CEO & CIO, Newfound Research | 🥞 Return Stacked® ETFs | 🌊 Liquidity Cascades | 📆 Rebalance Timing Luck | ⚡️ Risk cannot be destroyed, only transformed.

Joined October 2009

- Tweets 41,529

- Following 1,246

- Followers 84,340

- Likes 80,397

5,683 Photos and videos

Pinned Tweet

28 Aug 2023

My company, Newfound Research, turned 15 today.

Coming up on this anniversary, I reflected quite a bit on my career. I’m not sure why, but this milestone feels larger than I would've expected.

So I decided to write something.

15 Ideas, Frameworks, and Lessons from 15 Years

98

274

1,693

655,101

Jun 12

Someone please tell me why LLM text structure is always so obvious.

The same phrases and structural patterns all the time.

"is the tell"

"It isn't X it's Y"

"X is Y; Z isn't"

19

1

56

7,546

Jun 12

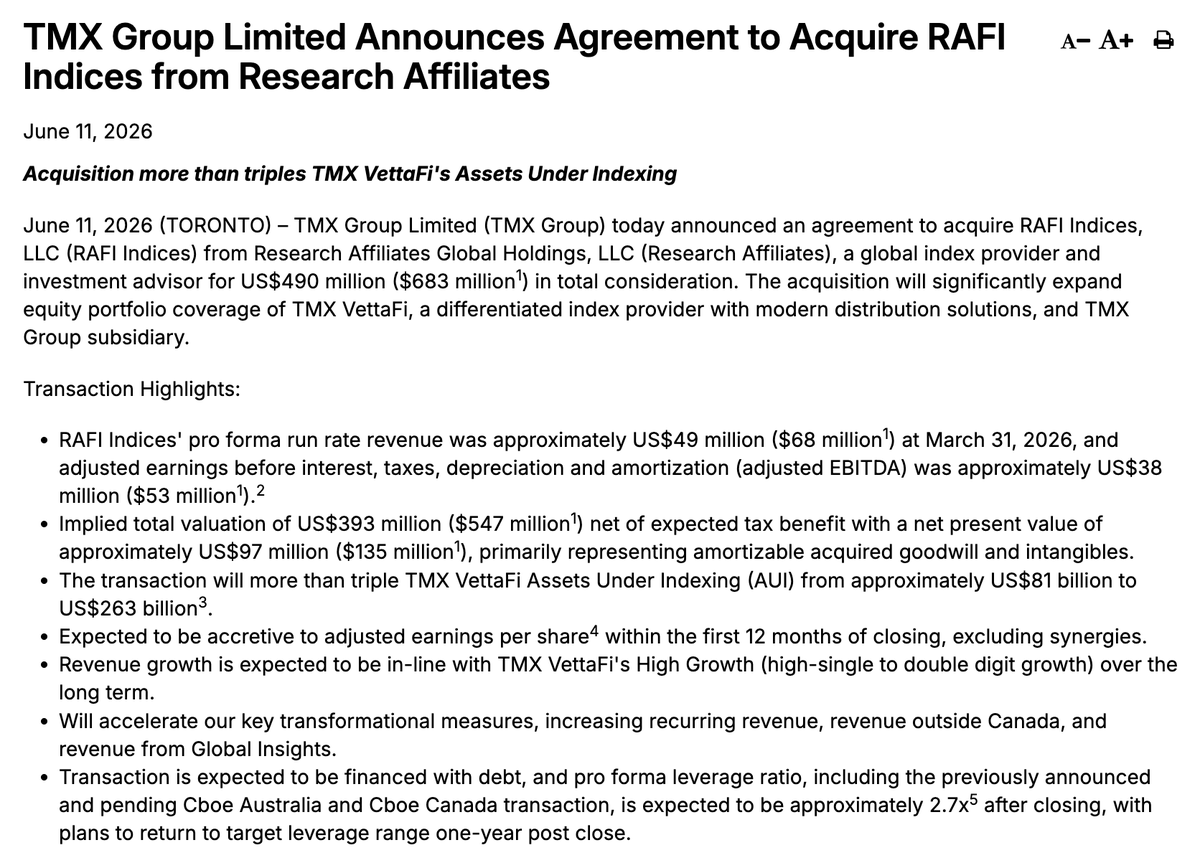

RAFI Indices selling for 10x revenue ($490mm valuation on $49mm revenue).

But here's the wild part: they have $182 billion in AUI.

Which implies an average indexing fee of 2.9bp.

tmx.com/en/newsroom/press-re…

6

5

28

6,748

Jun 11

what if I told you that the role of bonds in a portfolio was never about diversifying the path, but always about diversifying the destination...

4

3

66

8,175

Jun 11

I really don't get this fear mongering coming from ETF folks.

In mutual fund world, Schwab Mutual Fund OneSource is Schwab's no-load, no-transaction-fee fund service.

Most NTF funds pay Schwab 40bp per year.

Now, this can theoretically get passed onto mutual fund investors in three ways:

1. A higher management fee

2. 12b-1 fees (max 25bp)

3. In sub-TA fees

But all of that rolls up into the stated gross expense ratio. There's nothing hidden.

In the ETF world we charge unitary fees. There is no 12b-1 (technically it can be adopted, but who does?). There is no sub-TA fees or "Other Expenses" line.

Unless we raise our management fees (good luck), the issuers simply end up less profitable.

Which I think is what everyone is actually upset about?

Jun 11

"I don't want to see ETFs going back to the mutual fund dark ages where nobody knows what the fees are. It should be clear, transparent.. and not use the customer as negotiating tool." - @Perth_Tolle on Fidelity's (and Schwab) move to charge ETF issuers for shelf space and how that could stifle innovation and trigger the return of dreaded 12b-1 fee for ETFs w/ @kgreifeld @scarletfu

2

3

26

10,357

Jun 11

is it too much to ask for my wife to coordinate a year long, recorded series of absurd yet earnest tasks – a la taskmaster – for my friends and family to perform, all to be revealed and judged by me on my 40th birthday?

5

25

6,615

☠️ death to dad bod

feeling like I can't buy the time for a workout lately...

25 strict pushups

🚣♂️

10 minutes @ 20 s/m

25 strict pushups

🚣♂️

2x

4 min @ 22 s/m 1 min @ 26 s/m

25 strict pushups

🚣♂️

2 min @ 22 s/m

2x

1 min @ 28 s/m

1 min @ 22 s/m

4x

30s @ 30 s/m

30s @ 22 s/m

25 strict pushups

1

1

14

3,471

Bet you didn't expect to see @RodGordilloP headlining his local Hamilton product

9

1

40

7,552

"You're not supposed to hold levered ETFs for the long run!"

Depends how you're using them.

A nice exploration of a roll-your-own return stacked portfolio. In this case, 100% equities 50% diversified alternatives stack.

Leverage for multiplication vs leverage for addition.

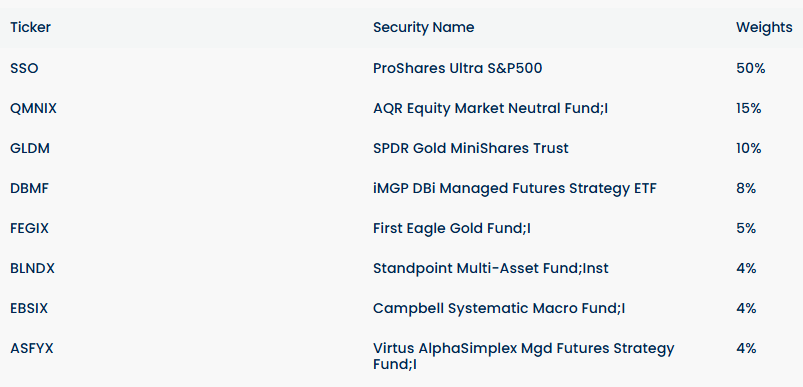

Portfolio Review: Leveraged Equity Diversifiers Portfolio. What are the current holdings?

This portfolio was sent by a client, who kindly agreed to our showcasing it. The portfolio aims to be an all-weather portfolio that uses leveraged equities to make more room for a higher allocation to diversifying strategies. It does not include bonds.

The largest allocation is to a 2x leveraged S&P 500 ETF (SSO, 50%), followed by the AQR Equity Market Neutral Fund (QMNIX, 15%) and gold (GLDM, 10%). The remaining funds mostly represent CTAs / managed futures funds. The portfolio is expensive at 0.93% pa.

finominal.com/portfolio-anal…

10

6

70

18,903

me: finally, a night alone in a hotel with no kids to wake me up. i can't wait for a good night's sleep.

my brain: wake up bitch, it's 5am

10

85

10,298

Where are my HFT crypto folks at who can scrutinize this analysis?

16

3

87

39,018

1

11

4,319

It's awesome to see friends who spend years and years building their businesses just quietly dominating now.

@MebFaber with $4bn in ETF AUM.

@alphaarchitect with $8bn in AUM and $20bn total across Alpha ETF Architect.

@michael_venuto with $62bn in platform AUM at Tidal.

@jdgardner251 with $6bn in ETF AUM

@Perth_Tolle with $3.6bn in $FRDM

10

7

214

22,622

Here's a story for you @EricBalchunas or @DaveNadig: the ETF upstarts of the early 2010s who didn't just survive, but thrived.

2

1

34

3,282

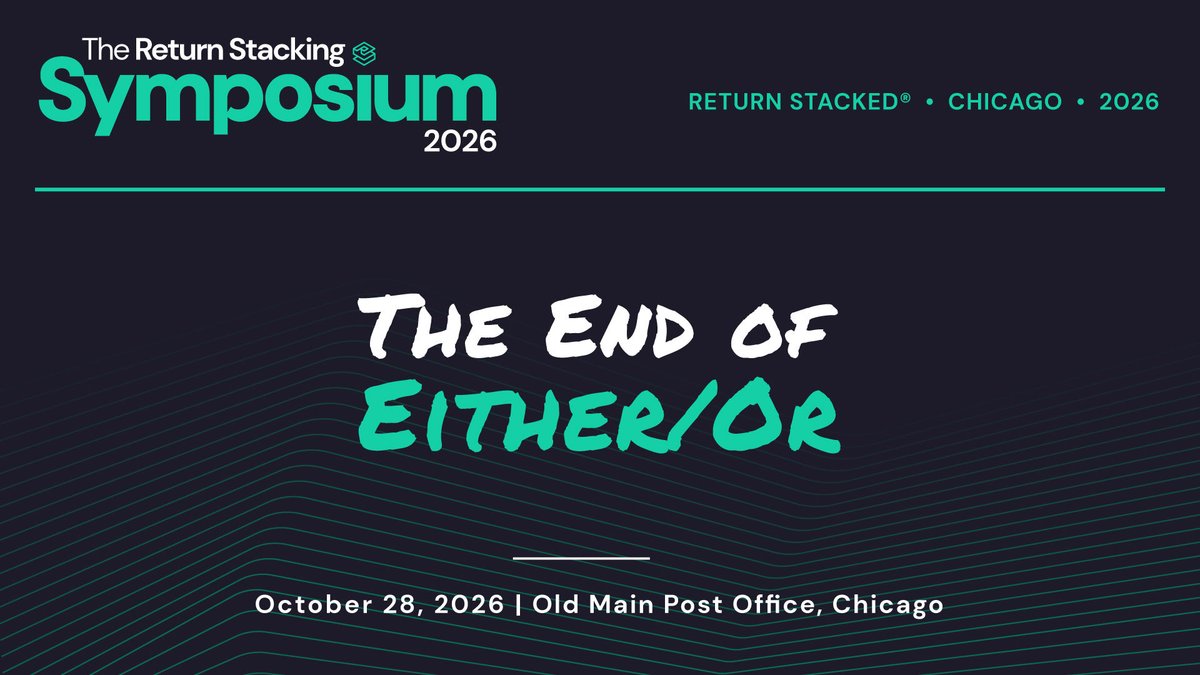

We're back with an absolutely stacked line-up!

📆🥞

The Return Stacking Symposium is back.

📅 October 28, 2026 📍Chicago

🔊 @CliffordAsness @AQRCapital, @jpmorgan,

@ManGroup

💰 Free for advisors, CIOs, and selected media

Registration is now open. 👇

3

34

8,103

May 31

Sometimes I think I deserve the block.

Othertimes, I'm confused by the Internet.

19

2

93

11,949

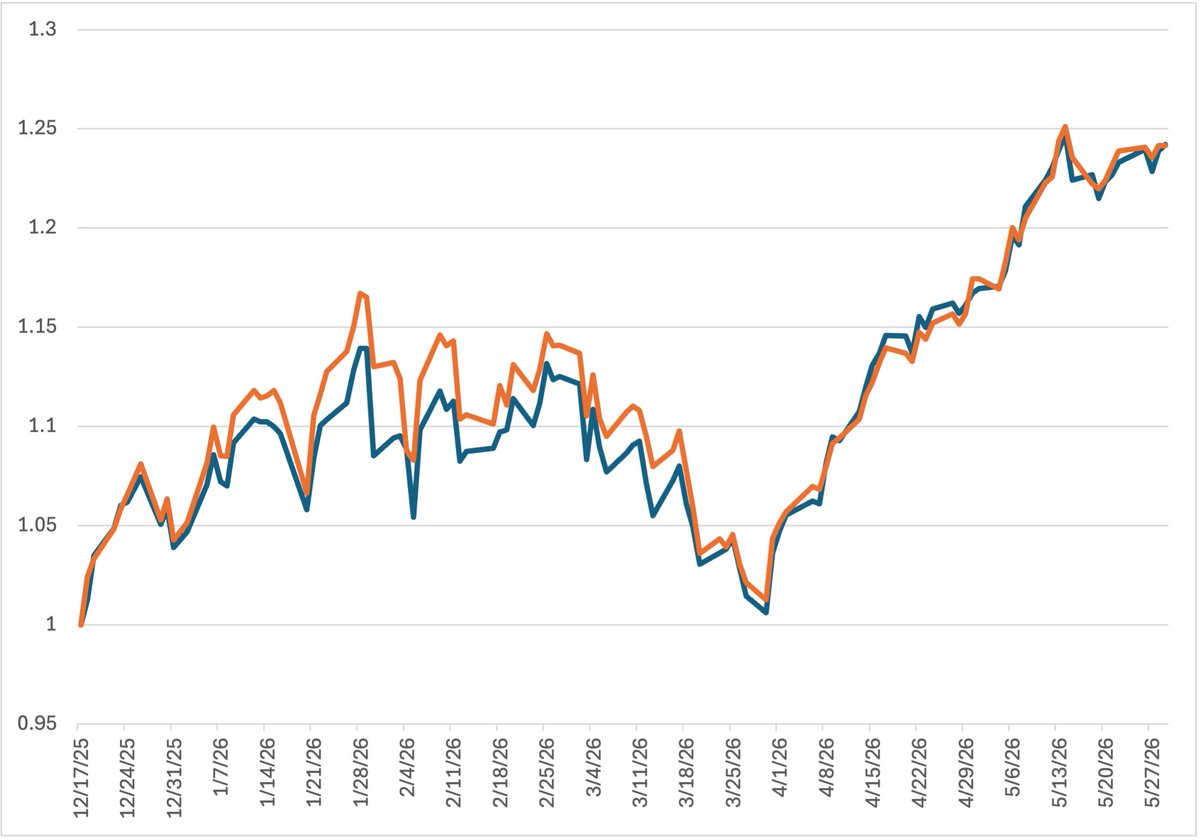

May 30

Some Saturday musings on turnkey return stacking / portable alpha solutions...

Consider two fund choices: 100% S&P 500 100% Managed Futures or 100% US Bonds 100% Managed Futures

At the portfolio level, both allow you to do the same thing: stack managed futures.

But there are some very important trade-offs.

Let's assume that both implement their beta with 75% cash securities 25% futures.

Right now, the financing in S&P 500 futures is approximately SOFR 88bp while in US Treasuries it is approximately SOFR. That means implementing the structure on top of equity beta has an invisible 22bp drag (88bp x 25%).

In fact, S&P 500 futures are almost always more expensive than Treasury futures and have traded substantially over the SOFR 30-50bp historical average for the last several years.

Furthermore, if you ask people outright which structure is "riskier" (e.g. which one is more likely to face a substantial margin call), almost everyone will say the equity plus managed futures approach.

And yet equity plus managed futures seems to absolute dominate bonds plus managed futures in sales.

Why?

I'd argue it's all about the perceived line item risk.

Equities are already risky... so what if we add something else on top? And when you combine stocks managed futures, neither dominates the return.

Bonds on the other hand are supposed to be safe and steady. Adding managed futures on top adds substantial volatility. Plus the managed futures dominate the variance, making the alternative return really stand out.

That line-item risk has an increasingly costly trade-off though (especially if you're implementing the beta only with futures...)

12

3

105

19,483

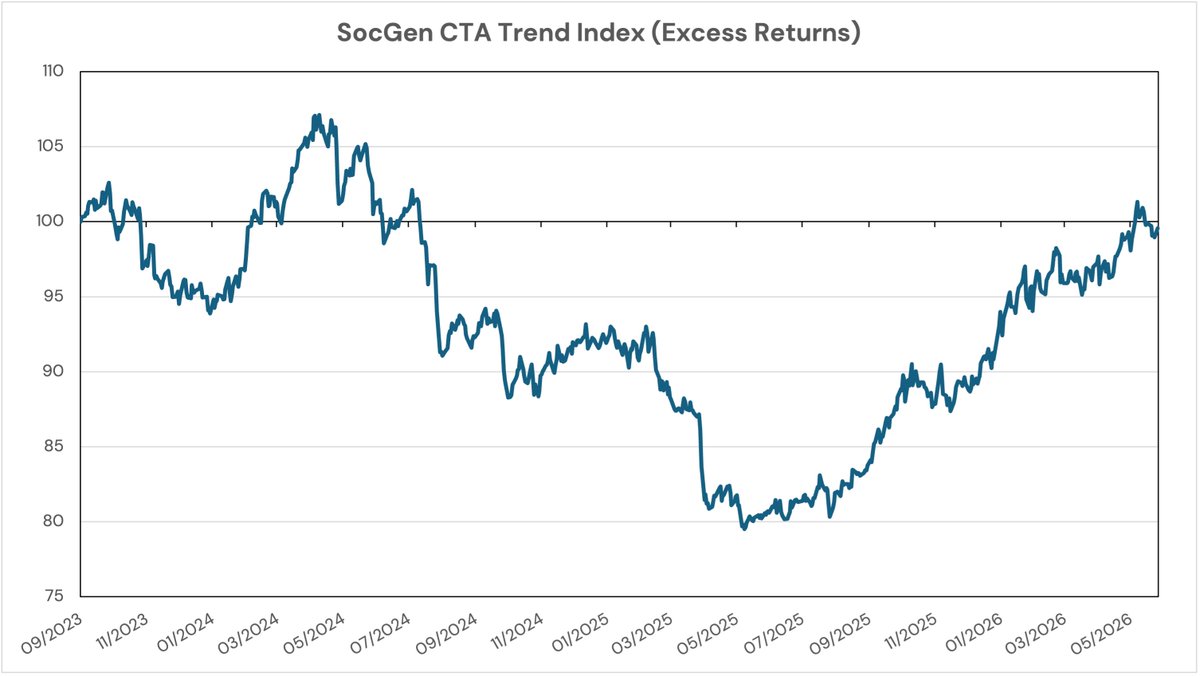

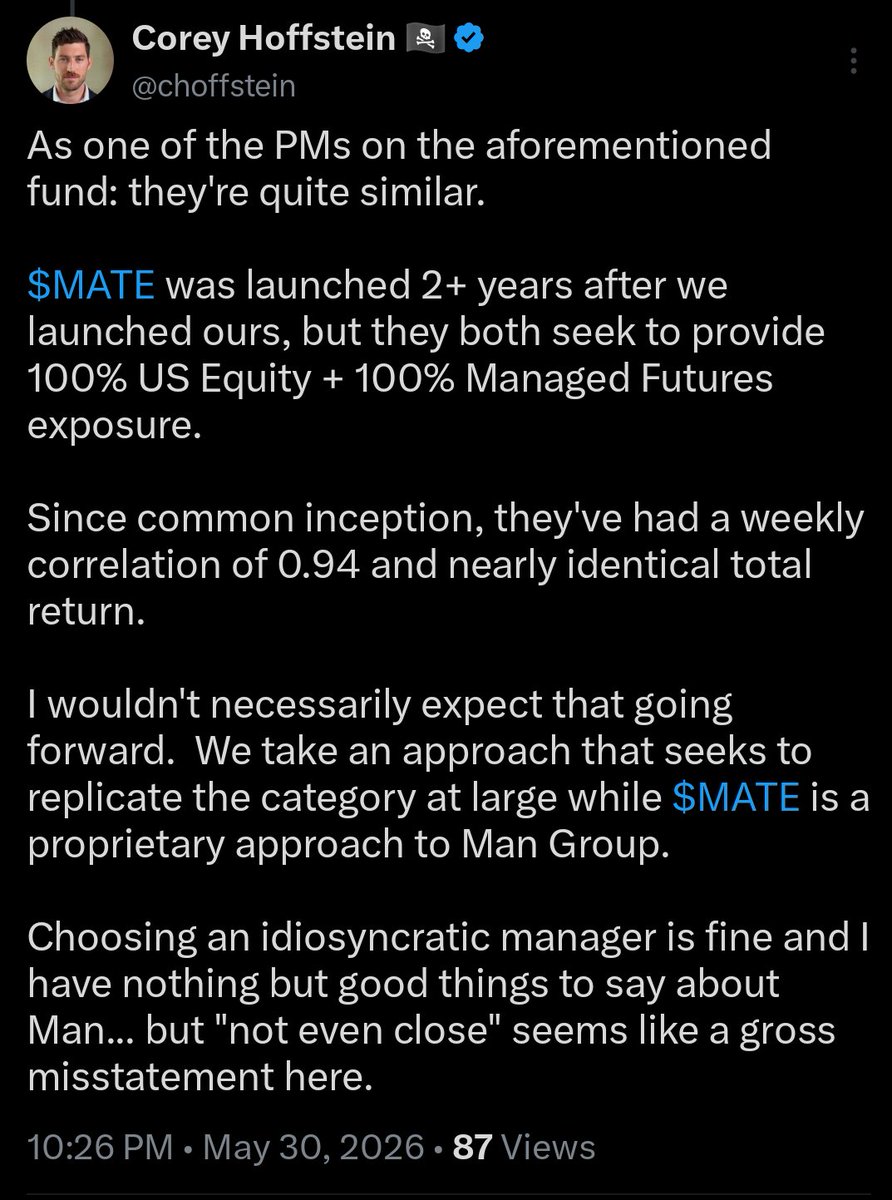

May 28

US 100% Equity 100% Trend funds...

Return Stacked (Sep 6, 2023) →

AQR – QCFIX (Jun 18, 2025) →

Simplify – CTAP (Dec 8, 2025) →

Man Group – MATE (Dec 17, 2025) →

JPMorgan – JPFP (May 28, 2026)

I bet we'll see more...

14

2

144

21,359