Private investor. Investment views, strategies, stocks held and actions taken based on personal financial goals for retirement. It should NOT be taken as advice

Joined August 2011

- Tweets 7,471

- Following 2,343

- Followers 2,800

- Likes 16,414

16 Photos and videos

Pinned Tweet

Jan 1

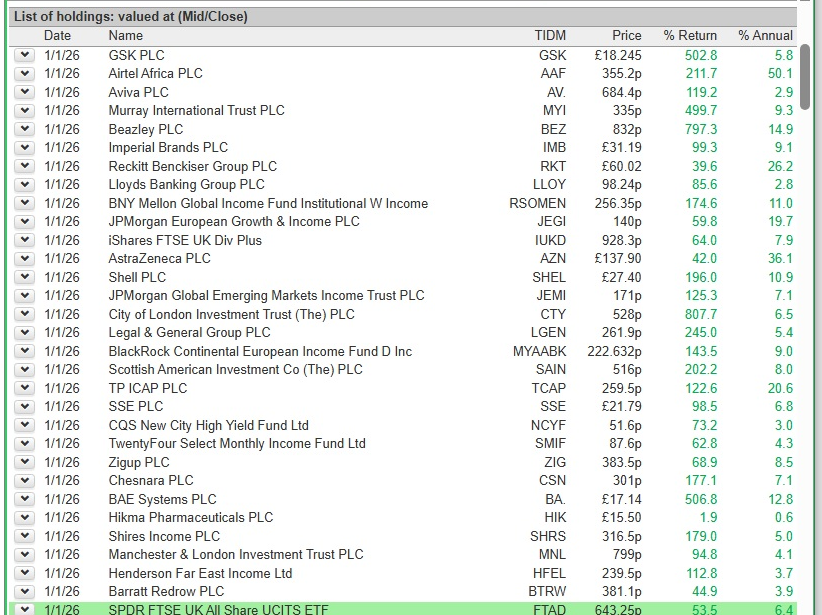

Top 30 equity holdings ending Q4 2025; GSK, AAF, AV., MYI, BEZ, IMB, RKT, LLOY, RSOMEN, JEGI, IUKD, AZN, SHEL, JEMI, CTY, LGEN, MYAABK, SAIN, TCAP, SSE, NCYF, SMIF, ZIG, CSN, BA., HIK, SHRS, MNL, HFEL, BTRW. Totals 58.13% of portfolio (64.61% at Q4 2024). #smidd2025

1

15

1,482

May 29

Big sudden volume/move in one of my minnows #VTU so is this Constellation Automotive Group making a move? they already have 11%. Well no announcements yet.

3

8,344

May 28

#MNL hit a new ATH yesterday and is still £3 off NAV. But what interests me more is there appears to have been some major changes in top holdings, so I will be looking to the May factsheet to confirm and get manager commentary. I have been a long term holder.

1

6

428

May 19

Just catching up on paperwork I note pleasingly that AJ Bell @Investcentre have dropped the £1.50p charge for regular monthly reinvestment. A minor charge but it all added up over time, a boost and incentive for small investors. Effort I think to match @ii_couk competitive edge.

3

15

779

Sandy retweeted

🔥 #TWINPETESINVESTING #Podcast 179: INVESTING OPPORTUNITIES with WINNING POTENTIAL📈#ABDN #BA. #SMT #QQ. #GRG #PCTN #LMP #SREI #HRI #SPACEX #ENSI #ALL #ITRK #REITS #Dividends #TAKEOVERS & Hidden Gems💎

conkers3.com/twin-petes-inve…

open.spotify.com/episode/0s2…

youtu.be/Ha4L9YcYA1w?si=ywIq…

6

4

14

13,844

May 16

Been away from market this week, but #AAF worthy of mention on fall of ~10% this week after a control swap transaction gives largest holder 79%, no dilution but possible minority or taking private concerns ahead of Africa Money float. Folio down ~0.2% this week, YTD up ~6.2%.

1

7

630

May 11

As @Keir_Starmer doubles down on rebuilding European relationship, @UKLabour clearly don't understand why @reformparty_uk got so many votes in labour strongholds and beyond.

6

253

May 9

People voted for @reformparty_uk for many different reasons and it can't just be hate Starmer. Serious analysis required, and in the meantime @UKLabour MPs will see it as more socialism required. More tax, more benefits, wasteful spending, spiralling pay awards = economy screwed.

7

245

Apr 17

#SSE hit by Reeves and Miliband plans for change in charging structure, splitting electricity and gas pricing. Can understand market worries, but I have been accumulating and a further BUY today at £24.54 pushes me toward my long term target holding.

4

369

Mar 30

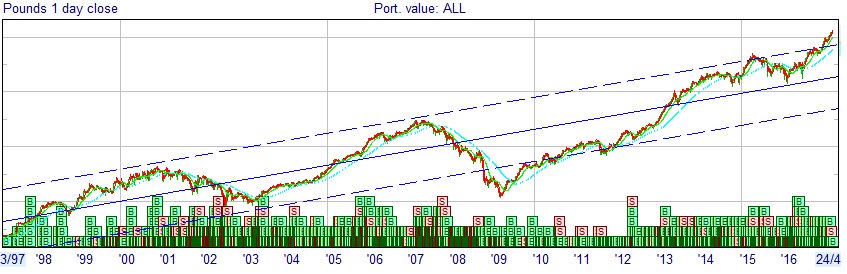

Apart from an intra-day dip into -ve territory last Monday, portfolio regained and held ve YTD gains to end week, even though just under 1%. Some further negativity seems likely as Trump briefs possible Iran invasion. Adding not selling.

1

11

537