QuantEcon is a @NumFOCUS fiscally sponsored project dedicated to developing open source computational tools for economics. Supported by the @SloanFoundation.

Joined September 2015

- Tweets 364

- Following 421

- Followers 7,288

- Likes 4,937

51 Photos and videos

Pinned Tweet

Mar 21

Pure, beautiful abstract Dynamic Programming theory❣️❣️❣️

#DynamicProgramming #EconomicTheory #QuantEcon #EconTwitter

Tom and I have finally finished a draft of Dynamic Programming Vol 2! Exhausting but satisfying. New approach to DP theory, advanced material, many applications... dp.quantecon.org/

17

103

9,723

May 14

Definitely should not miss this❣️❣️❣️

May 13

Thrilled to share a project I've been refining: a complete, open-source repository on "Deep Learning for Solving and Estimating Dynamic Models in Economics and Finance."

I've cleaned up the materials from my PhD classes and summer schools into one coherent resource. 🧵 1/6

3

29

3,255

May 1

Exciting to see our co-founder @john_stachurski leading a fantastic workshop on Advanced Computational Method at @CarnegieMellon ❣️❣️❣️

See more here:

github.com/QuantEcon/cmu_202…

#Python #GoogleJAX #EconTwitter

6

58

4,111

Mar 28

Beautiful and deeply deserved.

Truly grateful for your guidance and the opportunity to work with you❣️❣️❣️

I know we shouldn't be driven by desire for accolades but I am proud of this one. Maybe I didn't entirely waste my short moment of time on this beautiful planet 🥹❤️ comp-econ.com/contest-and-pr… @SocCompEcon

7

56

4,942

Mar 27

Dynamic Programming II just got its final chapter - - -

Approximation reinforcement learning — free forever ❣️❣️❣️

#DynamicProgramming #QuantEcon #OpenSource #EconTwitter

We added a new and final chapter to Dynamic Programming Vol II (DP2) on approximation and reinforcement learning: dp.quantecon.org/. DP1 and DP2 will always remain freely available online -- give me liberty or give me death 🤟💀

7

64

5,424

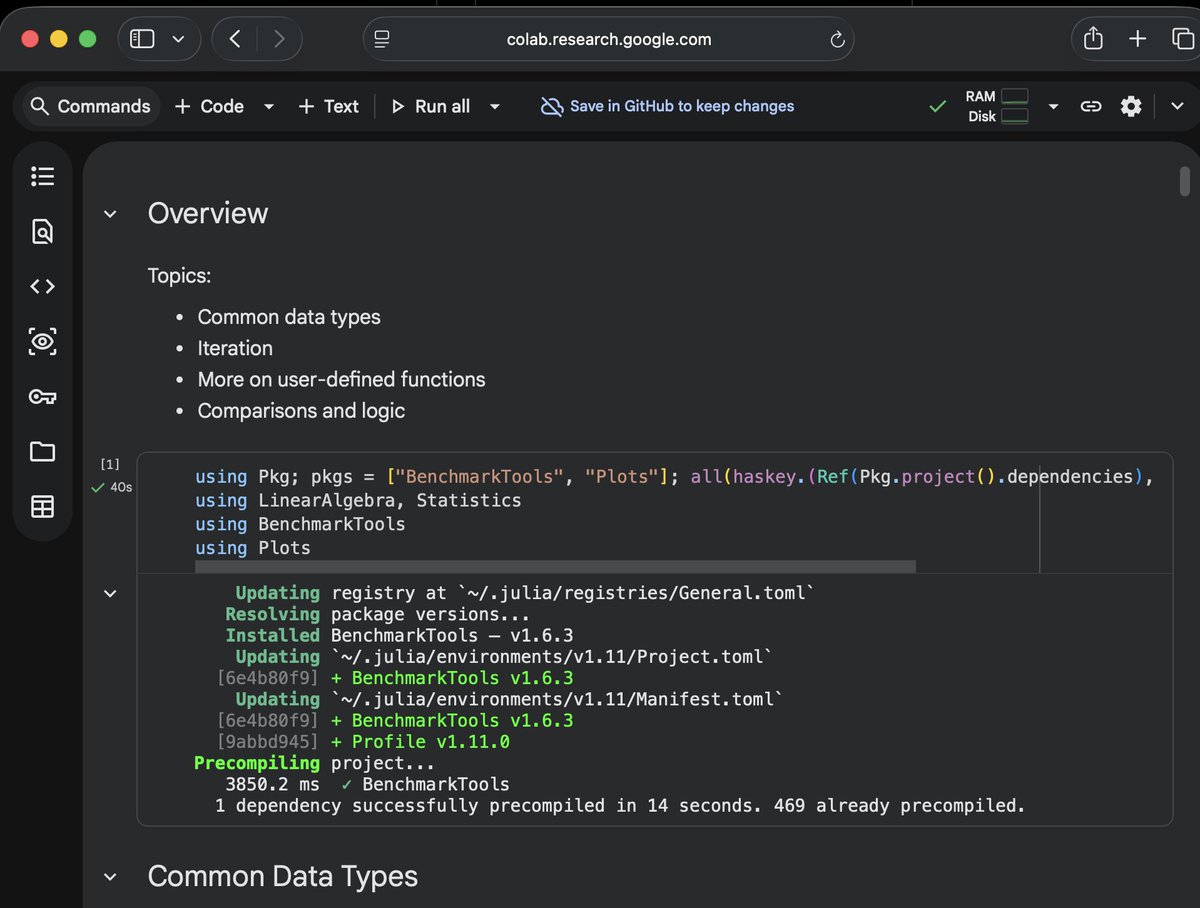

Feb 25

QuantEcon lectures can now be launched straight into Google Colab—no local setup needed🎉🎉🎉

Thanks @jlperla for making this even more accessible❣️❣️❣️

#JuliaLang #QuantEcon #OpenSource #ComputationalEconomics #EconTeaching #JuliaNotebooks #GoogleColab #Economics #DataScience

Feb 24

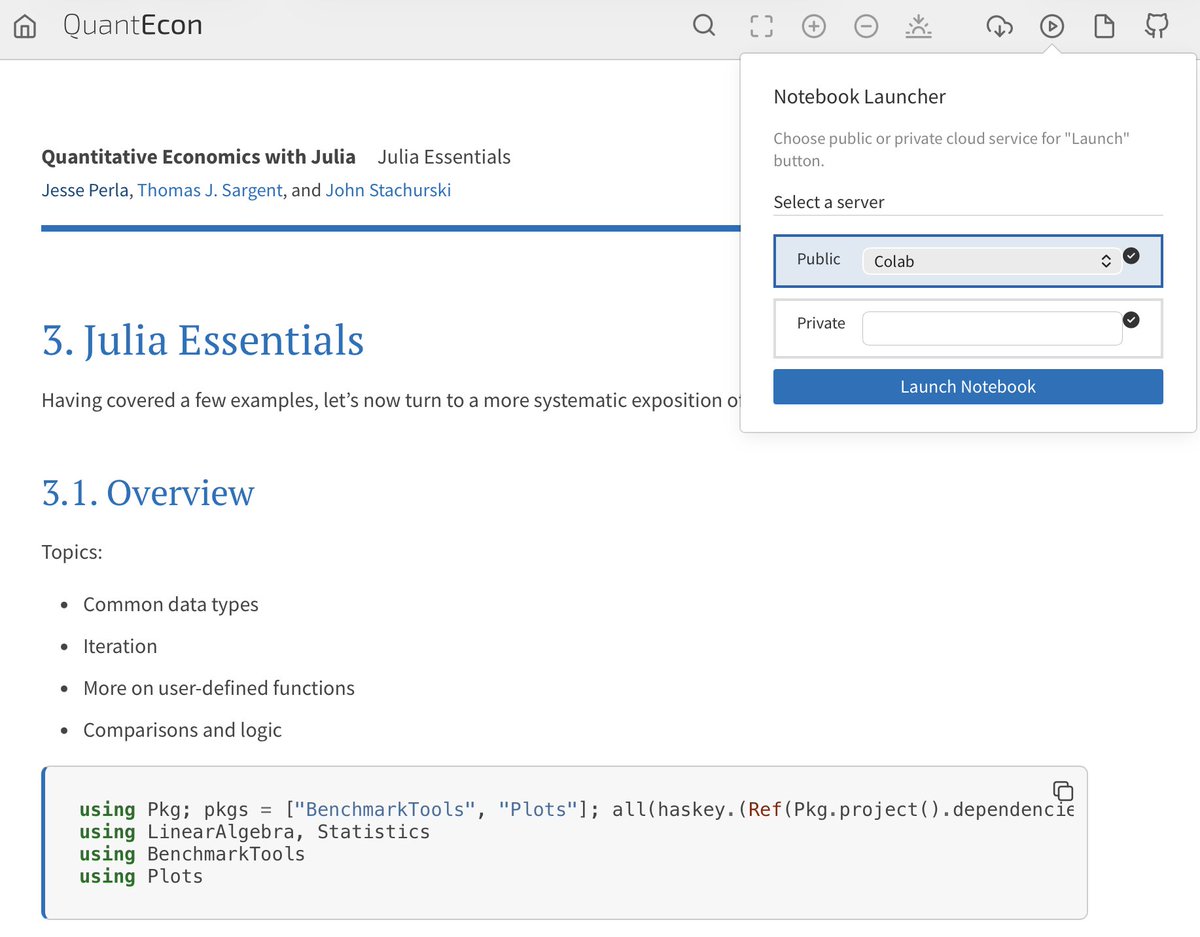

In the latest @QuantEcon Julia release, you can now launch notebooks directly in @GoogleColab.

Just click ▶️ on the online lecture to open it in Colab.

On first run, the notebook automatically installs all required packages.

16

61

5,792

Feb 20

A big new release for Quantitative Economics with Julia 🎉 🎉 🎉

Thanks @jlperla for the overview — lots of improvements ❣️❣️❣️

#QuantEcon #JuliaLang #ComputationalEconomics #OpenSource

1

23

115

12,367

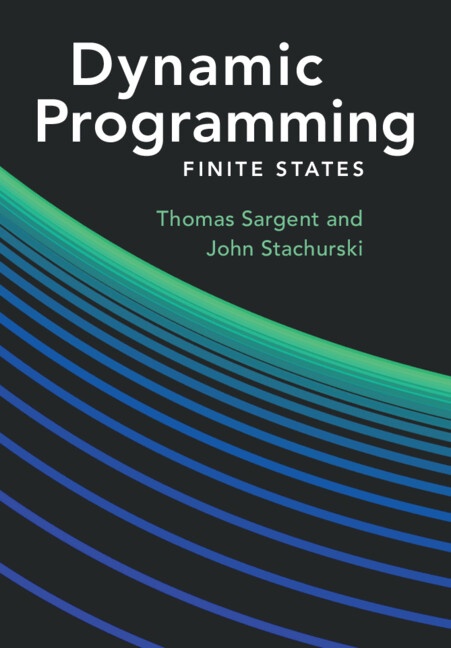

29 Nov 2025

Super happy to see Dynamic Programming by Sargent & Stachurski out in the world — rigorous, elegant, and full of applications. A beautiful piece of work❣️❣️❣️

1 Oct 2025

Dynamic Programming by Thomas J Sargent and John Stachurski

Provides a rigorous and unified presentation of recent advances in dynamic programming, along with code, algorithms, and many applications.

📚 cup.org/452So7L

2

70

390

51,271

29 Nov 2025

11 Nov 2025

From hours to seconds 🤯. An economist from @QuantEcon tells the story of how JAX's simple and expressive API transformed a critical economic model for the Central Bank of Chile, making high performance accessible. #JAX #SciComp #Economics #Python

goo.gle/jax-economics

7

69

11,631

26 Jul 2025

Should not miss it❣️❣️❣️

22 Jul 2025

The tentative program for the summer school/conference on "Deep Learning in Economics and Finance (August 25-29)" is online: sites.google.com/carloalbert…, and sites.google.com/carloalbert… @YuchengYang1993 @glviolante @unito @nuvoloscloud

1

8

1,843

3 Jan 2025

Great❣️It’s always nice to have more options available‼️

notes.quantecon.org/submissi…

2 Jan 2025

I added a notebook to @QuantEcon Notes. It shows how to use Julia JuMP for OLS and ML estimations.

Of course the purpose of the document is not to argue that we should use JuMP for OLS or ML! I wanted to see how JuMP could accommodate estimations with data.

20

2,686

23 Nov 2024

We have just added a new lecture on Neural Network using Keras and JAX.

❣️Don’t miss it.❣️

jax.quantecon.org/keras.html

21 Nov 2024

Also, a reminder that @quantecon has rapidly expanding content for other frameworks, including Python JAX jax.quantecon.org/intro.html

12

55

9,178

QuantEcon retweeted

21 Nov 2024

@QuantEcon has released an updated version of the Julia lecture notes, with updated manifests and packages for Julia 1.11 support: julia.quantecon.org/intro.ht…

2

50

256

26,318

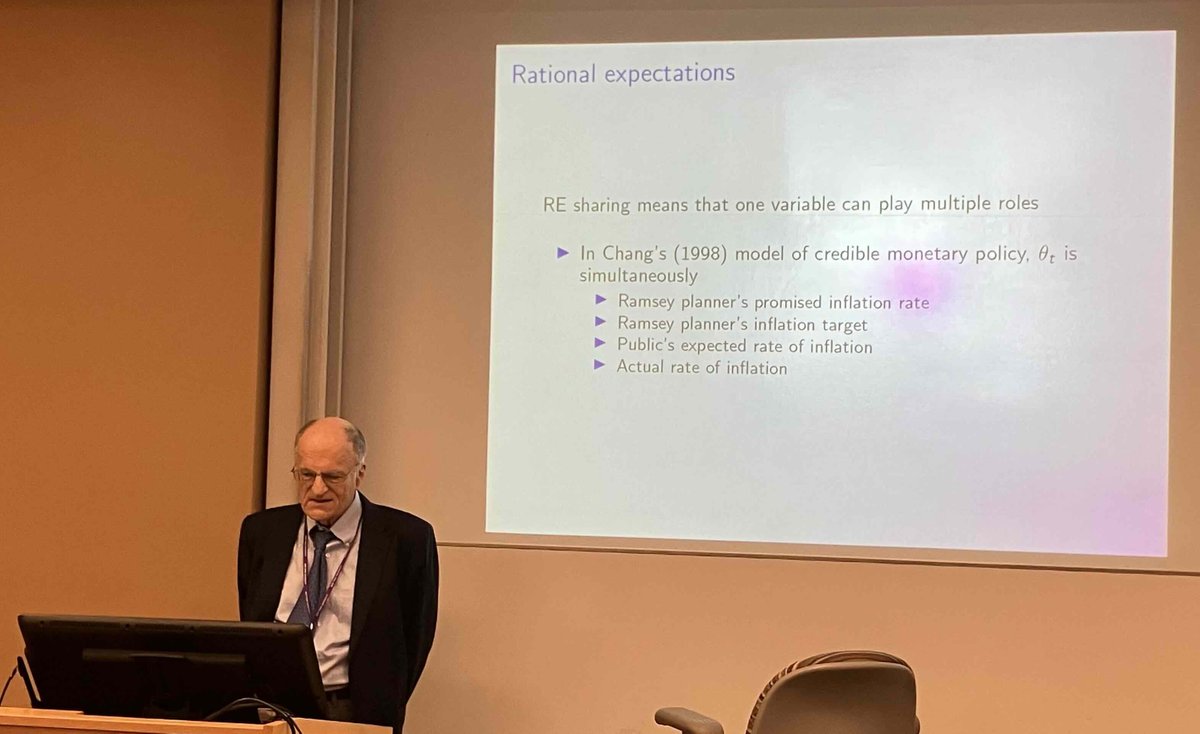

4 Oct 2024

Those fascinating reflections❣️❣️❣️

4 Oct 2024

You don't hear very often this kind of reflections on economics' methodology. So interesting to hear Tom Sargent talking about Lucas' approach to macro (today at NYU)

tomsargent.com/research/Macr…

2

14

3,230

30 Aug 2024

Thanks for the very nice talk at Quantecon❣️

1

8

28

5,932

5 Aug 2024

Great talk today at #QuantEcon❣️

A.Prof. Inna Tsener (@UIBuniversitat)

presented "Piecewise Linear Solutions for Non-Stationary Models" (with @MarianoKulish). Their innovative approach computes fast, accurate solutions for non-stationary models. #EconTwitter

1

10

36

3,509