☕️

Joined December 2012

- Tweets 4,855

- Following 149

- Followers 74

- Likes 2,192

242 Photos and videos

FIDEL SARAH retweeted

Jun 12

#Silver

We need to keep an eye on the trend lines. Ideally, we need to get back into the $72 range so that we can sound the all-clear in the short term. I’m almost fully invested and made 7.26% yesterday, but caution is still warranted for now.

Jun 10

And the #Gold/ #Silver ratio is holding its downward trendline. Sometimes it’s not the triangles you need to watch

4

6

25

3,530

FIDEL SARAH retweeted

Jun 12

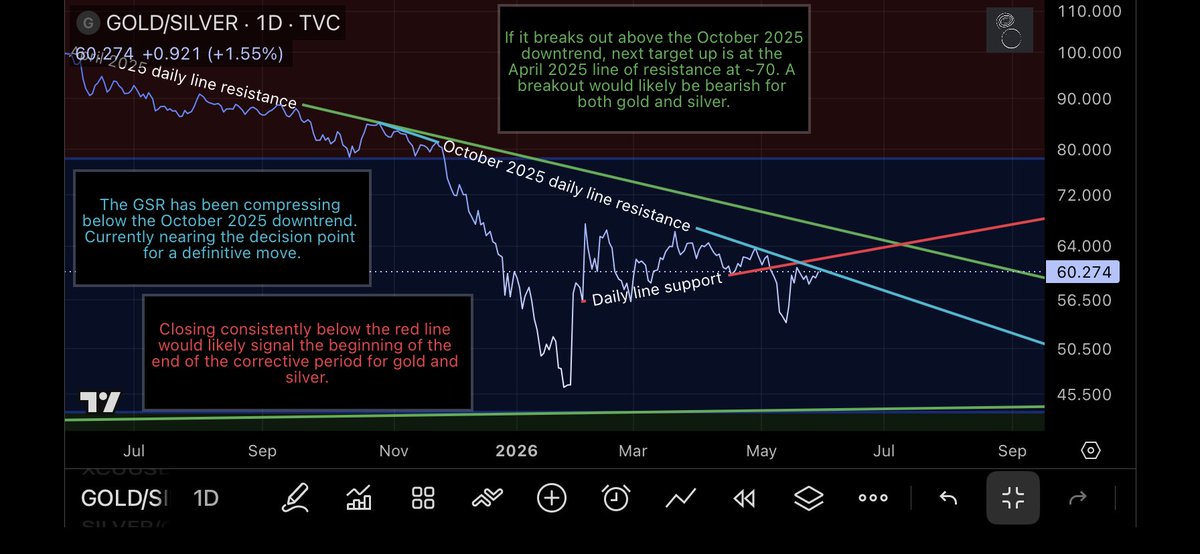

GOLD/SILVER🥇/🥈 — 62.4 — rejected April 2025 resistance — the spike to 65.8 made a lower high from the Feb 2 wick. Might have been the final flush.

Not to say it can’t continue to be choppy.

Need it stay below the green and red lines for this week’s close and go back below the light blue line next week 👀

🧘🏼♂️🥈🫡

May 30

GOLD/SILVER 🥇/🥈 — back at 60 — believe it or not the GSR is still in a downtrend 📉

Still closing below the October 2025 downtrend and the red daily line support that broke down on May 6th.

The beginning of the end of the correction has begun.

Take a look 🔍👀👇👇

For the good of the order 🫡

3

5

66

7,596

RT @manerhushi123: Silver swing long ✅

Buy #silver here at 65$ -66$ range

Target:- 84$-88$

Timeframe:- 15-20 days

6

8

FIDEL SARAH retweeted

$XAUUSD BUY Signal 📈

Entry: 4315-4310

Stop Loss: Below 4290

Targets: 4340 • 4380 • 4420🎯

Strong Bullish Reversal Expected From Order Block FVG Zone ⚡

Trade Smart & Manage Risk ⚠️

Stay Tuned For Updates. 🚀

12

6

31

6,581

FIDEL SARAH retweeted

May 22

Act like you already have it, and soon, you will.

208

4,943

30,387

401,018

FIDEL SARAH retweeted

May 22

Please get addicted to thinking positively in your life

214

4,329

22,979

357,473

May 13

RT @manerhushi123: Positional #silver short between 89$ to 90$ range

Target:- 76$ - 62$

Stoploss:- 96$

9

Was not expecting another push higher today but looks like $SILVER might be coming down for that 4hr low. Connecting the 1hr cycle high-low-high look where the fork lines up! Also interesting how yesterdays lows are exactly at .382 from todays top...

5

3

52

5,620

FIDEL SARAH retweeted

May 6

Hammer the basics of kettlebell training with this workout.

The most versatile piece of fitness equipment to get you strong, athletic, and fit just in time for summer.

Kettlebellworkout.com for Programs.

#kettlebell #fitness #summer

2

37

443

29,715

FIDEL SARAH retweeted

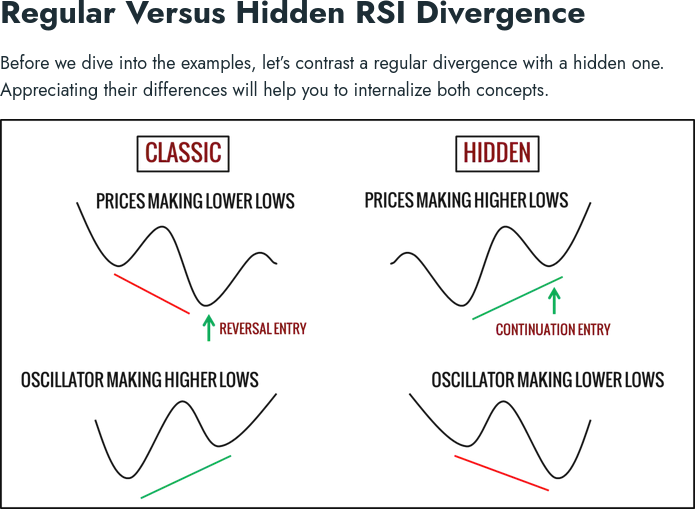

Most traders reach for RSI when they need an oscillator filter. I ran 4.5 million tests to see if that is actually right.

It is not.

RSI hit a 50% recommendation rate across our test set - 1,000 strategies, 1,000 market conditions. Good enough to use, not great, not robust.

CCI hit 100%.

The condition that made the difference was not the standard CCI above or below zero. It was this: take the highest CCI value over the last N bars. If that value is above 100, meaning the market touched momentum territory recently, even once - that is your filter.

Period 30. Lookback 12 bars. Average trade improved by 65% across 650 strategies. Maximum drawdown cut from $40,000 to $30,000. Bounce index- the percentage of losing strategies that recovered up 60%.

The optimization map showed consistent green across almost every parameter combination we tested. You can pick almost any value within the valid range and you are not overfitting.

I have 110% confidence in this filter because I did not test it on one strategy. I tested it across 1,000 strategies and 1,000 market conditions.

RSI: 50%. CCI: 100%. 4.5 million iterations.

12

20

157

17,745