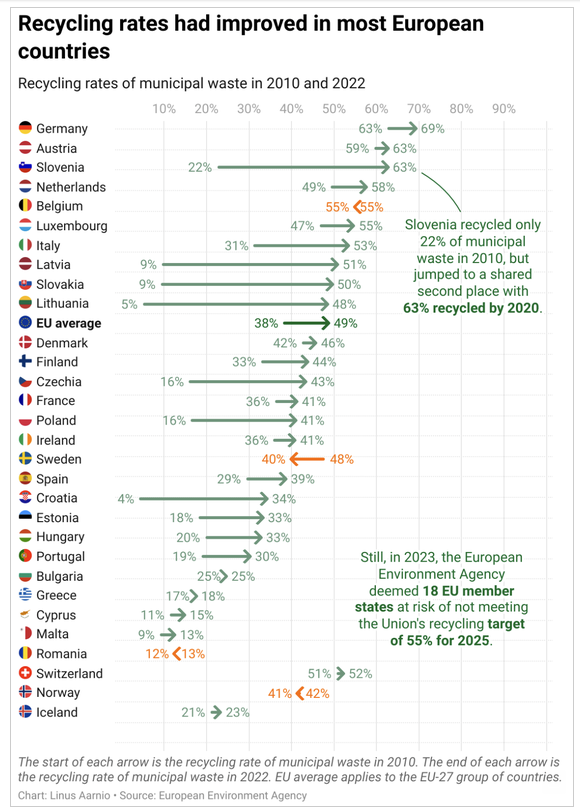

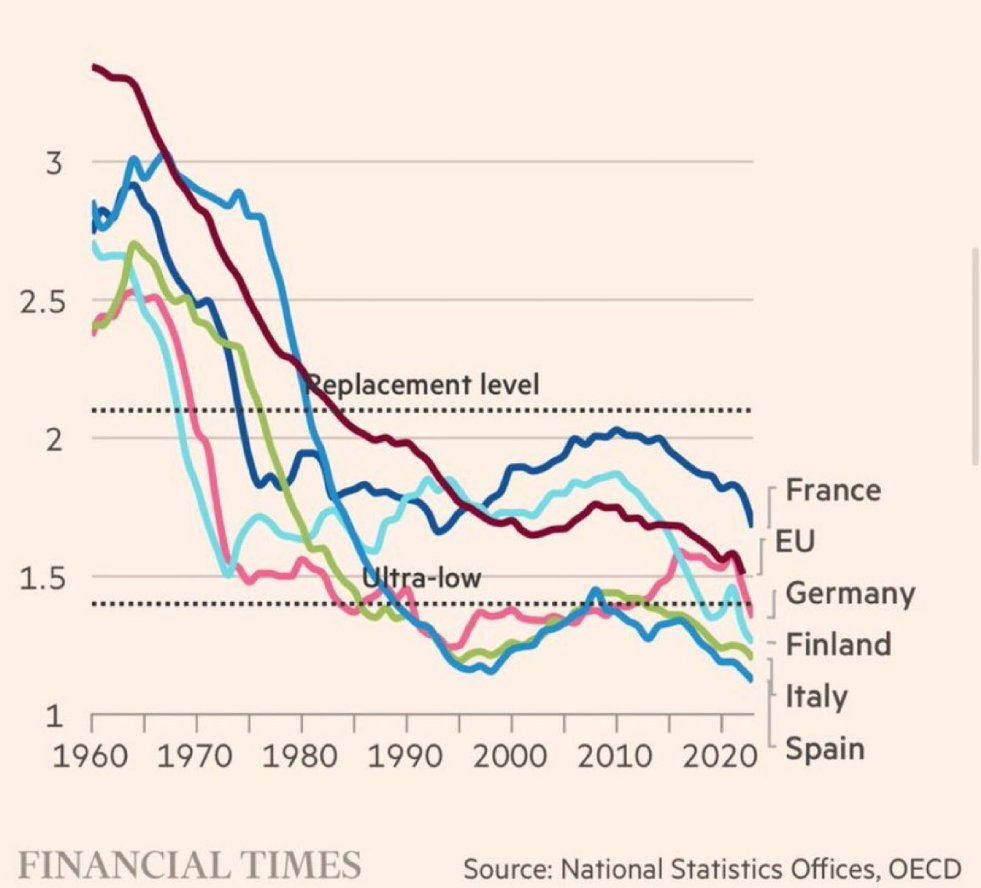

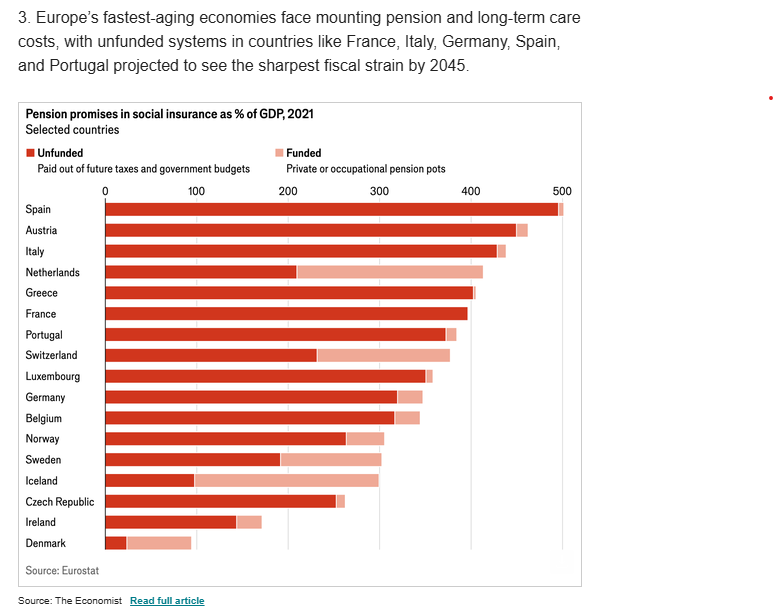

Who is going to honor these promises where the birth rates are falling? Immigrants?

1

81

4 Dec 2025

"Trick of the trade in insurance is how do I originate premium, retain as much of it as I can and cede all the difficult risk back out to the reinsurance market so I can transfer all my earnings volatility to reinsurers."

Pure gold from @CedarStResearch

1

115

21 Nov 2025

20 Nov 2025

@grok, list the companies leading, who are first movers, or who have an advantage in the area described above, regarding recovering more than 15% of the shale oil in place. Symbols and prices.

1

2

381

14 Nov 2025

At WTI $150, an E&P company operating in Permian Basin may not able to pump oil out of the ground despite having the capital, plant, people, oil gathering pipeline if they don't have a way to dispose off the Produced Water(PW).

PW is THE limiting factor, NOT the oil price. $WBI

2

3

14

2,819

14 Nov 2025

“We wanted to be able to take our story out, educate the market and show how this is really a superior asset to what exists today and show how it has tremendous long-term growth with great barriers to entry,”

$WBI

1

1

1

321

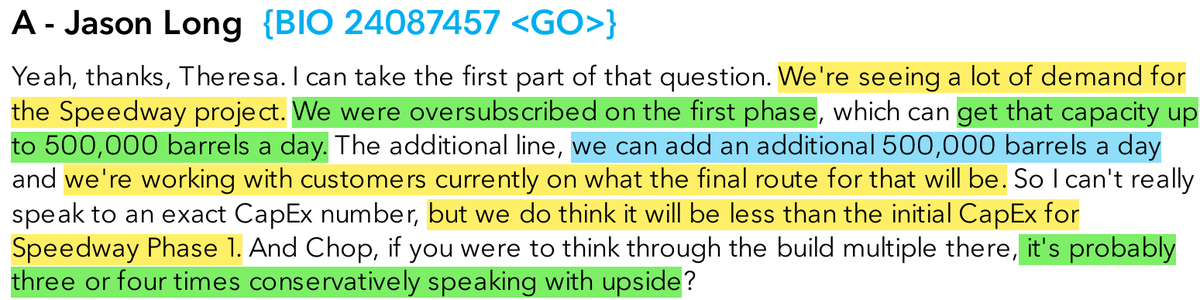

14 Nov 2025

On future CapEx and ROI, he said:

“So you're talking about $700 million or $800 million of capital, and we would do that at a really attractive return level (of around 30%)"

Management mentioned similar return in Q3'25 earning call. $WBI

Source: bizjournals.com/houston/news…

2

3

1,588

13 Mar 2025

Here you go. $TTD tried to connect advertisers directly with publishers and as a result being criticized by industry for conflict of interest it is preaching to avoid for so long.

x.com/kouroshshafi/status/18…

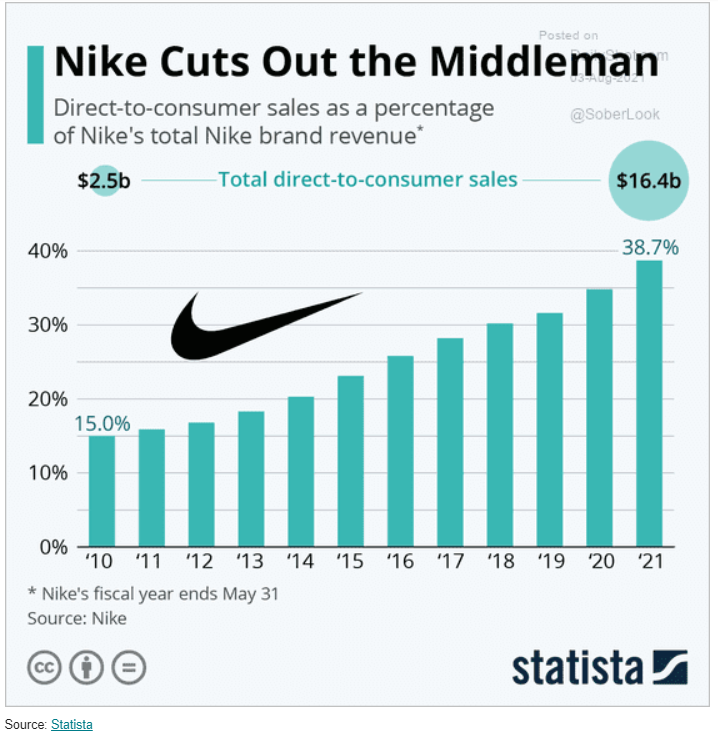

3 Aug 2021

Capitalism improves distribution by eliminating the middlemen. GEICO did it. Nike has done it.

AdTech won't be different $TRMR

1

491

7 Jan 2024

Retailers could suffer ‘perfect storm’ of Red Sea and Panama Canal disruption, says logistics expert - MarketWatch

$PLCE $CRI marketwatch.com/story/retail…

295

18 Sep 2023

1

1

558

18 Sep 2023

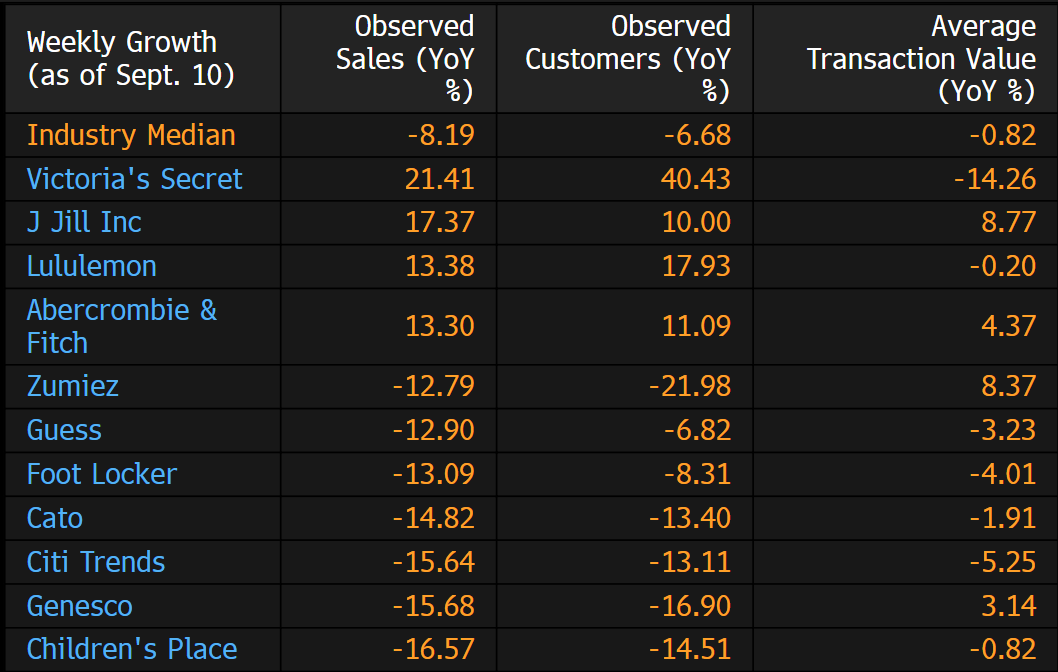

r = 63.91% which shows high predicting power using the weekly sales data to predict reported revenue. $PLCE

253