A beginner, Learner

Joined July 2021

- Tweets 572

- Following 90

- Followers 129

- Likes 364

22 Photos and videos

One of the best podcasts I’ve listened to, not just for the insights (there are plenty), but for the honesty and free-flowing convo.

Both @jasoncbuck and @jposhaughnessy were excellent. Despite being unstructured, the transitions between topics felt natural and seamless.

1/2

May 28

Jason Buck (@jasoncbuck), founder and CIO of @MutinyFunds, joins Infinite Loops to explore risk, religion, failure, resilience, the Cockroach Portfolio, and why being less certain may be the ultimate edge.

TIMESTAMPS

0:00 Intro

4:32 Jason Buck’s Unusual Career Path

10:26 The Crash That Changed Everything

15:23 Does Alpha Really Exist?

16:52 Why Diversification Should Hurt

26:05 The Cockroach Portfolio

30:38 Firing Potential Clients

50:21 Right About the Crash, Wrong Trade

1:17:13 Walking Through Nihilism

2:02:12 Enjoy Your Burrito

1

1

5

825

I found myself laughing along with them at multiple points.

They make you appreciate friends who can wander across topics for hours without the conversation ever feeling forced.

2/2

1

2

125

Hope @business did this analysis in their

bloomberg.com/news/articles/…

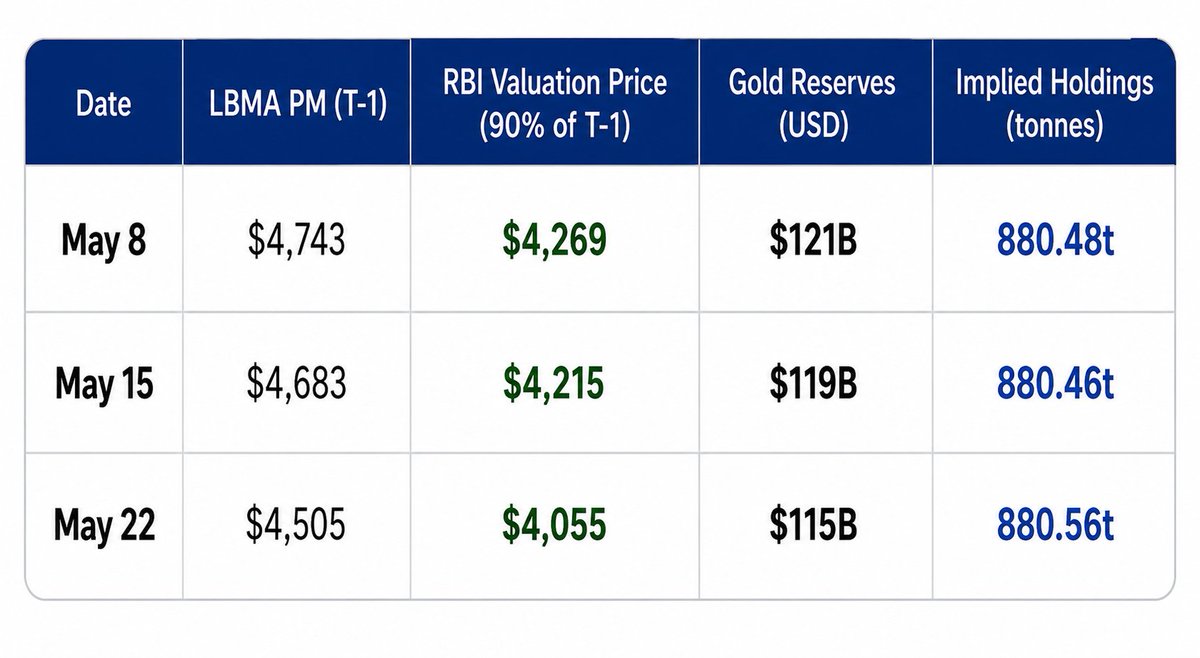

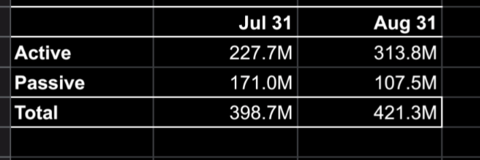

The RBI uses 90% of LBMA PM fixing price with a day's lag to value its gold.

Using this methodology and RBI's gold value in $ terms, one can derive the gold qty. As you can see, there is no change in it and matches RBI number perfectly

1

149

Instead, they wrote

> A fall in the reported value of the RBI’s bullion reserves came despite a hike in import duties on the precious metal, which should have boosted the value of the bank’s bullion and dollars. This suggests the RBI was selling gold

1

61

thanks @business for retracting the article 😀

x.com/business/status/206257…

Bloomberg has retracted a post on X based off an inaccurate Bloomberg Economics report bloom.bg/4ebLXmi bloomberg.com/news/articles/…

42

May 24

Difficult experience to share. So, thanks for sharing @bennpeifert . Shows how difficult OPM business is and experience can make anyone humble

May 23

Good morning my loves, happy Saturday. Sorry I've been quiet, obviously been busy, but thought it'd be nice to give you all the details on the multi-strategy absolute return program that experienced the 28% drawdown this year. (1/n)

1

200

May 24

For me, this is the core point of the thread

x.com/i/status/2058215655619…

May 23

and actively chose to hold and increase positions that we believed in, waiting for the reversion that would take us from down 15-20% on the year to up 20% and make us look like geniuses.... obviously did not turn out to be the right thing.

1

60

May 24

May not agree with the choice of words here but this is reality. A targeted vol doesn't give a smooth ride. Realized vol can be clustered and lumpy. Very difficult for the smaller funds without lockups

x.com/i/status/2058214583509…

May 23

No one month was that bad, no one trade experienced some major blowup, but four months of down 7-9% in a row, even in an 18-vol target strategy, is too much for investors to reasonably handle. Our investors were great through this process.

40

Quant Padawan retweeted

Apr 13

What is the North Sea physic mkt, and how should the gap between the paper and physical markets be resolved?

Every time I post about the physical market, I see a lot of complaints about why oil prices aren't rising further. Many ppl even criticize me, claiming I’m not explaining things properly.

First, I’ll summarize the basic components of the North Sea market.

ICE Brent Futures: A financially settled paper contract used primarily for broad directional hedging and speculation without the intention of physical delivery.

EFP (Exchange of Futures for Physical): A swap that acts as a bridge, allowing a trader to convert a paper futures position into a physical cargo contract.

Forward Brent: A standardized OTC physical swap for future delivery. It represents actual oil but remains non-dated bc the exact loading schedule is not yet determined.

Dated Brent: The global benchmark price for physical crude. It is assessed daily by agencies like Platts based on actual trades of the most competitive grade within the BFOET WTI basket, triggered once specific loading dates are confirmed (typically 10-30 days prior).

CFD: A short-term swap representing the price difference between Forward Brent and Dated Brent. It is used to plot the physical forward curve and assess whether the market is in contango or backwardation.

DFL (Dated to Frontline): A swap that links the physical Dated Brent assessment directly to the front-month ICE Futures contract, managing exposure between the physical and financial markets.

Diff (Grade Basis): The premium or discount applied to a specific physical cargo relative to the Dated Brent benchmark. Driven by crude quality, logistics, and refinery demand, this unhedgeable spread is where physical traders generate profit.

This alone should be enough. From there, I’ll explain how the gap between the paper market and the physical market actually closes.

A massive divergence between Dated Brent (physic) and ICE Brent futures (paper) typically indicates acute near-term physical tightness relative to forward expectations.

If Dated Brent remains at $120-130/bbl leading into the expiration of the front-month ICE Brent futures contract (currently around $100/bbl), the futures contract must converge toward the physical price.

The convergence is not optional; it is mathematically enforced by the exchange's settlement rules and market arbitrage. This operates through three primary mechanisms:

1) Cash Settlement via the ICE Brent Index

ICE Brent futures are cash-settled upon expiration and do not involve physical delivery. Expiring contracts are settled against the ICE Brent Index.

The Index is a calculated average of trading activity in the relevant physical Forward BFOET(Brent, Forties, Oseberg, Ekofisk, Troll) WTI Midland market during the final trading days of the futures contract.

Bc Forward Brent and Dated Brent are intrinsically linked, a physical market sustaining $130 will generate an ICE Brent Index near $130.

Consequently, any futures positions left open at expiration are forcibly settled at this higher Index price.

2) The Arbitrage Channel (EFP Mechanism)

If a $30 spread exists between paper and physical markets, traders will immediately exploit the arbitrage using the EFP mechanism.

Traders buy the undervalued ICE Brent futures at $100 and simultaneously sells a physical Forward Brent cargo at $130. They execute an EFP to swap their long paper futures position into a long physical Forward position.

The newly acquired long physical position cancels out their short physical position, locking in a profit (minus the EFP swap cost). To execute this arbs on a large scale, traders must aggressively buy ICE futures. This massive purchasing volume forces the futures price up until the gap closes and the arb window is eliminated.

3) Forced Short Covering

Market participants holding short positions in the ICE Brent futures market face extreme risk if the physical market disconnects to the upside.

Knowing the contract is destined to cash-settle against a $130 physical Index, paper shorts cannot afford to hold their $100 positions into expiration.

They are forced to buy back their futures contracts to close their positions before the expiry date.

This forced buying—often resulting in a short squeeze—accelerates the upward momentum of the ICE futures price, driving it into alignment with the physical market.

Through the combination of final index settlement and active EFP arbs, the paper market is structurally tethered to physical reality as expiration approaches.

#oott #iran

103

307

1,753

345,742

Quant Padawan retweeted

Mar 11

Thought a little and wanted to write about optimal execution today!

Most of us work really hard on the alpha part of the investment process. It’s the “sexiest” part and we all love to feel like biggus brainus producing PnL charts that go diagonally from left to right with no bumps. Unfortunately, translating that perfect PnL chart into actual dollars earned is pretty difficult once you account for real life trading frictions. We have fees we need to pay to the exchange, slippage from being front-ran and bid-ask spread if we have no patience.

Large firms often hire large execution trading teams that decide on trading policies. These policies decide whether to make or take, and when quoting, whether to wait and leave the quote as-is, or refresh their quotes and lose time priority.

You’re not a large firm, so you are probably thinking to yourself, should I use limit or market orders? Should I be aggressive or passive? When do I switch between them? This article is meant to address these questions.

As usual happy to give a copy to supporters who retweet and drop a comment :-).

19

15

59

10,279

Quant Padawan retweeted

Feb 6

Very saddened to hear of the passing of John C. Hull, whose book Options, Futures and Other Derivative Securities was a foundational text in finance. I purchased the second edition (the first of many editions I would buy) in a mall bookstore decades ago. Liar’s Poker showed me what trading was, and Hull’s book was my first practical resource on how to do it. In today’s world of massively available educational resources it’s difficult to express how critically important the text was at the time. And still is.

37

193

1,329

77,706

Quant Padawan retweeted

Feb 1

You read about index rebalance strategies everywhere, and it seems like a hedge fund darling, why?

It's one of the few systematic* strategies that are extremely scalable (you can run BILLIONS in capacity), and where the economic rationale for working is easily understood.

Index rebalance is all about predicting how much dollar flow is going into a stock relative to its average daily traded dollar volume. A high dollar flow relative to its usual traded dollar volume will mean the stock price will go up, and vice versa. It is beautifully simple conceptually, but VERY difficult to get right practically. A lot of PMs talk a big game about index rebal, but actually getting it right and managing your risks is NOT easy. Especially when so much of your gross returns can show up as momentum and short interest factors!

---

I write below about a foundational methodology, a starting point for thinking systematically about index changes. You’ll build more sophisticated signals over time, but this framework captures the core mechanics.

This methodology on systematic index change prediction crystallizes an approach many quant shops have traded for years.

Comment AND retweet on THIS post to get a chance for a free article!

22

22

117

20,936

Quant Padawan retweeted

Jan 22

As systematic traders, we are often working with tens of thousands of features where we need to find out what are the most predictive, uncorrelated features.

Even at 10,000 features, a standard correlation matrix is 50 million calculations, and is near untenable. At 1,000,000 features, almost all uncorrelated feature selection methods break down.

Not this one. In today's article we discuss a pretty cool feature selection method that removes all redundant features and still find the most predictive features.

As usual, retweet and comment for a free chance at a free article :-).

30

36

143

24,727

Quant Padawan retweeted

Jan 7

You will often hear practitioners say that when you generate forecasts for instruments, what REALLY matters is the RANK of your forecasts, not the actual MAGNITUDE.

Why?

It's because in a cross-sectional strategy where you are going long some instruments and short some instruments, you make money from getting the RANKING right, even if you can get the magnitude very wrong (really, I show an example later)!

So most systematic long short flows look like this:

1. You generate some forecasts using some ml model

2. You rank the forecasts

3. You go long/short the top/bottom decile

Here's today's problem... your ml model is trained on MSE, which is a pointwise estimate that doesn't give 2 shits about ranking! So you can have fairly accurate forecasts and still get ranking wrong (and lose money)!

---

How do we solve this?

Read on at the bad place to find out more!

As usual, happy to give out free reads to anyone who retweets! Have a great day!

17

33

110

18,395

Quant Padawan retweeted

Jan 5

You have produced multiple forecasts over multiple horizons, how do you trade them optimally?

These are the things your PM (the monetization team) is trying to solve!

When you have forecasts at multiple horizons, the natural instinct is to combine them somehow and trade toward the combined target.

Perhaps you'll try equal weights.

Maybe returns-weighted.

Maybe volatility-adjusted.

All of these are wrong!

Want to understand how your PM monetizes multiple forecasts?

I'm giving away free articles to random retweets as per usual!

8

50

91

17,398

Quant Padawan retweeted

Jan 1

The context in which people hear about factor models is always about using factor models to hedge. This is ONE side of the story, where you are trying to remove systematic risks from your portfolio.

The real pros understand that factor models are a denoising technique.

They partition returns into “stuff that does not matter” (systematic factor exposure) and “stuff that does matter” (idiosyncratic returns where alpha lives).

The better you model the systematic part, the cleaner the residual and the cleaner the residual, the easier it is to find tradeable alpha.

In today's article, I talk about this phenomenon and how to roll your own factor models no matter what markets you are trading!

As usual, I will be giving out the articles for free to some retweets!

11

40

114

18,561

Quant Padawan retweeted

17 Dec 2025

Most factor investors are trading the wrong thing.

You found a signal. You want exposure. So you sort stocks, go long the top quartile, short the bottom... and call it a day.

The problem you'll face is that the "value portfolio" isn't pure value. It's value whatever other systematic risks happen to be correlated with cheap stocks.

You've introduced unwanted bets to your signal. Here's how to actually trade factors and not proxies for them.

(I'm going to try something new where the I'll grant free access to 10 random users who retweet and comment *anything* at the end of the hour!)

👇

20

13

52

9,255

17 Dec 2025

2

1,372

Quant Padawan retweeted

24 Oct 2025

194

571

3,176

577,602