Joined June 2024

- Tweets 55

- Following 13

- Followers 132

- Likes 167

20 Photos and videos

🚨 𝐋𝐀𝐍𝐃𝐄𝐑 𝐖𝐄𝐒𝐓 #FDR #GOLD

I’m standing on the red dirt of the Lander West gold target, 250km northwest of Alice Springs, and the silence is about to be shattered.

𝐅𝐢𝐫𝐬𝐭 𝐃𝐞𝐯𝐞𝐥𝐨𝐩𝐦𝐞𝐧𝐭 𝐑𝐞𝐬𝐨𝐮𝐫𝐜𝐞𝐬 (AIM: FDR) has just completed its final pre-mobilisation reconnaissance.

Drill-holes are refined, the earthworks contractor is locked in, and the rig from GeoDrill Australia is already working next door on Itech Minerals’ ground.

For the first time, this quiet corner of the Northern Territory’s Stafford Gold Trend is about to be properly tested, and at a market capitalisation of just £4M; 𝐭𝐡𝐞 𝐥𝐞𝐯𝐞𝐫𝐚𝐠𝐞 𝐨𝐧 𝐨𝐟𝐟𝐞𝐫 𝐢𝐬 𝐭𝐡𝐞 𝐤𝐢𝐧𝐝 𝐨𝐟 𝐨𝐩𝐩𝐨𝐫𝐭𝐮𝐧𝐢𝐭𝐲 𝐩𝐫𝐢𝐯𝐚𝐭𝐞 𝐢𝐧𝐯𝐞𝐬𝐭𝐨𝐫𝐬 𝐝𝐫𝐞𝐚𝐦 𝐚𝐛𝐨𝐮𝐭.

Let’s put that £4M into perspective.

With 139.2 million shares in issue, and a share price of 2.85p, FDR is obscenely undervalued. Yet the company is fully-funded for a maiden reverse-circulation drilling programme that will test a target with the geological hallmarks of a multi-million-ounce gold system.

If even the first-pass drilling delivers a discovery, that £4M valuation could be a footnote in a much bigger story.

Meanwhile, astute investors will have noticed the steady drip of stock being fed onto the tape in recent weeks.

𝐅𝐢𝐫𝐬𝐭 𝐄𝐪𝐮𝐢𝐭𝐲 has been acting for Armstrong Investments, a shareholder that accumulated a meaningful position between November 2025 and March 2026. That holding topped out at 6.25%, but since March, the position has been gradually unwound. Today, it sits at just 3% (~4.2 million shares).

The beauty of the 3% threshold is that it represents the floor for the UK’s major shareholding notification regime. Once a stake dips below that line, no further TR1 disclosures are required.

More importantly though, the evidence suggests the heavy lifting is already done. The stock has been absorbing this supply without falling over; in fact, the shares have been gently rising into the news flow.

The remaining rump is small enough to be cleared in a couple of trading days, and with the overhang now largely behind us, the path is clear for the drilling catalysts to do their work.

But back to the investment case here. FDR isn’t chasing a few grams per tonne of oxide gold. The team is hunting a large, structurally controlled, intrusive-related gold system; the kind of deposit that can underpin a standalone mining operation.

The integrated geophysical interpretation completed earlier this year revealed a mineralised corridor stretching over 3km at Lander West, with multiple high-order chargeability and resistivity anomalies sitting directly beneath a coherent gold-in-soil footprint.

That footprint peaks at over 100ppb Au and sits exactly on the intersection of the deep-crustal Stafford Fault and a set of oblique cross-structures → 𝐭𝐡𝐞 𝐬𝐚𝐦𝐞 𝐚𝐫𝐜𝐡𝐢𝐭𝐞𝐜𝐭𝐮𝐫𝐞 𝐭𝐡𝐚𝐭 𝐡𝐨𝐬𝐭𝐬 𝐦𝐮𝐥𝐭𝐢-𝐦𝐢𝐥𝐥𝐢𝐨𝐧-𝐨𝐮𝐧𝐜𝐞 𝐝𝐞𝐩𝐨𝐬𝐢𝐭𝐬 𝐞𝐥𝐬𝐞𝐰𝐡𝐞𝐫𝐞 𝐢𝐧 𝐭𝐡𝐞 𝐓𝐞𝐧𝐧𝐚𝐧𝐭 𝐂𝐫𝐞𝐞𝐤-𝐌𝐭 𝐈𝐬𝐚 𝐢𝐧𝐥𝐢𝐞𝐫.

So what does all this mean?

Internally, the company is cautious, but the scale is writ large. 𝐀 𝟑𝐤𝐦-𝐥𝐨𝐧𝐠 𝐜𝐨𝐧𝐝𝐮𝐜𝐭𝐨𝐫 𝐰𝐢𝐭𝐡 𝐰𝐢𝐝𝐭𝐡𝐬 𝐨𝐟 𝟐𝟎𝟎𝐦 𝐭𝐨 𝟒𝟎𝟎𝐦, 𝐦𝐨𝐝𝐞𝐥𝐥𝐞𝐝 𝐟𝐫𝐨𝐦 𝐬𝐮𝐫𝐟𝐚𝐜𝐞 𝐭𝐨 𝟑𝟎𝟎𝐦 𝐝𝐞𝐩𝐭𝐡, 𝐬𝐮𝐠𝐠𝐞𝐬𝐭𝐬 𝐚 𝐜𝐨𝐧𝐜𝐞𝐩𝐭𝐮𝐚𝐥 𝐞𝐱𝐩𝐥𝐨𝐫𝐚𝐭𝐢𝐨𝐧 𝐭𝐚𝐫𝐠𝐞𝐭 𝐨𝐟 𝐛𝐞𝐭𝐰𝐞𝐞𝐧 𝟏𝟓 𝐚𝐧𝐝 𝟐𝟓 𝐦𝐢𝐥𝐥𝐢𝐨𝐧 𝐭𝐨𝐧𝐧𝐞𝐬 𝐚𝐭 𝐚 𝐠𝐫𝐚𝐝𝐞 𝐨𝐟 𝟏.𝟓 𝐭𝐨 𝟐.𝟓 𝐠/𝐭 𝐠𝐨𝐥𝐝.

That’s a 𝟏.𝟓 𝐭𝐨 𝟑 𝐦𝐢𝐥𝐥𝐢𝐨𝐧-𝐨𝐮𝐧𝐜𝐞 𝐬𝐲𝐬𝐭𝐞𝐦 if everything comes together.

These aren’t pie-in-the-sky figures. They’re derived from the same geophysical signatures that led to the discovery of the nearby 1.8Moz Warrego deposit and the high-grade Golden Forty mine.

Now consider this: a discovery hole of, say, 20 metres at 3 g/t gold from 80 metres depth, perfectly achievable given the geochemical and geophysical data, would instantly transform sentiment.

Peers with comparable hits in the Northern Territory routinely trade at market caps of £20-30M. For FDR, that would imply a share price of 𝟏𝟒-𝟐𝟏𝐩; 𝐚 𝐫𝐞𝐭𝐮𝐫𝐧 𝐨𝐟 𝟓 𝐭𝐨 𝟕 𝐭𝐢𝐦𝐞𝐬 𝐭𝐡𝐞 𝐜𝐮𝐫𝐫𝐞𝐧𝐭 𝐥𝐞𝐯𝐞𝐥.

And that is just the re-rate on the first decent intersection.

A multi-hole campaign confirming a broad zone of mineralisation could attract a mid-tier suitor hungry for Australian ounces in one of the world’s last great underexplored gold frontiers.

And the neighbouring catalyst adds an extra layer of excitement.

𝐈𝐭𝐞𝐜𝐡 𝐌𝐢𝐧𝐞𝐫𝐚𝐥𝐬 (ASX: ITM) is about to commence its own drilling campaign at the Golden Gate prospect, a few hundred metres from FDR’s boundary along the Stafford Gold Trend.

Golden Gate already boasts historical intercepts such as 14m at 9.8 g/t Au, and Itech’s programme is designed to extend that mineralisation down-plunge and test a large induced-polarisation anomaly at depth.

𝐈𝐧 𝐞𝐟𝐟𝐞𝐜𝐭, 𝐈𝐭𝐞𝐜𝐡 𝐢𝐬 𝐝𝐫𝐢𝐥𝐥𝐢𝐧𝐠 𝐭𝐡𝐞 𝐧𝐨𝐫𝐭𝐡𝐞𝐫𝐧 𝐞𝐱𝐭𝐞𝐧𝐬𝐢𝐨𝐧 𝐨𝐟 𝐭𝐡𝐞 𝐯𝐞𝐫𝐲 𝐬𝐚𝐦𝐞 𝐬𝐭𝐫𝐮𝐜𝐭𝐮𝐫𝐚𝐥 𝐜𝐨𝐫𝐫𝐢𝐝𝐨𝐫 𝐭𝐡𝐚𝐭 𝐅𝐃𝐑 𝐰𝐢𝐥𝐥 𝐛𝐞 𝐩𝐫𝐨𝐛𝐢𝐧𝐠 𝐨𝐧 𝐢𝐭𝐬 𝐨𝐰𝐧 𝐠𝐫𝐨𝐮𝐧𝐝.

If Itech hits a meaningful sulphide zone, the spotlight on the entire trend, and on FDR’s fully funded Phase I programme, will intensify overnight.

Two junior explorers drilling simultaneously on adjacent tenements, chasing a district-scale gold system that has never been systematically explored at depth: it’s the kind of scenario that gets pulses racing among resource investors and can create a rising tide that lifts both boats.

And things are moving apace.

TMAE, the Alice Springs-based earthworks contractor, has already began cutting access tracks and drill pads.

GeoDrill Australia, already operating on Itech’s ground, will mobilise the RC rig with minimal downtime.

Environmental permits are signed, land access agreements are in place, and the bank account is topped-up.

𝐅𝐃𝐑 𝐢𝐬 𝐝𝐞-𝐫𝐢𝐬𝐤𝐞𝐝 𝐚𝐧𝐝 𝐫𝐞𝐚𝐝𝐲 𝐭𝐨 𝐝𝐫𝐢𝐥𝐥.

For the private investor, the narrative is brutally simple; A tightly held AIM explorer, backed by real science, is about to drill a high-conviction gold target that could define a new district. The shares trade at 2.85p, giving a market cap of just under £4M.

The protracted seller that has lingered over the stock for weeks is now down to its last few million shares and may well have walked away for good → leaving a clean register and a fully-funded drill programme ahead.

The company is fully funded, so there is no imminent dilution. The neighbours are drilling concurrently, which means a steady flow of news and a growing wave of district recognition.

And the geological model points towards a prize that could be measured in millions of ounces.

𝐁𝐎𝐓𝐓𝐎𝐌 𝐋𝐈𝐍𝐄

✅ The kit is mobilising.

✅ The ground is prospective.

✅ The neighbours are drilling.

✅ The geophysics is compelling.

✅ The overhang has pretty much cleared.

✅ And the stock is priced as if nothing is about to happen.

Thus, if you’re looking for an asymmetric exploration bet with the potential to deliver a life-changing return, you might want to take a long, hard look at FDR at 2.85p → before the drill bit turns.

3

10

4,807

🚨 𝐓𝐑𝐎𝐔𝐁𝐋𝐄 𝐁𝐄𝐇𝐈𝐍𝐃, 𝐓𝐑𝐄𝐀𝐒𝐔𝐑𝐄 𝐀𝐇𝐄𝐀𝐃: #ARCM #ARCMINERALS

For close to three years, Arc Minerals has been a story defined by what it couldn't do (explore freely) rather than what it could.

Today, that story just changed.

The company dropped an RNS that sent its shares surging 25% on the day: It has settled every outstanding legal dispute in Zambia → 𝐭𝐞𝐫𝐦𝐢𝐧𝐚𝐭𝐢𝐧𝐠 𝐞𝐢𝐠𝐡𝐭 𝐬𝐞𝐭𝐬 𝐨𝐟 𝐩𝐫𝐨𝐜𝐞𝐞𝐝𝐢𝐧𝐠𝐬 𝐚𝐜𝐫𝐨𝐬𝐬 𝐦𝐮𝐥𝐭𝐢𝐩𝐥𝐞 𝐜𝐨𝐮𝐫𝐭𝐬 𝐚𝐧𝐝 𝐭𝐫𝐢𝐛𝐮𝐧𝐚𝐥𝐬, 𝐞𝐱𝐭𝐢𝐧𝐠𝐮𝐢𝐬𝐡𝐢𝐧𝐠 𝐚𝐥𝐥 𝐩𝐚𝐬𝐭, 𝐩𝐫𝐞𝐬𝐞𝐧𝐭, 𝐚𝐧𝐝 𝐟𝐮𝐭𝐮𝐫𝐞 𝐜𝐥𝐚𝐢𝐦𝐬 𝐛𝐞𝐭𝐰𝐞𝐞𝐧 𝐭𝐡𝐞 𝐩𝐚𝐫𝐭𝐢𝐞𝐬, 𝐚𝐧𝐝 𝐝𝐞𝐥𝐢𝐯𝐞𝐫𝐢𝐧𝐠 𝐜𝐥𝐞𝐚𝐧, 𝐮𝐧𝐝𝐢𝐬𝐩𝐮𝐭𝐞𝐝 𝐭𝐢𝐭𝐥𝐞 𝐭𝐨 𝐢𝐭𝐬 𝐤𝐞𝐲 𝐙𝐚𝐦𝐛𝐢𝐚𝐧 𝐥𝐢𝐜𝐞𝐧𝐜𝐞.

For the patient investor who has watched this share price tumble from 1.70p in February 2025 to as low as 0.34p last week, a brutal 80% decline, this is the moment the overhang lifts.

And the thesis for owning ARCM is no longer just about what's been resolved, but about what lies beneath the ground.

1️⃣ 𝐓𝐇𝐄 𝐒𝐄𝐓𝐓𝐋𝐄𝐌𝐄𝐍𝐓: 𝐖𝐇𝐀𝐓 𝐈𝐓 𝐌𝐄𝐀𝐍𝐒 𝐈𝐍 𝐏𝐋𝐀𝐈𝐍 𝐄𝐍𝐆𝐋𝐈𝐒𝐇

𝐓𝐡𝐞 𝐏𝐫𝐨𝐛𝐥𝐞𝐦: Arc Minerals has been entangled in a web of litigation with ZAMEX, Lunda Resources (formerly Zamsort), and an individual named Mumena Mushinge. The disputes centred on competing claims over exploration licences in Zambia, and most critically, 𝐋𝐢𝐜𝐞𝐧𝐜𝐞 𝟏𝟗𝟗𝟎𝟔-𝐇𝐐-𝐋𝐄𝐋, held by Arc's subsidiary Handa Resources.

At various points, Arc faced injunctions, writs, and consent judgments that clouded its ownership and distracted management. The company described some of these claims as "vexatious" and "without merit," but the simple reality was that the legal overhang made it impossible for the market to price Arc's assets with any confidence.

𝐓𝐡𝐞 𝐒𝐨𝐥𝐮𝐭𝐢𝐨𝐧: The Settlement Agreement achieves four things:

✅ All eight sets of proceedings are terminated by consent. No more court dates, no more legal bills, no more uncertainty.

✅ Mutual releases: each party "irrevocably and unconditionally" releases the others from any and all claims, past, present, or future, anywhere in the world. This is the legal equivalent of a clean slate.

✅ Licence clarity: Lunda formally renounces all claims to Arc's Licence 19906-HQ-LEL. Arc, in turn, walks away from any interest in Licence 41777-HQ-LEL → a 42.5 square kilometre parcel originally carved out of Handa's wider licence area, but which management describes as "immaterial."

✅ A deferred payment of US$200,000 falls due only if Lunda delivers a JORC-compliant Measured Resource of at least 30 million tonnes at 1.5% copper on that licence by 31 December 2031. If they don't, Arc pays nothing. This is not a liability that should trouble shareholders. It's a success-based kicker on a licence Arc doesn't even own.

Rémy Welschinger, Arc's CEO, captured the mood succinctly: "I am very pleased that we have successfully reached a comprehensive and final resolution of all outstanding legal disputes in Zambia. This settlement allows us to focus entirely on advancing our exploration and development activities across Botswana and Zambia."

𝐖𝐡𝐲 𝐭𝐡𝐞 𝐦𝐚𝐫𝐤𝐞𝐭 𝐜𝐡𝐞𝐞𝐫𝐞𝐝. Zambian litigation has been the single biggest discount factor on ARCM's share price. With it removed, the market can begin to value the company on the basis of its copper exploration portfolio and not its legal bills.

2️⃣ 𝐓𝐇𝐄 𝐆𝐀𝐏 𝐓𝐇𝐀𝐓 𝐍𝐄𝐄𝐃𝐒 𝐓𝐎 𝐁𝐄 𝐅𝐈𝐋𝐋𝐄𝐃: 𝐀 𝐂𝐇𝐀𝐑𝐓𝐈𝐒𝐓'𝐒 𝐏𝐄𝐑𝐒𝐏𝐄𝐂𝐓𝐈𝐕𝐄

ARCM's 52-week range tells you everything about the journey shareholders have endured.

The stock hit 1.70p in February 2025, driven by a combination of the Anglo American joint venture excitement and broader copper market enthusiasm.

From there, it was a near-uninterrupted slide: 0.34p by last week; a decline of 80% from peak to trough.

Today's 25% jump, taking the shares to approximately 0.50p, begins to close a vast valuation gap.

To visualise this: on a weekly chart, the decline from 1.70p to 0.34p creates a gap spanning roughly 1.25p.

Even after today's move, the shares sit at less than half their 2025 high. The next significant technical resistance sits at the 1.00p level, a psychologically important round number that also represents a 50% retracement of the prior decline.

Above that, the 1.20–1.30p zone, where the stock consolidated in mid-2025, forms the next target.

What makes this gap compelling is that it was created not by a deterioration in the underlying asset base, but by sentiment and legal risk.

The rocks in the ground haven't changed. The copper price has. And the legal risk has now been extinguished. When a stock falls on a solvable problem and that problem gets solved, the recovery can be swift.

3️⃣ 𝐁𝐄𝐘𝐎𝐍𝐃 𝐓𝐇𝐄 𝐇𝐄𝐀𝐃𝐋𝐈𝐍𝐄𝐒: 𝐖𝐇𝐀𝐓 𝐀𝐑𝐂 𝐀𝐂𝐓𝐔𝐀𝐋𝐋𝐘 𝐎𝐖𝐍𝐒

The settlement is the catalyst, but the real story lies in Arc's project portfolio.

𝐊𝐚𝐛𝐨𝐦𝐩𝐨 𝐖𝐞𝐬𝐭(𝐙𝐚𝐦𝐛𝐢𝐚) → The Flagship. This is Arc's crown jewel: a 680-square-kilometre exploration footprint straddling the western flank of the Kabompo Dome in the Western Domes region of the Central African Copperbelt.

To put that in context, 680km² is larger than the entire city of Toronto. It sits in the same geological neighbourhood as First Quantum's Sentinel and Kansanshi mines, and Barrick's Lumwana → all Tier 1 operations.

Previous work, including geophysics, soil sampling, and drilling, confirmed widespread copper mineralisation across the licence. The joint venture with Anglo American may have ended in 2025, but that departure was not a commentary on the ground's prospectivity.

Anglo spent meaningful exploration dollars here before making a portfolio-level decision. The data Arc retains from that programme is, by itself, a valuable asset; one that a future partner or acquirer would pay handsomely to replicate.

𝐕𝐢𝐫𝐠𝐨 𝐏𝐫𝐨𝐣𝐞𝐜𝐭(𝐁𝐨𝐭𝐬𝐰𝐚𝐧𝐚) → The Near-Term Catalyst. In Botswana's Kalahari Copper Belt, Arc holds a 75% interest in the Virgo Project, covering over 210 square kilometres along the same MMG Zone 5 corridor that hosts the recently commissioned Khoemacau copper mine.

In March 2026, Arc commenced a ground-based magnetic and Induced Polarisation (IP) survey aimed at defining up to 15 kilometres of the D'kar–Ngwako Pan formation contact; the key host structure for all known copper deposits in the belt.

Results from that survey are expected by the end of Q2 2026. Positive chargeability anomalies, combined with existing drilling data confirming mineralisation, could rapidly de-risk Virgo and attract the attention of nearby operators MMG and Cupric Canyon Capital.

4️⃣ 𝐓𝐇𝐄 𝐌𝐀𝐂𝐑𝐎 𝐓𝐀𝐈𝐋𝐖𝐈𝐍𝐃: 𝐂𝐎𝐏𝐏𝐄𝐑'𝐒 𝐒𝐓𝐑𝐔𝐂𝐓𝐔𝐑𝐀𝐋 𝐃𝐄𝐅𝐈𝐂𝐈𝐓

It's one thing to own prospective copper ground. It's another to own it at a moment when the world is desperately short of copper.

UBS recently upgraded its copper price forecasts, targeting US13,200 per tonne (£10,400/t) for 2026.

The drivers are structural: underinvestment in new mines, declining ore grades at mature operations, and demand growth from electrification, grid infrastructure, and renewable energy buildout. This is not a cyclical spike. It is a secular supply shortfall that may persist for years.

For Arc, the implication is clear: every pound of copper it can prove up in the ground becomes more valuable with each passing quarter.

5️⃣ 𝐕𝐀𝐋𝐔𝐀𝐓𝐈𝐎𝐍: 𝐖𝐇𝐀𝐓'𝐒 𝐓𝐇𝐄 𝐅𝐀𝐈𝐑 𝐏𝐑𝐈𝐂𝐄 𝐅𝐎𝐑 𝐀𝐑𝐂𝐌?

This is where the arithmetic gets genuinely interesting, and where the opportunity for a multi-bagger return starts to take shape.

With the shares closing at 0.50p, up 25% on the day, and 2,459,587,314 shares in issue, Arc Minerals carries a market capitalisation of approximately £12.3 million.

Adjusting for the modest net cash position the Company held at its last reporting date, the enterprise value sits at roughly £11.8 million.

𝐂𝐨𝐧𝐬𝐢𝐝𝐞𝐫 𝐰𝐡𝐚𝐭 𝐭𝐡𝐚𝐭 𝐬𝐮𝐦 𝐛𝐮𝐲𝐬 𝐲𝐨𝐮 𝐭𝐨𝐝𝐚𝐲:

✅A 680-square-kilometre exploration footprint in the heart of Zambia's Copperbelt.

✅ 210-square-kilometre project in Botswana's Kalahari Copper Belt sitting along the same structural corridor as the Khoemacau mine.

✅A clean balance sheet with negligible debt.

✅An experienced management team that has navigated the Company through a multi-year legal labyrinth, and, critically.

✅Not a single ongoing court case to distract from the drill bit.

Junior explorers with district-scale land positions in proven copper belts routinely command market capitalisations of £25 million to £65 million before delivering a maiden resource.

The discount applied to ARCM has been almost entirely a function of perceived legal and jurisdictional risk.

With that risk now extinguished, the gap between Arc's market value and the value implied by its asset base should begin to close.

4

6

13

2,262

🚨 𝐃𝐈𝐒𝐂𝐎𝐍𝐍𝐄𝐂𝐓𝐄𝐃 #ATERIAN #ATN

Let me paint you a picture of London's junior mining market in Q2 2026;

🟢 Altona Rare Earths PLC: Mcap is £17.2M. No revenue. No profit. Relies entirely on dilutive capital raises. Holds 890 km² of KCB ground plus a rare earths project in Mozambique that has a defined resource.

🟢 Switch Metals PLC: Mcap is £15.4M. No revenue. No profit. Reliant on fundraisings. Holds 3,000 km² of coltan and lithium licences in Côte d'Ivoire. Early-stage exploration.

🟢 Great Western Mining Corporation PLC: Mcap is £13.7M. No revenue. No profit. Reliant on heavily discounted placings. Holds 60 km² of exploration ground in Nevada, USA.

🔴𝐀𝐓𝐄𝐑𝐈𝐀𝐍 𝐏𝐋𝐂: Mcap is £5.1M (29p per share). Generating cash and profitable👉~£750,000 NET PROFIT targeted in 2026 and £1M in 2027 from its Tantalum trading JV with WOGEN. Chiefly, it holds a staggering 𝟓,𝟏𝟔𝟕 𝐤𝐦² of one of the most diversified, high-quality critical minerals portfolios in Africa.

Considering the above, the market has valued Aterian at less than one-third of Altona, Switch Metals, and GWMO.

𝐓𝐡𝐚𝐭'𝐬 𝐧𝐨𝐭 𝐚 𝐯𝐚𝐥𝐮𝐚𝐭𝐢𝐨𝐧 𝐠𝐚𝐩. 𝐓𝐡𝐚𝐭'𝐬 𝐚 𝐦𝐚𝐫𝐤𝐞𝐭 𝐟𝐚𝐢𝐥𝐮𝐫𝐞.

1️⃣ 𝐏𝐀𝐑𝐓 𝐎𝐍𝐄: 𝐓𝐇𝐄 𝐀𝐂𝐑𝐄𝐀𝐆𝐄

Aterian's portfolio is a sprawling, multi-commodity, multi-jurisdictional asset base that any major would kill for. Here's what the company actually owns, project by project.

MOROCCO (COPPER-SILVER DISTRICT)

✅ 100% ownership of Agdz Copper-Silver Project (34.5 km²). A copper-silver asset at an advanced stage of development, with permitting already de-risking the pathway to exploration.

✅ 100% ownership of West Tazalaght Project (27.4 km²). Located just 7km east of the Tazalaght Copper Mine operated by the Managem Group; a £7.5bn mcap company. The geological setting is identical.

✅100% ownership of Tata Project (138.6 km²). Positioned 50 km southeast of the Tizert copper-silver project, which boasts 57 million tonnes grading 1.03% copper and 23 g/t silver. That project is currently under development by Managem. Aterian is sitting on the same structural corridor.

✅100% ownership of Jebilet Est Project (73.6 km²). Located in the Jebilet Massif, a region considered highly prospective for volcanic massive sulphide and vein-hosted base metal and copper deposits.

✅100% ownership of Akka Project (47.1 km²). In the western Anti-Atlas Mountains, with copper as the primary target metal.

BOTSWANA (KALAHARI COPPER BELT)

✅ 90% ownership of 2,298 km² of prospecting licences in the Kalahari Copper Belt (KCB); a proven copper-silver district.

✅ 90% ownership of the 2,517 km² Sua Pan Project in north eastern Botswana, targeting lithium brines within the expansive Makgadikgadi basin.

RWANDA (TANTALUM-NIOBIUM-LITHIUM)

✅ 70% ownership of the 27.5 km² HCK1 Project. A comprehensive exploration dataset already exists, including mapping, geochemistry, ground geophysics, and core drilling undertaken by mining giant Rio Tinto. Tantalum and niobium is the near-term focus, with lithium under evaluation.

✅ 100% ownership of the HCK2 Project (Musasa Project). A highly prospective area for lithium (LCT pegmatites), tantalum, niobium, tungsten, and tin.

👉 𝐓𝐇𝐄 𝐆𝐑𝐀𝐍𝐃 𝐓𝐎𝐓𝐀𝐋𝐒

❶ Altona Rare Earths: 890 km² of KCB ground plus a rare earths project. Mcap £17.2M.

❷ Switch Metals: 3,000 km² of coltan/lithium ground. Mcap £15.4M.

❸ Great Western Mining Corporation: 60 km² of tungsten/copper exploration ground in Nevada, USA. Mcap £13.7M.

❹ Aterian: 𝟓,𝟏𝟔𝟕 𝐤𝐦² of diversified (copper, silver, tantalum, lithium), strategically-located ground plus a profitable metals trading business. 𝐌𝐜𝐚𝐩 £𝟓.𝟏𝐌.

The arithmetic is not complicated. The market has simply stopped doing it.

2️⃣ 𝐏𝐀𝐑𝐓 𝐓𝐖𝐎: 𝐂𝐀𝐒𝐇 𝐅𝐋𝐎𝐖

Here's the detail that should make every serious investor sit up;

❶ Altona Rare Earths: Zero revenue. Zero profit. Every drill hole is funded by a dilutive placing.

❷ Switch Metals: Zero revenue. Zero profit. Same story. Raise, drill, dilute, repeat.

❸ Great Western Mining Corporation: Zero revenue. Zero profit. Same story. Raise, drill, dilute, repeat.

❹ 𝐀𝐓𝐄𝐑𝐈𝐀𝐍 𝐏𝐋𝐂: Targeting £750,000 NET PROFIT in 2026 and £1M in 2027. Fully funded. In partnership with the billion-dollar WOGEN Resources and Lithosquare.

Let me translate.

A £1M net profit, at a conservative 12x price-to-earnings multiple, gives the trading division a standalone value of £12 million. That's 2.5 x Aterian's current mcap.

Or put another way: Aterian holds 86 times more exploration ground than GWMO. It has a metals trading business already generating cash.

But the market values Aterian at less than half of GWMO's price tag?

The arithmetic is not complicated. The market has simply stopped doing it.

3️⃣ 𝐏𝐀𝐑𝐓 𝐓𝐇𝐑𝐄𝐄: 𝐓𝐇𝐄 𝐈𝐌𝐏𝐄𝐍𝐃𝐈𝐍𝐆 𝐂𝐀𝐓𝐀𝐋𝐘𝐒𝐓𝐒

On 31 March 2026, Aterian announced that its AI collaboration with Lithosquare had delivered 8 high-priority exploration targets. Three in Morocco. Five in Botswana.

The AI analysis combined advanced geological modelling, detailed interpretation of Aterian's proprietary datasets, and a global review of analogous mineral systems. The CEO of Lithosquare stated: "The geological quality was there to be found."

The next phase is now underway. Work programmes and budgets are being prepared. The long-form JV is being finalised. The explicit goal is to advance these targets to drill-ready status on an aggressive timeline.

And when those drill bits begin to turn, the market will have to re-evaluate. And when they hit the target, with AI-guided precision, the upside will be obscene.

4️⃣ 𝐏𝐀𝐑𝐓 𝐅𝐎𝐔𝐑: 𝐓𝐇𝐄 𝐂𝐎𝐌𝐌𝐎𝐃𝐈𝐓𝐘 𝐒𝐔𝐏𝐄𝐑𝐂𝐘𝐂𝐋𝐄

The market is ignoring Aterian at precisely the moment when the commodities it trades and explores for are in once-in-a-decade bull markets.

Last week, Silver touched US$82 per ounce. Some analysts forecast US$100 in 2026.

Copper is trading at US$6.11 per pound, up from US$4.25 a year ago.

Tantalum is changing hands at US$206 per pound (April spot).

5️⃣ 𝐏𝐀𝐑𝐓 𝐅𝐈𝐕𝐄: 𝐓𝐇𝐄 𝐌𝐁𝐎

The Aterian BOD, with serious skin in the game (~15%) is openly contemplating a management buyout. They know the value. They see the arithmetic. And they're considering buying the entire business at a fraction of its fair value. My advice? Take them seriously.

🚨 𝐓𝐇𝐄 𝐁𝐎𝐓𝐓𝐎𝐌 𝐋𝐈𝐍𝐄

The size of the exploration acreage (𝟓,𝟏𝟔𝟕 𝐤𝐦²) is unparalleled for a microcap. The blue sky potential is staggering. And now, the AI has delivered. The drill bits are coming. And the tantalum trading business is not only printing cash, but is also profitable; removing the perennial curse (persistent placings followed by endless dilution) that so often afflicts junior explorers.

More importantly, Aterian's conservative Fair Value, ahead of the catalysts, stands at £𝟐𝟔.𝟏𝐌 → 𝟏𝟒𝟖𝐩 𝐩𝐞𝐫 𝐬𝐡𝐚𝐫𝐞.

𝐎𝐧𝐞 𝐰𝐨𝐫𝐝: 𝐃𝐈𝐒𝐂𝐎𝐍𝐍𝐄𝐂𝐓𝐄𝐃

1

2

7

2,401

🚨What's Aterian Actually Worth? #ATERIAN #ATN

Aterian has 17,684,000 Ordinary Shares in issue. At 23p per share, the entire company (everything it owns, its trading business, its exploration projects, its partnerships) is being valued by the market at just £4.07M.

That is the starting point.

Now, let's walk through the Executive Chairman's recent interview with Sunday Roast and see what it tells us about the company's actual worth.

By the way, this is not speculation.

These figures come directly from what third parties have already spent or committed to the company's assets.

1️⃣Exploration Licenses:

Lithosquare, a strategic partner, is spending €1.4M to acquire a 20% stake in eight of Aterian's licenses. If 20% is worth €1.4M, then 100% of those licenses is worth approximately €7 million. In pound sterling, that is £6.1M.

2️⃣HCK Project (Rio Tinto Validation):

Mining giant Rio Tinto spent US$5M proving-up the HCK project. That's money already in the ground. If we then acknowledge that the 'sunk exploration cost' has real value, this single project is, therefore, worth at least £2M to Aterian.

3️⃣Moroccan Copper-Silver Project (Agdas):

Aterian owns 100% of Agdas. It has just secured its Environmental Impact Assessment approval, a major regulatory milestone that materially de-risks the project. While not yet drilled, a copper-silver project at this stage of development with full permitting carries a baseline value. A conservative placeholder is £1M.

4️⃣Tantalum Trading Joint Venture with WOGEN:

This is where the story transforms. Charles Bray has explicitly targeted the trading business to deliver £1M in NET PROFIT to Aterian in 2027.

To be crystal clear, a profitable, scalable, trading platform with a TOP-FIVE global partner is NOT a speculative asset.

Chiefly, in the public markets, a business generating £1M in annual net profit would typically command a price-to-earnings multiple of 10x. That alone gives this division a standalone value of £10M.

5️⃣The Remaining Exploration Portfolio:

Aterian's Rwanda, Botswana, and Morocco acreage, with significant exploration upside, is assigned a nominal value of £5M - which is more than reasonable given the scale of the opportunity and the calibre of BIG PLAYERS (£3.6bn mcap Sandfire Resources in Botswana, £7.5bn mcap Managem SA in Morocco, and £350M mcap Trinity Metals in Rwanda), extracting metal within close proximity of the assets.

🚨Adding It All Up:

1️⃣ Exploration Licences (Lithosquare) → £6.1M

2️⃣ HCK Project (Rio Tinto) → £2M

3️⃣ Moroccan Copper-Silver Project → £1M

4️⃣ Tantalum Trading JV with WOGEN → £10M

5️⃣ The Remaining Exploration Acreage → £5M

👉TOTAL FAIR VALUE: £24.1M (136p per share)

That's a 6x UPSIDE just to reach the conservative sum-of-the-parts valuation!

In a BULL case scenario — where Tantalum prices remain strong, the HCK project moves into development with a partner (as Bray is targeting by year-end), and the trading business exceeds its targets, a fair value of £35M is easily achievable. That would equate to approximately 198p per share, representing an 8.5x return from current levels.

🚨BOTTOM LINE:

Boasting a Target Share Price (fair value) of 136p, Aterian represents one of the most compelling, deep-value opportunities in the junior resource sector today.

6

11

1,664

🚨JUST RELEASED: Chairman's Interview #ATN #ATERIAN #TANTALUM #WOGEN #MULTIBAGGER

For those unaware, Aterian’s Executive Chairman just said something extraordinary.

youtube.com/watch?v=c8_jpuhq…

In an interview (53mins in...) released today, at 12:30, Charles Bray looked directly at a £4M market cap and effectively told the market it has lost its mind. His words, not mine.

And for private investors sitting on the side lines, this interview is the most direct, unfiltered, and compelling explanation of why Aterian represents one of the MOST ABSURD MISPRICINGS on AIM today.

1️⃣Let's start with the partnership that just went live. Aterian has secured a 50|50 joint venture with Wogen, and Bray is unflinching in describing its significance:

"This is one of the world's best, metal-focused trading companies! Wogen is a billion-dollar, London trading house with 50 years of history, and they have chosen Aterian as their exclusive partner in Rwanda.”

2️⃣Bray then goes on to explain the strategic shift:

"The Rwandan market has historically had a heavy dependence on Chinese refiners. So for us, this offers the opportunity to increase those margins by broadening the market pool. The result is a funded, scalable platform that fundamentally changes the company's financial trajectory.”

3️⃣What does this mean for 2026? Bray is specific:

“The company now expects trading revenues to cover 2026 operational expenses, and in effect, investors will have exploration assets for free."

Let that sink in.

The entire exploration portfolio—high-grade copper in Morocco, district-scale copper in Botswana, the HCK lithium-tantalum project with Rio Tinto's US$5 million data set—becomes a zero-cost option package funded entirely by the trading division.

4️⃣When asked if this removes the need for equity raises, Bray responded:

“I don't see why we would need to go back to the equity markets.”

No dilution. No death spiral. Just cash flow funding growth.

5️⃣And the growth trajectory is explicit. Bray outlined targets:

"We're looking to increase the gross profit per quarter at approximately 50%. So that for us would mean that in 2026, we would cover our expenses. And 2027 would be, let's say, closer to £2.5M of gross profit!”

That is not a forecast. That is a stated target from the Executive Chairman.

6️⃣Then there is HCK, the Rwandan project where Rio Tinto spent US$4.7 million proving mineralisation before walking away because it wasn't Tier-1 scale.

For Aterian, it is a company-maker. Bray walked investors through the numbers:

"From our preliminary analysis, it's approximately 35% Tantalum and approximately 40% Niobium, and that's virtually the entire hill that you can see."

7️⃣The Tantalum price has more than trebled since Rio walked. Bray confirms:

"Last year this time, we could have worked on developing HCK and it still would have been profitable. So we're in a much, much better situation. The company is now in discussions with partners to take HCK into development by the end of this year.”

8️⃣The competitive landscape is equally telling. When asked who else provides fully traceable, conflict-free tantalum at scale, Bray was candid:

"If you read the reports by the various NGOs... nobody, just us."

9️⃣He acknowledged Traxys as a billion-dollar competitor, but concluded:

"That's our only competition. Aterian IS ONE OF TWO PLAYERS IN THE WORLD, offering what the market increasingly demands: certified, ethical, fully traceable critical minerals.”

The demand drivers are accelerating. Bray notes that:

“Tantalum is not a niche curiosity; it is the hidden backbone of the AI revolution, and Aterian has a front-row seat.”

🔟The exploration portfolio is also advancing. The EIA approval for Agdz in Morocco has been secured, a milestone Bray describes as "not easy to come by." It de-risks the project and accelerates development.

And Lithosquare, the AI exploration partner, has completed its targeting. Bray reveals:

"They matched off with what we had prioritised, not necessarily in the same order. The work they did was actually quite remarkable. They did the equivalent of what it would take us probably 20 geologists to do over the past three to four months. The announcement of their expenditure focus is imminent.”

🚨Which brings us back to the VALUATION.

Bray's closing comments are the most damning indictment of the market's inefficiency.

"Rio Tinto spending US$5 million on HCK1 alone gives you some indication of what Eastinco or the Rwandan business is worth. That's not counting the trading. Lithosquare spending 1.4M Euros across 8 different licenses gives you an indication of what those eight licenses are worth. And that's for 20% of those licenses. I think it just boggles the mind."

Then the punchline:

"I no longer believe in the efficient market hypothesis."

🚨BOTTOM LINE:

For private investors on the side lines, the message is unmistakable. Aterian has a funded, scaled trading platform with a billion-dollar partner, targeting profitability in 2026.

It has a fully owned exploration portfolio that includes a project Rio Tinto spent millions proving. It has AI partners spending millions to earn into its licenses. It has a management team that has executed partnerships with the world's best. And the entire package trades at £4m?

Bray's bewilderment is your opportunity.

One Word: MULTIBAGGER!

4

7

2,339

Serial Investor retweeted

Mar 24

Yes a 3m company has just signed a JV with a billion dollar company

Huge huge news

#ATN without any doubt in my mind is a multibagger

1

3

6

446

Serial Investor retweeted

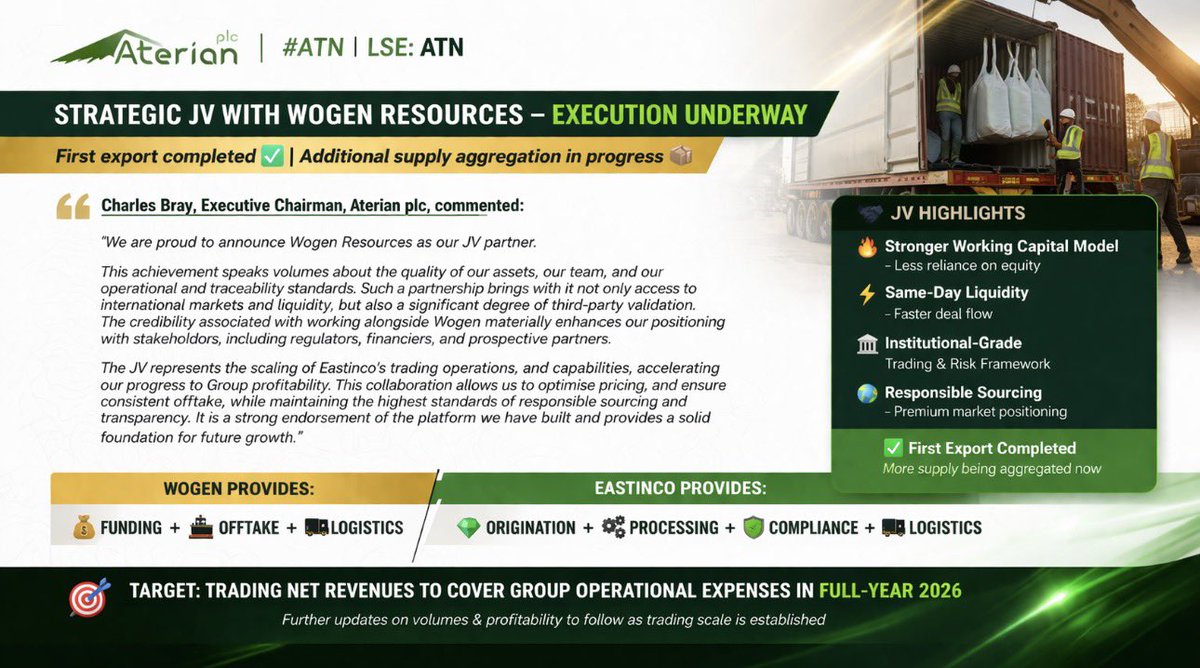

🚨 BIG STEP FOR @aterianplc 👀

A major milestone for #ATN just landed… and this is EXACTLY what execution looks like 👇

🔥 Strategic JV with Wogen Resources Limited now LIVE

🚚 First export already COMPLETED

📦 More supply being aggregated RIGHT NOW

💰 Near-term revenue generation underway

⚡ Key Takeaways:

✅ Stronger working capital model (LESS reliance on equity 👀)

✅ Same-day liquidity = faster deal flow

✅ Institutional-grade trading & risk framework

✅ Premium positioning via responsible sourcing 🌍

✅ Built to SCALE trading volumes

💡 From agreement → execution at speed

💡 Revenue visibility improving

💡 Platform now set for growth

This is how you build a serious critical minerals trading business 🔋

londonstockexchange.com/news…

5

7

1,012

Serial Investor retweeted

Mar 17

£100k buy in a £4m mcap company

#ATN

assume price has been held there to allow that buy at 25p. Could start go properly move now from tomorrow

1

1

6

467

Serial Investor retweeted

Next BIG mover in the small cap space ⁉️

Have a look into @aterianplc #ATN

🚨 TRANSFORMATIONAL NEWS for #ATN

@aterianplc secures a landmark tantalum funding & marketing partnership in Rwanda

🔹 50/50 profit share on international tantalum sales

🔹 Working-capital bottleneck removed

🔹 Scale volumes without equity dilution

🔹 Direct exposure to global pricing & margins

💬 Charles Bray:

“A step change in our ability to trade, scale and generate cash — without balance-sheet stress or shareholder dilution.”

This fundamentally changes the economics and scalability of the business.

londonstockexchange.com/news…

1

4

7

790

🚨HIDDEN IN PLAIN SIGHT

#ATERIAN, #ATN, #TANTALUM, #MULTIBAGGER, #LITHIUM, #COPPER, #SILVER

👉How a Tiny London Lister Just Secretly Partnered with a Multibillion-Dollar Giant to Corner the Tantalum Market

London-listed junior miner Aterian recently delivered what could only be described as a career-defining masterstroke, yet the market appears to have missed it entirely.

The announcement landed in early February 2026 with the kind of understated legalese that typically sends retail eyes glazing over.

Heads of Terms signed. Strategic commercial partnership. Working capital solution. Yawn.

But scratch the surface, and what emerges is possibly the most asymmetric setup on the entire AIM market.

So let's revisit the numbers, the structure, the hidden partner, and the staggering upside that this tiny stock just unlocked.

🚨In a Nutshell:

Aterian has signed a 50 | 50 profit share with what we strongly suspect is a multibillion-dollar global trading titan, likely Traxys. This isn't just another mining update. It's a financial revolution.

By outsourcing the financial heavy lifting, Aterian has effectively removed the bottleneck from its business model, turning a cash-constrained penny stock into a scalable, cash-generative machine with direct exposure to the red-hot tantalum market.

We are looking at a potential 600 percent to 1,600 percent rerating by 2029, all hiding in plain sight on the London exchange.

🚨The Holy Grail Deal:

On paper, with a market cap hovering just above £4.3 million, Aterian looks like just another AIM-listed explorer burning through cash and hoping for a drill result. But look closer.

On February 09, 2026, they announced they had signed Heads of Terms for a transformational strategic commercial and funding partnership relating to the sale, marketing, and funding of their Rwandan-origin tantalum concentrates.

The key details are electric:

✅First, the 50 | 50 profit share means Aterian keeps half the profits on every dollar of tantalum sold internationally. This is direct leverage to surging global prices, not a fixed fee that caps upside. If tantalum prices double, Aterian's profits double. Simple.

✅Second, and this is the kicker, the partner provides 100 percent working capital. That means same-day funding for purchases, in-warehouse inventory financing in Kigali, and cash for material procurement. For a company with a tiny market cap and a previously undervalued share price that made equity raises painfully dilutive, this is the equivalent of strapping a rocket to a skate board.

✅Third, this deal grants institutional status. It embeds Aterian directly into the global tantalum supply chain, moving them from a stressed trader, constantly hunting for cash, to a scalable platform with serious firepower and direct end-customer relationships.

🚨The Silent Partner: Why Traxys Makes Sense:

Here is where the narrative gets really interesting. The partner has not been named, cited only as a global metals and minerals trading house specialising in non-ferrous and specialty materials. But the clues are everywhere, and they point in one direction.

This partnership is actually an expansion of an existing relationship.

In September 2025, Aterian announced it had partnered with a major international trading house to launch its Coltan trading operations in Rwanda, complete with a US$250,000 mezzanine loan facility. That initial partner was described in identical terms. The February 2026 deal is simply that relationship on steroids.

So who is it? The strongest candidate, by far, is Traxys.

traxys.com/detailnew/185/tra…

Traxys is a physical commodity trader and merchant in the metals and natural resources sectors.

Its annual turnover is in excess of US$10 billion (£7.4bn). The company is actively engaged in sourcing, trading, marketing, and distributing non-ferrous metals, ferro-alloys, minerals, industrial raw materials, and energy.

So, we're talking about a partner with multibillion-dollar scale.

Imagine the dynamic; A £4m London micro-cap standing shoulder to shoulder with a multibillion-dollar global trading powerhouse, splitting profits fifty-fifty on every shipment!

That is the kind of asymmetric partnership that venture capitalists dream about. And it’s currently hiding in plain sight because the market is too busy scrolling past the headline to read the fine print.

Other candidates exist, of course.

Cogency, now part of IXM and backed by Mitsubishi Corporation's massive balance sheet, would also fit the profile.

Global Advanced Metals, a key player in the tantalum supply chain, could represent a deep vertical integration play.

But Traxys ticks every single box, from African focus to specialty materials expertise to serious financial firepower.

🚨The Numbers Game:

Based on the April 2025 US$4.5 million operational trading facility, and aggressive volume assumptions, the growth trajectory is staggering.

We are modeling net margins of 15 to 20 percent on concentrate sales, with Aterian taking half.

In the conservative path, which we assign a 30 percent probability, volumes hit 80 tonnes by 2029. Revenue reaches approximately US$36 million, and Aterian's share of net profit lands around £1.02m (US$1.35 million).

The base case, which carries a 50 percent probability and represents our target, sees volumes double to 150 tonnes. With tantalum prices firming on AI-driven demand, revenue hits roughly US$71 million. Aterian's net profit climbs to £2.3m (US$3.2 million). This implies a three-year revenue compound annual growth rate of 26 percent.

In the bull run scenario, which carries a 20 percent probability, volumes explode to 250 tonnes. Revenue smashes through US$125 million, and net profit for Aterian hits £4.5m (US$6.25 million).

To put those numbers in context, Aterian's latest reported revenue for Q42025 was just £106,000, with revenues in Q12026 recently mooted (in CEO Interview on 05 Feb 2026) to be approaching £300,000!

youtube.com/@thesundayroast4…

We are talking about scaling from tens of thousands to tens of millions in under three years. That is not growth. That is metamorphosis.

🚨Valuation: The Multiples Game:

Using the current share count of 17,084,000 ordinary shares and a current share price of 27p, the math gets seriously exciting.

Comparable junior mining and trading companies trade at 10 to 15x price-to-earnings once profitability is established.

Applying a 12x multiple to the base case net profit of £2.3m (US$3.2 million) gives an implied market cap of £27.6 million at current exchange rates. Dividing that by the 17,084,000 shares in issue yields a theoretical share price of 161p.

In the bull case, applying a 15x multiple to £4.5m (US$6.25 million) of net profit pushes the market cap to £67.5 million. That implies a share price of 395p.

Let's put that in perspective.

From the current 27p, the base case represents ~600 percent upside and the bull case represents over 1,600 percent upside.

That is asymmetric risk at its finest. And it’s hiding in plain sight because the market is, quite frankly, asleep.

🚨Why This Isn't Just Hype:

✅First, there is AI-driven demand. Tantalum is critical for semiconductors and high-performance capacitors.

The AI revolution, with its insatiable hunger for computing power and advanced components, is a demand supercycle for this metal. Markets are only beginning to price this in. The Pentagon recently sought up to US$100 million in tantalum for defence applications. This is not speculative demand. It is here, and it is growing.

✅Second, there is Rwanda. It is the only stable, OECD-compliant sourcing hub in the Great Lakes region, offering full traceability and ethical supply chains under ITSCI and RMI standards. Aterian is the only London-listed company with boots on the ground and an operational trading presence there. That is a moat.

And with Rwanda actively pushing to position itself as a regional mineral processing hub, early movers like Aterian stand to benefit from long-term government alignment.

✅Third, there is the free option. Beyond trading, Aterian holds the HCK exploration project, which comes with a Rio Tinto-generated dataset following the major's US$4.73 million investment and eventual exit.

Rio Tinto does not spend that kind of money on dirt without seeing serious potential. If Aterian converts that project into production, they vertically integrate from miner to trader and command even higher multiples. The exploration upside is a free call option on top of the trading cash flow.

🚨The Risks (Because Nothing is Free):

The partner remains anonymous. If that relationship sours, the entire funding model breaks. Investors are placing trust in management's ability to maintain that alignment. The fact that this is an expansion of an existing relationship rather than a new one provides some comfort, but it remains a concentration risk.

Rwandan tax policy is shifting. A new bill before parliament aims to incentivise local processing, which could eventually impose higher taxes on raw concentrate exports. Aterian will need to navigate this carefully. The flip side is that if they eventually process in-country, they could qualify for lower royalty rates of just 2 to 3 percent.

Tantalum prices, while hot, are volatile. A sudden demand shock or supply glut would directly impact the 50/50 profit share. That said, the long-term demand story from AI, defence, and 5G provides a structural floor.

And finally, there is competition. Other traders are eyeing Rwandan supply. Aterian's first-mover advantage is real, but it is not permanent. They need to execute and scale quickly to cement their position.

🚨The Final Word:

Aterian has executed a classic financial manoeuvre: de-risking the balance sheet to maximise operational leverage. The company is poised to transform its revenue base from thousands to tens of millions.

For investors willing to look past the market's apparent indifference, the next three years offer a compelling narrative of scarcity, demand, and financial alchemy.

The definitive agreements are being finalised as we speak. When they drop, and when the market finally connects the dots between a tiny London lister and a multibillion-dollar trading partner hiding in plain sight, the rerating could be violent.

🚨Data Snapshot:

Shares in issue stand at 17,084,000. The current price is 27p, giving a market cap of approximately £4.60 million. The catalyst to watch is the finalisation of the Heads of Terms into definitive agreements, which is imminent. The partner remains unnamed, but all signs point to a Traxys-scale giant with billions in backing.

🚨Conclusion:

Aterian is not a mining stock. It’s a leveraged play on the Tantalum supercycle, funded by a multibillion-dollar partner, trading at a fraction of its intrinsic value.

The market has missed it because it looks small, because it sounds complicated, and because the partner is playing silent. But the numbers do not lie. Base case fair value is 161p. Bull case is 395 pence.

From 27p, that is the kind of setup that defines careers. And it's hiding in plain sight.

discoveryalert.com.au/global…

3

1,671

Serial Investor retweeted

Feb 20

For some tantalum exposure been buying #ATN recently following their commercial partnership. Not many options out there #SWT is another one but decided on former.

"Immediate acceleration of trading capacity, enabling higher volumes without an overly constrained balance sheet"

2

2

6

872

Serial Investor retweeted

Feb 9

Strategically, #ATN is now embedded in the global tantalum supply chain with fully traceable, ESG-compliant sourcing.

A genuinely transformational moment for the company.

#MiningNews #CriticalMinerals #Rwanda

londonstockexchange.com/news…

3

7

2,061

Serial Investor retweeted

🚨 TRANSFORMATIONAL NEWS for #ATN

@aterianplc secures a landmark tantalum funding & marketing partnership in Rwanda

🔹 50/50 profit share on international tantalum sales

🔹 Working-capital bottleneck removed

🔹 Scale volumes without equity dilution

🔹 Direct exposure to global pricing & margins

💬 Charles Bray:

“A step change in our ability to trade, scale and generate cash — without balance-sheet stress or shareholder dilution.”

This fundamentally changes the economics and scalability of the business.

londonstockexchange.com/news…

1

3

1,882

Serial Investor retweeted

🚨🔥 #ATN on the move… and this story is only getting started 👀⛏️

Aterian’s Agdz Cu–Ag project in Morocco 🇲🇦 is shaping up fast:

✅ Up to 2.97% Cu 51g/t Ag

✅ Multiple mineralised structures

✅ Only ~10% tested so far

✅ Clear path to drilling

With #copper & #silver at historic highs 📈⚡️

district-scale discoveries = BIG leverage.

24% today.

Momentum building.

Drill story loading… 🎯

Think you’ve missed it?

The party hasn’t even started yet 🚀

#ATN #Aterian #Copper #Silver #MiningStocks #SmallCaps #FOMO #CriticalMetals #Commodities

2

2

374

Serial Investor retweeted

Jan 28

#ATN

Aterian.

Some good value here post-Rio exit.

My thoughts.

open.substack.com/pub/thatst…

2

8

6

1,962

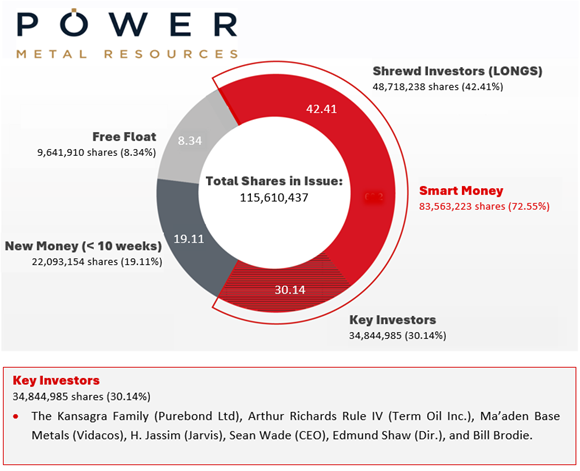

Power Metal Resources #POW

For those unaware, Friday’s closing bell marked a genuine inflection point — one the broader market has yet to price in.

POW launched its rocket; the Minestarters ‘Go Live’ event. This isn't just another milestone; it’s an entry into an untapped financial arena where POW faces ZERO direct competitors across the London, Canadian, and U.S. markets.

But to understand the shift, you must understand Minestarters — because it fundamentally redefines what you own with POW shares.

Let’s talk first-mover advantage — a term often overused, but here, utterly deserved.

Real World Asset (RWA) tokenisation has surged from US$8.6Bn to over US$25Bn in just six months — a 260% explosion! Yet, until now, it’s been limited to bonds and credit. The multi-trillion-dollar mining and exploration sector remained untouched.

Enter Minestarters: the FIRST fully compliant platform built exclusively to tokenise early-stage mining projects.

It transforms physical copper, silver, gold, platinum, and uranium assets into liquid digital tokens, unlocking global pooled capital and solving the industry’s perennial funding gap.

In essence, they’ve built the ‘stock exchange’ for next-gen mining finance — and it went live on Friday. The site is open, and the project pipeline is building now.

Now, consider the explosive potential of a 2026 Nasdaq | TSX listing of Minestarters? The appetite on these exchanges for disruptive, high-growth fintech and RWA platforms is absolutely phenomenal.

Thus, a successful pathway to a North American listing could see its valuation run into the tens of millions of pounds (‘first mover’ propulsion). This is the scale of opportunity now in play.

But in the meantime, how does Minestarters create value for POW?

Minestarters generates scalable, high-margin fees from vetting, tokenising, and managing projects. As the anchor shareholder, POW captures a major share of these earnings — a powerful new revenue stream built on financial innovation, not just drill results.

Now, the valuation case — where things get compelling.

POW’s current market cap is ~£18M, backed by ~£15M in cash. That means the market values POW’s entire global portfolio — Oman, Saudi, Botswana, Canada, Austrailia, plus active drilling in a historic metals bull market — at just £3M. That’s simply insane.

And that’s before including Minestarters.

POW paid £1M for 35%, implying a £2.86M starting valuation.

Hitting key milestones — onboarding projects, securing exchange listings — triggers an option to invest another £2M for 49%, lifting Minestarters’ valuation to £6.12M.

Once live with a pipeline, a conservative next-round valuation, based on current RWA peer valuations, approaches ~£45M — making POW’s 49% stake worth ~£22M. And that’s before factoring in the monumental rerate potential of a 2026 Nasdaq | TSX listing.

Thus, the catalyst engine is already firing.

This isn’t a “wait-and-see” story. The platform is live. Milestones that trigger POW’s increased stake are now actionable. Thus, expect news in weeks, with each RNS forcing a market rerate of this embedded fintech gem.

BOTTOM LINE: As of Friday (evening), POW transformed into a powerful hybrid; a cash-rich explorer with prime critical metals acreage and multiple drills turning, a shrewd strategic investor (Apex Royalties, GSAe, FCM), the largest shareholder in Minestarters — a platform poised to finance the industry’s future (now with a clear and explosive pathway to a North American listing), and an aggressive £2.5M buyer of its own stock!

In a market desperately searching for real innovation and asymmetric opportunities — where else would you rather be?

ATB

2

7

19

1,319

Serial Investor retweeted

Jan 16

We are LIVE → minestarters.com 🚀

See how #Minestarters brings compliance-first, on-chain access to mining exploration opportunities—with KYC access and clear reporting.

Subscribe to our YouTube channel where we'll be creating more detailed explainers - going live next week 👋

youtube.com/@minestarters25

More to come! Stay tuned.

#RWA #MiningFinance #Tokenization #MiningTokenization #Mining

1

11

23

1,306

Serial Investor retweeted

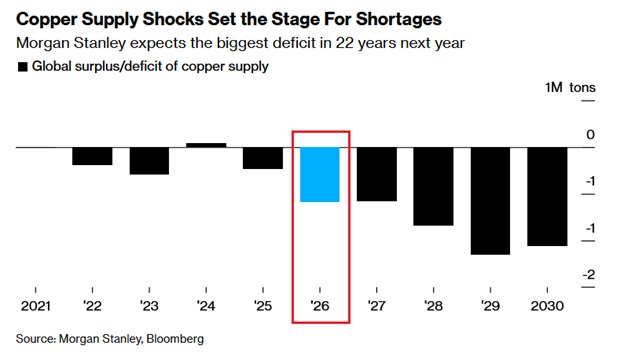

10 Nov 2025

Copper is set for a historic shortage next year:

The copper market is expected to face its most severe deficit in 22 years in 2026, at -590,000 tons, according to Morgan Stanley.

The deficit is expected to widen by 2029 to a whopping -1.1 million tons.

This comes as global annual copper production is on course to contract for the first time since 2020.

Major production disruptions have impacted mines worldwide, with operational issues at several major mining sites exacerbating supply constraints.

At the same time, demand from AI data centers and electric vehicles is expected to outpace supply.

Copper miners have already struggled for years to keep pace with surging demand.

Higher copper prices are here to stay.

118

652

3,318

791,140

24 Aug 2025

Power Metal Resources #POW

BACKED BY LEGENDARY CAPITAL ⚡

Rick Rule (4.07%) ➡️ The titan of natural resources!

The Kansagras (4.52%)➡️ A £600m resource conglomerate!

When giants like this align, you pay attention. The market cap is £17.92m.

The signal is priceless!

7

14

985