Providing my thoughts and commentary on things. It's not financial advice. Don't follow me. Do your own due diligence. Have a good day!

Joined April 2024

- Tweets 1,591

- Following 176

- Followers 230

- Likes 1,382

63 Photos and videos

Pinned Tweet

26 Jan 2025

$HSI $FXI $KWEB For those who have seen my posts regarding China related names in the past, it should be no surprise that I am currently bullish on China related names. From a big picture perspective, I believe that it is possible that we see a period during Trump’s presidency in the US, perhaps a 2 to 4 year period, where China related names can perform well. But nothing is guaranteed and I am keeping mindful that whatever bull case can be made for China related names could become invalidated. Potentially overnight. This is where my China thesis stands as of today:

To begin with, I believe that when looking at China related names, you first need to look at China from a political and geo-political perspective. It is important to keep in mind that China has certain long term strategic aims they want to accomplish. One of which is the issue of Taiwan. It should be no secret to anyone as to how important the issue of Taiwan is to China both politically and geo-politically. To this end, they have and continue to offer both the carrot and stick as possible paths regarding Taiwan. And the stick is where the intersection between economic and military issues intertwines.

The carrot is a peaceful political settlement to the issue of Taiwan. The stick is the forceful path via military force. To support the possibility of the stick in political and geo-political matters regarding Taiwan, China needs the economy to support a large and sufficient military strong enough to present a credible threat.

To present a credible threat, China must continue building up its naval and aerial capability. This necessitates a buildup in armament, equipment, skilled personnel, logistics and all the necessary requirements to maintain it all on an ongoing basis. China is not winning a sea and land invasion of Taiwan by sheer mass of infantry. And this is a process that is accomplished on a time span measured in years.

If China does not get its economic problems under control and its economic problems spirals into economic disaster, then this would present a serious threat to China’s military ambitions. If China must reduce and cut military expenditures due to economic problems, then this would cause large problems in China’s military calculus, to China’s stick regarding matters of Taiwan.

Which is why Trump returning to the presidency presents both a potential opportunity and danger to China. Trump presents an opportunity for China to reset relations to something more reconciliatory but also a danger in further breakdown of China and US relations. China’s economic problems such as its deflation and domestic consumption issues are no secret to anyone. And should the US and China get into a serious trade and tariff war, this would threaten China’s export reliant economy. And there would also be other negative repercussions such as the negative impact on sentiment within China about their economy.

China can look to history to know what could happen to their economy if things go wrong. It's not like their isn't plenty of examples like Japan's lost decades, the US great depression in the 1930s, etc. It will be hard for China to talk tough on the issue of things like Taiwan reunification over the coming years when they may have to cut back on military spending and make budget cuts on their military because they can't afford it due to an economy spiraling down the drain.

Which is why I believe that China is currently not in a strong enough position relative to the US to play hard ball. In the short term, I believe that China may be highly interested in putting issues of Taiwan and other international issues on the back burner to focus on more important domestic matters. I think the bottom line is that both China/Xi and the US/Trump have important domestic agendas which they want to focus on. Aside from posturing, I doubt either of them want to become embroiled in serious international distractions. I think they may put on a show but it may turn out to be business as usual aside from some Trump styling. Also, China doesn't seem to have much wiggle room here. I doubt Xi and China are in a position where they can feel confident in playing brinkmanship with their economy. In my opinion, fears and concerns regarding a potential trade and tariff war between the US and China may be overblown.

So if China/Xi can strike a deal with the US/Trump, and possibly reset US and China’s relations in the short term to something more reconciliatory, then this would be a positive tailwind to China’s economy. And may potentially signal an inflection point in US and China relations in the short term, possibly for as long as Trump is US president.

Also, if you look at things from the US perspective, if you look at the current situation, while China has been in a period of deflation, the US has been in a period of inflation. And with China exporting their deflation through their exports, it would be tough for the US to give up this a positive disinflationary tailwind that has been helping the US solve its inflation problem.

The seriousness of China’s economic problems should be emphasized by the fiscal and monetary stimulus that China is doing. China itself made the largest change in monetary policy stance for the first time since the 2008 Great Financial Crisis indicating that they are easing monetary policy. I believe that China will follow through on the fiscal and monetary stimulus that they’ve stated they will do to rescue their economy.

Moreover, if you look at the moves China has been making so far, China has been hinting at its possible intentions. The moves that China has made regarding its stock market has caught my eye. The wealth effect that China’s property market generated is gone since China’s property market burst. I believe that China is highly interested in utilizing their stock market to replace their property market in generating this wealth effect.

The US is an example of how when a property market bubble bursts, it takes a long time for it to recover. And it most likely won’t return to anything resembling how it was before the bubble burst for possibly many years. So whatever wealth effect generated by this, in terms of sentiment and domestic spending, is essentially gone and not coming back for the time being.

Yet, the US also an example of how a stock market creates a wealth effect. If the Hang Seng and the other China indexes are able to produce back to back years of return for their domestic investors, this may go quite a way to generating a possible wealth effect within China which may positively impact China’s domestic consumption problem.

If we look at the latest moves that China has made, they expanded their pilot private pension program, their 401K/IRA equivalent, nationwide to their populace. They also changed policy and allowed for their own stock market index funds to be added to them. And they have now stated that their insurers are to invest a certain amount of their premiums into their stock market on an annual basis. And we will see what else China may do in the future. Also, If China can get the ball rolling in improving the fortunes of their stock market, their stock market may keep rolling in a positive manner all on its own without further time and resources on China’s part. And there are numerous other benefits in having a healthy stock market in terms of business sentiment, raising of capital, job creation, and more.

Moving forward, China seems highly incentivized in making sure that their stock market does well. If their entire nation become invested in their own stock market index funds through their private pension system and other means, then logically speaking China is going to be very invested in making sure that their own stock market does well. Because of this, we may also see a more friendly tone from China towards foreign investors and capital which would also help with stabilizing the situation regarding foreign investors and capital fleeing from China.

But there are many variables to consider regarding China. Some of note are the relative strengths of the Yuan and US Dollar currencies to each other, US and China bond yields, and critical matter of technology to both the US and China.

With the Bank of Japan raising interest rates recently this past month, January 2025, along with possible further rate hikes to come, it seems that an inflection point of the relative strength of the Yen, Yuan, and other currencies against the US dollar may have happened. And if Asian currencies like the Yen and Yuan have indeed hit an inflection point where they strength against the US dollar, this may provide tailwinds to asset prices in Japan and China.

Moreover, if China’s bond yields revert higher after having fallen immensely, there is a question of where this money within China goes. If some of this money goes to China’s stock, then this may also provide tailwinds to asset prices in China.

Furthermore, as we have seen in recent days, Deep Seek has also been making waves and has gotten big attention. But whether this will be positive or negative regarding China large cap and tech stocks remains to be seen. This could get more attention to China large cap and tech stocks both domestically within China and internationally with foreign investors in the US and around the world. But it could also negatively impact US and China relations as a possible “technology war” could be a concern.

Despite being currently bullish on China in the short term for possibly the next 2 to 4 years during the time of Trump’s administration in the US, I am still skeptical of China being truly investable on a real multi-year, multi-decade, time frame.

There are real reasons why China related names have underperformed over the past years and decades. One of which is the way that China structures the ADRs of its various publicly listed business entities in the US stock market. There is real and legitimate risk and concern regarding how the ADRs are structured. But the structure of the ADRs is just one part of it. There are many good reasons why the US stock market has outperformed the rest of the world over the past several decades while other developed and emerging markets have underperformed relative to the US. And going direct to the Hong Kong exchange to bypass the ADRs doesn't resolve key issues. One of which is how China may or may not treat foreign investors over a long span of time depending on how things go in the world over the coming years and decades. Which is why as we have seen in the past high volatility in China related names to the up and downside where China related names haven’t gone anywhere.

I think the market, and the market participants within it, have moved and will continue to move on China related names based on how "investable" or "uninvestable" they are in certain time periods. In my opinion, the biggest issue facing China names right now is market sentiment. Everyone knows that China is mosty likely going to engage in fiscal and monetary simulus. Everyone knows what the theoretical valuations are of China’s publicly listed business entities in the US stock market. And I say theoretical because of how China structures the ADRs for foreign investors. The market knows what the cash flows are, the PE ratios, whatever multiples you want to use to value China related names.

Yet, I can see a possible scenario where China will play nice and play ball in the short term over say the next 2 to 4 years. They need to resolve serious domestic issues. But regardless of how China related names perform in the short term, the fundamental and structural issues in investing in China for the long term may continue to persist. Though this may change over time. For example, the political and geo-political issues with Taiwan will remain a lingering issue but this as well as other issues may get resolved.

I also expect things to be highly volatile. Things can literally change overnight, even if it may be from a single post on X as we have seen in the past with Trump. I am uncertain if China can be truly be “investable” over the long span of years and decades. But Trump may mark a short term shift where China does becomes "investable" again.

China becoming “investable” again is a contrarian idea in my opinion. Market sentiment in China related names has been terrible looking at the recent past few years. The idea that there may be a rotation into US small and mid caps has been said repeatedly in recent years. It's a common idea. In contrast, China related names have been considered "uninvestable" and for good reasons in the past. But if events unfold such that China related names go from "uninvestable" to "investable", then I can see a scenario unfold where they can perform well. I think a scenario can unfold where we see a rotation go from US large cap and tech to China large cap and tech in contrast to the idea that the rotation goes from US large cap and tech to US small and mid cap. The theoretical valuations in China large cap and tech are compelling. And they offer some of the only reasonable competition to US large cap and tech when thinking on a global perspective. Perhaps the rotation to US small and mid caps gets put on the back burner for some time as money flows from market participants goes to China related names.

If you look at the timeline of events with China/Xi and the US/Trump regarding trade and tariffs, things have progressed to a more positive place so far. The situation has gone from trade and tariff rhetoric to words of reconciliation. We have seen Trump extend Xi an invitation to his inauguration and while Xi himself didn’t go, he did send a high-level representative Vice President Han Zheng who met with Vice President JD Vance. Moreover, Xi and Trump have spoken over the phone. And it seems that things have gone well so far. Now, the Wall Street Journal has reported recently that Trump is interested in making a trip to China as a big item in his list of things to do sooner rather than later.

With Trump having put out a proposal for a 10% China tariff to take effect February 1st, the ball is in China’s court. With the Chinese New Year fast approaching in China, in my opinion, China/Xi may be highly interested in maintaining positive sentiment through and past the Chinese New Year. One thing which I am watching out for, is if China may be able to convince Trump to delay the 10% China tariff to a later time to give time for more substantial talks and negotiation. In recent days, Trump himself has said he does not want to put tariffs on China. In my opinion, it would make sense if some deal could be reached to at least delay the matter if Trump does follow through on making a visit to China in the future.

If what Trump said during the 2025 World Economic Forum this past month is true, if Xi initiated the phone call with Trump rather than Trump with Xi, then that's a very interesting detail in my opinion. It may signal the willingness of China/Xi to strike a deal. Also, Trump may be receptive to delaying the 10% China tariff in exchange for potentially some minor concessions which would allow him to present a win to his domestic audiences.

Finally, it does seem that market participants within the US may be offsides for China related names if they move higher. For example, there does seem to be notable short interest on China related names. And it seems to me that market sentiment is terrible for China related names.

Despite all this, I am keeping mindful that whatever bull case can be made for China related names in the short term could become invalidated, potentially overnight. I may also be wrong. Nothing is guaranteed. But I have been encouraged by what I have been seeing so far. We will just have to see what actually happens in the future.

3

10

4,215

$ORBS has a partnership with Futurum Group to develop a trust and authentication platform that was said to start beta testing in Q2 2026 per their PR earlier this year. Perhaps the CEO's Form 4 filing today was in relation to this. We'll see what happens. prnewswire.com/news-releases…

1

1

5

414

$ORBS One reason why this insider buying is notable is that the company has been issuing shares to raise cash on the balance sheet these past several months. The CEO buying on the open market may indicate that the company may be done, or mostly done, with the share issuance.

1

8

1,089

$ORBS This kind of insider buying is what I wanted to see. Perhaps the CEO was trying to time a buy for possible OpenAI IPO hype due to the SpaceX IPO. But maybe he is making this buy due to insider info we don't have yet that he does have. So we'll see what happens.

1

5

349

$ORBS The CEO filed a Form 4 today, showing that he purchased 200K shares in the open market at an average of $0.9198 on 6-11-2026. With $ORBS building up cash on the balance sheet these past several months per their PR updates, I think we may hear news soon, whatever it may be.

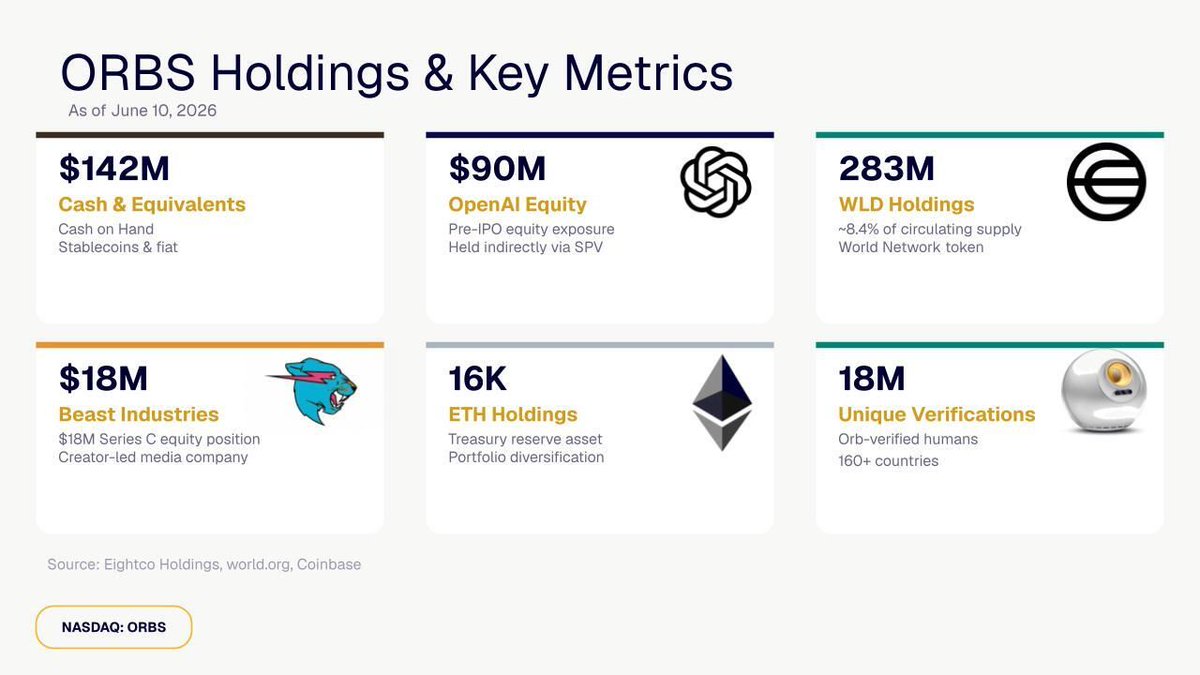

1/ $ORBS treasury crosses $406M across AI, digital identity, and the creator economy

Portfolio update as of June 10, 2026:

- $90M OpenAI equity (indirect via SPVs)

- 283.4M $WLD (~8.4% of supply)

- 16,278 $ETH

- $18M Beast Industries

- $1M Mythical Games

- ~$142M cash & stablecoins

🔗 Press Release:

prnewswire.com/news-releases…

4

6

2,074

Jun 6

$ORBS has a $90M stake in OpenAI and may benefit from this if the Trump administration does follow through with a government stake. if OpenAI doesn't IPO yet, this may be through a new funding round that puts OpenAI at a higher valuation than $ORBS got its own stake at.

BREAKING: Trump administration is discussing a possible government stake in OpenAI, per CNBC

2

413

Jun 6

$WLD might fall this weekend as it seems a number of people may have bought $WLD due to this crypto influencer buying $WLD. And those same people may be selling now due to this same crypto influencer saying he sold his $WLD. This may have ramifications for $ORBS as it has a lot of $WLD on its balance sheet. But $ORBS has recently decoupled from $WLD somewhat so we'll see what happens.

158

Jun 5

Though I do have concerns about this $ETH purchase by $ORBS, it's probably around $10M to $11M in cash used to make the purchase, so not insignificant, but it isn't something that will destory the company if the $ETH purchase is underwater at an unrealized loss for some time.

Jun 5

$ETH grew on the balance sheet from 11,068 tokens as of May 27th to 16,278 tokens as of June 3rd per the $ORBS PR updates. So assuming the purchase happened at market prices sometime from May 28th to June 3rd, that means the purchase price was somewhere between the time period high of $2042.54 and low of $1771.31. I'm assuming the purchase price was at the higher end of the range so it's probably underwater at an unrealized loss at the moment.

3

529

Jun 5

$ETH grew on the balance sheet from 11,068 tokens as of May 27th to 16,278 tokens as of June 3rd per the $ORBS PR updates. So assuming the purchase happened at market prices sometime from May 28th to June 3rd, that means the purchase price was somewhere between the time period high of $2042.54 and low of $1771.31. I'm assuming the purchase price was at the higher end of the range so it's probably underwater at an unrealized loss at the moment.

Jun 5

3

960

Jun 5

Criticism where criticism is due. $ETH grew on the balance sheet versus the last balance sheet update after a purchase of 5210 tokens and I don't like this $ETH purchase. This raises the question why $ETH is being bought when this cash should be used for the "proof of human" thesis. Hopefully, we'll hear news soon that they are working on something over at $ORBS.

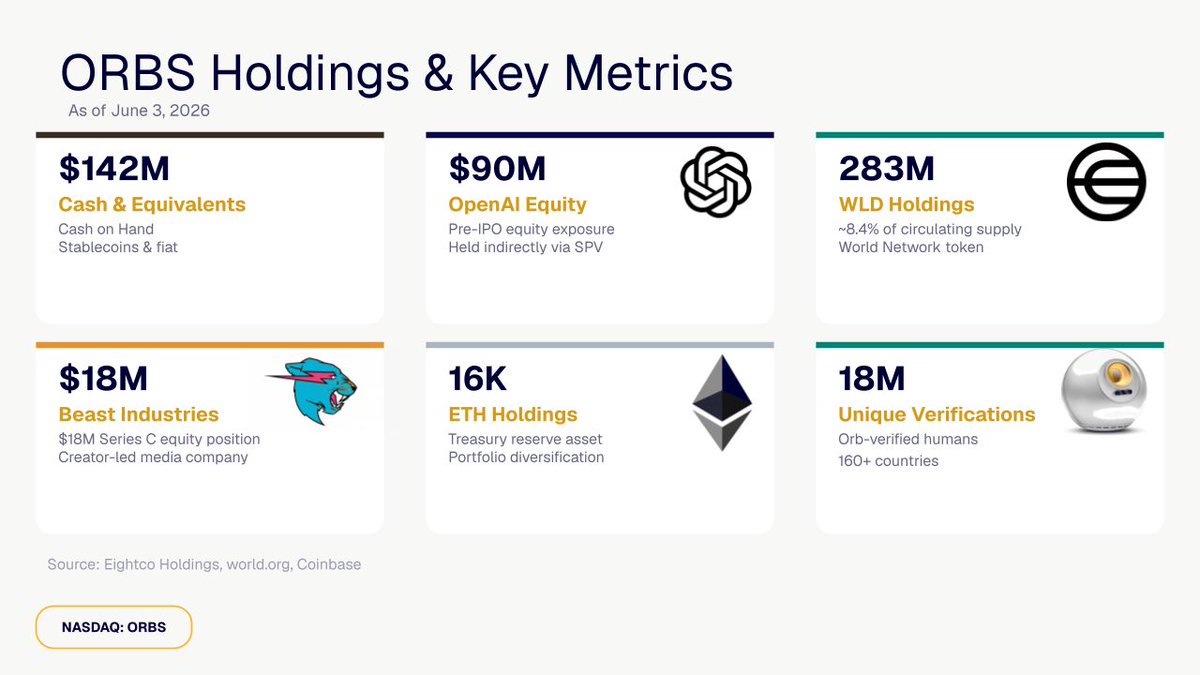

1/ 🧵 $ORBS treasury crosses $437M across AI, digital identity, and the creator economy

Portfolio update as of June 3, 2026:

- $90M OpenAI equity (indirect via SPVs)

- 283.4M $WLD (~8.4% of supply)

- $18M Beast Industries

- 16,278 $ETH

- $1M Mythical Games

- ~$142M cash & stablecoins

🔗 Press Release:

prnewswire.com/news-releases…

115