Documenting the journey. Quantitative Investing ⚙️ : Macroeconomic Modelling 🧬 : Long & Medium-term Bias📈

Joined November 2022

- Tweets 1,225

- Following 150

- Followers 255

- Likes 1,159

932 Photos and videos

🚨Updated Disclaimer🚨Not financial advice. I share long-only strategies. My posts are NOT intended for shorting, gambling, or the use of leverage—do not interpret any of my content for these purposes. Do your own research and consult a financial advisor before making decisions.

5

2,461

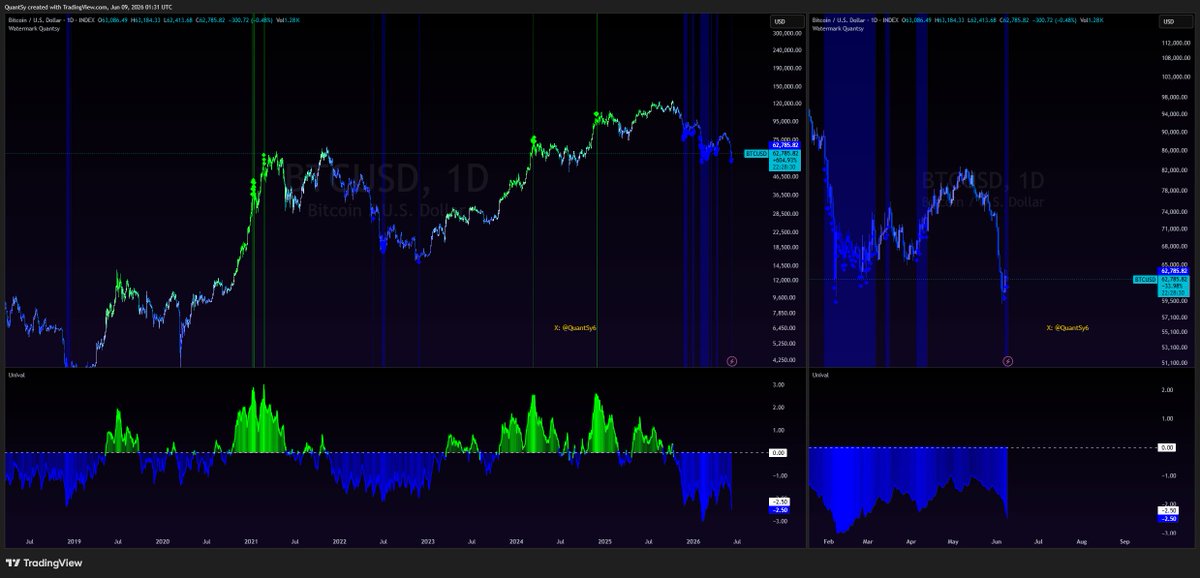

$BTC price is sitting around the same zone as February 2026, where we had a record all time low in terms of valuation. What's the issue though? We have price at the same levels, with a much higher valuation, a long term trend that has not reached its full downside potential (current reading -0.67, lowest reading possible is -1), and a liquidity heatmap suggesting we are in a slight contraction zone.

Valuation has room to the downside.

Long term trend has room to the downside.

Liquidity heatmap not only is suggesting downside but is currently only in a slight contraction phase; full contraction can still be reached.

Expect more volatility instead of stability. Exhaustion has not been reached.

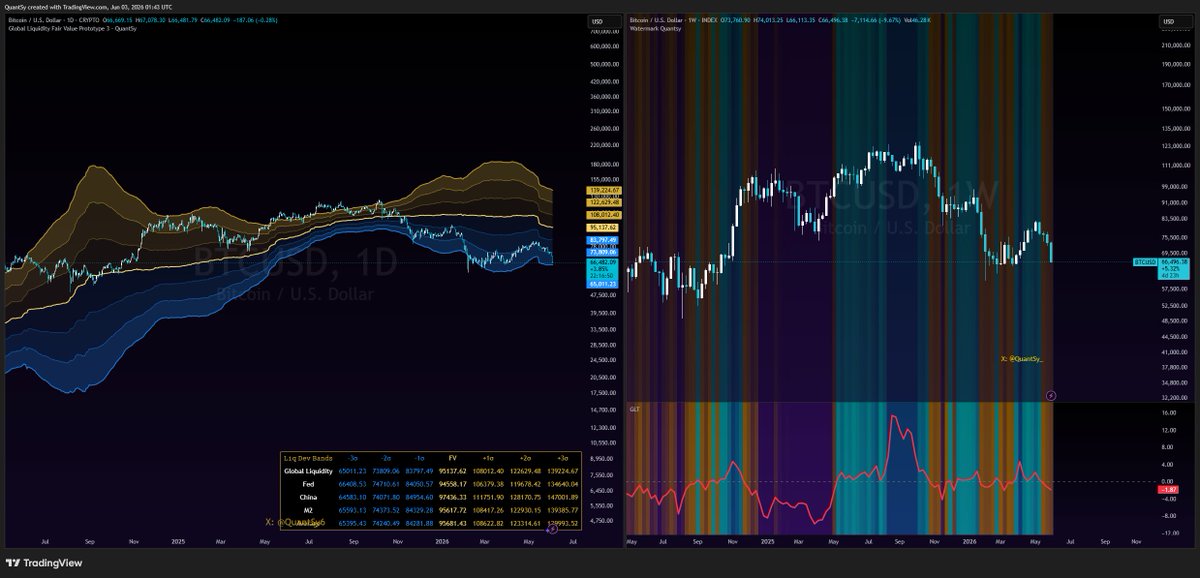

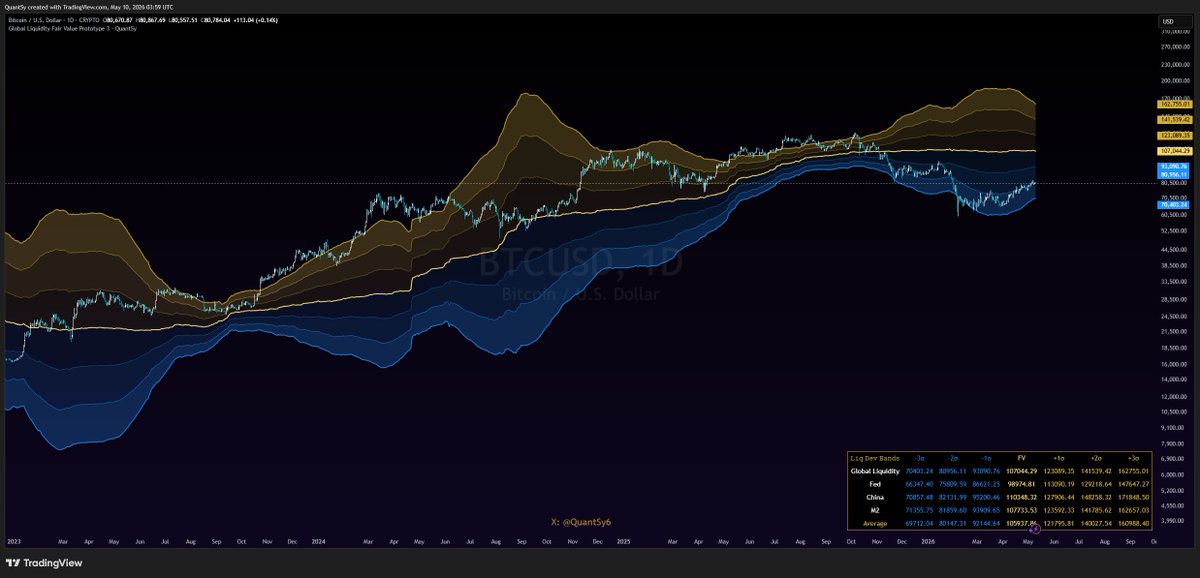

Global Liquidity Fair Value for $BTC currently sits around $95.1k with current price sitting close to the 3rd st deviation band below the mean.

In addition to the above, the liquidity heatmap (custom proxy, not GLI) has been flagging a slight contraction zone for a little while now.

Current readings do not show that stability is the most probable outcome. Next post will show why there is still room for more nukes.

1

5

348

Global Liquidity Fair Value for $BTC currently sits around $95.1k with current price sitting close to the 3rd st deviation band below the mean.

In addition to the above, the liquidity heatmap (custom proxy, not GLI) has been flagging a slight contraction zone for a little while now.

Current readings do not show that stability is the most probable outcome. Next post will show why there is still room for more nukes.

1

14

616

The reset is building up according to Parralax. The last leg has been exhaused and the metric cooled off to the green zone. Elevated readings suggest areas of exhaustion where a move has reached its potential ceiling.

In this case, the plateau has been hit and the gauge is now sweeping the floor for $BTC. A resolution of a durable trend can be the next move from here. The real question is, bull or bear?👀

13

283

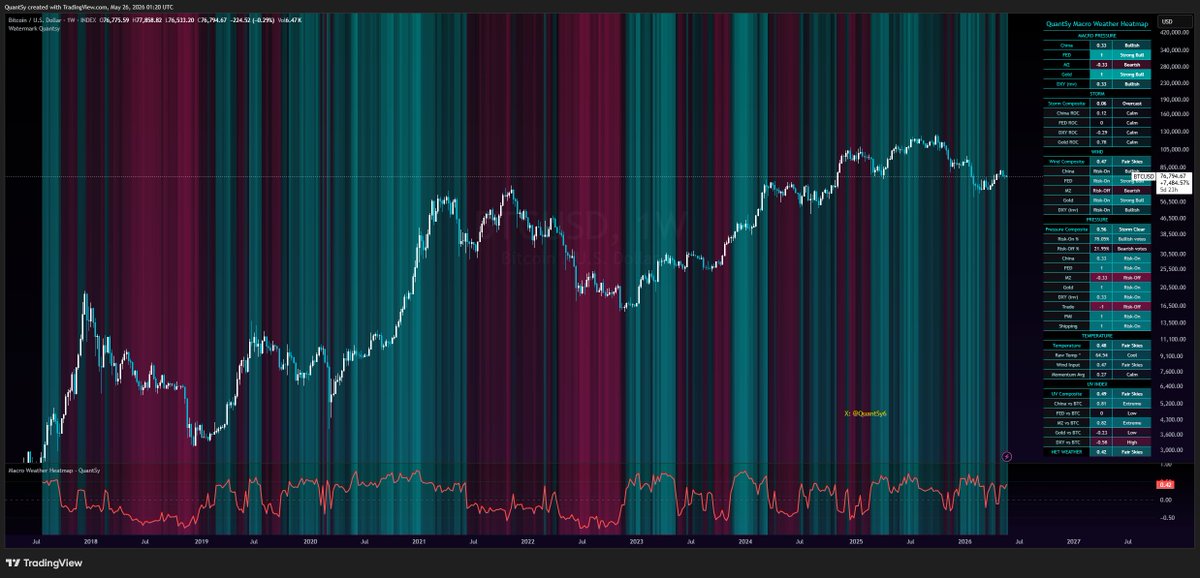

$BTC Macro Weather Report May 25, 2026:

Net Weather: 0.42 | Fair Skies

Macro Pressure split: FED and Gold both Strong Bull. China and DXY (inv) holding Bullish. M2 the lone drag, bearish at -0.33.

Storm: 0.06 -> Overcast but calm. Every RoC reading sits Calm. No volatility pressure building beneath the surface.

Wind Composite: 0.47 -> Fair Skies. Headwinds minimal. Risk-On vote 78.05% vs Risk-Off 21.95%. M2 the only component flashing Risk-Off alongside Trade.

Pressure: 0.56 -> Storm Clear. PMI and Shipping confirming Risk-On.

Temperature: 0.48 -> Raw Temp 64.5 (Cool). Momentum Avg 0.27, still Calm.

UV Index: 0.49 -> M2 vs BTC correlation is strong (0.82). China vs BTC is also strong (0.81). FED decoupled (0/neutral). Gold and DXY both inverse.

Read: liquidity backdrop broadly supportive and risk votes overwhelmingly skewed bullish, but M2 keeps dragging across every section. Momentum still Calm, temperature still Cool. Skies are clear, the engine hasn't lit yet.

1

7

187

Oscillator Suite Update:

- FSVZO: Bottomed and flashed a buying opportunity. Metric is reverting back up but still remains within the lower band.

- Vector Thrust: Trend continues to be reported as bullish; however, the regime shifted from high confidence uptrend to a low confidence one.

- VA-RSI: currently flashing a risk-off regime on intrabar data. Confirmed close? remains bullish.

All in all, the suite is not showing high conviction with the current market state. The only optimistic piece of information is the FSVZO. It is easy to make a bearish scenario here. The FSVZO could be signaling a consolidation period where it would give itself time to edge higher before nuking for another bottom, and for Vector Thrust to flip from low confidence uptrend to a bearish one. This can also be confirmed with the Volatility-Adjusted RSI peaking into the red zone.

18

253

GM!

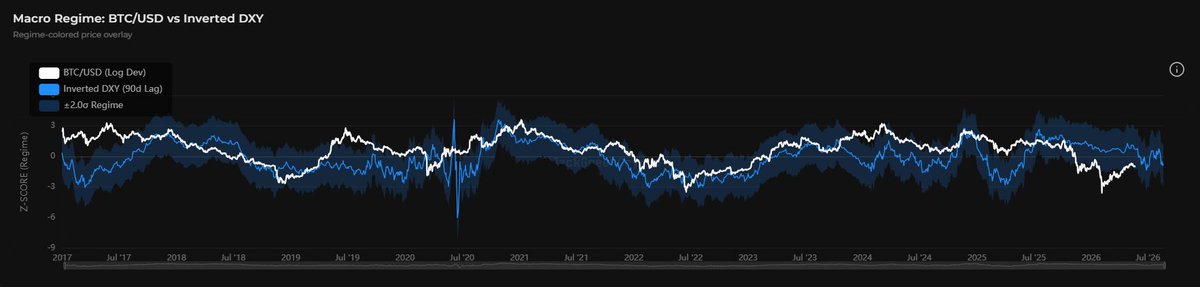

The 90-day-lagged inverted DXY indicator acts as a leading proxy. Dollar moves take time to reach risk assets. In a nutshell, what the dollar did three months ago is lined up against where $BTC trades now. BTC sitting below that line means it has underperformed what the earlier dollar setup would normally point to.

The gap between price and the midline is a representation of where BTC sits relative to the inverted dollar action. In this case, BTC looks to be priced close to -2 standard deviations away from where it should be. The chart here suggests a bearish outlook with a small possibility of price consolidating towards its implied "fair value"; even then, downward pressure still wins.

Three probable outcomes:

- Mean reversion: if the lead-lag holds, BTC is behind and closes the gap by moving up or consolidating (refers back to what I mentioned above).

- Regime break: correlation to this metric breaks and BTC breaches above it. Same way it happened with the famous M2 charts last year when the correlation flipped negative.

- Correlation remains: BTC maintains its relationship with the inverted dollar and nukes for the next month or so.

What decides it? Direction. A narrowing gap supports mean reversion. A widening one means the correlation is breaking down, and that's the riskier setup. The lag is the whole point. Without it you're plotting two correlated lines and calling it confirmation. The 90 days is what turns the second line from "these move together" into "this one moves first." It's also worth stress-testing, since that lag drifts with the macro regime.

@JackGreenCrypto's metric.

1

1

6

434

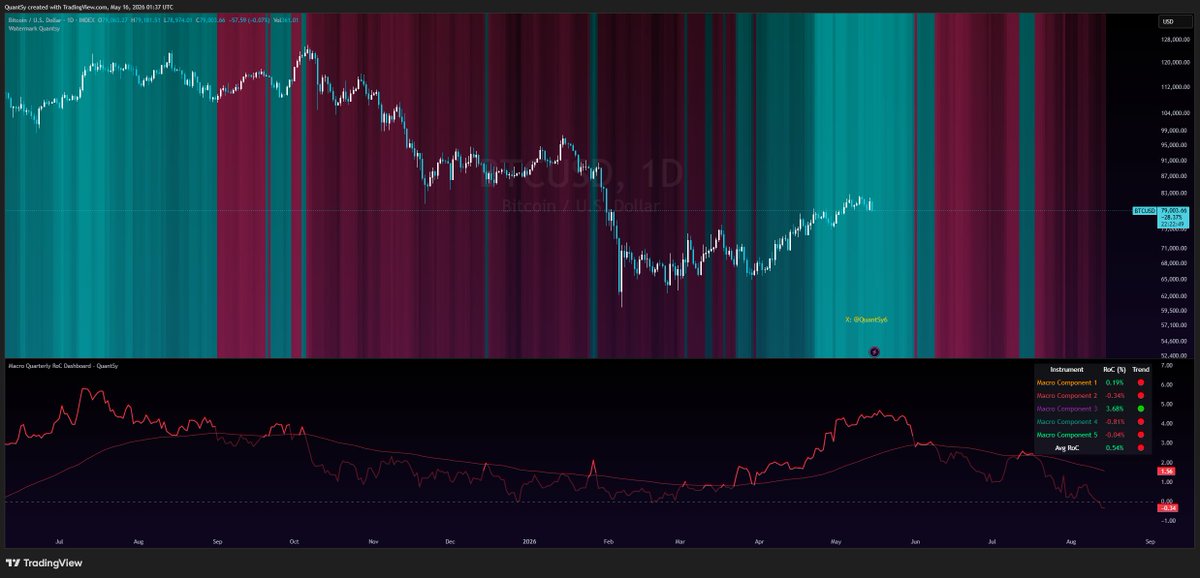

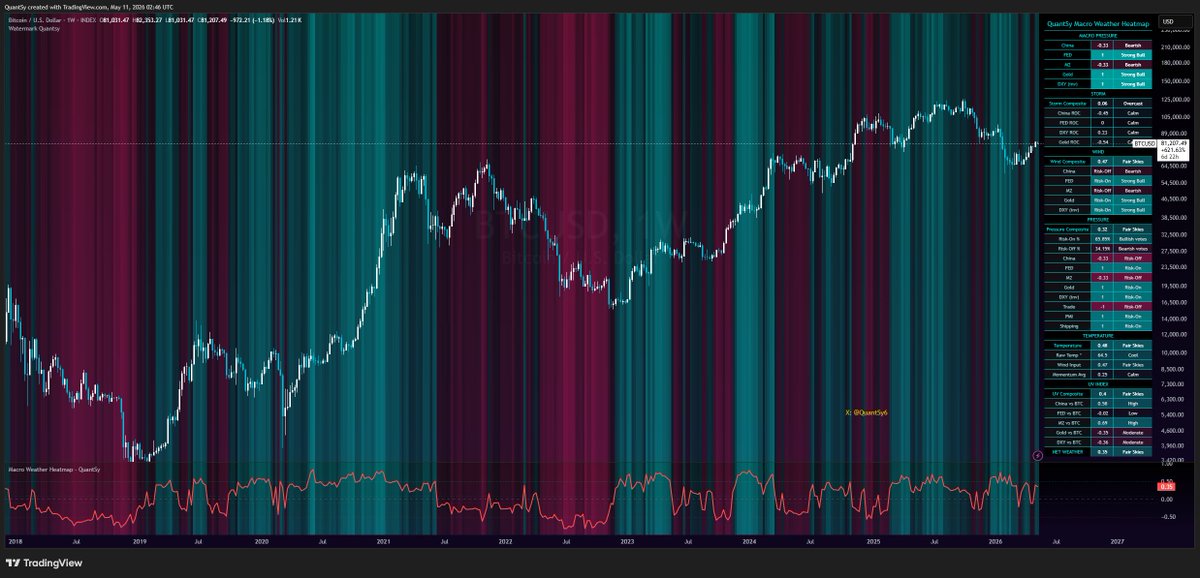

Two different macro tools are aligned with a current risk-off regime for $BTC.

The 3M and 12M annualized RoC in Global Liquidity is signaling that the current market state is not in favour of growth (pink and green plot).

The GLI ( 11W) & BTC 6W Changes from @JackGreenCrypto not only agrees with the above report but also suggests a high probability chance of seeing a risk-on regime only until around early July, 2026.

2

15

541

Universal Valuation on $BTC continues to print higher numbers making price score closer to fair value over time.

The bottom has been priced in for months now. A period of small turbulence can be normal after major onces hit the market for around half a year.

Dips like these equal opportunities.

1

10

294

What this may imply for $BTC price is that despite the expected reduction in liquidity strength affecting the market, the impact might not be as significant as we think it is due to the the rolling β coefficient being so low.

Perhaps some slight down pressure or sideways action. To be monitored as more data becomes available.

Bitcoin's sensitivity to global liquidity is not a constant. It's a regime that can be measured.

The rolling β coefficient, built out by @JackGreenCrypto measures how strongly BTC responds to a unit change in global liquidity over a trailing 52-week window. Full-sample reference: 0.0404.

When β sits above the reference line, Bitcoin is in a hyper-sensitive period where liquidity changes carry outsized weight. When β compresses below, the macro link breaks down, typically during idiosyncratic shocks like exchange failures or regulatory events.

Current read: β sitting near 0.018, well below the full-sample reference. Bitcoin is in a macro-decoupled regime.

Periods where β climbs well above 0.04 have preceded the strongest expansion phases. Sustained compression below the reference often coincides with macro-disconnected drawdowns where idiosyncratic flows dominate price action.

Liquidity is not always the driver. Knowing when it is matters more than knowing the level itself.

1

6

276

Bitcoin's sensitivity to global liquidity is not a constant. It's a regime that can be measured.

The rolling β coefficient, built out by @JackGreenCrypto measures how strongly BTC responds to a unit change in global liquidity over a trailing 52-week window. Full-sample reference: 0.0404.

When β sits above the reference line, Bitcoin is in a hyper-sensitive period where liquidity changes carry outsized weight. When β compresses below, the macro link breaks down, typically during idiosyncratic shocks like exchange failures or regulatory events.

Current read: β sitting near 0.018, well below the full-sample reference. Bitcoin is in a macro-decoupled regime.

Periods where β climbs well above 0.04 have preceded the strongest expansion phases. Sustained compression below the reference often coincides with macro-disconnected drawdowns where idiosyncratic flows dominate price action.

Liquidity is not always the driver. Knowing when it is matters more than knowing the level itself.

1

1

9

690

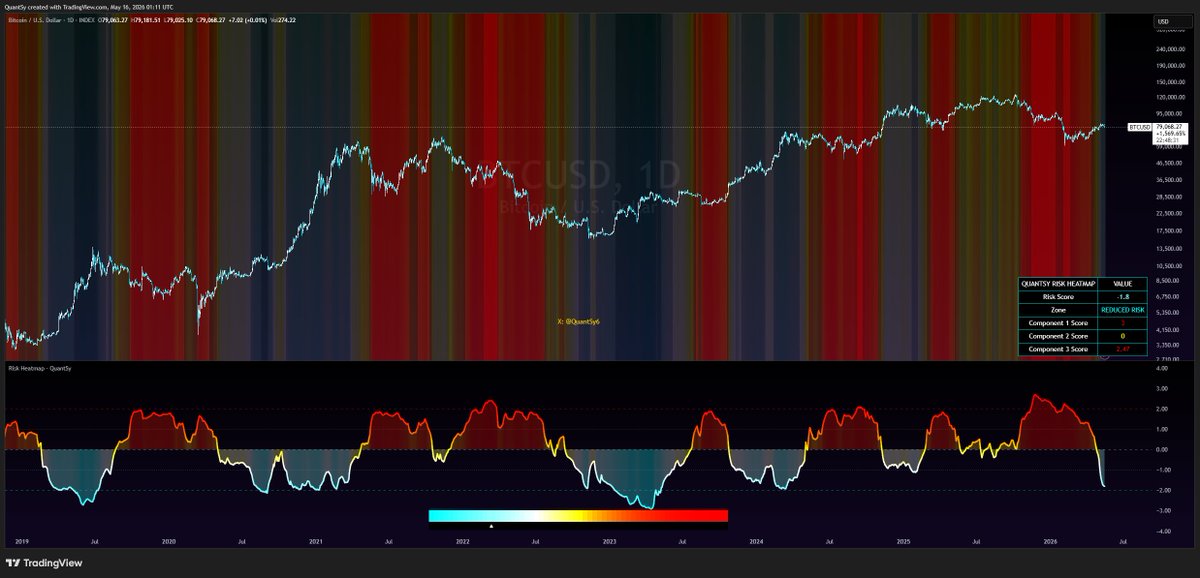

The Risk Heatmap composite reading at -1.8, sitting in the Reduced Risk zone.

Component scores split across the suite: 3.00 / 0.00 / 2.47.

A three-signal composite framework built to systematically identify periods of elevated risk and accumulation windows across the cycle.

Sub-zero readings typically align with constructive risk-on conditions, while sustained pushes above 2.0 mark zones where capital preservation takes priority over exposure.

14

366

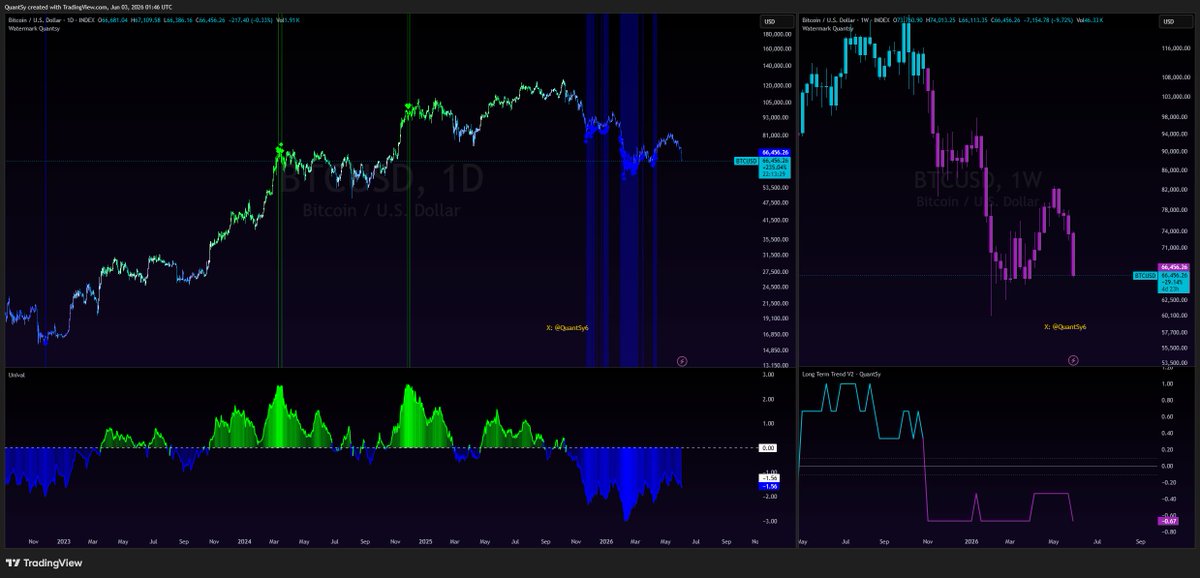

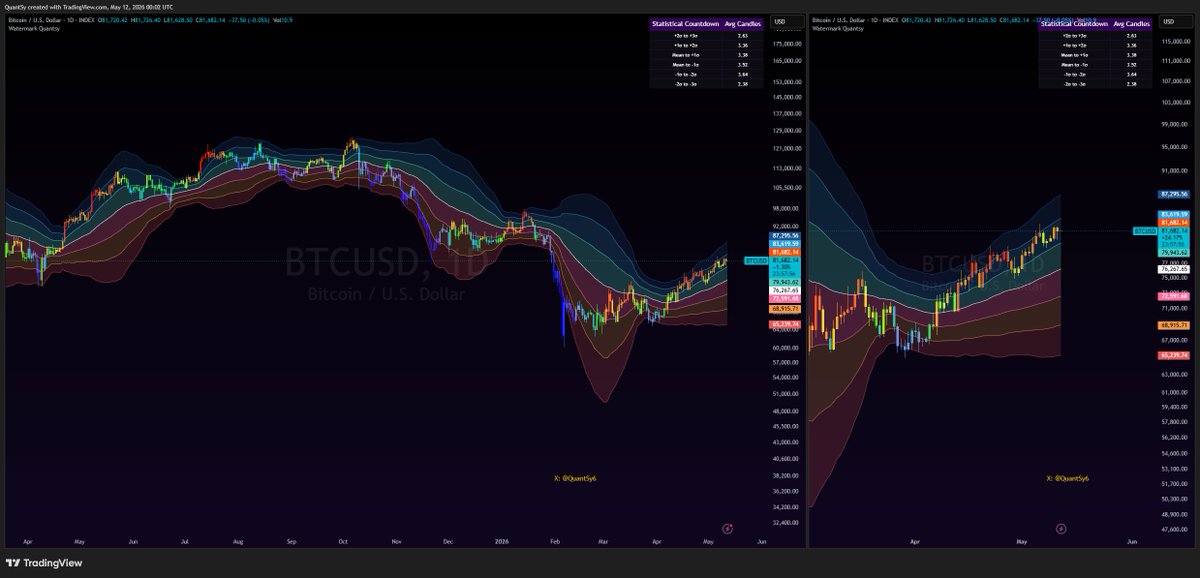

$BTC price is trading between the 1σ and 2σ bands. Slightly elevated but not yet extreme levels of volatility.

An interesting observation is the divergence between the 3σ and the -3σ bands. The lower band has remained flat and is slowly curling upwards while the above band has kinked significantly higher.

The concerns? current heatmap is suggesting we are warm. Yes, not very hot but warmth at these levels can imply a pause that can potentially let the mean get closer to price or a retracement towards the mean.

The risk is of course not super elevated but remains present.

1

4

181

$BTC Macro Weather Report May 11, 2026:

Net Weather: 0.35 | Fair Skies

Macro Pressure split:

FED, Gold, DXY (inv) all Strong Bull. China and M2 dragging Bearish.

Storm:

0.06 -> Overcast but calm. Risk environment remains low, no ROC pressure building.

Wind Composite:

0.47 -> Fair Skies. Not much in the way of headwinds. Risk-On vote 65.85% vs Risk-Off 34.15%.

Pressure:

0.32 -> Fair Skies. Manufacturing and Shipping confirming Risk-On. Trade, China, and M2 putting down pressure.

Temperature:

0.48 -> Raw Temp 64.5 (Cool). Momentum Avg 0.25, still Calm.

UV Index:

0.40 -> M2 vs BTC correlation High (0.69). China vs BTC High (0.58). Gold and DXY decoupled (Moderate inverse).

Read: liquidity tailwind intact, dollar weakness confirmed, but momentum hasn't ignited. Skies are clear, the engine isn't redlining yet.

15

322

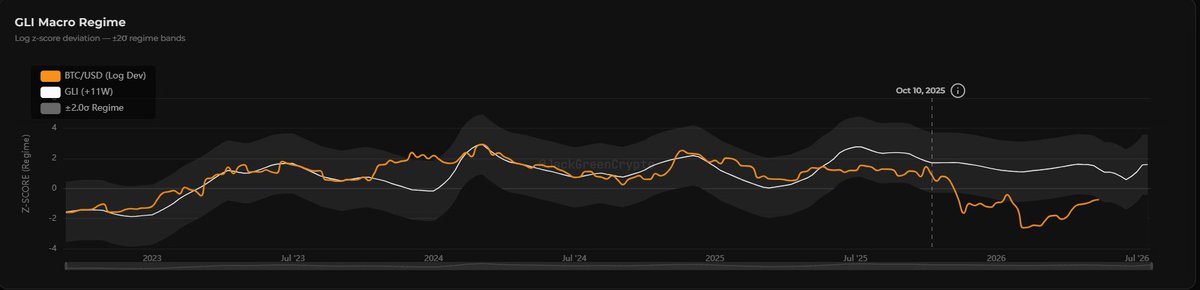

$BTC at ~$80.7K is trading below Global Liquidity Fair Value of ~$107K, placing it nearly 25% beneath where liquidity prices it.

Confluence layer: the GLI Macro Regime model from @JackGreenCrypto has BTC's log-deviation pressing the lower -2σ band since October 2025, while global liquidity itself remains elevated in regime terms. Liquidity never rolled over with price.

The dislocation is real, but so is the setup. Liquidity has held its ground, and price is beginning the walk back toward it.

1

1

16

797

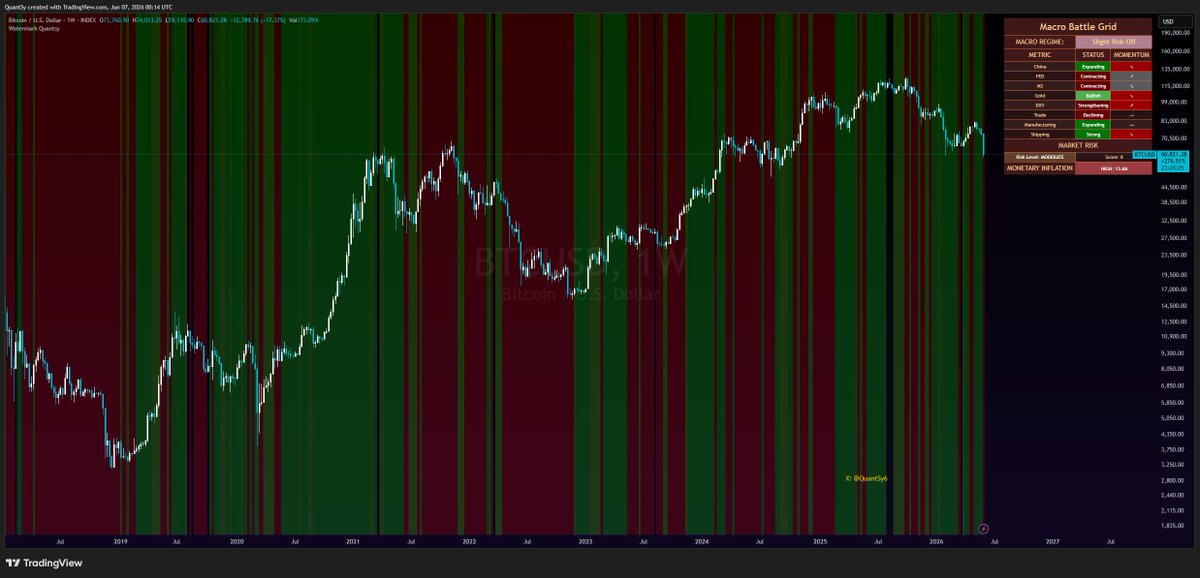

Macroeconomic Report for $BTC:

Macro Battle Grid Summary:

🟢 FED — Expanding ↗️

🟢 Gold — Bullish ↗️

🟢 DXY — Weakening ↗️ (Bullish)

🟢 Trade — Improving

🟢 Manufacturing — Expanding

🟢 Shipping — Strong ↗️

🔴 China — Contracting ↘️ (positive momentum building though)

🔴 M2 — Contracting ↘️ (positive momentum building though)

Net read: 6 green / 2 red, with both red prints showing positive momentum signs. The composite resolves to a Risk-On regime with a low risk score of 5.4.

Liquidity Conditions:

Short-Term Global Liquidity Fair Value (top right):

$BTC closed between the 1σ and 2σ bands above fair-value. Price is no longer cheap relative to short-horizon liquidity, it has absorbed the tailwind and is now pricing above it. Mean reversion risk rises in this zone; sustained moves into 2σ can be rare, but possible. A fresh wave of liquidity would be needed to maintain this statistical level.

Liquidity Heatmap (bottom right):

The heatmap sits in slight expansion territory, but the rate of change is accelerating into stronger expansion. This is the more constructive signal of the two. Short-term fair value is stretched, but the underlying proxy is gaining velocity in the long term, which can pull the fair-value envelope higher and validate current price action rather than punish it.

Synthesis:

Risk-On regime confirmed by macro breadth, but the setup is asymmetric: liquidity is accelerating (heatmap RoC) while price has already front-run short-term fair value. Two paths from here, either liquidity expansion catches up and ratifies the 1 to 2σ premium, or BTC mean-reverts toward the short-term fair-value midline while the macro tape stays constructive. China and M2 turning from red toward green would be the cleanest catalyst for the former.

15

368