Ron Cadman is a Real Estate Developer and Founder of Southwest Urban Ventures

Joined November 2013

- Tweets 575

- Following 240

- Followers 93

- Likes 6

491 Photos and videos

#BankOfCanada #InterestRates #CanadaEconomy #HousingMarket #EconomicOutlook

The Bank of Canada held its key interest rate at 2.25%, citing ongoing economic uncertainty, elevated energy prices, and inflation risks despite signs of modest economic growth.

bankofcanada.ca/2026/06/fad-…

4

Jun 15

#AlbertaHousing #RentalMarket #RealEstateCanada

Alberta dominates Canada’s most affordable rental markets, claiming six of the seven lowest-cost cities for renters in 2026 and reinforcing the province’s strong rental value relative to other regions.

culturealberta.com/articles/…

3

Jun 12

#PhoenixRealEstate #CanadianBuyers #HousingMarket #InternationalRealEstate

Phoenix continues to attract Canadian homebuyers, ranking among the top U.S. destinations as demand rebounds for Sun Belt markets offering warm weather, lifestyle, and relative affordability.

azbigmedia.com/real-estate/p…

9

Jun 11

#CanadaHousing #CMHC #RealEstateCanada #HousingMarket #UrbanDevelopment

New CMHC research suggests Canada could have built nearly 30% more homes—and seen lower home prices—if housing supply responded to demand as efficiently as it does in the U.S.

realestatemagazine.ca/new-cm…

11

Jun 10

For LPs and capital partners, Phoenix multifamily is still a market that demands caution.

But it is no longer a market that should be dismissed with a one-line “too much supply” thesis.

The better way to frame Phoenix today is this: current operations are still messy, but the forward math is improving.

That distinction matters.

On the surface, there is still plenty to make investors uncomfortable. Kidder Mathews reported Q1 2026 vacancy at 11.8%, average asking rents at $1,535 per unit, and average pricing down 12% year over year to $221,942 per unit. Northmarq has also been clear that oversupply conditions are likely to persist through the coming quarters, which means this is not a market for aggressive rent growth assumptions or thinly capitalized deal structures.

But the market is not standing still.

Cushman & Wakefield reported Phoenix posted 6,261 units of net absorption in Q1 2026, the strongest quarterly multifamily absorption in at least the last 26 years. At the same time, Kidder Mathews reported the construction pipeline fell 30% year over year to 16,399 units. Marcus & Millichap also expects completions to fall by nearly 50% across the market in 2026. That combination is the heart of the current investment case: Phoenix is still digesting supply, but the amount of future competition is finally starting to recede in a meaningful way.

For equity, that changes the underwriting conversation.

Read more at: medium.com/p/9df618776d7a

Ron Cadman – southwestuv.com

#PhoenixMultifamily #CommercialRealEstate #MultifamilyInvesting #LPInvesting #JVEquity #CapitalMarkets

2

31

Jun 10

#Multifamily #Construction #SupplyChain #RealEstateDevelopment #MadeInUSA

Multifamily developers are increasingly turning to U.S.-made cabinetry and building materials to improve supply-chain reliability, reduce delays, and gain greater control over project timelines.

multihousingnews.com/why-mul…

4

Jun 9

#CanadaHousing #RealEstateCanada #EconomicOutlook

Canada's housing market showed signs of improvement in May, with stronger activity in several cities. However, buyer confidence remains cautious as economic uncertainty continues to weigh on a broader recovery.

rbc.com/en/economics/canadia…

2

Jun 8

#RentalMarket #RealEstateTrends #PropertyManagement

Renters have more negotiating power this spring, with nearly 40% of rental listings offering incentives like free rent, waived fees, or move-in discounts as supply continues to outpace demand.

azbigmedia.com/real-estate/i…

1

Jun 5

Lenders and equity partners should be thinking about Phoenix multifamily less as a directional bet and more as a precision exercise.

That is where the market is now.

The broad narrative is still familiar: elevated vacancy, soft rents, active concessions, and lingering supply pressure. Those risks are real. Kidder Mathews reported Q1 2026 vacancy at 11.8% and asking rents down 3.0% year over year. Northmarq said 2026 is shaping up more as a year of stabilization than a true inflection year, which is exactly why capital discipline still matters so much.

But the reason Phoenix remains investable is that the demand side is proving stronger than many expected.

Cushman & Wakefield’s Q1 2026 data showed 6,261 units of net absorption, the strongest quarterly performance in at least 26 years. That matters because it shows demand is not broken. The issue is not whether renters want Phoenix. The issue is that too much product arrived too quickly. As new supply finally slows, that distinction becomes very important for lenders, preferred equity, and JV partners evaluating medium-term risk.

The capital-markets signal is also becoming clearer.

Northmarq reported that recent Phoenix transaction activity has been concentrated in Class A and Class C, with Class A cap rates around 5.0% and Class C generally in the 6.5% to 7.0% range. That bifurcation says a lot. Buyers are either pursuing stronger assets where they believe fundamentals will improve as new competition fades, or they are demanding enough current yield and basis discount to justify near-term operating noise. The middle is less obvious, which is exactly why Phoenix is no longer a market where generic underwriting works.

The submarket story reinforces that point.

Read more at: medium.com/@ron_cadman/lende…

Ron Cadman – southwestuv.com

#PhoenixMultifamily #CRE #MultifamilyInvesting #RealEstateDebt #JVEquity #CapitalAllocation

14

Jun 5

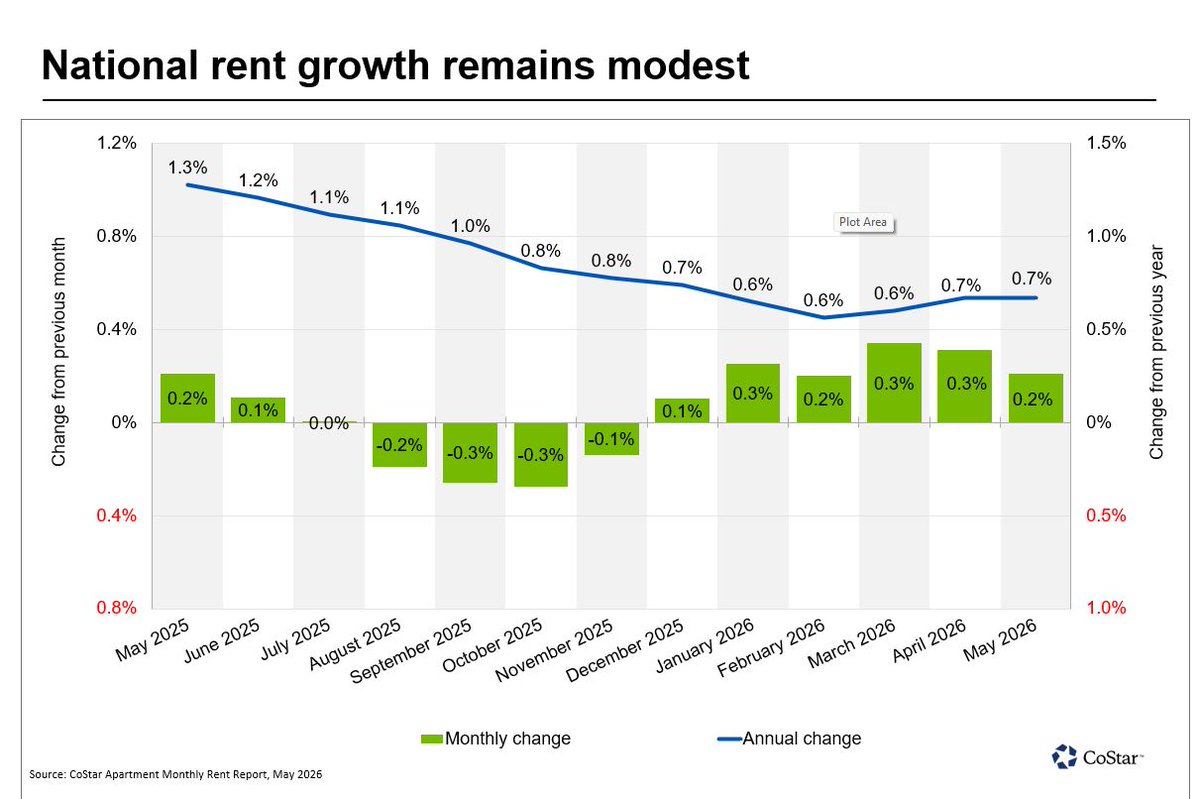

#Multifamily #CRE #RentGrowth #HousingMarket #RealEstateTrends #MarketUpdate

U.S. apartment rents rose 0.2% in May, marking six straight months of growth. However, rent gains remain modest as new supply and slower demand continue to limit pricing power.

businesswire.com/news/home/2…

3

Jun 4

#CRE #InvestmentTrends #CanadianRealEstate #CapitalMarkets #MarketOutlook

Improving geopolitical conditions and lower bond yields are boosting investor confidence, with signs pointing to a stronger Canadian real estate market in the second half of 2026.

cbre.ca/insights/briefs/cana…

1

1

18

Jun 3

#Multifamily #NOI #PropertyManagement #RealEstateInvesting #InvestmentStrategy

In today’s multifamily market, strong NOI is driven by operational excellence—not market momentum. Rising costs and selective lending are making execution more important than ever.

multihousingnews.com/rewriti…

13

Jun 2

#CanadaHousing #RealEstateCanada #HousingMarket #EconomicTrends

New research suggests Canada's homeownership decline may be driven not only by affordability, but also by delayed family formation and changing household demographics.

kelownarealestate.com/blog-p…

3

Jun 1

#LasVegasRealEstate #RealEstateTrends #HousingMarket #SmartGrowth

Despite its reputation for urban sprawl, Las Vegas ranks among the top U.S. metros for density and connectivity, with limited land driving more concentrated development.

liedcenter.unlv.edu/wp-conte…

2

May 29

#Multifamily #CRE #Refinancing #RealEstateLending

Commercial and multifamily lending surged in early 2026, with originations up 52% year-over-year as banks returned to refinance maturing debt.

worldpropertyjournal.com/rea…

5

May 28

#CanadaHousing #RealEstateCanada #HousingMarket #MarketUpdate #CREA

Canadian home sales edged up 0.7% in April, signaling the market may be stabilizing as inventory and supply return to more balanced levels.

kelownarealestate.com/blog-p…

3

May 27

Phoenix multifamily is moving from a market-selection story to an asset-selection story.

For the last two years, the dominant institutional view on Phoenix was straightforward: too much supply, too much lease-up competition, too much headline risk. That view was understandable, and for a period it was correct. But markets do not stay in the same phase forever. What matters now is not whether Phoenix experienced a supply shock. It did. What matters now is whether the market is still deteriorating broadly, or whether it is beginning to differentiate in ways that create investable asymmetry. The evidence increasingly points to the second. Cushman & Wakefield reported that Phoenix posted 6,261 units of net absorption in Q1 2026, the strongest quarterly performance in at least the last 26 years. That is not the statistic of a market with broken demand. It is the statistic of a market still clearing excess inventory. (Cushman & Wakefield)

The challenge, of course, is that absorption alone does not restore pricing power overnight. Kidder Mathews reported Q1 2026 vacancy at 11.8%, average asking rent at $1,535 per unit, and a 30 percent year-over-year decline in units under construction to 16,399. Those figures capture the current phase well: operations remain soft, but future competitive pressure is beginning to recede. This is exactly the kind of transition period where broad market narratives become less useful and basis discipline becomes more important. If you are underwriting Phoenix today, the question is no longer simply whether the market is overbuilt. The better question is whether your basis adequately compensates you for one more year of noisy fundamentals while positioning you for a more rational supply backdrop ahead. (Kidder Mathews)

Read more at: roncadman.substack.com/p/pho…

Ron Cadman – southwestuv.com

#PhoenixMultifamily #InstitutionalRealEstate #CommercialRealEstate #MultifamilyInvesting #CapitalMarkets #PhoenixRealEstate

6

May 27

#ArizonaRealEstate #Multifamily #RealEstateInvesting #1031Exchange

More Arizona property owners are using tax-deferred strategies to transition from hands-on real estate management into professionally managed multifamily investments.

azbigmedia.com/real-estate/h…

4

May 26

#Multiplex #CanadaHousing #RealEstateInvesting #ZoningReform #HousingMarket

Multiplexes are emerging as a key path to housing affordability in Canada, driven by zoning reforms and growing demand from buyers priced out of single-family homes.

realestatemagazine.ca/multip…

1

12

May 25

#HousingMarket #RealEstateTrends #MarketUpdate #PhoenixRealEstate #EconomicOutlook

Global conflict and rising energy costs are impacting housing decisions, as higher everyday expenses make buyers more cautious and budget-focused.

azbigmedia.com/real-estate/h…

4