Hi! This is a hate-free zone, where I research Memory, Semis, Power, Robots, Space, data centers, and aligned areas.

Joined March 2009

- Tweets 8,622

- Following 7,188

- Followers 1,538

- Likes 132,571

44 Photos and videos

Nice Serenity analysis

Jun 14

基于本周周报提炼:

这周 @aleabitoreddit(Serenity)粉丝破 70 万。跟她票的人多,看懂她「脑子」的人少。我把她本周所有公开帖扒完,提炼出八条核心思想:

先定调:用一手产业信息+供应链推导,在机构进场前埋伏「不可绕过」的瓶颈小票,然后扛波动、等前瞻营收兑现。

1️⃣ 卡脖子优先:市场定价前,顺供应链找结构性瓶颈。本周几乎每条线都是它:$SIVE(CPO 激光)、$AXTI(InP)、$IQE(外延片)、$SOI(衬底)、WF₆→后成 093370、绿的谐波 688017(人形减速器)。瓶颈=定价权+不可替代。

2️⃣ 看前瞻营收,不看当下财报。她盯 2027-2029 放量拐点,不是今天的 EPS 和烧钱。$XFAB 被当「萎靡车规股」就因为欧洲只看 TTM;$SIVE 现 <$2B,看的是 Celestial 2028/2029 营收曲线。「CPO 标的不该用 1 个月去判断。」

3️⃣ 资金博弈是她最强的叙事引擎:散户早于机构卡位 → 分析师唱衰洗盘 → 机构吸筹 → 新高。本周 JPM 把 $SIVE 从 0.4% 加到 5.25%、Fidelity 主动建仓、BlackRock 被动纳入,正是这个剧本。$NBIS、$RKLB 是她反复引用的模板。「机构不是你的朋友。」

4️⃣ 资本结构/流通盘=第一过滤器。$IREN(无限稀释)≠ $NBIS(NVDA 直投、结构干净)≠ $CRWV(高息债)。关键:不是所有稀释都坏,看钱去建产能还是填窟窿。

5️⃣ 信一手产业口径,不信二手分析师。CPO/800V「延期」砸盘,她站英伟达网络 SVP、Lumentum、富士康、大摩,不信「连 $MU HBM4 都搞错的分析师」。龙头比分析师更清楚自己的时间表。

6️⃣ 地缘就是供应链战争。出口管制互掐(中国 InP/钨、日本 WF₆)本身在制造瓶颈。她点破一个错误交易:做空在重建的西方公司、做多有补贴的亚洲股,会反噬;反过来押被补贴、回流的西方关键环节($AAOI、$IQE、$SOI)。

7️⃣ 不对称押注:埋伏小市值瓶颈,赌赢家凸性不赌胜率。她的仓清一色小市值($AXTI、$IQE、$LPK、$ALRIB…):「$AAOI 当年 $3B 干到 $14B,那同区间的 $SIVE 凭什么不行。」纪律:除非基本面实质变化否则不平多仓,拥抱波动等拐点。

8️⃣ 钱从市场赚,不从粉丝赚。不接广告、只 $1 订阅、内容全免费。这不是道德表演:利益对齐 → 可信 → 散户跟随 → 自我实现的资金流。

统领这一切的方法论:独立推导、映射非结构化关系。$LPK 从 SpaceX 进口记录里挖出来;$SIVE→$POET→$MRVL→hyperscaler 的 OSINT 映射;$RPI 从「朋友都在买 Mac Mini/RPI 跑 AI」反推。她管这叫「在正常重定价的几个月前去猜」。

39

Jun 13

Good news Texas!

There you go. The United States is built on a limitless ethos of entrepreneurship, innovation, and excellence. Canada is built on feminized and "empathetic" parasitic taxation fuelled by envy and resentment toward those who produce.

51

Jun 13

We are out of time

“We’re raising alarm bells right now,”

- American Petroleum Institute CEO Mike Sommers

“…The oil market can’t run down to the last drop, like your car can.

Below a certain threshold, pipelines can’t maintain pressure and refineries can’t deliver all the various fuel grades their customers demand….

..Once you get to that point, then you’ll see prices shoot up,..”

1

77

Jim P., down in Texas retweeted

Jun 13

$KEEL has one of the best setups right now in the neocloud space.

The CEO is targeting one lease at each site by year-end at Panther Creek, Sharon, and Moses Lake sites.

People are speculating $AMZN could be a tenant.

Jun 13

$KEEL has a realistic path to a 10x, and it is simpler than people think. It all comes down to leasing the power they already control.

Here is the math that gets you there.

KEEL controls a 2.2 gigawatt pipeline across Pennsylvania, Washington, and Quebec, with grid interconnections already in place.

That power is the entire asset. The whole business model is turning secured megawatts into signed leases that throw off long term recurring revenue.

Start with what a lease is actually worth. AI data center colocation runs roughly $150 to $200 per kilowatt per month. Take the three leases the CEO has committed to signing by year end. Panther Creek at 350MW, Sharon at 110MW, and Moses Lake at 18MW.

That is roughly 478MW of near term capacity. Leased out, that alone is somewhere in the range of $850 million to $1.1 billion in annual recurring revenue. On a company with a current market cap a fraction of that.

Now extend it to the full pipeline. 2.2 gigawatts fully leased at those same rates is north of $4 billion in annual recurring revenue. Data center operators with contracted hyperscaler revenue trade at 6 to 7 times sales.

Put a conservative multiple on $4 billion in recurring revenue and you land around a $30 billion company. From where this trades today, that is the 10x.

And here is why the path is simple, not complicated. KEEL does not need to invent anything.

They do not need a new product. They do not need to win a technology race. They already own the power. They already have the interconnections.

They just need to sign the leases, and the CEO has told the market the priority for this year is signing three of them.

Every lease that gets signed converts speculative power into contracted cash flow and re rates the entire pipeline behind it.

We saw $DGXX do exactly this with Cerebras. The first signed hyperscaler lease changes the whole story overnight.

Secured power. Grid connections in place. Three leases targeted this year. A 2.2 gigawatt pipeline behind it.

The path to a $30 billion company runs straight through those signatures. And they are coming.

8

42

4,305

Jun 13

Wow! Great post by Ms. MBA.

🚨Everyone is still buying the chips. The bottleneck already moved.

A GPU that computes in nanoseconds and waits microseconds for data is a stranded asset. At 1.6T speeds, copper runs out of physics. The constraint on AI is no longer how fast you can think. It's how fast you can move what you thought.

Jensen has now said it twice in three months.

At GTC in March: "Is copper going to still be important? The answer is yes... Are you going to scale up optical? Yes. Are you going to scale out optical? Yes... We need a lot more capacity for copper. We need a lot more capacity for optics. We need a lot more capacity for CPO."

Last week at Computex, on Marvell's stage: "Optics where you must, copper where you can." Then he called Marvell the next trillion-dollar company and the optical complex repriced within days. The same keynote put a date on the handoff: 200G per lane is the last generation where copper is sufficient. After that, optics takes the rack.

Translation: not copper OR light. Copper now, light next, unprecedented amounts of both. 🔥

The chain is unavoidable: AI tokens are profitable → more GPUs → more bandwidth → copper hits its wall → photonics becomes the chokepoint.

And the smart money stopped debating. Follow the closed deals:

→ $NVDA has committed at least $6.5B to photonics in three months: $2B into Lumentum, $2B into Coherent, a $500M stake in Corning, and a piece of Ayar Labs' $500M round. Direct investments to secure its own light supply.

→ $MRVL paid $3.25B for Celestial AI, up to $5.5B with milestones, to build what its CEO calls a silicon photonics powerhouse.

→ $CRDO closed DustPhotonics two weeks ago. Ciena bought CPO startup Nubis for $270M.

North of $10B of strategic capital locked up one supply chain in under a year. Capital like that doesn't chase a theme. It secures a bottleneck.

LAYER 1: WAFER. Every laser starts as a crystal.

🟠 $AXTI: the InP substrate leader. The first chokepoint in the stack.

🟡 $IQE: compound-semi epiwafers feeding the laser makers. Speculative, but structurally upstream.

LAYER 2: LIGHT. Photons don't make themselves.

🟠 $LITE: revenue 90% YoY last quarter to $808M. EML shipments doubled and management says demand still exceeds supply across EMLs, pump lasers, and transceivers. NVIDIA just wired them $2B. OCS backlog past $400M plus a multi-hundred-million CPO order for 2027.

🟢 $SIVEF (Stockholm: SIVE): the external light source. CPO does not emit its own light. Every optical engine needs a continuous-wave InP laser feeding it, and that is the layer you cannot engineer around. ELS modules with POET hit production readiness end of this year. Disclosure: long.

🟣 $POET: the optical engine wildcard. Its Optical Interposer pairs with Sivers' lasers on external light sources for CPO, with a LITEON module deal stacked on top. Binary commercialization, real architecture.

LAYER 3: OPTICS AND MODULES. Where light meets the rack.

🟠 $COHR: the volume anchor in transceivers, holding NVIDIA's other $2B check.

🔵 $AAOI: Q1 revenue 51% to a record $151M, datacenter revenue more than doubled, $124M of 800G orders plus a $200M 1.6T order in hand. Scaling Texas capacity toward 500K units a month by year-end, targeting $1B revenue this year. Domestic supply while everyone fights over offshore. Disclosure: long.

🟠 $FN: the foundry of optics. When Fabrinet is building, the orders already exist.

THE INTERCONNECT: the layer the rack cannot route around.

🔵 $CRDO: just closed DustPhotonics. SerDes → DSP → silicon photonics → system integration, one company, 800G through 3.2T. Electrical AND optical, end to end. FY26 revenue tripled to $1.34B at 68% gross margin. The toll booth on both roads. Disclosure: long.

🟠 $MRVL: $3.25B for Celestial AI, and Jensen's trillion-dollar nod on the Computex stage.

🟠 $AVGO: switch silicon, optical DSPs, CPO engines. They define the socket.

🟠 $ANET: the AI spine. 100K-GPU clusters get stitched together in light.

LAYER 4: PACKAGING, FIBER, FOUNDRY. Where photons get industrialized.

🔵 $TSEM: the neutral silicon photonics foundry. Prints wafers for whoever wins.

🟣 $LPKF: glass-substrate packaging for glass-based CPO. Real technology, binary commercialization.

🟠 $GLW: AI racks demand several times the fiber density of legacy cloud, and NVIDIA just took a $500M stake. Corning sells density.

LAYER 5: TEST AND THE ANALOG UNDERLAYER. Complexity is a tax paid in validation.

🔵 $AEHR: silicon photonics test, ramping with the cycle. '

🔵 $VIAV: every 800G and 1.6T transceiver gets validated before it ships. The gate the market prices like an accessory.

🔵 $SMTC: the drivers and TIAs that fire the lasers. Sits directly under the LPO trade.

🔵 $MTSI: the high-speed analog behind 1.6T engines.

🟠 $CIEN: transport. Even long-haul is buying light.

💡The counter-thesis, because every map needs one. The honest debate on this stack is whether these are genuine bottleneck assets or cyclical optics suppliers enjoying peak demand at peak multiples. Lumentum's May print showed 90% growth with the stock up roughly 1,400% over the prior year at a triple-digit trailing multiple. That is a price for perfection. Most of these names live or die on a handful of hyperscaler capex lines, and one digestion quarter hits the whole stack at once. CPO timing has already slipped once. Architecture risk is real: LPO, CPO, and stretched copper are still fighting for the same sockets. The cycle is real. So is the gravity. 🔥

But the bears have to explain one thing: $NVDA, $MRVL, $CRDO, and $CIEN just spent over $10B securing this supply chain with their own balance sheets. The people with the best information are paying up for the layers.

The market owns the top of this stack. The asymmetry is at the edges: wafer, light, packaging, test.

Own the layers, not the logo.

Bookmark this for the weekend. Then tag the one investor you know who's still all compute and no interconnect. 👀

1

2

276

Jun 13

Great visual. Thank you EI.

Jun 13

Low PEG ratio can signal the rare combination of strong earnings growth and reasonable valuation, making these stocks worth watching as potential leaders in the next market uptrend.

$MU $LITE $HPE $STX $MXL $DELL $BE $SIMO $CLS $AMD $CRDO $TSM $AAON $VIAV $SANM $TER $STRL

This list highlights companies where expected EPS growth is outpacing current valuation multiples, with PEG ratios below 1.

33

Jim P., down in Texas retweeted

Jun 13

$AAOI bears… I think hedge funds know more than you. 🤷🏻♂️

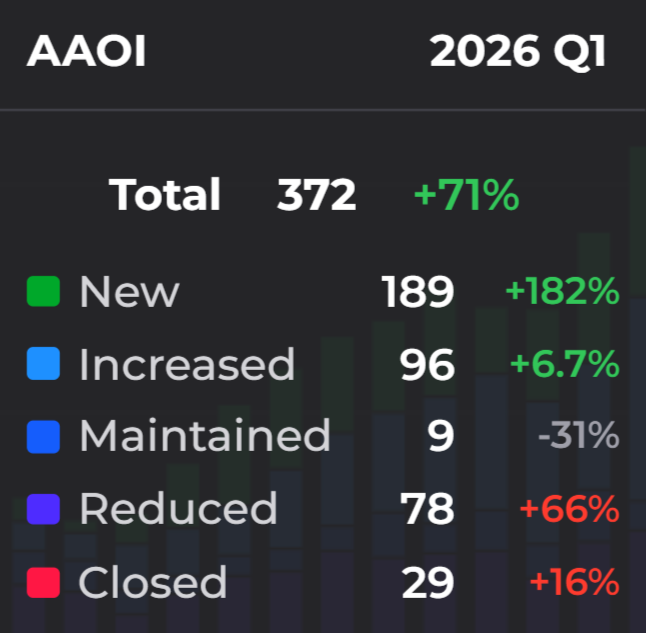

Or do you think you know more? 😂

Jun 10

OMG! 😮 I didn't know this on $AAOI Q1 2026...

182% NEW positions from hedge funds and large institutions.

Can't believe it went off my radar. And you are bearish anon?

10

4

116

24,412

Jun 12

Does anyone know about $APRTEC. Datacenter cooling company. May have a technology advantage. Thanks Johan!

Jun 12

$APRTEC is a Swedish thermal management company validated in space by NASA and ESA, with a global tech customer integrating its EHD technology into chip-level product development.

Every watt of AI compute becomes heat. In 3D-packaged chips that heat is trapped inside the package, and rack-level cooling cannot reach it. The solution requires a pump small enough to operate at microchannel scale with no moving parts. Mechanical pumps have a physical lower bound on miniaturization. Electrohydrodynamic conduction pumps do not.

APR has spent 15 years developing EHD micropumps for highly demanding thermal environments, including spacecraft qualified by ESA and NASA. Space qualification imposes reliability requirements that are among the most demanding in any industry and are generally more stringent than those found in commercial data center environments. An unnamed global tech company has now integrated APR’s EHD pump into its product development and placed a pilot production order. That moves the relationship beyond pure evaluation.

The confirmatory event is a volume order from the tech customer. It would move APR from a component in a competitive cooling layer to a potential node in near-chip thermal management.

Risks:

•The tech customer remains unnamed and the volume decision is not yet taken. The relationship could stall.

•APR’s space and defense channel runs through ZIHET, which controls production, distribution and customer relationships. The economics accruing to APR remain uncertain.

•Core EHD conduction pumping is prior art from 2003. Patent protection covers specific implementations, not the principle. A well-funded competitor could develop an alternative path.

Position:

Long, small and a volume order from the tech customer would materially change the size of this position.

4

1

4

542

Jun 11

I am watching a pre-IPO behind-the-meter candidate, which Claude found for me. I wanted to share it with you. $NSCALE

1

2

128

Jun 11

@ChairmansLedger -- Claude sent me this one. It is close in position to another stock I am watching, INIO. I like the behind-the-meter plays. You may want to look at either.

43

Jun 11

Leo appears to be copying me again!

Jun 11

33

Jun 11

Wow

Jun 11

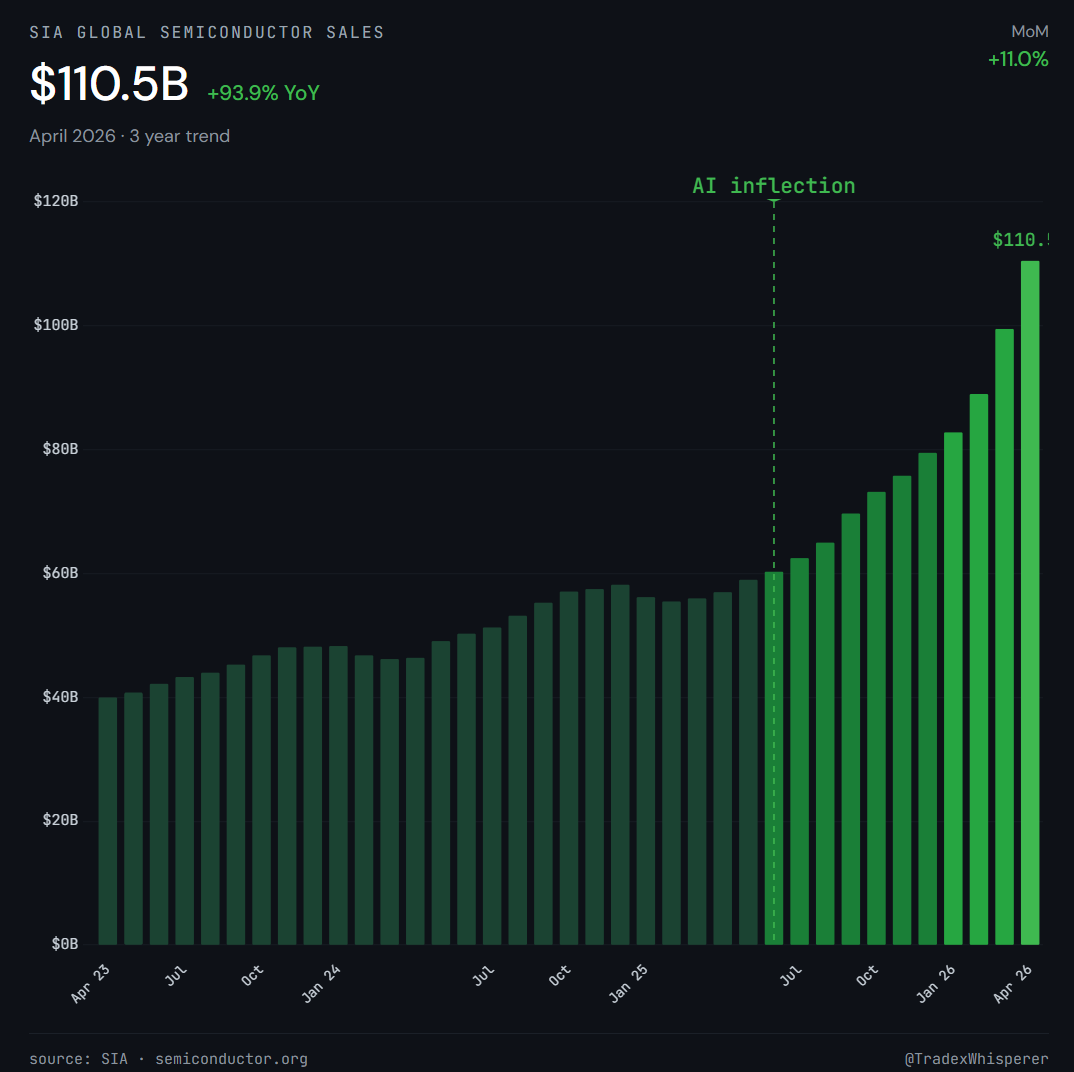

Monthly Semiconductor Sales.

April just hit $110.5 billion in a single month.

Annualized, that is $1.3 trillion.

The $1 trillion milestone was penciled in for 2030🤯

AI doesn't give a fuck about some retard's put positions, war & oil. It waits for nothing.

2

46

Jun 11

It is good to laugh

Jun 10

$AAOI ruined me.

A few months ago, this company did so well.

The stock was going up. It was a dream.

In the last 4-5 days, it became a dumpster fire.

- Everything is going down.

- Bankruptcy could be near.

- Do they even sell products?

- Their business could be dead.

- They're probably going under $100 soon.

It's incredible how business can be exception one week, and a dumpster fire just one week after.

Sell everything, now!

You can help me pay my rent here:

Gofund me / thebigberbowskiisruined

Thank you.

1

33

Jun 10

Great news for post-war buys

Jun 10

OMG! 😮 I didn't know this on $AAOI Q1 2026...

182% NEW positions from hedge funds and large institutions.

Can't believe it went off my radar. And you are bearish anon?

25

Jim P., down in Texas retweeted

I’m seeing a lot of red pre-market again.

This has me very concerned.

It must mean war, inflation, bond yields and the yen carry trade have put all my companies on the verge of bankruptcy.

Prices are down so that is proof that I’m right.

I’m going to panic sell everything now and perfectly buy back in right at the bottom, which emotionally is the most rational thing to do.

It’s always a good idea to act on your emotions.

27

4

215

20,421

Jim P., down in Texas retweeted

Jun 9

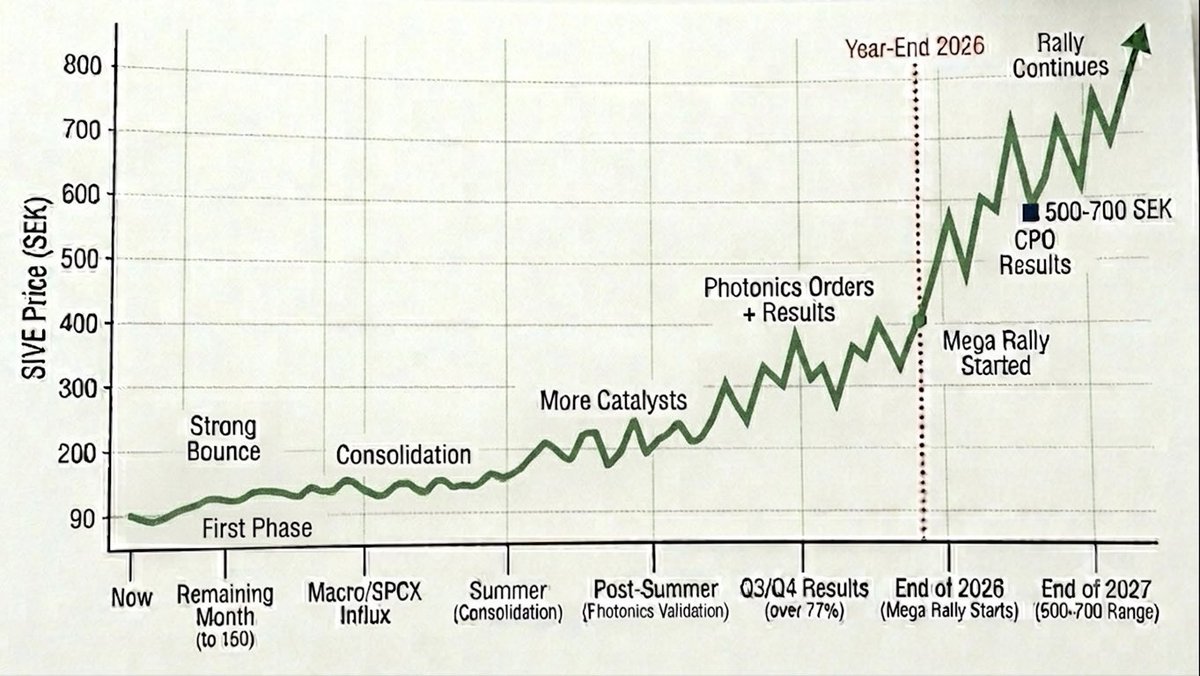

Let me speculate a bit on $SIVE

Based on my own assumptions, I’m going to map out a timeline for $SIVE

We are seeing upcoming catalysts and growing expectations:

- Ayar Labs integrating into the $NVDA ecosystem

- Partnership with $GFS

- Dual listing on the Nasdaq

But recently, we've also been seeing actual order confirmations

Even if these aren't in the photonics segment, they are hitting their other business units

This cleans up their financials and gives them the breathing room to smoothly develop the photonics and CPO branch

What I expect next:

Short-term: I see a strong rally through the rest of the month up to 150 SEK

Driven by a shift in macro market sentiment and capital inflows returning after the migration to $SPCX

Consolidation: After that, I expect a consolidation phase in the 150 SEK range, similar to what we are seeing right now

Summer Catalysts: More catalysts will keep rolling in throughout the summer, moving the price into the 200-250 SEK range

Post-Summer & Looking into 2027:

After the summer, I firmly believe the first orders from the photonics branch will start coming in

Nothing crazy, but they will serve as massive validation, alongside the upcoming quarterly results

For those quarters, I expect growth to surpass the 77% surge we saw in Q1

This should move us into the 300-400 SEK range

As we approach the end of 2026, we'll be right on the doorstep of CPO starting to show tangible results by early 2027

Larger photonics orders will kick in, and the second mega rally for $SIVE will begin

I foresee more catalysts dropping

While institutional investors finish locking down a massive piece of the pie

I see $SIVE wrapping up the year in the 500-700 SEK range

From there, the rally will continue into numbers I won't even try to guess

This timeline is based on recent developments, the company's execution, and price action

It is pure speculation on my part, but keeping it realistic

If the current catalysts start solidifying

Ultra bullish on $SIVE

22

21

256

35,168

Nice map

Jun 9

Most people think the AI buildout is just a couple of stocks – Memory, CPU, GPU, NeoClouds, Photonics..

$SNDK, $MU, $ARM $INTC, $AMD, $NBIS, $LITE, $AAOI, $TSEM, $SIVE

The reality is there’s so much more to it.. I built a complete map of the AI buildout – at least the one I’ve been trading around for the last year.. I put that map on my Substack… 12 layers deep.

Since I’ve seen it circulating on here, I’ll just post it myself.

The hard part isn’t knowing the full stack – it’s making sense of it.

Why is photonics down today but memory isn’t? Why is CPO so relevant in the AI buildout?

Bullish AF on AI infrastructure.

Go check out the full article for free on my Substack, and if you’re going to share it – please do, but link back to my article.

Here is the link: open.substack.com/pub/rensub…

Let’s go find the next 1000% stock ⚡️⚡️

35

Great company

Jun 9

$ASML is now the first public company in European history to be valued at more than $700 Billion

3

36

Spac = IPFX

Jun 9

.@QuantumSpace_US announced its intention to go public via SPAC. The move to take the in-space mobility company public is driven by the company’s desire to move quickly to meet the military’s needs in orbit.

payloadspace.com/quantum-spa…

50