“Al Nut…..Al Nyet”…….i've been around , trading, since 1989. last stop…. family office… multi billion... less conservative than others. AMSTERDAM

Joined November 2021

- Tweets 2,521

- Following 315

- Followers 191

- Likes 4,341

112 Photos and videos

ES1 retweeted

Jun 12

CNN montage of all the times Trump announced deals with Iran.

Anderson Cooper: Today marks 39 times that he has said something like that.

595

8,703

25,441

1,928,598

ES1 retweeted

May 22

Per the Fed Model, when stocks and bonds are correlated and offer similar yields, when bonds reprice, so will equities. That’s the transmission link between rates and equities.

If yields rise to 5%, how much would equities need to derate? Per the scatter plot below, a move in bonds from a 22x “P/E” (4.6%) to a 20x P/E (5%), should push the equity P/E-multiple from its current 22x to 18-19x. That’s approximately a 15% haircut for the S&P 500, at least in terms of valuation. With earnings growing 18%, the price decline would be less, as was the case in March when the Iran conflict was flaring.

7

28

165

12,832

ES1 retweeted

May 15

BOMBSHELL: Trump officially throws Taiwan under the bus on Fox News. He explicitly admits withholding a $12 BILLION weapons package, using their survival as a mere negotiating chip.

He casually dismisses Taiwan as a "very small island" that is simply too far to defend.

164

898

2,318

170,258

ES1 retweeted

May 15

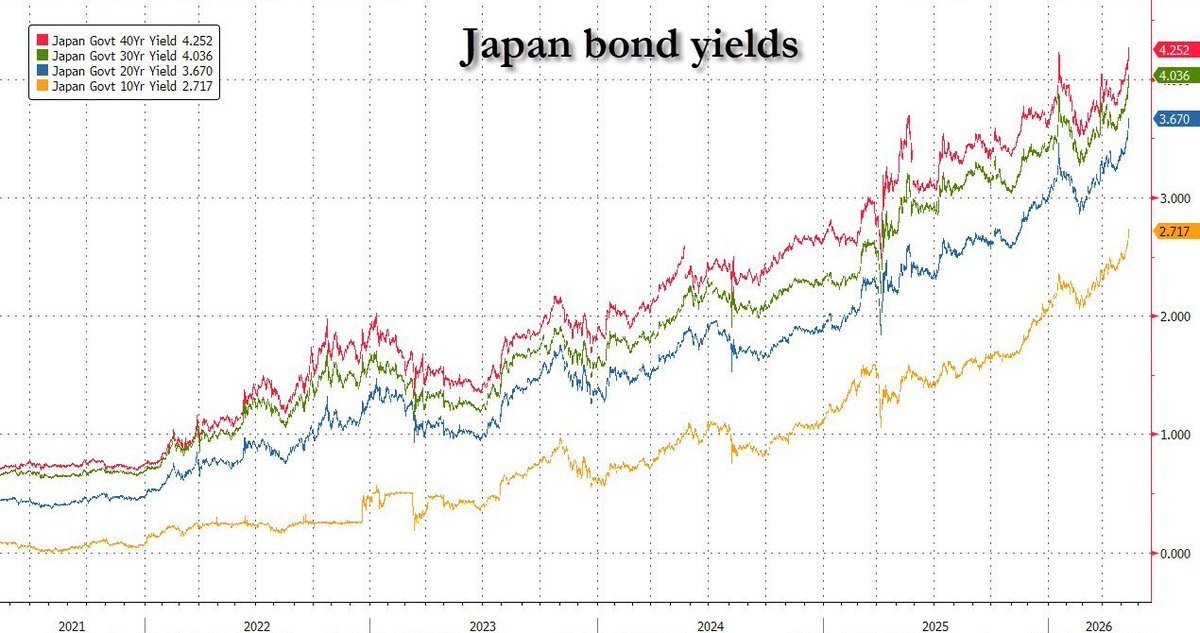

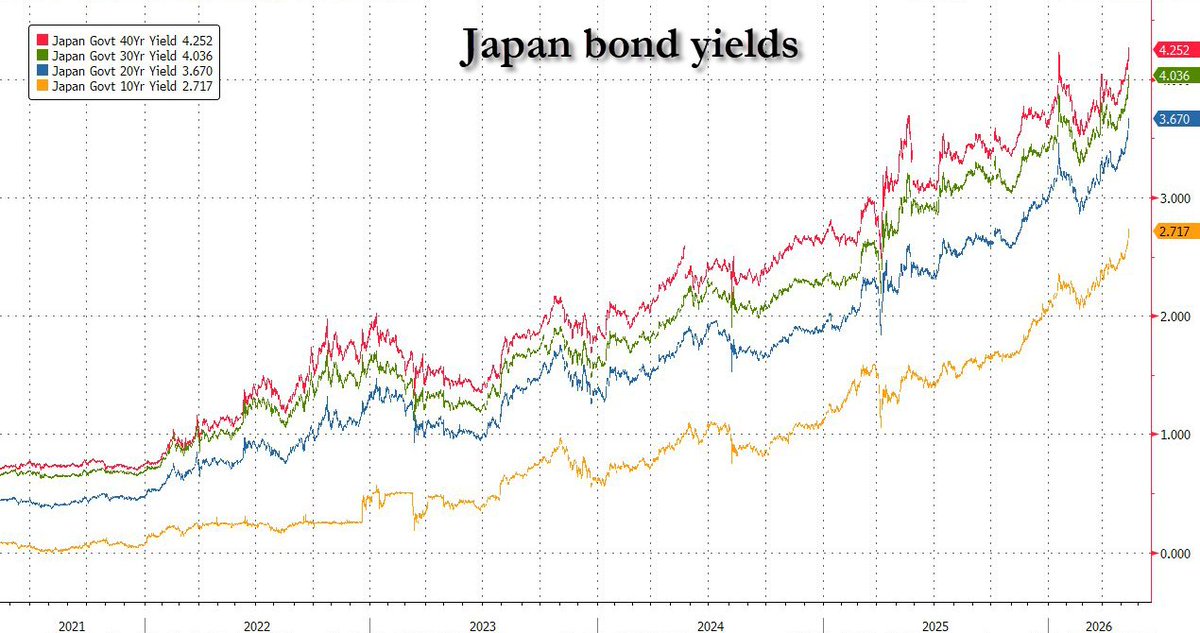

Japan Is Building A Rate Cushion Before The Next Crisis

Japan is not trying to return to deflation. That is the key point.

For 30 years Japan fought stagnant wages, weak demand, falling price expectations, and a monetary system pinned near zero. Now it finally has inflation, wage momentum, and nominal growth. But this is not the clean inflation Japan wanted.

It is energy driven.

It is yen driven.

It is imported.

That changes the entire policy equation.

They Want Inflation But Not A Bond Market Accident

Japan can tolerate moderate inflation because it lifts nominal GDP and helps manage a debt load above 250% of GDP. But oil shock inflation is different.

When crude rises and the yen weakens, Japan imports inflation through food, fuel, utilities, transport, and industrial inputs. That squeezes households before wages fully catch up. It also hits corporate margins and makes bond investors question whether the BOJ is behind the curve.

So Japan’s problem is not simply inflation versus deflation.

It is controlled reflation versus imported stagflation.

They want to escape the zero rate trap, but they cannot let the yen collapse or allow long term JGB yields to reprice disorderly.

The BOJ Is Buying Time

The sharper point is that Japan is not just hiking to fight today’s inflation. It is trying to rebuild policy space before the next downturn.

At a 0.75% policy rate, the BOJ still has very little room to cut if a global recession hits. If they stay near zero forever, they enter the next crisis with almost no conventional ammunition.

So the strategy is becoming clearer.

Raise rates while inflation gives political cover.

Defend the yen before import inflation worsens.

Create a cushion before recession arrives.

Show bond markets Japan is not trapped in fiscal dominance.

That is why a move toward 1.0% matters. It is not only about inflation today. It is about having room to cut tomorrow.

Fiscal Policy Is The Risk

The danger is that fiscal and monetary policy are pulling in opposite directions.

The BOJ is normalizing. The government is still running large budgets and considering more relief for fuel and utility costs. That may help households in the short run, but it also raises questions about debt, issuance, and credibility.

Bond markets care about cash flow.

They care about JGB supply.

They care about whether inflation is lifting real growth or just raising the cost of living.

If fiscal support becomes too broad while the BOJ is tightening, Japan risks a dangerous loop.

Higher deficits.

More JGB supply.

Higher term premium.

More yen weakness.

More imported inflation.

That is the loop policymakers are trying to avoid.

Why This Hits The World

The 10 year JGB near 2.7%, the 30 year above 4%, and the 40 year above 4.2% tell you Japan is no longer the world’s automatic cheap money anchor.

For years, Japanese capital had to go abroad to find yield. That supported U.S. Treasuries, European bonds, emerging market debt, credit, equities, and carry trades.

Now domestic Japanese yields are becoming investable again.

That changes global capital flow math. Japanese insurers, pensions, banks, and households do not need to chase foreign yield as aggressively. Even if they do not dump foreign bonds, reduced buying at the margin tightens global liquidity.

Less Japanese capital leaving home means more pressure on U.S. duration, more pressure on European bonds, more pressure on carry trades, and less hidden support under risk assets.

My Take

Japan is using energy driven inflation as cover to escape zero rates and rebuild a cushion before the next downturn.

But the tradeoff is brutal.

Move too slowly and the yen weakens. Move too fast and they risk crushing demand, exporters, and the carry trade.

So Japan likely chooses controlled tightening, targeted relief, bond support only in disorder, and FX intervention if the yen breaks.

The old Japan exported cheap money.

The new Japan may pull it back home.

6

32

100

17,146

ES1 retweeted

May 15

The Bond Market Is Testing The Fed Put

The 2 year Treasury chart is the Fed path chart. It shows what the market thinks policy will look like over the next several quarters. The breakout back above 4% matters because investors spent months assuming rate cuts would eventually rescue the cycle. That assumption is now being challenged.

In a clean recession scare, the 2 year usually falls because the market prices easier policy. This chart is saying the Fed may not have that freedom yet. Oil, sticky inflation, fiscal deficits, and still firm nominal data are keeping the front end tighter than a normal slowdown would suggest.

The Long End Is The Bigger Warning

The 30 year is not just about the Fed. It is about term premium, fiscal credibility, Treasury supply, inflation uncertainty, and foreign demand.

A long bond above 5% means investors want more compensation to hold U.S. debt for decades. That hits mortgages, commercial real estate, bank balance sheets, corporate refinancing, equity valuations, and government interest expense.

The 2 year says policy may stay tight.

The 30 year says the market is questioning the cost of funding the system itself.

The Energy Shock Bridge

The missing bridge is demand destruction.

High energy prices are inflationary at first, but if they stay high long enough, they become deflationary through the real economy. Oil above $100 acts like a tax on consumers and businesses. It raises gasoline, diesel, trucking, food distribution, utilities, chemicals, plastics, and industrial input costs.

At first, CPI rises and the Fed stays trapped. Then households cut spending, businesses lose margin, freight slows, credit stress rises, and demand starts breaking.

If that demand destruction becomes global, the regime changes again. Europe imports less. China exports less because foreign buyers weaken. Emerging markets get hit through food, fuel, FX, and dollar debt. Japan gets squeezed by energy imports and weaker external demand. The U.S. consumer pulls back. Inventories build. Margins compress. Then layoffs and credit losses catch up.

That is why falling oil later would not prove the shock was harmless.

It may mean the shock finally reached demand.

The Signal

The dangerous part is that both ends of the curve are rising while the economy is already showing late cycle cracks.

If yields were rising because growth was booming, equities could handle it better. But if yields are rising because inflation, energy costs, debt supply, and fiscal credibility are trapping the Fed while growth weakens, that is a very different setup.

This is where the late 1960s and 1970s matter. Recessions did not instantly bring bond market relief because inflation psychology and oil shocks were embedded. Growth weakened, stocks fell, and yields stayed high because the market did not trust the inflation backdrop.

The early phase looks inflationary.

The late phase becomes deflationary.

The damage happens in between.

My Take

The 2 year is saying the Fed may not be able to cut as fast as the market wants. The 30 year is saying investors want more compensation to hold long duration U.S. debt.

If global demand destruction becomes undeniable, the 2 year should eventually roll over as markets price cuts. The 10 year likely catches a bid too if recession risk overwhelms inflation fear. The 30 year is harder. It only rallies cleanly if inflation expectations and fiscal fears calm down.

That is the signal.

The bond market is not just pricing inflation. It is pricing the possibility that the usual rescue mechanism is delayed, constrained, or no longer fully trusted.

May 15

The U.S. 30 year and 2 year yield have both broken out.

This is the nightmare scenario we saw in 1968 and 1974 where the economy entered a recession, the market turn downward while yields doubled.

Not a good way for Kevin Warsh to begin his Federal Reserve term.

11

25

126

19,640

ES1 retweeted

May 14

The Fed won’t cut rates until the bond market gives them permission.

That probably means they need enough demand destruction to cool oil, soften inflation expectations, and bring buyers back into long duration Treasuries.

If they cut while the 30 year is clearing above 5%, the market may read it as surrender, demand even more term premium, and push borrowing costs higher anyway. They may tolerate economic pain longer than people expect because a growth scare solves several problems at once. It weakens commodities, strengthens the Treasury bid, stabilizes the dollar funding system, and gives the Fed cover to cut without looking like it lost control of inflation.

They are not waiting for the economy to be fine. They are waiting for the pain to become politically and financially useful.

7

12

79

7,720

ES1 retweeted

May 12

Someone just opened a pop-up in NYC displaying all 3.5 million pages of the Epstein files.

Walk in. Read. See for yourself.

May 11

🇺🇸 Epstein survivors were shocked by Melania denying ties to Epstein, and are now alarmed by reports Republicans may push to pardon Ghislaine Maxwell.

Survivor Annie Farmer called it “extremely troubling.”

If true, they're not doing it for free.

727

31,929

106,841

3,906,346

ES1 retweeted

May 1

Join now and AMA -

how we move markets by hedging them

GIVING AWAY 1-MONTH OF VS3D TO A LUCKY SOMEONE WHO RETWEETS THE STREAM

x.com/i/broadcasts/1NGaraqpa…

5

30

33

4,605

ES1 retweeted

Apr 29

El clip colaborativo del rapero sueco Yung Lean y GENER8ION supera los límites de un simple videoclip musical y ya es un festín visual extraordinario. 🔥

La coreografía, a cargo del gran coreógrafo francés Damien Jalet. 💥

Hoy, 29 de abril, Día internacional de la danza.

301

6,494

39,749

2,201,207

ES1 retweeted

Apr 29

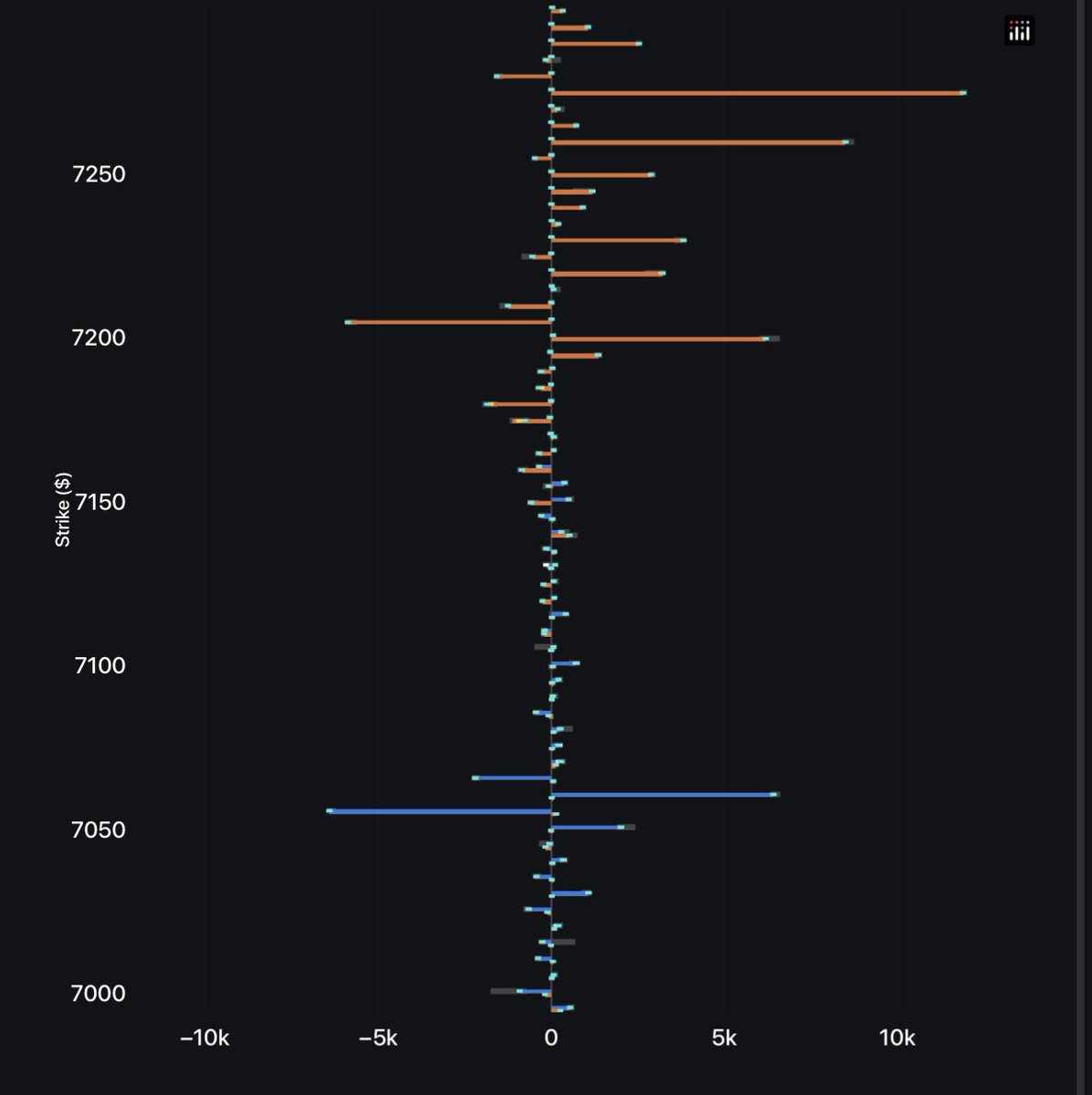

3k size condor. 98th %'ile.....not quite the fun times of 50k lots.

6

4

38

18,437

ES1 retweeted

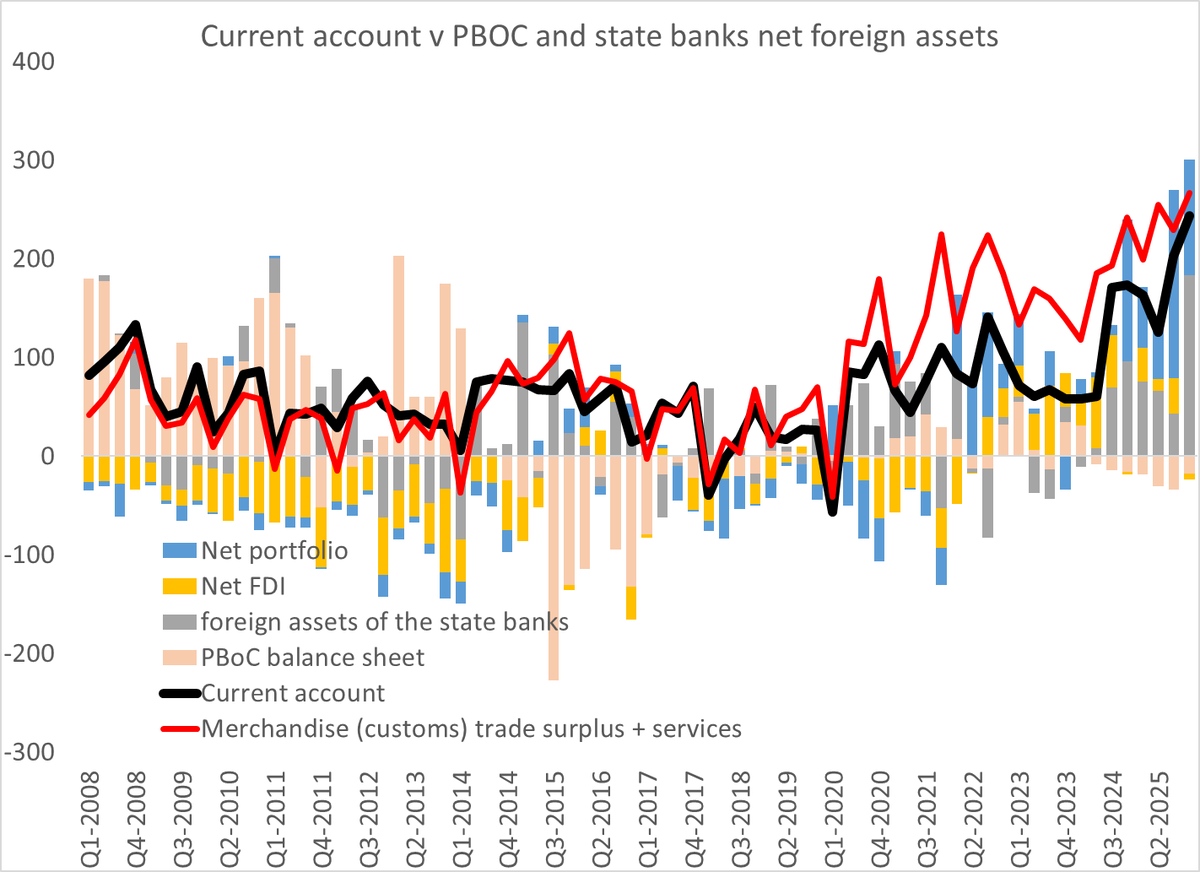

Apr 25

Gonna keep repeating this until it registers --

The PBOC may or may not be reducing its real Treasury holdings; it could just be moving out of US custodians

But the state banks are clearly adding to their dollar portfolios, and thus indirectly funding the global accumulation of US assets

Apr 25

i bet we'll be repeating this conversation next year: many say usd and ust are over yet data show the world cannot get enough of it; china is reducing its holding but it hasn't mattered at all (for quite some time)

13

52

211

37,840

ES1 retweeted

Apr 21

TODAY'S SPX POSITION

WAS A RED FLAG FOR BULLS

...here's why

18

47

436

75,748

ES1 retweeted

Apr 17

Schrödinger's Strait

Apr 17

BREAKING: Dozens of ships are making U-turns in the Strait of Hormuz, heading back into the Persian Gulf after surging toward it following Araghchi's "completely open" declaration, per MarineTraffic data.

Iran had warned earlier today that the opening would be "practically limited," with Iran alone deciding which ships qualify for passage.

3

4

31

12,072

ES1 retweeted

Apr 11

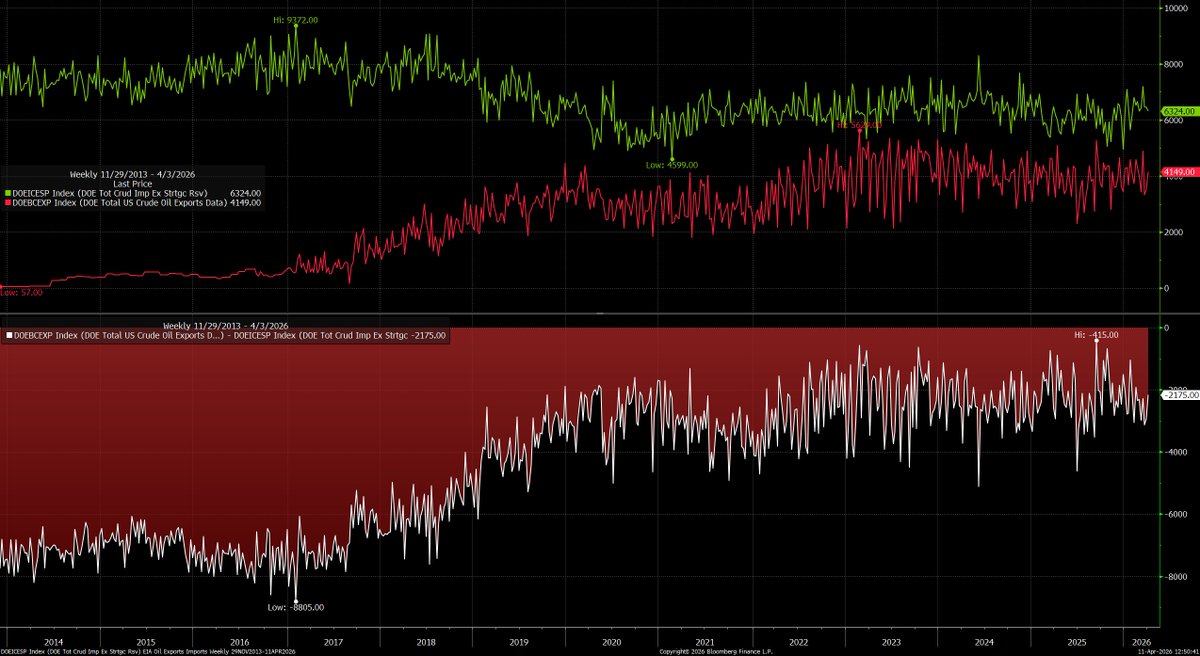

Much needed reminder that the USA is still a net crude oil importer.

23

10

97

53,758

ES1 retweeted

Apr 2

It prevents fed funds cuts, props up Wall Street, props up inflation, all because the Repo Gang of Four won't deal with uneven distribution of reserves.

Fed's Logan: Fed balance sheet growth is not bad if it meets public needs.

Fed's Logan: Current ample reserves system is efficient and effective.

4

2

66

19,790