A system dynamicist specializing it's application for Macroeconomic Forecasting.

Joined February 2022

- Tweets 18,376

- Following 230

- Followers 12,729

- Likes 20,878

2,776 Photos and videos

Pinned Tweet

"Teach a parrot the terms 'supply and demand' and you've got an economist."

-Thomas Carlyle

38

369

2,487

63,721

Free markets don't create prosperity by themselves. Profits, investment, wages, credit, and institutions do the heavy lifting.

4

6

32

687

You don't save first and then create investment. In a modern monetary economy, investment comes first.

Firms invest when they expect sales and profits. Banks create credit to finance that investment, generating new deposits in the process. The act of lending creates the purchasing power that makes production possible.

Savings are not a pool of money waiting to be lent out. At the aggregate level, savings largely emerge as a result of investment and income creation. One person's spending becomes another person's income, and income generates saving.

Interest rates do not coordinate a fixed supply of savings with a demand for investment. Investment depends primarily on expectations, profitability, demand conditions, and access to credit. A low interest rate can help, but it cannot make firms invest when they see no customers.

Modern banking does not transfer existing savings from patient households to ambitious entrepreneurs. Banks create deposits when they make loans. The constraint is not prior saving, but creditworthiness, profitability, regulation, and the willingness of banks to lend.

Economic downturns occur not because people consume too much and save too little. They occur when profits weaken, debt burdens rise, expectations deteriorate, and investment slows. What looks like excessive consumption is often the consequence of an economy attempting to maintain demand in the face of insufficient income growth.

The challenge for a capitalist economy is not encouraging more abstinence and delayed gratification. It is maintaining sufficient demand, productive investment, financial stability, and income growth to keep resources fully employed without generating unsustainable debt dynamics.

6

21

50

2,178

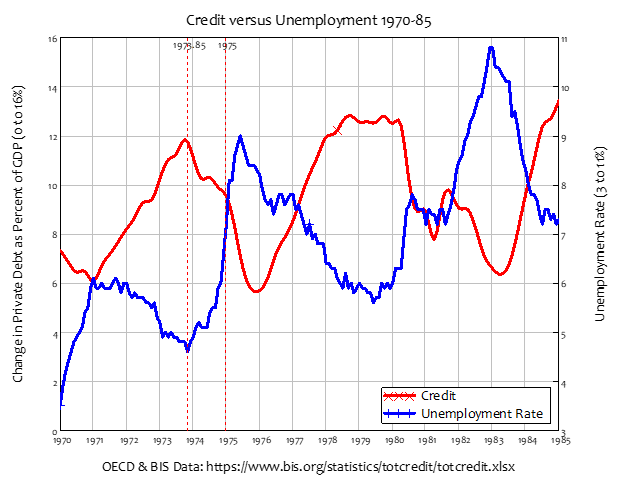

The post-Keynesian growth cycle doesn't begin with central banks distorting a mythical natural interest rate. It begins with the normal functioning of capitalism itself.

Businesses invest because they expect profits. Investment creates income, income creates demand, and demand encourages further investment. Growth feeds on itself.

As the expansion continues, unemployment falls and labor markets tighten. Workers gain bargaining power. Wages begin rising faster as firms compete for scarce labor.

Higher wages are not a distortion. They are a predictable consequence of successful growth. But rising wages can compress profit margins. As profits come under pressure, firms become more cautious. Investment slows.

At the same time, businesses and households often turn to debt to maintain growth. Banks are eager to lend because recent success makes risk appear low. Credit expands, asset prices rise, and optimism becomes self-reinforcing.

The longer stability persists, the more fragile the system becomes.

What began as productive investment gradually shifts toward speculation. Rising debt commitments require continued growth to remain sustainable. The economy becomes increasingly dependent on expectations that cannot all be fulfilled.

Then reality intervenes. A slowdown in profits, rising debt burdens, falling asset prices, or declining investment can trigger a wave of deleveraging. Spending falls. Layoffs begin. Income declines. The boom turns into a bust.

The crisis was not caused by an external distortion imposed on an otherwise stable system.

The boom itself created the conditions for the bust.

This was the insight of Richard Goodwin. It was the insight of Hyman Minsky and formalized by @ProfSteveKeen Cycles emerge from the interaction of wages, profits, investment, employment, and debt.

Capitalism does not require policy mistakes to become unstable.

Its internal dynamics are often enough.

7

46

149

6,213

Relearning Economics retweeted

Concern about wealth inequality is not about jealousy over some guy having a bigger house.

It is more about the fact that it may be a problem that one person has more economic power than entire countries.

19

49

142

6,014

The idea that prosperity emerges simply by removing rules and barriers assumes that markets naturally organize themselves into efficient outcomes.

Every successful market economy relies on a framework of institutions. Property rights, contract enforcement, accounting standards, banking regulation, product standards, professional certification, and consumer protection laws all shape how markets operate. None of these arise automatically from voluntary exchange alone.

This does not mean every regulation is good. Many are outdated, inefficient, or captured by special interests. But the existence of bad regulations is not evidence against regulation itself any more than the existence of bad businesses is evidence against markets.

The relevant question is always institutional design. Which rules enhance competition, transparency, and productive activity? Which rules merely protect incumbents? Which rules create trust and reduce uncertainty?

Reducing every discussion to government versus markets misses the point. Markets are themselves institutional creations. The debate is about what kinds of institutions produce the best outcomes, not whether institutions should exist at all.

10

37

82

2,706

Relearning Economics retweeted

Jun 13

Australia’s housing obsession is one of its greatest weaknesses.

Rising house prices are not a sign of prosperity.

What they actually tell you is that more money is being borrowed from the banking sector to buy homes.

The cause of rising house prices is rising household debt, and that is unproductive.

House prices are now five times more expensive than consumer goods compared to 1970. We should never have allowed that to happen.

Housing should not be an asset.

It is not something you should profit out of. It is something you should live in.

The people who really benefit from rising house prices are real estate agents and property developers, not the families who live in them.

We are paupers living inside castles. Paying a fortune on the mortgage, a fortune on private schools, and out of the remainder, just trying to live.

For the more information, check out the comment section,

#SteveKeen #AustraliaProperty #HousingCrisis #MortgageDebt #Economics #HousingAffordability

113

300

1,029

54,418

The fantasy isn't that the state creates markets. The fantasy is believing modern markets could exist without states, courts, contracts, property law, infrastructure, and money. History says otherwise.

25

48

153

14,601

Relearning Economics retweeted

Jun 12

Very interesting conversation

Building real-world economics

@ProfSteveKeen joined Katy Shields katyrshields.com/

youtu.be/nsIC2SUa2Nk?si=YVPb… via @YouTube

1

5

4

1,056

Relearning Economics retweeted

Jun 12

The biggest market crashes and recessions come from collapsing fiscal impulse (surpluses).

The reason is simple: govt spending = financial assets for the private sector, this fuels the business cycle.

Fiscal is getting dangerously weak here!

21

35

126

10,630

The strangest criticism of Keynesian economics is the claim that government spending cannot create wealth because it only redistributes existing money.

By that logic, no investment creates wealth. Building a factory merely redistributes money to construction workers. Hiring engineers merely redistributes money to engineers.

The point is not the money. The point is what the money mobilizes.

When an economy has unemployed workers, idle factories, and unused resources, the problem is not a lack of productive capacity. The problem is a lack of spending to activate that capacity.

A dollar spent hiring an unemployed worker does not simply transfer income. It increases output. The worker now produces goods and services that did not exist before.

Wealth is not money. Wealth is production.

28

79

218

8,896

"The subjects of every state ought to contribute towards the support of the government, as nearly as possible, in proportion to their respective abilities; that is, in proportion to the revenue which they respectively enjoy under the protection of the state."

-Adam Smith

10

19

47

7,200

Going live in 30 minutes to discuss Thursday's ECB rate hikes with @ProfSteveKeen

youtube.com/live/QrkdGJvcWdU…

2

13

1,799

"I began to read Capital, just as one reads any book, to see what was in it; I found a great deal that neither its followers nor its opponents had prepared me to expect."

-Joan Robinson

5

22

106

4,544

Relearning Economics retweeted

24 Nov 2025

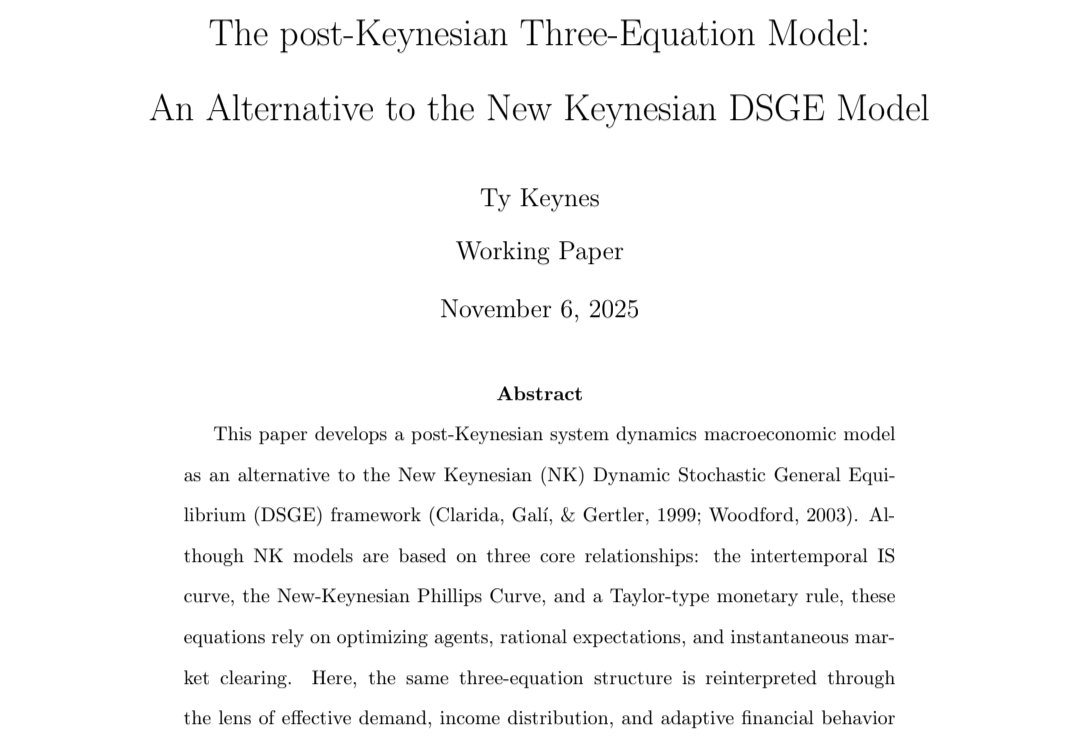

🚨 My new working paper out today

I propose a post-Keynesian, system-dynamics alternative to the New Keynesian DSGE model, one that produces business cycles and financial instability endogenously, without rational expectations or microfoundations.

dx.doi.org/10.2139/ssrn.5713…

🧵1/8

25

62

230

26,903

"Of all classes the rich are the most noticed and the least studied."

-John Kenneth Galbraith

5

25

84

3,480

"Governments and central banks were quietly admitting something they were still reluctant to announce publicly: the extraordinary power of private-sector banks lending to determine the pace of money creation, and therefore economic growth."

-Mariana Mazzucato

6

43

111

6,064

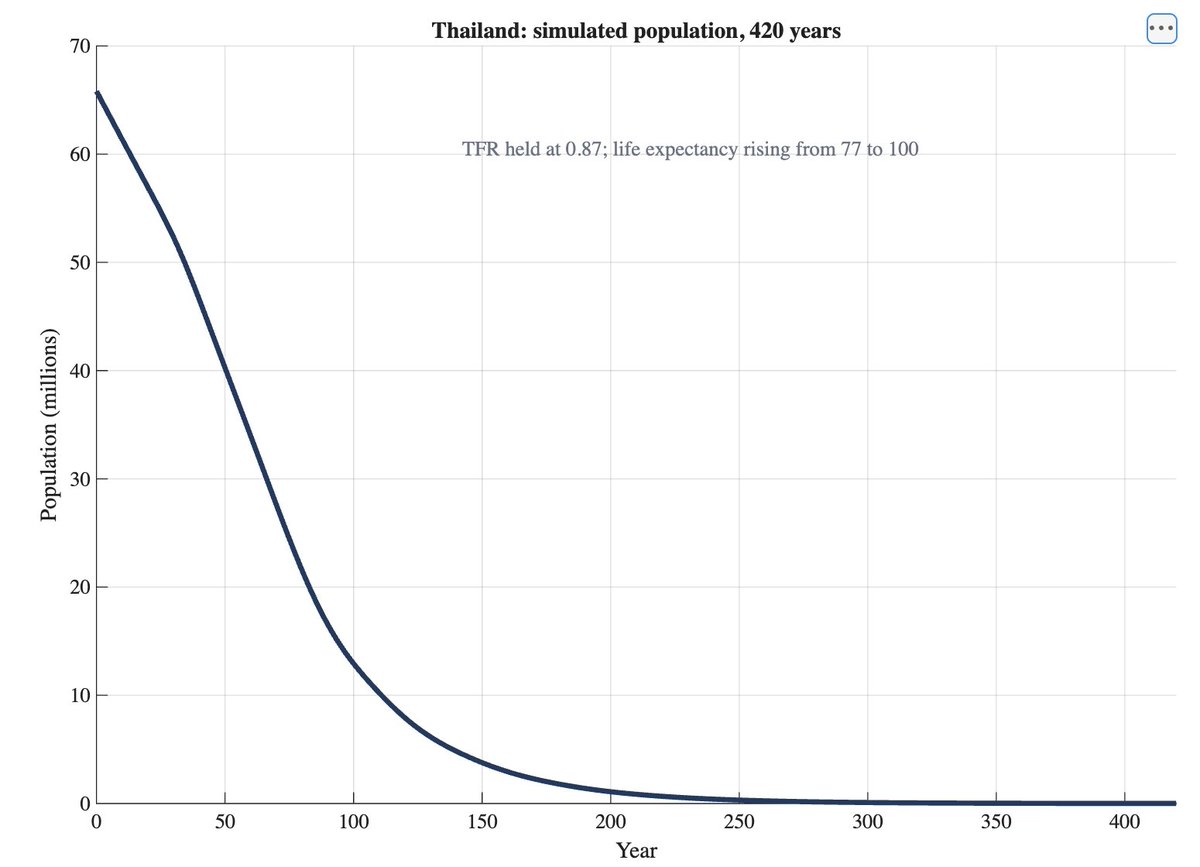

"God" playing "Limits to Growth" without a model.

A closed human population needs about 500 women of reproductive age (15-45) to remain biologically viable in the medium run. That number is not what drives a population to zero: sub-replacement fertility does that on its own. The 500-floor mark is the point of no return: the size below which the gene pool is too narrow to recover, even if fertility later bounces back.

In a hypothetical scenario where Thailand maintains its total fertility rate (TFR) at the 2025 level of 0.87 and has no immigration, its population of women of reproductive age would fall below 500, entering the extinction-risk zone, around the year 2445.

We can play with the numbers a bit (extending the fertile-age window, for example, or lowering the floor through medical advances), but the message holds. Any population that remains below replacement eventually goes extinct.

I make this point because when I write statements of the form “with its current TFR, country A will have a population of X in the year 2200,” I hear the reply “we can live with that.” That reply misreads the year-2200 population as a new stationary point. No, it is just a snapshot of a population still in decline. Sub-replacement fertility has no resting place above zero.

Now, one can legitimately argue that as the population falls, the TFR will rise again, perhaps due to cheaper housing or the selection of groups with higher fertility. (The “more natural resources per capita” story I trust least: the demographic transition broke the old Malthusian link between abundance and fertility, so in modern conditions the sign runs the other way.) These are possible mechanisms, and we can discuss another day whether, given the current evidence, they will be enough to get back to replacement (my two cents: I have run some quantitative simulations, and the answer is likely “no”).

I only want to force everyone to accept the realities of demographic accounting. If you tell me “we can live with that,” you are asking me to buy two separate claims: 1) that we can go from population X to 0.05X without a major social breakdown, and 2) that we will not only avoid that breakdown but also bring the TFR back to replacement by the time we reach 0.05X.

1

3

17

1,385

Relearning Economics retweeted

Jun 10

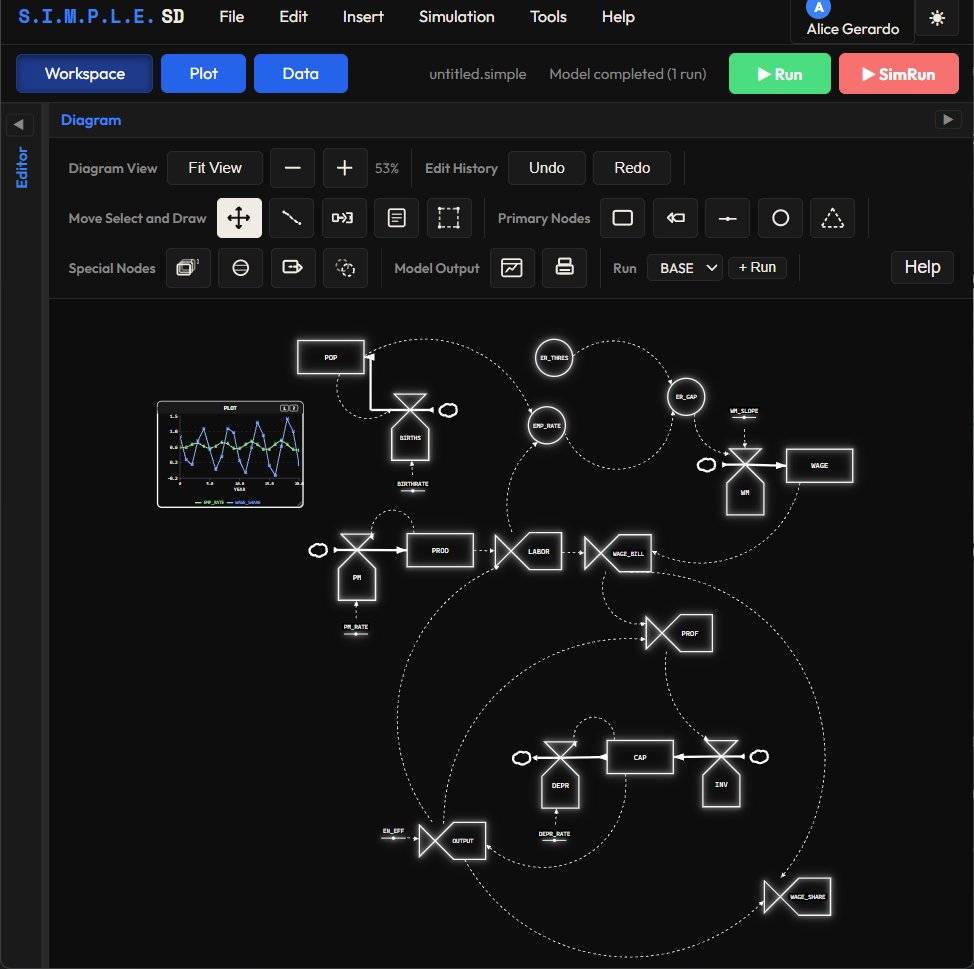

Just constructed the Goodwin model with @RelearningEcon's S.I.M.P.L.E. SD system dynamic web browser tool. It was interesting to learn the old DYNAMO code that system dynamicists used in the early days, before the use of personal computers. One can say it is quite simple to code.

1

6

355

"By what modus operandi does credit restriction attain this result? In no other way than by the deliberate intensification of unemployment."

-John Maynard Keynes

3

33

98

5,686

"Generally speaking, changes in the prices of finished goods are cost determined while changes in the prices of raw materials inclusive of primary foodstuffs are demand determined."

-Michał Kalecki

6

27

121

5,078