461 Photos and videos

"Our ambition is to become one of the largest companies in the UK. I believe that our strategy gives us a credible path to achieving that goal"

Jun 13

Our ambition is to become one of the largest companies in the UK. I believe that our strategy gives us a credible path to achieving that goal.

At the centre of our approach is the balance sheet. We are building a balance sheet around what we believe is the best form of capital available: Bitcoin. As that balance sheet grows, it creates opportunities across the business. It can support the growth of our operating activities, enable strategic acquisitions, provide flexibility to pursue new opportunities as they emerge, and allow us to further strengthen and expand the balance sheet itself.

These are often viewed as separate strategies, but we do not see them that way. They are all connected. We have one strategy, and it revolves around building and intelligently deploying a strong balance sheet. Everything else flows from that foundation.

Because of this we think that it is important for investors and potential investors to understand this balance sheet at any moment in time and increasingly these investors include institutional investors who are used to specific metrics.

We believe the term "mNAV" is currently being used in ways that can create confusion rather than clarity. Various companies and commentators often calculate the metric differently. Some use Market Capitalisation as the numerator, while others use Enterprise Value. On the denominator side, some use Net Asset Value, while others use the market value of Bitcoin holdings, often referring to this as "BTC NAV" despite it being closer to a gross asset value than a true NAV calculation.

The treatment of outstanding securities is also a further element. We use the fully diluted number of shares which includes all in the money warrants and then factors in cash linked to the warrant proceeds, however if we were creating our analytics from the beginning, understanding everything that we know now, we would treat Smarter Convert as debt rather than an instrument that will convert into equity.

In traditional finance, mNAV generally refers to Market Capitalisation divided by Net Asset Value, producing a premium or discount multiple relative to NAV. However, many of the mNAV metrics currently used in the Bitcoin treasury company sector employ neither of these measures, resulting in a broad range of calculations that share the same label but convey very different information.

We believe this lack of standardisation becomes increasingly problematic as treasury companies introduce debt, preferred equity and other financing instruments. As capital structures become more complex, comparisons between companies become less meaningful if investors are not working from a common framework.

For this reason, we updated our analytics dashboard during the week and are moving away from mNAV as a primary valuation metric. Instead, we now display "Fully Diluted EV vs BTC Value", calculated as Fully Diluted Enterprise Value divided by the current market value of total Bitcoin holdings. We have also added charts that show “Net Bitcoin Value Per Fully Diluted Share” and “Net Sats Per Fully Diluted Share”. For all calculations on our analytics page, you can hover over the question marks and view the formulas.

In our view, this provides a completer and more transparent picture of the value of a Bitcoin treasury company. We believe investors should also consider several important measures, including leverage or amplification, Bitcoin per share growth over time ("Bitcoin Yield"), and the sustainability of that growth going forward. The last being harder to statistically analyse.

This naturally leads to another question we were asked this week: what is the single most important metric for evaluating a Bitcoin treasury company?

Our view is that there is no single number.

Our treasury objective is straightforward: to increase the amount of Bitcoin attributable to each share over time. However, we would encourage investors to assess performance over quarters and years rather than days or weeks. The key question is whether management decisions are increasing Bitcoin per share on a sustainable basis.

For a simple, ungeared treasury company, the analysis can appear relatively straightforward. One could argue that issuing shares is accretive whenever the value received exceeds the Bitcoin value attributable to the shares issued. However, the reality becomes considerably more nuanced once debt financing, debt repayment, warrant repurchases, share buybacks and other capital allocation decisions enter the equation.

A transaction that appears dilutive when viewed through one metric may in fact be accretive when viewed through another. This is precisely why we believe the industry requires better and more transparent analytics. As treasury strategies become more sophisticated, and treasury companies become much larger, investors need to consider multiple variables rather than relying on a single ratio or headline figure.

For public companies, such as The Smarter Web Company, there is an additional dimension. Investors should not only consider the Bitcoin treasury itself, but also operating revenues, corporate costs, cash generation and the broader business activities that sit alongside the treasury strategy. These elements can have a meaningful impact on the company's ability to grow Bitcoin per share over the long term.

If Bitcoin treasury companies are to mature into a recognised institutional asset class, the industry will benefit from greater consistency in reporting standards, valuation methodologies and performance metrics. Investors should be able to compare companies using measures that are transparent, widely understood and economically meaningful.

Over the coming months, we intend to continue refining our analytics framework and working with others across the sector to help improve consistency and comparability throughout the industry.

On Monday this week we announced an update to our ATM-style facility. We raised £145,670 (before expenses), equivalent to approximately £0.29 per share. The ATM-style facility continues to be an important part of our capital markets toolkit and provides us with valuable flexibility as we execute our strategy.

Throughout the week we continued sharing the remaining videos filmed at the Bitcoin Treasuries Unconference UK. As a reminder, early bird tickets for the 2027 event are available on our website.

Looking ahead, we have decided to rename the event series from Bitcoin Treasuries Unconference UK to Bitcoin Treasuries Conference UK. As we scale both the event and help scale the wider industry in the UK, we believe this name will be more familiar to a broader audience. The core spirit and format of the event will remain largely unchanged, but we believe this evolution will help us reach and engage a larger community.

I would also like to remind shareholders that we have an important vote at our General Meeting on 17 June. Shortly afterwards, we will announce the results via RNS. Thank you to everyone who has already taken the time to vote. Depending on your platform, there may still be an opportunity to submit your vote if you have not yet done so. Voting is an important part of share ownership, regardless of whether you vote for or against a resolution.

Finally, I would like to acknowledge that our share price is not currently performing as well as I would like. I cannot control the market, but I can control what we are building and the two certainly seem a little disconnected from where I am sitting.

While short-term market performance can be frustrating, my conviction in the direction of the business has never been stronger. I believe we are executing the right strategy, and I am excited about where we are heading. As our progress becomes more widely understood and the opportunity ahead of Smarter Web becomes clearer, I believe the market will recognise the value of what we are building.

Thank you for your support.

LSE: #SWC | OTCQB: $TSWCF | FRA: $3M8

1

1

16

550

SWC-Wiki retweeted

Every evening, @matthewkerridge updates the community with his Smarter Web Tracker.

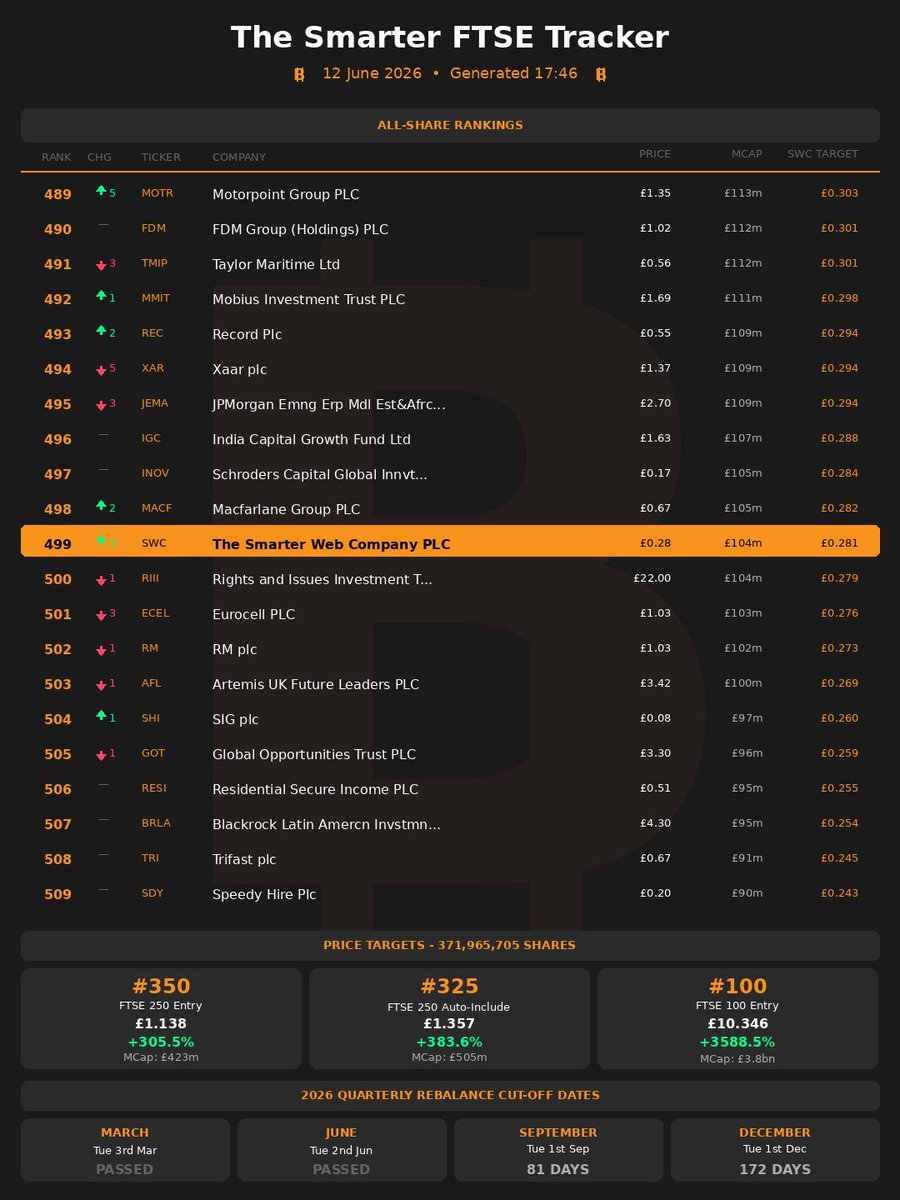

Last Friday, SWC closed the week at number 499 in the FTSE rankings.

The first target is position 325, which would mean automatic inclusion in the FTSE 250. As of Friday, that would require a market cap of around £505 million.

Sounds miles away, doesn't it?

Maybe not.

With the Capital Reduction vote underway, most shareholders I speak to believe SWC will eventually follow the path laid out by companies like MicroStrategy and issue preferred shares to acquire more Bitcoin.

Under the Bitcoin Power Law, Bitcoin is currently fairly valued at around £104,500 ($140,000). The next FTSE review takes place in September. If Bitcoin returns to that fair value by then, SWC would need approximately 4,832 BTC to reach the FTSE 250 threshold.

If the target isn't reached until the December review, that figure falls to around 4,105 BTC because the Power Law fair value would have risen to approximately £123,000 ($165,000).

Once FTSE 250 inclusion is achieved, the next destination is the FTSE 100.

That currently requires a market cap of around £3.6 billion.

Again, it sounds like a huge leap.

But look at the bigger picture.

The next Bitcoin halving arrives in April 2028. By then, the Bitcoin Power Law suggests a fair value of around £186,000 ($250,000).

At that valuation, SWC would need roughly 19,400 BTC to support a £3.6 billion market cap based purely on its Bitcoin holdings.

Of course, this is a simplified model. It assumes no further dilution, Bitcoin tracking the centre line of the Power Law, and the market continuing to value SWC broadly in line with its Bitcoin treasury.

But what it does show is that @asjwebley and the team's ambitions are not as far-fetched as some people think.

Personally, if preferred shares become part of the strategy, I can see a realistic path to the FTSE 100 before the end of the decade.

Do your own research.

But if you're bullish on Bitcoin long term, and you believe the predictions of $1 million Bitcoin eventually becoming reality, then perhaps these targets aren't as crazy as they first appear.

Not financial advice.

Jun 12

A good end to the week. $SWC up 6.6% on the day.

6.5% up in Bitcoin terms.

6th Highest Riser for the day on the FTSE All-Share Index.

4th Highest Riser for the day on the FTSE Small Cap Index.

h/t @Toffeebdm & @andysmith_asap

Today rightly belonged to Space X.

Tomorrow may belong to more AI plays.

But there will be a day where capital looks elsewhere for a home.

Players are positioning as we speak.

Capital will continue finding its way into Bitcoin.

Via Digital Credit products like STRC and SATA, via self storage Bitcoin, via ETFs and via leveraged / amplified plays like MSTR, ASST and SWC.

There will always be short term plays and noise but the lower time preference the clearer the long term opportunity Bitcoin and amplified Bitcoin opportunities appear.

Keep an eye out for @TimKotzman’s latest pod with @asjwebley and @Croesus_BTC on X to be released today.

Have a great weekend all!

Onwards! 🚀

2

2

16

238

SWC-Wiki retweeted

1h

Sunday shoutout 📣

Alongside hundreds of websites, The Smarter Web Company & Squarebird are quietly building something much bigger too.

Helping businesses establish their digital presence.

Growing a Bitcoin treasury.

And this upcoming week, an #SWC General Meeting vote to lay foundations that could unlock new strategic options for the future.

The websites being built today generate the cash flows.

The treasury compounds the balance sheet.

And the team keeps executing with a road to Prefs for further amplified Bitcoin.

Know a business that needs a new website, stronger online visibility, or help getting started online?

Send them this way 👇

#SWC #TSWCF #3M8 #WebDesign #DigitalMarketing #Bitcoin

smarterwebcompany.co.uk/web-…

Jun 7

Sunday shoutout 📣

Every week, The Smarter Web Company and Squarebird are helping businesses build their digital home.

Websites that attract customers.

Platforms that support growth.

Digital foundations that help businesses get found, trusted and chosen.

And alongside that, a growing SWC Bitcoin treasury that makes it all possible.

Know a business that needs a new website, a stronger online presence, or help navigating the digital world?

Point them in the right direction 👇

#SWC #TSWCF #3M8 #WebDesign #DigitalMarketing #Bitcoin

smarterwebcompany.co.uk/web-…

4

10

200

SWC-Wiki retweeted

Should You Invest In SpaceX IPO, Elon Musk, Bitcoin or AI? - Pomp & Jordi. I really enjoyed this one

youtube.com/watch?v=gAqXcGn3…

1

13

670

SWC-Wiki retweeted

Interested in learning more about, The Smarter Web Company, the UK’s largest Bitcoin treasury company?

Since our IPO in April 2025, our CEO, @asjwebley, has provided a weekly update to stakeholders demonstrating a consistent and transparent approach to communication.

In this week’s update, he discusses how we define key industry metrics such as mNAV and why they matter as the Bitcoin treasury sector continues to evolve. He also provides an update on the progress made across the business during the week.

Follow him for regular insights and to stay updated on our progress.

LSE: #SWC | OTCQB: $TSWCF | FRA: $3M8

Jun 13

Our ambition is to become one of the largest companies in the UK. I believe that our strategy gives us a credible path to achieving that goal.

At the centre of our approach is the balance sheet. We are building a balance sheet around what we believe is the best form of capital available: Bitcoin. As that balance sheet grows, it creates opportunities across the business. It can support the growth of our operating activities, enable strategic acquisitions, provide flexibility to pursue new opportunities as they emerge, and allow us to further strengthen and expand the balance sheet itself.

These are often viewed as separate strategies, but we do not see them that way. They are all connected. We have one strategy, and it revolves around building and intelligently deploying a strong balance sheet. Everything else flows from that foundation.

Because of this we think that it is important for investors and potential investors to understand this balance sheet at any moment in time and increasingly these investors include institutional investors who are used to specific metrics.

We believe the term "mNAV" is currently being used in ways that can create confusion rather than clarity. Various companies and commentators often calculate the metric differently. Some use Market Capitalisation as the numerator, while others use Enterprise Value. On the denominator side, some use Net Asset Value, while others use the market value of Bitcoin holdings, often referring to this as "BTC NAV" despite it being closer to a gross asset value than a true NAV calculation.

The treatment of outstanding securities is also a further element. We use the fully diluted number of shares which includes all in the money warrants and then factors in cash linked to the warrant proceeds, however if we were creating our analytics from the beginning, understanding everything that we know now, we would treat Smarter Convert as debt rather than an instrument that will convert into equity.

In traditional finance, mNAV generally refers to Market Capitalisation divided by Net Asset Value, producing a premium or discount multiple relative to NAV. However, many of the mNAV metrics currently used in the Bitcoin treasury company sector employ neither of these measures, resulting in a broad range of calculations that share the same label but convey very different information.

We believe this lack of standardisation becomes increasingly problematic as treasury companies introduce debt, preferred equity and other financing instruments. As capital structures become more complex, comparisons between companies become less meaningful if investors are not working from a common framework.

For this reason, we updated our analytics dashboard during the week and are moving away from mNAV as a primary valuation metric. Instead, we now display "Fully Diluted EV vs BTC Value", calculated as Fully Diluted Enterprise Value divided by the current market value of total Bitcoin holdings. We have also added charts that show “Net Bitcoin Value Per Fully Diluted Share” and “Net Sats Per Fully Diluted Share”. For all calculations on our analytics page, you can hover over the question marks and view the formulas.

In our view, this provides a completer and more transparent picture of the value of a Bitcoin treasury company. We believe investors should also consider several important measures, including leverage or amplification, Bitcoin per share growth over time ("Bitcoin Yield"), and the sustainability of that growth going forward. The last being harder to statistically analyse.

This naturally leads to another question we were asked this week: what is the single most important metric for evaluating a Bitcoin treasury company?

Our view is that there is no single number.

Our treasury objective is straightforward: to increase the amount of Bitcoin attributable to each share over time. However, we would encourage investors to assess performance over quarters and years rather than days or weeks. The key question is whether management decisions are increasing Bitcoin per share on a sustainable basis.

For a simple, ungeared treasury company, the analysis can appear relatively straightforward. One could argue that issuing shares is accretive whenever the value received exceeds the Bitcoin value attributable to the shares issued. However, the reality becomes considerably more nuanced once debt financing, debt repayment, warrant repurchases, share buybacks and other capital allocation decisions enter the equation.

A transaction that appears dilutive when viewed through one metric may in fact be accretive when viewed through another. This is precisely why we believe the industry requires better and more transparent analytics. As treasury strategies become more sophisticated, and treasury companies become much larger, investors need to consider multiple variables rather than relying on a single ratio or headline figure.

For public companies, such as The Smarter Web Company, there is an additional dimension. Investors should not only consider the Bitcoin treasury itself, but also operating revenues, corporate costs, cash generation and the broader business activities that sit alongside the treasury strategy. These elements can have a meaningful impact on the company's ability to grow Bitcoin per share over the long term.

If Bitcoin treasury companies are to mature into a recognised institutional asset class, the industry will benefit from greater consistency in reporting standards, valuation methodologies and performance metrics. Investors should be able to compare companies using measures that are transparent, widely understood and economically meaningful.

Over the coming months, we intend to continue refining our analytics framework and working with others across the sector to help improve consistency and comparability throughout the industry.

On Monday this week we announced an update to our ATM-style facility. We raised £145,670 (before expenses), equivalent to approximately £0.29 per share. The ATM-style facility continues to be an important part of our capital markets toolkit and provides us with valuable flexibility as we execute our strategy.

Throughout the week we continued sharing the remaining videos filmed at the Bitcoin Treasuries Unconference UK. As a reminder, early bird tickets for the 2027 event are available on our website.

Looking ahead, we have decided to rename the event series from Bitcoin Treasuries Unconference UK to Bitcoin Treasuries Conference UK. As we scale both the event and help scale the wider industry in the UK, we believe this name will be more familiar to a broader audience. The core spirit and format of the event will remain largely unchanged, but we believe this evolution will help us reach and engage a larger community.

I would also like to remind shareholders that we have an important vote at our General Meeting on 17 June. Shortly afterwards, we will announce the results via RNS. Thank you to everyone who has already taken the time to vote. Depending on your platform, there may still be an opportunity to submit your vote if you have not yet done so. Voting is an important part of share ownership, regardless of whether you vote for or against a resolution.

Finally, I would like to acknowledge that our share price is not currently performing as well as I would like. I cannot control the market, but I can control what we are building and the two certainly seem a little disconnected from where I am sitting.

While short-term market performance can be frustrating, my conviction in the direction of the business has never been stronger. I believe we are executing the right strategy, and I am excited about where we are heading. As our progress becomes more widely understood and the opportunity ahead of Smarter Web becomes clearer, I believe the market will recognise the value of what we are building.

Thank you for your support.

LSE: #SWC | OTCQB: $TSWCF | FRA: $3M8

5

31

1,119

SWC-Wiki retweeted

21h

While we’re still in this bear market, my conviction in SWC hasn’t changed.

You are more than welcome. It is right to ask these questions - and right to get answers. Appreciate the support.

2

1

15

547

SWC-Wiki retweeted

20h

I share the sentiment that we should aim to view the companies actions within the wider strategic context, rather than assessing each tiny move in isolation and framing it as “good” or “bad”.

Based on everything they have done since IPO, I trust the team to execute in the best interests of the shareholders.

I’m excited for the future 🚀🌙

Thanks for the question.

To date, our partner has done a good job executing the ATM, and we provide instructions around how we want it managed.

As our treasury strategy becomes more sophisticated, I would encourage shareholders to focus less on individual days or weeks and more on the long-term results we deliver. Ultimately, the metric that matters is whether we are increasing Bitcoin per share and creating value for shareholders over quarters and years, not whether a particular day's ATM activity was above or below a certain threshold.

Decisions around when and how to issue stock need to be viewed in the context of all the competing opportunities and challenges we face as a management team. There are many factors that influence those decisions, and it's important that we retain the flexibility to act in the best interests of the company and its shareholders.

I appreciate that shareholders want complete visibility into everything we do. We will always aim to be transparent, but there are practical limits to what we can disclose. In some cases, providing too much detail around execution can be counterproductive and may allow others to trade against the company's objectives.

As always, I would ask shareholders to judge us by our results. If, over time, we continue to grow Bitcoin per share and execute our strategy successfully, that is the most meaningful measure of whether we are making the right decisions.

8

3

29

1,580

SWC-Wiki retweeted

And we have liftoff.

Join me as I cover the latest with Andrew and Jesse.

@asjwebley @Croesus_BTC @smarterwebuk

Jun 12

Welcome back to The Bitcoin Treasuries Podcast.

Presented by Bitcoin Treasuries Media.

Today's guests are Jesse Myers and Andrew Webley of The Smarter Web Company.

We discuss the latest developments at @smarterwebuk including their recent change in how they show value, their recent public announcement, the Bitcoin Treasuries Unconference UK, and why people are losing their minds over Bitcoin Treasuries and Digital Credit.

Here's my conversation with @asjwebley and @Croesus_BTC.

1

7

31

2,021

SWC-Wiki retweeted

Really glad to have attended the inaugural, Bitcoin Treasuries Unconference, hosted by Bristol's own @smarterwebuk.

Thoroughly excellent line-up of speakers, interesting, insightful & engaging. Met some really awesome people.

I'll definitely be grabbing a ticket for '27.

Our highlight reel from the Bitcoin Treasuries Unconference UK is now live.

A day of insightful discussions and great conversations, bringing together the people shaping the future of Bitcoin treasury companies.

We’re also pleased to announce that 28th May 2027 will see the event return – this time as the Bitcoin Treasuries Conference UK – at Bristol Beacon.

Tickets are now available (link in comments).

LSE: #SWC | OTCQB: $TSWCF | FRA: $3M8

1

2

8

775

SWC-Wiki retweeted

Jun 13

28 views in 18 hours - Bitcoin 5 Daily: The Last 24 Hours Explained (June 12th)

Please give @matthewkerridge feed back good or bad and support his channel, once he gets this right he is going to do a weekly $SWC round up. However he is running at a loss with the cost of AI tokens out of his own pocket until he can generate an income to pay for the fees.

youtube.com/watch?v=gJ3lq_9S…

6

5

22

1,666

SWC-Wiki retweeted

Jun 12

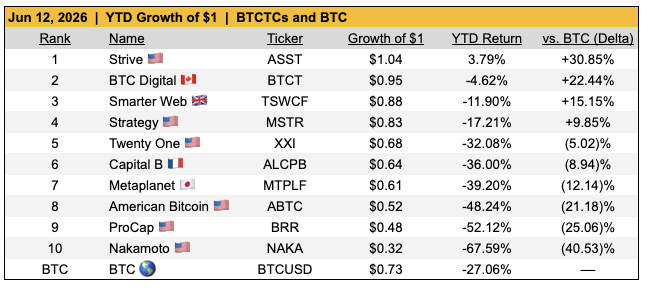

Ranking BTCTC YTD Growth of $1

6/12/26 Update:

BTC -27%

Strive 🇺🇸 4%

BTC Digital 🇨🇦 -5%

Smarter Web 🇬🇧 -12%

Others range from -17% to -68%

#1 $ASST 🔼1️⃣

#2 $BTCT 🔽1️⃣

#3 $TSWCF ↔️

#4 $MSTR ↔️

#5 $XXI ↔️

#6 $ALCPB ↔️

#7 $MTPLF ↔️

#8 $ABTC ↔️

#9 $BRR ↔️

#10 $NAKA ↔️

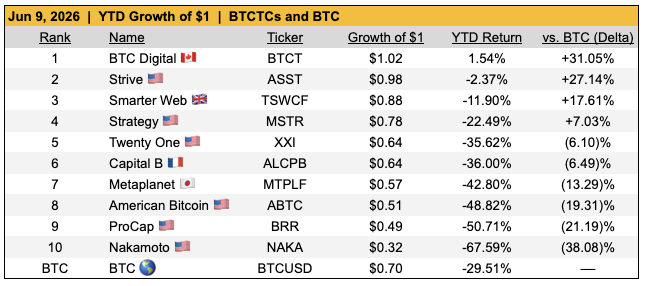

Jun 9

Ranking BTCTC YTD Growth of $1

6/9/26 Update:

In a year where $BTC is down 30%, Canada is somehow exporting gains. 🍁

BTC -30%

BTC Digital 🇨🇦 2%

Strive 🇺🇸 -2%

Smarter Web 🇬🇧 -12%

Others range from -22% to -68%

#1 $BTCT 🔼2️⃣

#2 $ASST 🔽1️⃣

#3 $TSWCF 🔽1️⃣

#4 $MSTR ↔️

#5 $XXI ↔️

#6 $ALCPB ↔️

#7 $MTPLF ↔️

#8 $ABTC ↔️

#9 $BRR ↔️

#10 $NAKA ↔️

2

6

433

SWC-Wiki retweeted

Jun 13

“TOBAM spoke to 100 companies and invested in 5” — @wildgoosejon .

That’s the calibre filter Smarter Web Company @smarterwebuk passed. The community already knew. Institutions are finally catching up.

Meanwhile, AI stole Bitcoin’s “fastest horse” crown and everyone here purely for number-go-up is panicking.

But nothing that actually matters changed: Bitcoin is still censorship-resistant, seizure-resistant, and absolutely scarce. The thesis didn’t break — the tourists just found a shinier ride.

The Fed has now hit peak hawkishness. Not “rates might stay higher for longer.” Peak. The next surprise can only be dovish from here. VIX curve is inverted. Everyone’s scared.

That’s not a warning. That’s a setup.

Kevin Warsh faces the impossible choice: defend the dollar → yields spike → debt spiral, or defend the bond market → dollar collapses → fiat crisis.

Bitcoin doesn’t care which one breaks first. It wins either way. Bitcoin is preeminent.

#Bitcoin #BTC #SWC

1

1

18

330

SWC-Wiki retweeted

Jun 13

Fully Focused ⬇️

Jun 13

Our ambition is to become one of the largest companies in the UK. I believe that our strategy gives us a credible path to achieving that goal.

At the centre of our approach is the balance sheet. We are building a balance sheet around what we believe is the best form of capital available: Bitcoin. As that balance sheet grows, it creates opportunities across the business. It can support the growth of our operating activities, enable strategic acquisitions, provide flexibility to pursue new opportunities as they emerge, and allow us to further strengthen and expand the balance sheet itself.

These are often viewed as separate strategies, but we do not see them that way. They are all connected. We have one strategy, and it revolves around building and intelligently deploying a strong balance sheet. Everything else flows from that foundation.

Because of this we think that it is important for investors and potential investors to understand this balance sheet at any moment in time and increasingly these investors include institutional investors who are used to specific metrics.

We believe the term "mNAV" is currently being used in ways that can create confusion rather than clarity. Various companies and commentators often calculate the metric differently. Some use Market Capitalisation as the numerator, while others use Enterprise Value. On the denominator side, some use Net Asset Value, while others use the market value of Bitcoin holdings, often referring to this as "BTC NAV" despite it being closer to a gross asset value than a true NAV calculation.

The treatment of outstanding securities is also a further element. We use the fully diluted number of shares which includes all in the money warrants and then factors in cash linked to the warrant proceeds, however if we were creating our analytics from the beginning, understanding everything that we know now, we would treat Smarter Convert as debt rather than an instrument that will convert into equity.

In traditional finance, mNAV generally refers to Market Capitalisation divided by Net Asset Value, producing a premium or discount multiple relative to NAV. However, many of the mNAV metrics currently used in the Bitcoin treasury company sector employ neither of these measures, resulting in a broad range of calculations that share the same label but convey very different information.

We believe this lack of standardisation becomes increasingly problematic as treasury companies introduce debt, preferred equity and other financing instruments. As capital structures become more complex, comparisons between companies become less meaningful if investors are not working from a common framework.

For this reason, we updated our analytics dashboard during the week and are moving away from mNAV as a primary valuation metric. Instead, we now display "Fully Diluted EV vs BTC Value", calculated as Fully Diluted Enterprise Value divided by the current market value of total Bitcoin holdings. We have also added charts that show “Net Bitcoin Value Per Fully Diluted Share” and “Net Sats Per Fully Diluted Share”. For all calculations on our analytics page, you can hover over the question marks and view the formulas.

In our view, this provides a completer and more transparent picture of the value of a Bitcoin treasury company. We believe investors should also consider several important measures, including leverage or amplification, Bitcoin per share growth over time ("Bitcoin Yield"), and the sustainability of that growth going forward. The last being harder to statistically analyse.

This naturally leads to another question we were asked this week: what is the single most important metric for evaluating a Bitcoin treasury company?

Our view is that there is no single number.

Our treasury objective is straightforward: to increase the amount of Bitcoin attributable to each share over time. However, we would encourage investors to assess performance over quarters and years rather than days or weeks. The key question is whether management decisions are increasing Bitcoin per share on a sustainable basis.

For a simple, ungeared treasury company, the analysis can appear relatively straightforward. One could argue that issuing shares is accretive whenever the value received exceeds the Bitcoin value attributable to the shares issued. However, the reality becomes considerably more nuanced once debt financing, debt repayment, warrant repurchases, share buybacks and other capital allocation decisions enter the equation.

A transaction that appears dilutive when viewed through one metric may in fact be accretive when viewed through another. This is precisely why we believe the industry requires better and more transparent analytics. As treasury strategies become more sophisticated, and treasury companies become much larger, investors need to consider multiple variables rather than relying on a single ratio or headline figure.

For public companies, such as The Smarter Web Company, there is an additional dimension. Investors should not only consider the Bitcoin treasury itself, but also operating revenues, corporate costs, cash generation and the broader business activities that sit alongside the treasury strategy. These elements can have a meaningful impact on the company's ability to grow Bitcoin per share over the long term.

If Bitcoin treasury companies are to mature into a recognised institutional asset class, the industry will benefit from greater consistency in reporting standards, valuation methodologies and performance metrics. Investors should be able to compare companies using measures that are transparent, widely understood and economically meaningful.

Over the coming months, we intend to continue refining our analytics framework and working with others across the sector to help improve consistency and comparability throughout the industry.

On Monday this week we announced an update to our ATM-style facility. We raised £145,670 (before expenses), equivalent to approximately £0.29 per share. The ATM-style facility continues to be an important part of our capital markets toolkit and provides us with valuable flexibility as we execute our strategy.

Throughout the week we continued sharing the remaining videos filmed at the Bitcoin Treasuries Unconference UK. As a reminder, early bird tickets for the 2027 event are available on our website.

Looking ahead, we have decided to rename the event series from Bitcoin Treasuries Unconference UK to Bitcoin Treasuries Conference UK. As we scale both the event and help scale the wider industry in the UK, we believe this name will be more familiar to a broader audience. The core spirit and format of the event will remain largely unchanged, but we believe this evolution will help us reach and engage a larger community.

I would also like to remind shareholders that we have an important vote at our General Meeting on 17 June. Shortly afterwards, we will announce the results via RNS. Thank you to everyone who has already taken the time to vote. Depending on your platform, there may still be an opportunity to submit your vote if you have not yet done so. Voting is an important part of share ownership, regardless of whether you vote for or against a resolution.

Finally, I would like to acknowledge that our share price is not currently performing as well as I would like. I cannot control the market, but I can control what we are building and the two certainly seem a little disconnected from where I am sitting.

While short-term market performance can be frustrating, my conviction in the direction of the business has never been stronger. I believe we are executing the right strategy, and I am excited about where we are heading. As our progress becomes more widely understood and the opportunity ahead of Smarter Web becomes clearer, I believe the market will recognise the value of what we are building.

Thank you for your support.

LSE: #SWC | OTCQB: $TSWCF | FRA: $3M8

1

2

17

504

SWC-Wiki retweeted

Jun 13

Our ambition is to become one of the largest companies in the UK. I believe that our strategy gives us a credible path to achieving that goal.

At the centre of our approach is the balance sheet. We are building a balance sheet around what we believe is the best form of capital available: Bitcoin. As that balance sheet grows, it creates opportunities across the business. It can support the growth of our operating activities, enable strategic acquisitions, provide flexibility to pursue new opportunities as they emerge, and allow us to further strengthen and expand the balance sheet itself.

These are often viewed as separate strategies, but we do not see them that way. They are all connected. We have one strategy, and it revolves around building and intelligently deploying a strong balance sheet. Everything else flows from that foundation.

Because of this we think that it is important for investors and potential investors to understand this balance sheet at any moment in time and increasingly these investors include institutional investors who are used to specific metrics.

We believe the term "mNAV" is currently being used in ways that can create confusion rather than clarity. Various companies and commentators often calculate the metric differently. Some use Market Capitalisation as the numerator, while others use Enterprise Value. On the denominator side, some use Net Asset Value, while others use the market value of Bitcoin holdings, often referring to this as "BTC NAV" despite it being closer to a gross asset value than a true NAV calculation.

The treatment of outstanding securities is also a further element. We use the fully diluted number of shares which includes all in the money warrants and then factors in cash linked to the warrant proceeds, however if we were creating our analytics from the beginning, understanding everything that we know now, we would treat Smarter Convert as debt rather than an instrument that will convert into equity.

In traditional finance, mNAV generally refers to Market Capitalisation divided by Net Asset Value, producing a premium or discount multiple relative to NAV. However, many of the mNAV metrics currently used in the Bitcoin treasury company sector employ neither of these measures, resulting in a broad range of calculations that share the same label but convey very different information.

We believe this lack of standardisation becomes increasingly problematic as treasury companies introduce debt, preferred equity and other financing instruments. As capital structures become more complex, comparisons between companies become less meaningful if investors are not working from a common framework.

For this reason, we updated our analytics dashboard during the week and are moving away from mNAV as a primary valuation metric. Instead, we now display "Fully Diluted EV vs BTC Value", calculated as Fully Diluted Enterprise Value divided by the current market value of total Bitcoin holdings. We have also added charts that show “Net Bitcoin Value Per Fully Diluted Share” and “Net Sats Per Fully Diluted Share”. For all calculations on our analytics page, you can hover over the question marks and view the formulas.

In our view, this provides a completer and more transparent picture of the value of a Bitcoin treasury company. We believe investors should also consider several important measures, including leverage or amplification, Bitcoin per share growth over time ("Bitcoin Yield"), and the sustainability of that growth going forward. The last being harder to statistically analyse.

This naturally leads to another question we were asked this week: what is the single most important metric for evaluating a Bitcoin treasury company?

Our view is that there is no single number.

Our treasury objective is straightforward: to increase the amount of Bitcoin attributable to each share over time. However, we would encourage investors to assess performance over quarters and years rather than days or weeks. The key question is whether management decisions are increasing Bitcoin per share on a sustainable basis.

For a simple, ungeared treasury company, the analysis can appear relatively straightforward. One could argue that issuing shares is accretive whenever the value received exceeds the Bitcoin value attributable to the shares issued. However, the reality becomes considerably more nuanced once debt financing, debt repayment, warrant repurchases, share buybacks and other capital allocation decisions enter the equation.

A transaction that appears dilutive when viewed through one metric may in fact be accretive when viewed through another. This is precisely why we believe the industry requires better and more transparent analytics. As treasury strategies become more sophisticated, and treasury companies become much larger, investors need to consider multiple variables rather than relying on a single ratio or headline figure.

For public companies, such as The Smarter Web Company, there is an additional dimension. Investors should not only consider the Bitcoin treasury itself, but also operating revenues, corporate costs, cash generation and the broader business activities that sit alongside the treasury strategy. These elements can have a meaningful impact on the company's ability to grow Bitcoin per share over the long term.

If Bitcoin treasury companies are to mature into a recognised institutional asset class, the industry will benefit from greater consistency in reporting standards, valuation methodologies and performance metrics. Investors should be able to compare companies using measures that are transparent, widely understood and economically meaningful.

Over the coming months, we intend to continue refining our analytics framework and working with others across the sector to help improve consistency and comparability throughout the industry.

On Monday this week we announced an update to our ATM-style facility. We raised £145,670 (before expenses), equivalent to approximately £0.29 per share. The ATM-style facility continues to be an important part of our capital markets toolkit and provides us with valuable flexibility as we execute our strategy.

Throughout the week we continued sharing the remaining videos filmed at the Bitcoin Treasuries Unconference UK. As a reminder, early bird tickets for the 2027 event are available on our website.

Looking ahead, we have decided to rename the event series from Bitcoin Treasuries Unconference UK to Bitcoin Treasuries Conference UK. As we scale both the event and help scale the wider industry in the UK, we believe this name will be more familiar to a broader audience. The core spirit and format of the event will remain largely unchanged, but we believe this evolution will help us reach and engage a larger community.

I would also like to remind shareholders that we have an important vote at our General Meeting on 17 June. Shortly afterwards, we will announce the results via RNS. Thank you to everyone who has already taken the time to vote. Depending on your platform, there may still be an opportunity to submit your vote if you have not yet done so. Voting is an important part of share ownership, regardless of whether you vote for or against a resolution.

Finally, I would like to acknowledge that our share price is not currently performing as well as I would like. I cannot control the market, but I can control what we are building and the two certainly seem a little disconnected from where I am sitting.

While short-term market performance can be frustrating, my conviction in the direction of the business has never been stronger. I believe we are executing the right strategy, and I am excited about where we are heading. As our progress becomes more widely understood and the opportunity ahead of Smarter Web becomes clearer, I believe the market will recognise the value of what we are building.

Thank you for your support.

LSE: #SWC | OTCQB: $TSWCF | FRA: $3M8

Jun 6

It has been a challenging week for Bitcoin, with the price experiencing one of its steepest weekly percentage declines since late 2022. However, investors should remember that volatility is an inherent characteristic of Bitcoin. It is also worth recalling that late 2022 marked the bottom of the previous bear market, before Bitcoin went on to reach new all-time highs.

While Bitcoin’s performance this year has fallen short of many investors’ expectations, periods of weakness have historically been followed by phases of renewed growth. Since its inception, Bitcoin has repeatedly overcome significant market corrections, regulatory concerns and macroeconomic challenges, ultimately rewarding investors who maintained a long-term perspective.

In fact, a number of institutional investors and asset managers have published research demonstrating that, despite its volatility, a modest allocation to Bitcoin has historically improved the risk-adjusted returns of traditional portfolios. One commonly used measure of risk-adjusted performance is the Sharpe ratio, which assesses how much return an investment generates relative to the volatility experienced to achieve those returns. While Bitcoin has often been one of the most volatile assets available to investors, its long-term returns have historically been sufficiently strong that, when combined with traditional assets, it has often improved overall portfolio efficiency rather than detracted from it.

Personally, I have a high allocation to Bitcoin and Bitcoin treasury companies at approximately 100% of my portfolio. I have always been open about this and it is what I am comfortable with as I attach little value to most other asset classes including cash. But, whilst not offering financial advice, I do think that everyone should have an allocation to Bitcoin and Bitcoin treasury companies. For most, who do not share my high conviction, perhaps somewhere between 1% and 10% is sensible.

There is currently considerable discussion around perpetual preferred equities as what may become one of the most important capital markets instruments available to Bitcoin treasury companies. Given the recent movement in Bitcoin's price, I thought it would be useful to explain these in the context of volatile price movements.

We have already reminded ourselves that Bitcoin is volatile. Despite that volatility, I believe it remains the best asset on which to build a corporate treasury. Equally, I believe that perpetual preferred equities represent one of the most attractive structures for raising permanent capital. It can appeal to yield-seeking investors while allowing the benefits generated from deploying that capital into Bitcoin to accrue to ordinary shareholders over time.

All forms of capital have a cost. With perpetual preferred equity, that cost is relatively straightforward to understand: the dividend commitment. The key question then becomes whether the return generated from the deployment of that capital exceeds its cost over time.

The Bitcoin treasury model is relatively simple in this regard.

For example, Strategy currently pays 11.5% on STRC and Strive pays 13% on SATA. Looking at Bitcoin's historical performance, the compound annual growth rate over the last 3, 5 and 10 years has been approximately 39%, 15% and 59% respectively.

£1 million invested three years ago would be worth approximately £2.26 million today.

£1 million invested five years ago would be worth approximately £2.00 million today.

£1 million invested ten years ago would be worth approximately £107 million today.

These figures illustrate an important point. While Bitcoin is volatile, the long-term historical growth rate has significantly exceeded the cost of capital represented by current perpetual preferred equity dividend rates.

Using the most conservative comparison above, if capital costs 13% per annum and the underlying asset compounds at 15% per annum, value is still being created over time. Of course, this is an intentionally simplified example and does not reflect all the complexities of a real corporate treasury model. However, it serves to illustrate the basic principle behind why a growing number of Bitcoin treasury companies view perpetual preferred equity as an attractive source of long-term capital.

Importantly, this approach seeks to minimise many of the challenges associated with other forms of financing while allowing a company to continue building its Bitcoin balance sheet, and increasing Bitcoin per share, over extended periods of time.

It is important to note that historical performance does not guarantee future results. The figures above are provided solely to illustrate the relationship between the cost of capital and Bitcoin's historical long-term growth rates and should not be interpreted as a forecast of future Bitcoin performance.

On Friday last week, we held the inaugural Bitcoin Treasury Unconference. I have received a great deal of positive feedback since then, and we have now released the individual videos, along with photographs from the event, on our website for everyone to enjoy. We will be holding the event again next year and early bird tickets are already available via our website. Thank you to everyone who attended, spoke at or sponsored the event.

On Monday this week, we released two announcements.

Firstly, we updated the market regarding warrants exercised since the pre-IPO warrant window was opened. Today, there are just 8,075,600 of these pre-IPO warrants held by external investors. When we listed the business, and Bitcoin treasury companies were far less understood than they are today, these warrants formed an important part of our route to becoming a public company. I am pleased that the warrant overhang has now been substantially reduced.

The second RNS on Monday related to a proposed capital reduction and notice of general meeting. There has been speculation online regarding the reasons behind this proposal and I would encourage shareholders to refer to the official announcement for the company's comments.

I would also like to ask every shareholder to vote their shares if they have not already done so. Whether you support or oppose a proposal, exercising your right to vote is an important part of being a shareholder. We hope that you will support this important resolution.

On Tuesday I had an update session with Squarebird, the business we acquired earlier this year using approximately 1% of our balance sheet enabling us to significantly grow our revenues. I am delighted with the progress they are making on growing the business and look forward to the hard work the team are putting into the projects developing into figures which will then be released in future updates we announce. We are lucky to have such a good business as part of our group.

For the remainder of the week, we made only two further announcements, both relating to updated TR-1 notifications from 210k Capital, LP. 210k have been a shareholder since the start of our journey and we are pleased to have Tyler Evans also on our board. These notifications were required because of our increased number of shares in issue and a change of ownership of their parent company. The quantity of shares held by 210k Capital has not changed; only its percentage ownership has changed. Under UK listing rules, significant shareholders must notify the company when certain percentage thresholds are crossed, and the company must then update the market accordingly.

Our team has been working exceptionally hard this week. Our focus remains on driving forward the various projects that we are working on, and I appreciate that it can sometimes be frustrating for shareholders not to know everything that is happening behind the scenes. However, we will disclose developments at the appropriate time and, in my view, the direction in which we are heading is the right one for the success of the business.

We are fortunate to have one of the most supportive shareholder communities in the Bitcoin treasury space. We will continue pushing forward every day, with speed, discipline and precision, as we work to build what we believe Smarter Web can become.

Thank you for your continued support; I never take that support for granted. We are working hard every day to justify the trust you place in us, and I look forward to updating you on our progress as we move forward.

LSE: #SWC | OTCQB: $TSWCF | FRA: $3M8

28

18

127

9,734

SWC-Wiki retweeted

Jun 12

The Bitcoin Treasuries Conference UK at the Bristol Beacon is born.

Our highlight reel from the Bitcoin Treasuries Unconference UK is now live.

A day of insightful discussions and great conversations, bringing together the people shaping the future of Bitcoin treasury companies.

We’re also pleased to announce that 28th May 2027 will see the event return – this time as the Bitcoin Treasuries Conference UK – at Bristol Beacon.

Tickets are now available (link in comments).

LSE: #SWC | OTCQB: $TSWCF | FRA: $3M8

2

17

666

SWC-Wiki retweeted

Jun 13

I thought this was a pretty good summary of what being a common shareholder means in a company also offering perpetual preferreds.

For the same reason, I’m happy to hold SWC common stock.

Being an MSTR shareholder feels a lot like being a venture capitalist.

Not because the company is a startup.

But because of where you sit in the capital structure.

The preferred shareholders get paid first.

The bondholders get paid first.

The lenders get paid first.

Common shareholders are last.

You’re the shock absorber.

You’re the one who takes the volatility.

You’re the one who watches 30%, 40%, and 50% drawdowns.

You’re the one everybody laughs at when things get ugly.

But there’s a reason venture capitalists accept that risk.

Because the common equity holder is also the one with the greatest upside.

The preferred shares have a ceiling.

The debt has a ceiling.

The lenders have a ceiling.

Common equity does not.

As a regular investor, I don’t get access to SpaceX private rounds.

I don’t get access to Anthropic.

I don’t get access to the next billion-dollar venture deal before everyone else.

But through MSTR, I get exposure to a high-risk, high-volatility equity where the upside is theoretically uncapped.

That’s the trade.

You can’t demand venture-capital upside while demanding treasury-bill risk.

The reward exists because the risk exists.

If you’re not comfortable being the last one in line during difficult times, you won’t be around long enough to benefit from being first in line when value is created.

That’s why most people won’t hold MSTR.

And that’s precisely why the opportunity exists. ₿

2

21

729

SWC-Wiki retweeted

Jun 12

👇🔥🔥🔥

Jun 12

Welcome back to The Bitcoin Treasuries Podcast.

Presented by Bitcoin Treasuries Media.

Today's guests are Jesse Myers and Andrew Webley of The Smarter Web Company.

We discuss the latest developments at @smarterwebuk including their recent change in how they show value, their recent public announcement, the Bitcoin Treasuries Unconference UK, and why people are losing their minds over Bitcoin Treasuries and Digital Credit.

Here's my conversation with @asjwebley and @Croesus_BTC.

1

2

17

848

SWC-Wiki retweeted

Jun 12

Welcome back to The Bitcoin Treasuries Podcast.

Presented by Bitcoin Treasuries Media.

Today's guests are Jesse Myers and Andrew Webley of The Smarter Web Company.

We discuss the latest developments at @smarterwebuk including their recent change in how they show value, their recent public announcement, the Bitcoin Treasuries Unconference UK, and why people are losing their minds over Bitcoin Treasuries and Digital Credit.

Here's my conversation with @asjwebley and @Croesus_BTC.

9

14

73

10,133

SWC-Wiki retweeted

Jun 12

$SWC just got real close. Actually their Net BPS os even more strict than CEBE because it uses fully dilluted share count

1

3

16

443