112 Photos and videos

Ricardo Reis retweeted

Pleased to be in Bangkok for the IMFER Conference, co-hosted by @IMFNews and @BankofThailand. Looking forward to discussing how shifts in trade, investment, technology, and finance are reshaping the global economy and geoeconomic policymaking. imf.org/en/news/seminars/con…

1

7

24

14,122

Extremely proud of our fantastic @LSEEcon PhD student @AnanyaKotia for winning the Daniel Cohen Award!!!

🏆 PSE & @ENS_ULM are pleased to announce the #DanielCohenAward 2026 winner: @AnanyaKotia, PhD student @LSEEcon, for his Job Market Paper "When Competition Compels Change: Trade, Management, and Productivity". 🔗 shorturl.at/Dws8D?utm_source…

Funded by Boussard & Gavaudan and AFPSE

1

3

134

16,292

Ricardo Reis retweeted

Jun 9

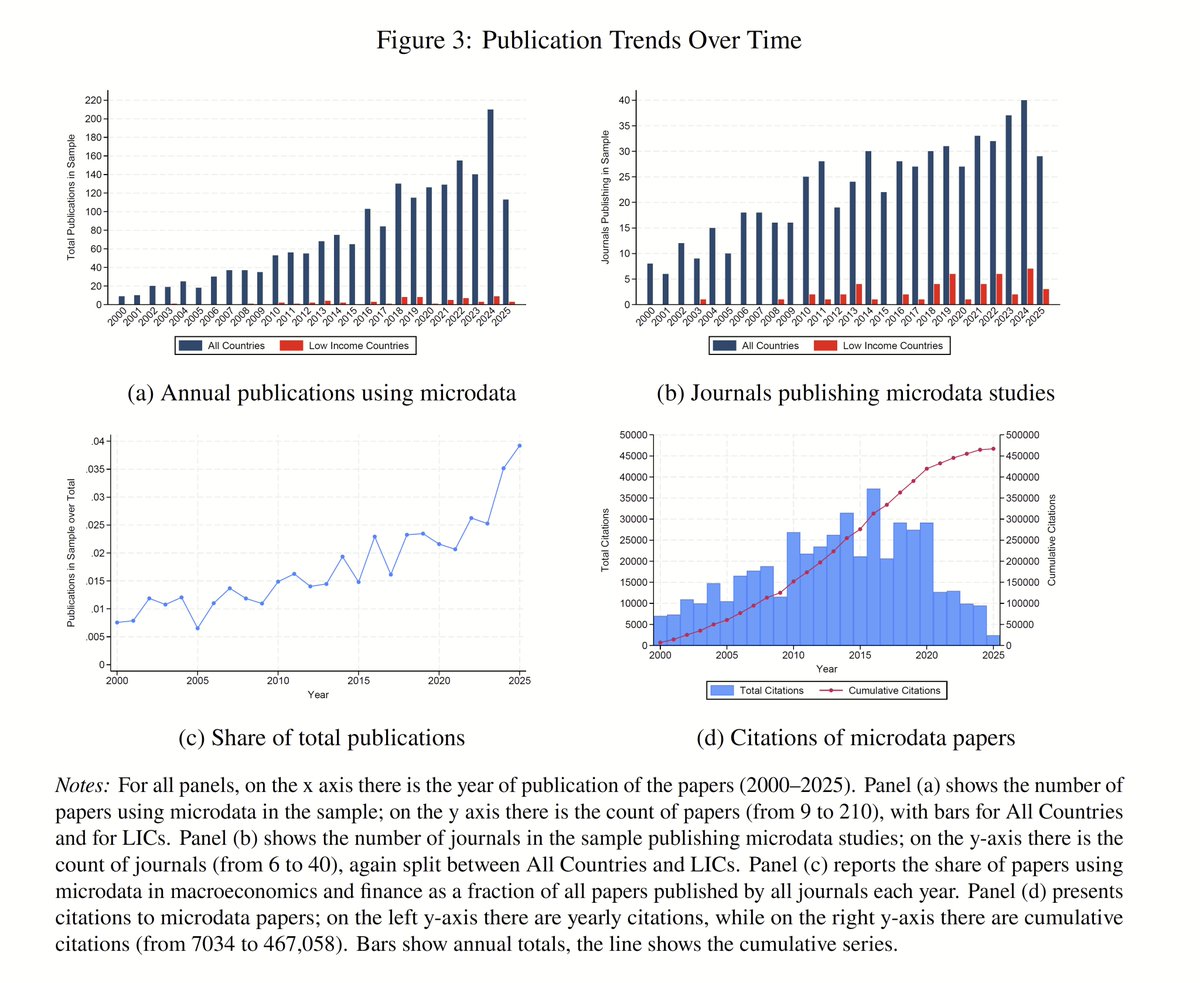

I typically do not post working papers. If anything, I prefer to write about published papers of mine (so rarely), or about the wonderful papers/colleagues from whom I learn so much (often about the #WEFIDEV network in #Finance & #Development).

But this one feels a little different.

"Microdata for Research in Macroeconomics and Finance" is a fun paper that I wrote along the way (@cepr_org DP link below), after @pogourinchas, #PetiaTopalova, and #NanLi from the @IMFNews reached out with the idea of taking stock of how microdata are changing research in macroeconomics and finance, stimulated by the excellent work of the @FCDOGovUK headed by @DennisNovy.

The central idea is simple: over the last two decades, economics & finance have been transformed by the growing availability of granular data (credit registries, firm balance sheets, digital payments, and more). These allow us to move beyond aggregate averages & ask sharper questions. Who is constrained? Which firms respond to policy? How do payment systems reshape economic activity? Where are market imperfections most binding? And more.

This matters everywhere, but especially in low-income countries, where importing policies from high-income settings can be misleading. Market frictions, informality, enforcement, institutional capacity, and financial infrastructure often differ in fundamental ways. Better policy requires understanding these mechanisms from the ground up.

In the paper, I construct a new dataset of more than 1,900 academic publications using nine types of microdata, drawn from the top 50 journals in economics and finance between 2000 and 2025. The dataset combines bibliometric work, LLM-processing, and human verification.

2

18

111

21,957

Ricardo Reis retweeted

Today @EconUCL has launched macromonitor.org/ -- a free, cutting edge, transparent and v frequently regularly updated tool for nowcasting UK GDP and CPI. Congrats to my colleagues on a great public good and thanks to @swatdhingraLSE for a great keynote! @UCLPolicyLab

1

12

51

6,959

Ricardo Reis retweeted

📢 New paper w/ @GregWKaplan 🧵1/10

How small is “small” for local-linear methods to deliver reliable answers in heterogeneous-agent models of fiscal stimulus?

Our answer: very small.

3

56

304

145,194

Ricardo Reis retweeted

May 31

.@paulkrugman has argued Europe is not suffering an economic decline relative to the United States using Purchasing Power Parities. In this post (a revision, without paywall, of our @ProSyn one on Friday), @Ph_Aghion @a_bergeaud and I explain why a chain of current purchasing power parity (PPP) indexes tells us nothing useful about productivity growth.

We make four points:

First, a PPP measures purchasing power across places at one moment; a deflator compares prices across time in one place. A sequence of current-PPP comparisons is not a measure of real growth, because the prices used to value output change from year to year.

Second, the two indexes need not agree. Difference the current-PPP comparison of France and the US across years and you recover the difference in their real growth plus a price residual. By 2024 the two are roughly 18 log points apart, enough to neutralize nearly all the measured growth divergence between France and America.

This is due to two reasons

Technology (our third point): where products improve fastest, as in information technology, the gap is largest. If a country doubles its computer output while the international price of computers halves, current PPP records no increase in value. (We all agree here.)

Fourth, the baskets. It is impossible to find a basket of products that is simultaneously representative within each country, comparable across countries, and stable through time. (A novel point in the discussion).

Convert GDP every year with a current PPP and French output per hour grows at a similar rate to the US. The match is built by the conversion. Nothing in it measures how much more either country produced.

Krugman has now answered to our column, in a post dated May 30. I think we are not that far. We agree that European productivity growth has trailed the US for three decades; a current-PPP chain and a national deflator answer different questions; and the weighting mechanism is part of the story. We disagree on one. Krugman reads the flat current-PPP line as evidence Europe is not falling behind; we see it as the product of moving the price measurement stick every year.

Finally, like @MESandbu on Friday in the @ft, @paulkrugman suggests as reductio ad absurdum that we should be willing to accept, if we believe our numbers, that the NL was way ahead of the US average in 2000 and declining ever since. We do not find the counter-example compelling. The counter example shows a clear decline of the Netherlands over a long period of time. That is the point!. Our claim (see my two Europes post):

1. Core Europe was very close to the US or higher 2 decades ago.

2. Every year since then we have seen much slower productivity growth. This has become particularly dire more recently.

3. This matters, particularly for our influence, our ability to sustain our welfare states, and our ability to pay for defense and other market goods.

siliconcontinent.com/p/the-m…

9

81

264

40,362

Ricardo Reis retweeted

May 15

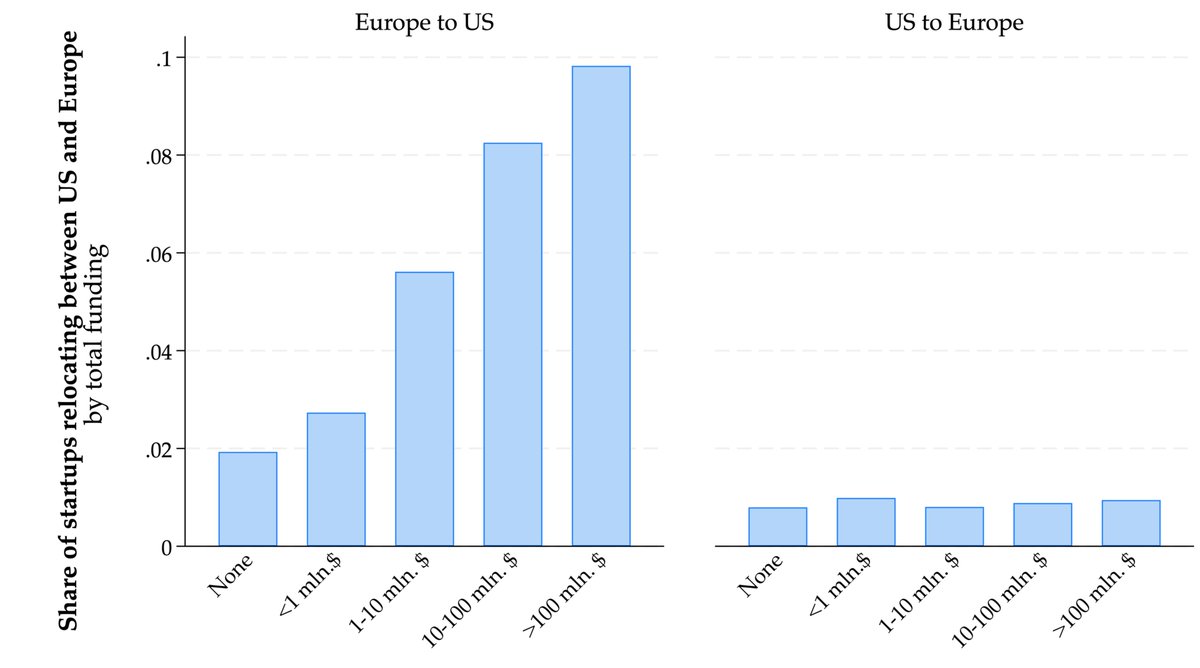

Which of the US or EU do economic agents choose to locate in?

Their choice reveals how they weigh all the factors that matter. The relevant agent for productivity and economic growth are firms. So, the migration rates of startups reveals the economy where you want to be to grow and succeed:

20

89

445

84,855

May 15

I am late to the debate on whether Europe's economy is behind the US. Many quotes on this tweet by @lugaricano propose looking at health, inequality, happiness surveys, beauty of landscapes, driving around, etc. But there is a *better* way. And economists have used it for decades...

May 12

We stopped everything to write an answer (link below) to Paul Krugman's two posts of today (one informal, one with a simple model) arguing that Europe is broadly not falling behind the United States.

The change measured by the Draghi report, he argues, is mostly due to growth in the technology industry, which has distorted GDP numbers without actually leading to higher standards of living. We should believe our eyes when we walk around France and walk around Mississippi.

Krugman is wrong. The measures he uses understate European stagnation. This matters enormously. Divergence with the United States is the strongest evidence for reform in Europe.

1. The growth numbers

Krugman compares the United States, France, and Germany at purchasing power parity in current prices. On that measure, France's and Germany's position relative to America has been roughly constant since 2000.

But current price comparisons miss productivity gains in sectors where prices fall. If America produces twice as much software while the price of each unit halves, the value of American software output looks unchanged even though the volume has doubled.

Most economists therefore use constant prices, which fix the base-year PPP level and apply each country's real output growth on top of it. American output growth has concentrated in tech, where prices have fallen tremendously as productivity rises. In terms of the volume of things produced, America has pulled away from Europe.

2. Is it all the tech industry?

Krugman concedes this tech divergence but says it is not welfare-relevant. The American growth lead is an accounting artefact of measuring more iPhones at base-year prices, not a sign that Americans are actually richer, because Europeans buy the same iPhones at the same world prices.

This is not the right way to think about the world today, as an earlier Paul Krugman would have argued.

His model assumes tradable goods, interchangeable workers, marginal-cost pricing, and no profits. Each assumption fails.

Most of what households buy is non-tradable: housing, healthcare, childcare, education. When American tech firms bid workers from haircutting to coding, American haircut wages rise. Germany has no growing tech sector to do the bidding, so German wages stay flat.

Technology is not priced at marginal cost. Apple's margins are around 40 percent. Anthropic's inference margins are at 70 percent. The major platforms enjoy network effects, switching costs, and lock-in that hold prices well above what a competitive market would deliver. A large share of the productivity gains in technology stays as profit.

A lot of the value of American technology dominance shows up in equity, not in wages. Apple, Microsoft, Nvidia, Alphabet, Meta, and Amazon together are worth $21 trillion, more than the entire combined stock market value of all European stock markets. Around 60 percent of US equity is held by American households. The median French or Spanish household holds almost no equity.

The median employee at Meta, a company with almost 80,000 employees, earned $388,000 in 2025.

This advantage is not going to go away. Krugman's own 1991 paper, cited in his Nobel prize, showed that comparative advantage in modern industries is produced by increasing returns to scale, specialized labor markets, supplier networks and the agglomeration of suppliers, workers, and ideas in particular places. Once an industry concentrates somewhere, the concentration is self-reinforcing. Europe is being pushed away from the next round of technology industries (AI!).

3. What about inequality?

Another retort is that GDP per capita hides substantial inequality, and so even if America is rich on average, this is mostly due to the super wealthy.

But despite the US's high pre-tax income inequality, it also achieves higher median incomes than Europe, in part because of such a high base, and in part because it actually redistributes more than many European countries.

The cleanest comparison is median equivalised disposable household income: income after cash taxes and transfers, adjusted for household size and purchasing power. According to the OECD's 2021 numbers, the median American earns 30 percent more than the median Dutchman, about 31 percent more than the median German, and about 52 percent more than the median Frenchman.

4. What about hours worked?

Krugman points out that while American GDP per person is higher, most of this is because Americans work more. For this divergence to be an hours worked story, Americans must work more relative to Europeans now than they did in 2000.

The opposite has happened. Birinci, Karabarbounis, and See in a 2026 NBER paper show that about half of the American-European hours gap that existed in the 1990s has reversed by the end of the 2010s. Americans work fewer hours per person than they did in 2000, while most Europeans work more.

5. Is America not a bad place to live?

Walk around Alabama and France: surely the former cannot be substantially richer than the latter?

American cities often have poorer centres and richer suburbs or exurbs. European cities preserve richer and more attractive historic cores. A visit to a city as a tourist in America compared with a city in France will leave one having seen different spots on the income distribution. Americans in Europe go to the nicest and richest European cities.

Rather than a walking around test, do a driving around test. Go to the periphery of any modern American city and see a level of new-built material wealth that is extremely uncommon in Europe, with thousands of enormous four- or five-bedroom homes. In the South, in places like Nashville and Austin, drive around the downtowns to see hundreds of luxury apartment buildings springing from the ground. This construction boom is replicated virtually nowhere in Europe today.

The other question is generational. Housing often costs more in Europe than in the United States, despite the quality of the housing stock generally being much better. Europe has nice city cores but these are inaccessible to young Europeans.

Consider the salaries available to entry-level workers. The starting pay for a London police officer is $57,000. In Washington, DC, $75,000. The entry-level Deloitte consultant job in Madrid pays around €28,000, roughly $33,000 per year. In Charlotte, the entry-level Deloitte job pays $63,000.

There are many things to dislike about life in America. But relative to 25 years ago, the gap in material wealth has shifted dramatically in America's favor.

siliconcontinent.com/p/europ…

8

21

189

72,524

May 15

Which of the US or EU do economic agents choose to locate in?

Their choice reveals how they weigh all the factors that matter. The relevant agent for productivity and economic growth are firms. So, the migration rates of startups reveals the economy where you want to be to grow and succeed:

20

89

445

84,855

May 11

Thursday (1:00 pm ET) there is a new episode of the @ClevelandFed’s Conversations on Central Banking, May 14. This time on "The Case for Central Bank Independence". Free and open to the public at this link: clefed.org/3QYkPio

8

33

3,160

Apr 7

Congratulations to @ludwigstraub for a well deserved honor. Read the prize description to learn about the exciting work he and others have been doing. The present and future of macroeconomic research is bright!

Congratulations to Ludwig Straub (@ludwigstraub) of @Harvard, winner of the 2026 John Bates Clark Medal! aeaweb.org/about-aea/honors-…

1

7

91

8,618

Apr 6

9) My written comments are here. These will appear in the Brookings Papers on Economic Activity @BrookingsInst.

personal.lse.ac.uk/reisr/pap…

1

1

10

3,511

Apr 6

10) For the full discussion, the video is available here:

youtube.com/live/HrTIj5h1N5I…

1

2

17

4,478

Apr 6

11/end) And for more academic in-depth discussions of this topic see:

x.com/R2Rsquared/status/1979…

17 Oct 2025

What happened since Wednesday in the US repo money markets? Why did banks have to borrow $15.1bn from the Fed's recent lending facility? Could we see this coming? What does it imply for QT?

(good clues in this thread...) [1/5]

ft.com/content/60663a88-6a86… via @ft

3

8

4,173

Apr 6

** Reducing the Fed's balance sheet **

Ten days ago, I was part of a discussion at @BrookingsInst on how to shrink the Fed's balance sheet with Darrell Duffie and @WenxinDu. I tried to lay out the discussion in terms that, hopefully, clarify it to a broader set of economists. Here are the main points: 🧵

2

57

220

27,211

Apr 6

8) "Stigma" is an expression used to explain why US banks leave money on the table and do not use some Fed standing facilities. To my ears, this is doublespeak for US supervisory failures and/or flaws in the design of those facilities. They can and should be corrected.

1

1

9

1,806

Apr 6

7) The elastic supply of money can be achieved by a standing repurchase facility open to banks, along the lines of the ones existing at the Bank of England or the ECB.

(Andrew Bailey laid out the reasons for this strategy at his @FMG_LSE Goodhart 2024 lecture)

bankofengland.co.uk/speech/2…

1

1

8

1,883

Apr 6

6) Keeping interest rates in money markets from becoming dangerously volatile while reducing the size of the balance sheet requires committing to an elastic supply of reserves.

(Isabel Schnabel has several speeches on this)

ecb.europa.eu/press/key/date…

1

8

1,693

Apr 6

5) Policies to reduce the balance sheet of the Fed are synonymous with policies that reduce the demand for bank reserves. You cannot do one without the other

(Lori Logan and Sam Schulhofer-Wohl @DallasFed have been making this point for a while.)

federalreserve.gov/monetaryp…

1

4

16

2,441

Apr 6

4) Less debatable, the Fed should aim to (i) stay close to the optimal supply of reserves (Friedman rule), and (ii) prevent a financial crisis in money markets as a result of spikes in demand for liquidity.

(See governor Stephen Miran's approach)

federalreserve.gov/econres/f…

1

1

10

2,003

Apr 6

3) But, today, the Fed wants to reduce the size of the balance sheet. There are pros and cons for this, but let us take the desire to shrink as given.

(The incoming chair Kevin Warsh gave some reasons for this goal).

hoover.org/sites/default/fil…

1

1

6

1,959

Apr 6

2) A simple answer to this shift in demand is to increase the inelastic supply of reserves. This is what we have done for the past 17 years.

(I wrote about the implications it has for monetary policy ten years ago at Jackson Hole.)

personal.lse.ac.uk/reisr/pap…

1

1

9

3,170