I trade stocks for a living and I’m damn good at it. Markets don’t scare me. Losses teach, wins build. I’m a full-time trader, but a full-time family man too.

Joined March 2015

- Tweets 82

- Following 13

- Followers 516

- Likes 183

11 Photos and videos

Pinned Tweet

Jan 28

Five years later and we’re still pretending January ’21 was just “volatility” and not a full-blown stress test that exposed how fragile (and how conflicted the plumbing of this market really is)

Vlad, you can publish all the polished retrospectives you want. Retail didn’t hallucinate the buy button disappearing. Liquidity didn’t magically evaporate for no reason. When brokers that sell order flow to the very firms taking the other side of customer trades run into “capital issues” at the exact moment their users are winning, people notice.

You can call it risk management. You can call it clearing requirements.

What it looked like was this: when the trade hurt the right institutions, the rules changed mid-game.

And let’s talk about narratives. For years, anyone questioning short interest reporting, fails-to-deliver, or off-exchange volume concentration got labeled a conspiracy theorist. Meanwhile, internalization keeps growing, price discovery keeps getting murkier, and somehow retail is supposed to believe the system is more fair than ever.

You don’t get to rewrite history just because time passed. Trust in markets is earned with transparency and aligned incentives, not PR campaigns and selective memory.

Retail learned a lot in 2021. About clearinghouses. About collateral. About who actually sits between them and “the market.” That knowledge doesn’t go away, and neither does the skepticism.

You can minimize it. You can joke about it. You can distance yourself from it.

But the bill for broken trust in financial markets always comes due in participation, in liquidity, and eventually in regulation. #GME #MarketTransparency #PowerToThePlayers

1

1

2

428

Ben Rickert retweeted

May 4

Proposal to acquire eBay.

investor.gamestop.com/ebay

1,612

3,558

16,426

2,127,107

Ben Rickert retweeted

10 Sep 2025

50

108

826

28,971

Ben Rickert retweeted

9 Sep 2025

not bad for a piece of crap retailer

2,083

3,655

16,074

940,101

Ben Rickert retweeted

28 Aug 2025

I've held 100k since .19 and never sold even during the offering panic plummet from $1.70 to $0.49. I know what i hold, and it's truw value will be proven in time. Don't give in to mindless short sellers and their dirty tactics. They will go broke trying to destroy the future.💰

2

1

7

1,593

28 Aug 2025

$IXHL is lining up catalyst after catalyst, and the momentum is undeniable.. The company has delivered back-to-back positive Phase 2 results, signaling real science behind their products. On top of that, they’ve authorized a $20M share repurchase program, something you almost NEVER see in a small-cap biotech, showing just how confident management is in the long-term value of their business. The technical setup is also strengthening by the day, with bears losing ground as the chart coils for a breakout. Looking ahead, the possibility of a Phase 3 partnership with ResMed could accelerate commercialization and validation even further, while their psychedelic program, PSX-001, sits in the same category as GM-2505, which AbbVie just valued at $1.2B. This isn’t your average penny biotech, it’s a company positioning itself as a serious pharma contender. The floor is rising, and the ceiling? Much, MUCH higher...

What makes $IXHL even more explosive is the setup behind the scenes: a low float, millions of shares already locked in dark pools, and shorts piling on at the worst possible time. Add in retail conviction and institutional eyes starting to watch, and you’ve got the recipe for a breakout that could melt faces. When fundamentals align with technical pressure like this, the move is never small. The question isn’t if IXHL runs, it’s how high it goes when the dam finally breaks and people start to catch on.

#IXHL #Biotech #StockMarket #StocksToWatch #SmallCapStocks #FDA #ClinicalTrials #Phase2 #Phase3 #HealthcareInnovation #Psychedelics #ShortSqueeze #LowFloat #DarkPoolData #MarketMomentum #BullishSetup #UndervaluedStocks #GrowthStocks #FuturePharma #BreakoutStocks

2

2

18

2,522

28 Aug 2025

$IXHL is no longer the “tiny penny stock” people thought it was. The Phase 2 results already proved the science, alongside patient reports, and Phase 3 is fully funded. On top of that, a $20M buyback has been authorized.. Management is signaling confidence while shorts scramble. The announcement of an actual buyback will easily push the needle past $1.

The real kicker? A potential partnership with ResMed. That could mean shared Phase 3 trial costs, faster commercialization, and instant validation from one of the biggest players in sleep health. IXHL is building toward billion-dollar pharma status with multiple shots on goal: OSA, anxiety, arthritis, and even psychedelics. We've seen their progress on the anxiety medication last week..

Shorts are betting retail folds, and many have taken the bait. But with capital in the bank, multiple billion-dollar candidates, and partnerships lining up, the math speaks for itself. This isn’t just a biotech story, it’s a setup for a generational squeeze. The long-term value is there and has been proven time after time again. This stock has MASSIVE potential, the facts speaks for itself. #IXHL #BiotechStocks #HealthcareInnovation #ClinicalTrials #FDAWatch #DrugDevelopment #MedicalBreakthrough #RickertReport

5

11

75

10,277

26 Aug 2025

Just when you thought $IXHL couldn’t deliver, PSX-001 pulls up and drops a 12.8-point HAM-A knockout. 44% response. 27% full remission. No safety flags. Phase 3 in sight, partners expected soon.

Once again… not hype. Just data.

#IXHL #BiotechBreakthrough #Biotech #RickertReport #Phase2Results #FDAWatch #BiotechStocks

4

12

52

6,529

26 Aug 2025

For context: Phase 2 enrolled 73 adults with GAD in a double-blind study:

⚪Avg HAM-A drop: -12.8 points vs -3.6 placebo (p<0.0001)

⚪44.1% saw ≥50% reduction

⚪27% achieved remission

⚪Zero serious adverse events

This isn’t a “what if” drug. It’s proving real, durable results!

2

748

22 Aug 2025

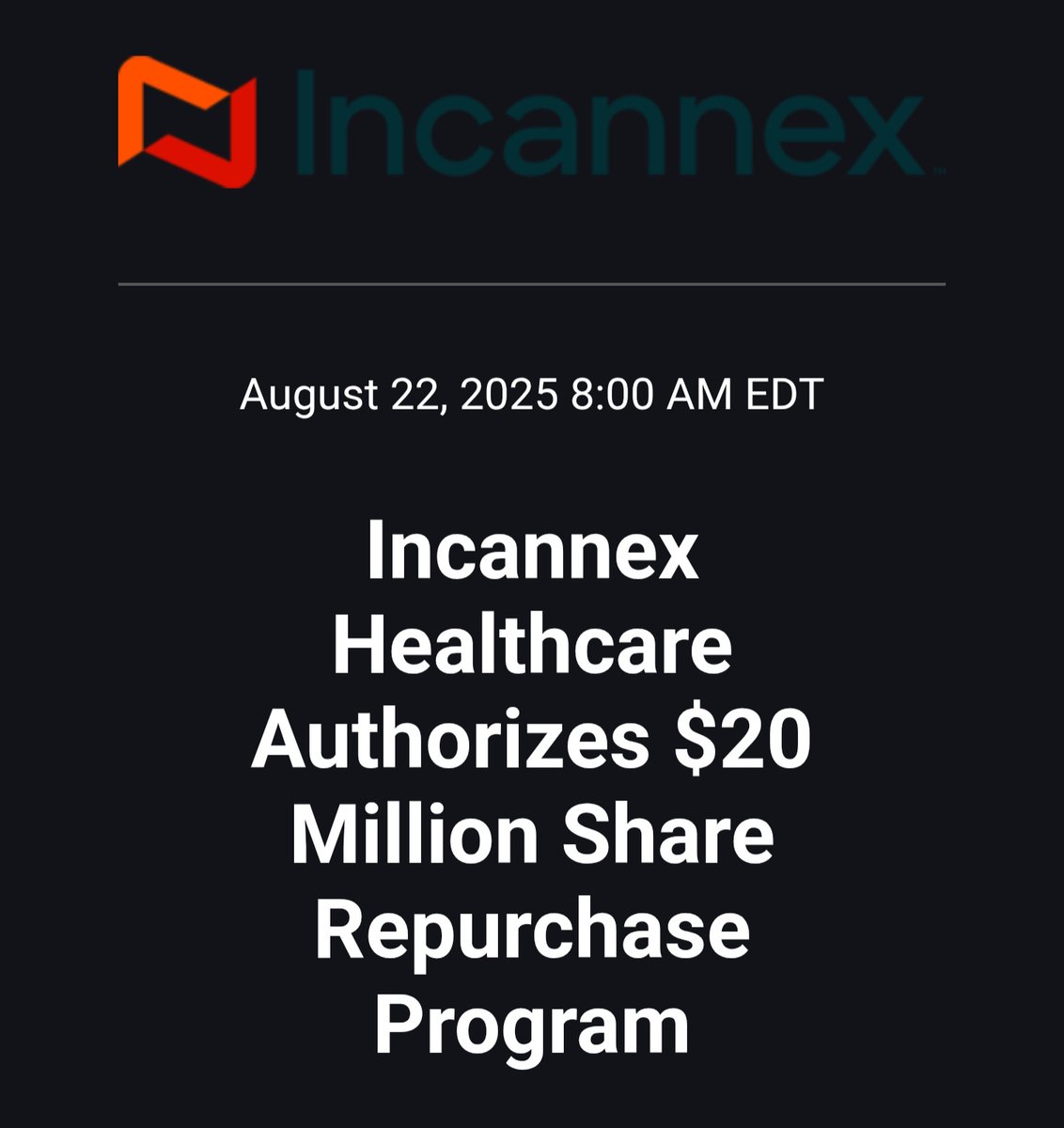

$IXHL just authorized a $20M buyback.

Let that sink in... management is literally BUYING SHARES BACK because Wall St. has this thing way undervalued.

Phase 2 ✅

Float cleaned up ✅

Short interest heavy ✅

Next stop: Phase 3 & beyond.

Retail runs this. Bullish #IXHL #BiotechStocks #FDA #Phase3 #Buyback #RickertReport

9

13

68

8,642

21 Aug 2025

Dark pools are drying up. Shorts are stuck recycling the same shares in a dead stall, with liquidity fading fast. Add T 13 pressure, a razor-thin float, and FDA news looming by end of August... We are in for a treat within the not too distant future. When this snaps, it won’t be a squeeze... it’ll be a reckoning. #IXHL #Biotech #FDACatalyst #ShortSqueeze #RickertReport

2

2

10

756

11 Aug 2025

Good morning. Phase 2 data came in strong, and institutional ownership sits at just 0.39%, making this a true retail battleground. Shorts remain positioned in a low float, betting we fold, but with a cleaned-up share structure and real science behind the move, the setup for a squeeze is building. #IXHL #Biotech #BiotechStocks #ShortSqueeze #LowFloat #RickertReport #Pennystock #PennystockPlay #Bullish

2

2

11

1,292

11 Aug 2025

For those asking about the squeeze math, low institutional presence means less resistance when retail steps in. Combine that with the short interest sitting on a small float, and every uptick forces more covers. We’ve seen how quickly these setups can move when momentum catches.

1

2

7

1,088

8 Aug 2025

As the days go by, #IXHL inches closer to FDA approval.

- Up to 83% AHI reduction in Phase 2

- Massive QoL improvements (sleep, fatigue, cognition)

- Zero serious side effects

- Targeting a $10B OSA market

- Real patients. Real impact. Real momentum.

The market’s waking up, and we’re just getting started.

#RickertReport #Biotech #SmallCapMonster #ClinicalData #SleepApneaTreatment #FDAWatch #BiotechStocks

2

4

16

1,933

8 Aug 2025

3

845

8 Aug 2025

Some of you were quick to say nothing was coming this Friday. But I didn’t make a wild guess. I had reason to be sure. The silence wasn’t empty, it was buildup. Now that it’s here, maybe next time you’ll think twice before doubting me. #IXHL #Biotech #RickertReport

6

3

15

1,211