I am a UK stock market private investor. My first published book is now available to order. Search for, "How to Become a MicroCap Millionaire".

Joined January 2009

- Tweets 64,394

- Following 1,887

- Followers 16,217

- Likes 38,331

8,796 Photos and videos

Pinned Tweet

16 Jul 2025

If you are going on holiday and looking for a cracking book to read by the pool, I’ve got the perfect suggestion 😉

My book has just hit 152 (4.9*) reviews on Amazon alone.

Buying the book also gets you 25% off The SharePickers Investment Club 👇

sharepickers.com/how-to-beco…

3

3

19

15,249

Jun 11

SpaceX - 5 Ways it will Impact the Market Negatively [PODCAST]

audioboom.com/posts/8915344-… $SPCX

2

613

Jun 10

Why is the oil price not higher, when 20% of global output is choked off via the St of Hormuz?

Before the conflict the global oil market was already deeply in surplus.

The reason prices haven't gone even higher is because the market recognises this crisis as a logistical bottleneck, not a permanent destruction of oil reserves or infrastructure.

Its a structural oversupply capped by a logistical shock.

Post-War the market is pricing in a massive supply-and-demand double whammy

On the SUPPLY side:

Trapped Middle East barrels will flood back onto the market plus there’s also likely to be elevated output non-OPEC output remains

On the DEMAND side:

There’s accelerating structural decline via global EV & Electrification adoption

The market is currently looking past the immediate physical disruptions because it knows a wave of supply is waiting on the other side of a ceasefire, precisely at a time when global transport electrification is permanently chipping away at structural demand.

Long-term forecasting models show that once this geopolitical crisis resolves, underlying market fundamentals are heavily weighted toward an oversupply, with some estimates pointing to Brent retreating right back down toward the $60-$70 range.

4

5

1,545

Justin Waite retweeted

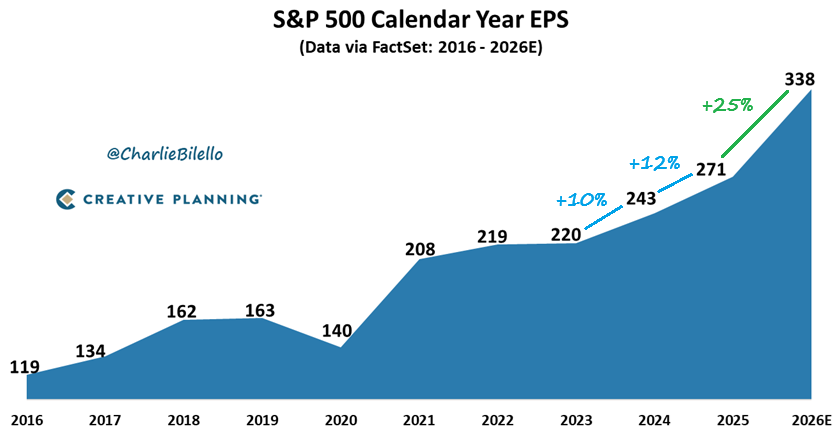

S&P 500 earnings are now expected to increase by 25% this year. We've never seen earnings growth this high outside of post-recessionary rebounds. An unprecedented boom fueled by massive EPS gains in big tech.

Video: youtube.com/watch?v=bXzTqIir…

80

174

933

105,121

Justin Waite retweeted

Jun 7

Labour risks being forced to seek emergency help from the International Monetary Fund (IMF) as Britain lurches toward a debt crisis, leading economists are now warning.

Former IMF chief economist Ken Rogoff says, in a new interview, that there is “more than 50:50 chance” of a major UK debt crisis before the end of this decade.

He is joined by Sir Charlie Bean, a former senior official at both the Bank of England and the Office for Budget Responsibility, who says the need for an IMF bail-out is now a “material risk” for the British economy.

I not only firmly agree with Ken Rogoff and Sir Charlie Bean – but have been repeatedly issuing the very same warnings for a very long time.

Because the grave risk of a major fiscal meltdown has been apparent for at least the last two years – to anyone who combines serious knowledge of UK economics and politics and global debt markets with an open mind.

The UK's public finances were already fragile when Labour took office back in July 2024.

But this government's misguided, ideologically-driven statist policies have made a bad situation much worse, seriously increasing the danger of a deep fiscal crisis - which would cause a disastrous state funding shortfall and a very nasty inflation spike.

That would result in Downing Street being forced to follow the orders of unelected technocrats flown in from Washington and elsewhere.

It would be a very major national humiliation combined with a deep economic slump and an even more intense cost-of-living crisis – in which low-income households, as ever, would suffer the most.

Yet those of us that have shown the brains and courage to point out these inconvenient truths over recent months and years have long been dismissed and derided for our trouble - not only by ignorant politicians and approval-seeking journalists but also the overwhelming majority of "leading economists".

Ahead of the general election in mid-2024, with Labour on course to win, the conventional wisdom among the great sages of broadsheet journalism and the economics establishment was that "the adults would soon be back in charge" ... Labour would "get lucky with the economy" ... and "Britain would now enjoy an extended period of political and fiscal stability".

I thought that was total nonsense – not least as I was well aware Labour's plans irresponsibly to increase borrowing and spending would be met with deep scepticism by the global pensions funds, insurance companies and other institutional investors that lend governments serious money.

My weekly @Telegraph "Economic Agenda" column of 23rd June 2024, a fortnight ahead of the general election, was a total outlier. I recounted the disaster of 1976 – when Britain was forced to go "cap in hand" to the IMF for a bailout – and warned that "The Ghosts of the 1970s" would haunt Labour's (so-called) economic resurrection".

Six months later, after the October 2024 "Hallowen" budget in which Chancellor Rachel Reeves did indeed sharply hike borrowing and spending, I assessed the market reaction then doubled-down – warning more assertively in my column of 12th January 2025 that "The UK risks a return to 1976 unless Reeves changes course".

And then again on 20th July 2025, as Labour's policies raised the costs of doing business, translating into price pressures which pushed up government borrowing costs even more, I again cautioned that "Inflation risks are taking Britain to the debt-crisis cliff edge".

"It’s now screamingly obvious that Labour’s crude Keynesianism – “pump priming” the economy by upping state borrowing and spending – isn’t working," I wrote in that column last July.

"Worse than that, this Government’s actions are pushing Britain towards a budgetary crisis every bit as serious as that in 1976 – when the UK was forced to go “cap in hand” to the IMF for a bail-out".

It's been a lonely task issuing these warnings. I've been hounded in public debates, slagged off by senior civil servants and often dismissed by "leading economists" as "alarmist".

So what do these same "leading economists" now say to Rogoff (Harvard Professor, Former IMF Chief Economist) and Bean (LSE Professor and Former Deputy Governor of the Bank of England)?

The "economics establishment" – with very few honourable exceptions, the brilliant @jagjit_chadha among them – has been and remains extremely reluctant to point out the deeply unsustainable nature of this government's addiction to ever more borrowing.

The systemic fiscal dangers of evermore "tax and spend" – and the prospect of a serious spike in gilt yields and related fiscal meltdown – are now so real and present as to be completely undeniable.

Yet the UK government is about to shift even further to the left, pushing up borrowing and spending even more under a new leader, in a bid to appease the massed ranks of economic illiterates among Labour's Parliamentary party and activist base – making those dangers even more acute.

Yet, still, the silence among "public intellectual" economists is deafening.

I'm glad the likes of Ken Rogoff and Charlie Bean are now issuing clear warnings. So where is the rest of the "economics establishment" - those who purport to understand fiscal management and financial markets, and often funded by taxpayers' money?

Britain is now clearly in the crosshairs of a very serious danger. The government's creditors are increasingly fickle and based overseas – with no regulatory or cultural obligations to lend money to the UK government.

Those holding UK gilts are increasingly "speculative" rather than "strategic" long-term investors – looking for quick returns, financing their government bond purchases with "leverage" (money borrowed from elsewhere), which will quickly be withdrawn when senitment decisively shifts, causing a plunge in gilt prices and a sharp additional surge in government borrowing costs, setting up a vicious circle.

The UK government is very heavily indebted – and the global investors we rely on to bankroll a huge slice of our state spending are alarmed that of the £132bn the government borrowed last year, no less than £110bn was spent on debt interest – as I wrote in a column on 17th May 2026, "As Labour lurches further left, the markets are calling time".

Global investors are alarmed the UK has consistently had the highest inflation in the G7 (which pushes up borrowing costs) and has easily the highest share of index-linked debt (which magnifies the burden of inflation on the state's balance sheet).

And they are deeply, deeply alarmed that when Labour came to power in mid-2024, the Office for Budget Responsibility was forecasting additional state borrowing of £323bn by 2029, the scheduled end of this Parliament.

But Labour’s runaway spending and growth-crushing tax rises mean that the same five-year borrowing forecast is now £583bn – 80pc higher. And still, the trade unions, MPs and Labour activists who will choose Starmer’s successor now want even more.

It is not too late to pull the UK back from the fiscal brink, to avoid the extremely painful and deep, lingering damage of being forced to go to the IMF and perhaps other multi-lateral creditors for a bailout.

It is not too late to avoid the inflation surge, the currency crash, the shocking blow to consumer and business confidence alongside the sky-high interest rates that will seriously whack our economy – or the perhaps even deeper damage of yet more of the British electorate losing faith in the ability of our establishment to manage the country in a manner that avoids imposing serious hardship on so many hard-working people simply trying to make their way.

But our political and media class needs to start acknowledging the economic and financial truth – that the UK government is borrowing and spending too much, taxation is now so high that it's hammering growth and employment, and that trying to finally get the economy moving by "moving further left", borrowing and spending even more, will result in a fiscal collapse.

Smart, experienced, high-profile economists need to start speaking out – as Rogoff and Bean just have – raising the alarm in a bid to force the broader establishment to face reality. Before it's too late.

If you've read this far, you clearly think this analysis is worthwhile and important. So please like and share.

And for more, read my "Economic Agenda" column in The Sunday Telegraph each week – and subscribe to "When The Facts Change: Economics and Politics in a fast-moving world, with Liam Halligan"

180

968

2,182

92,606

This is awful. The last ever Denby Pottery going to the kiln. Why is there not uproar? Where’s the government in this?? We all have Denby in our homes, in family heirlooms, as our history and now it’s closing through lack of support, such a sad sad day. #SaveDenby @denbypottery

1,501

7,337

26,643

1,203,623

Jun 5

When is a Market Sell Off Likely to Happen? When Most Least Expect It [PODCAST]

audioboom.com/posts/8912955-…

2

483

Jun 5

Bitcoin $BTC is now at October 2024 levels.

Down 53% from the high in October 2025.

Jun 4

Bitcoin $BTC hitting lows last seen in February. There's a lot of leverage in crypto and it could get ugly.

Strategy (MSTR) has shattered its multi-year "never sell" narrative.

According to their SEC 8-K filing submitted on June 1, 2026, the company disclosed that it sold 32 Bitcoin between May 26 and May 31, generating $2.5 million in proceeds at an average price of $77,135 per coin.

The filing states the reason for the sale: to fund distributions on its preferred stock (including the high-yield STRC).

Strategy's new perpetual preferred stock (STRC) offers a high yield (of around 11.5%)

Whilst 32 Bitcoin is not a huge sale the signal it sends to the market is immense. The loudest preacher of the HODL strategy, just contradicted their own tenet.

Paying a high yield is ok when the price of Bitcoin is rising but when it falls, it could be the start of a death spiral.

Strategy is not the only Bitcoin treasury company that pays a yield, many of them do it with debt. They will all struggle if Bitcoin drops.

They will be forced to sell more bitcoin to cover debts, this results in a further drop in the price of Bitcoin, reducing the company's collateral value, forcing more sales.

2

1,223

Justin Waite retweeted

Jun 4

SpaceX IPO is loading.

But this isn’t a listing.

This is the most carefully engineered insider exit Wall Street has ever signed off on.

Thread 🧵

31

145

876

113,951

Jun 5

There may be some good news in regards to AI replacing humans.

Some companies have been using AI so intensively, it is proving to be as or more expensive than the human they replaced it with.

While the unit cost of a single AI token is dropping rapidly, the total volume of tokens being consumed is growing exponentially.

In early 2026, several high-profile enterprise budget overruns hit the news—such as reports of Microsoft scaling back internal Claude Code licenses because the compute costs outpaced the human salaries they were meant to augment, and Uber reportedly draining its entire 2026 AI budget in just four months.

If an employee uses a basic AI tool to summarise a short email, it consumes a few thousand tokens and costs fractions of a penny.

The maths changes completely when a company attempts to use advanced AI "agents" to replace human workers (like software engineers, customer support teams, or legal analysts).

Human Efficiency

Humans can skim a 100-page document, pull out a relevant paragraph, and ignore the rest. AI models cannot. Every single time an employee or automated agent asks a follow-up question, the AI must re-read the entire historical conversation and all attached documents from scratch.

If you attach a 50,000-word corporate manual ($66,000 tokens) and ask 10 consecutive questions, you aren't paying for 10 small prompts.

You are paying the input fee for that entire 50,000-word manual 10 separate times.

More Power = More money

Standard models (like GPT-4o Mini or Gemini Flash) are incredibly cheap—often pennies per million tokens. But to replace highly skilled human labor, companies must use advanced reasoning models (like OpenAI's o1/o3 or Anthropic's Claude Opus).

A single highly complex reasoning request can generate hundreds of thousands of invisible, internal tokens. Top-tier reasoning outputs can cost up to $40 to $60 per million tokens. If an automated AI agent runs continuously 24/7, executing thousands of these deep-thinking tasks a day, a single "digital worker" can easily rack up thousands of pounds in fees per week.

The AI "Infinite Loop"

When a human works, they pause when stuck. When an autonomous AI agent is assigned a complex task, like fixing a bug in a massive software codebase, it operates in a continuous loop: it writes code, tests it, hits an error, reads the error log, modifies the code, and tries again.

This loop happens at lightning speed, entirely unmonitored.

If an agent gets stuck in a loop for 8 hours, it can silently burn through tens of millions of high-cost tokens before a human ever intervenes, resulting in an overnight bill that dwarfs a contractor's daily rate.

The Conclusion?

An internal cost-review discussion leaked from a 5,000-employee enterprise highlights this perfectly. Management noticed their AI API bills were skyrocketing month-over-month.

When they modelled whether they could offset those costs by laying off staff, they discovered the maths didn’t work.

Technology transitions historically follow an S-curve. The initial hype makes the tech look flawless and infinitely scalable. The reality phase brings a sharp realisation of infrastructure limits, energy constraints, and ballooning token bills.

AI will absolutely change how we work, but the sheer financial cost of running these models means that human intuition, reasoning, and adaptability remain an incredibly cost-effective asset for businesses.

The Irony? I used Gemini to come up with a lot of the content above.

4

3

1,155

Jun 4

Bitcoin $BTC hitting lows last seen in February. There's a lot of leverage in crypto and it could get ugly.

Strategy (MSTR) has shattered its multi-year "never sell" narrative.

According to their SEC 8-K filing submitted on June 1, 2026, the company disclosed that it sold 32 Bitcoin between May 26 and May 31, generating $2.5 million in proceeds at an average price of $77,135 per coin.

The filing states the reason for the sale: to fund distributions on its preferred stock (including the high-yield STRC).

Strategy's new perpetual preferred stock (STRC) offers a high yield (of around 11.5%)

Whilst 32 Bitcoin is not a huge sale the signal it sends to the market is immense. The loudest preacher of the HODL strategy, just contradicted their own tenet.

Paying a high yield is ok when the price of Bitcoin is rising but when it falls, it could be the start of a death spiral.

Strategy is not the only Bitcoin treasury company that pays a yield, many of them do it with debt. They will all struggle if Bitcoin drops.

They will be forced to sell more bitcoin to cover debts, this results in a further drop in the price of Bitcoin, reducing the company's collateral value, forcing more sales.

1

1

4

3,175

Jun 4

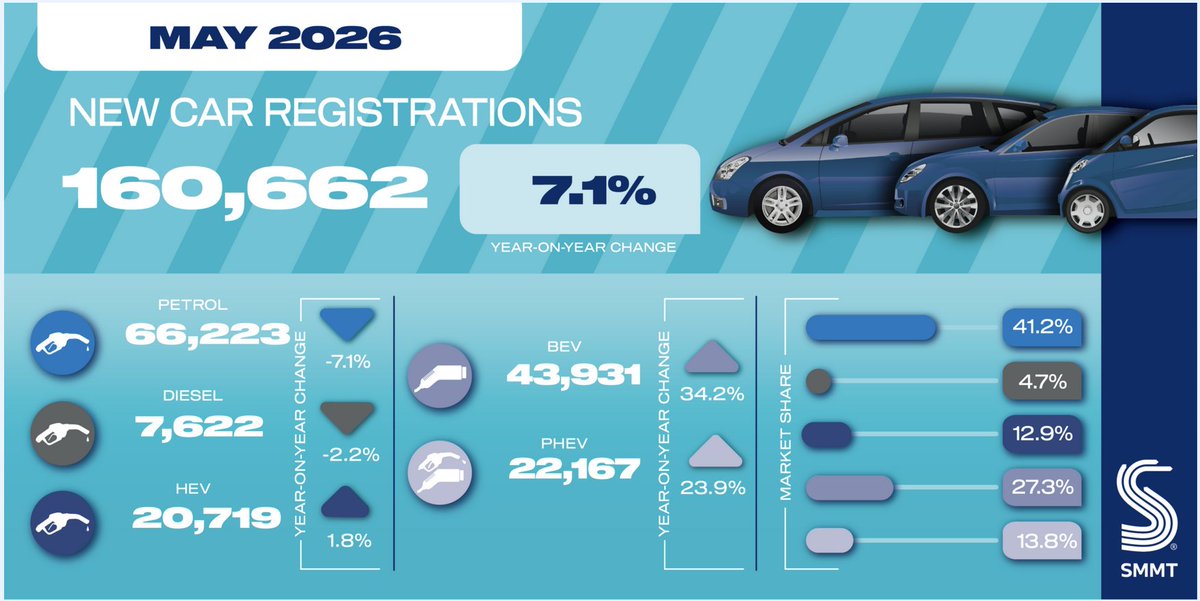

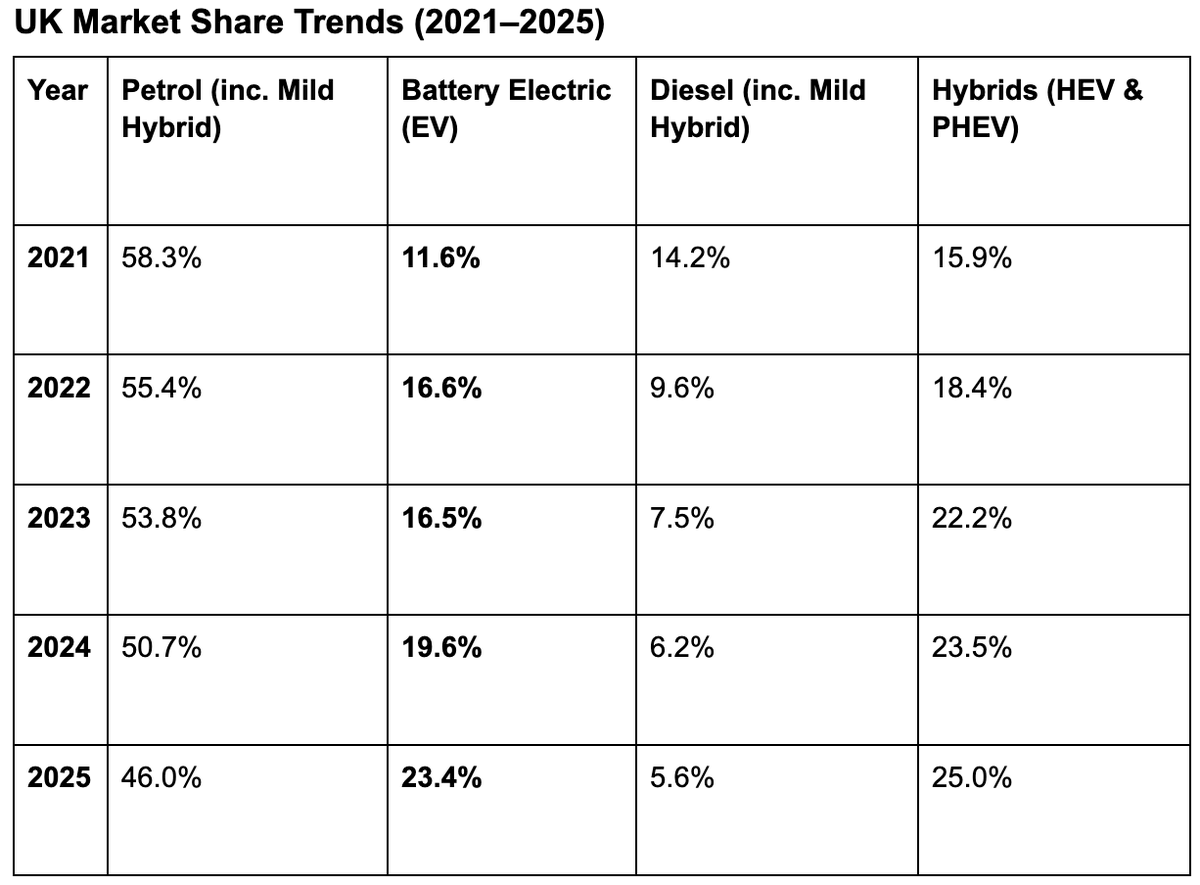

UK May 2026 New Car Registrations shows Electrification Dominates:

- Combined electrified powertrains (BEV, PHEV, and HEV) accounted for 54% of all new car registrations in May 2026 and over half of all registrations YTD.

- Overall Market Growth: Total new car registrations grew by 7.1% in May 2026 (160,662 units) and are up 8.7% Year-to-Date (YTD) to 924,763 units.

- BEV Market Share Surges: Battery Electric Vehicles (BEVs) captured a substantial 27.3% market share in May 2026, up from 21.8% in May 2025.

- Strong BEV Volume Increases: Pure electric registrations rose 34.2% in May (43,931 units) and have increased 24.3% YTD to reach 220,629 units.

- PHEVs Are the Fastest YTD Growers: Plug-in Hybrid Electric Vehicle (PHEV) registrations jumped 41.8% YTD to 121,430 units, boosting their YTD market share to 13.1%.

- Petrol Share is Eroding: Petrol vehicle registrations fell -7.1% in May and 2.5% YTD, causing its YTD market share to drop from 49% down to 41%.

- Diesel Continues to Shrink: Diesel registrations fell now representing a minor 4.7% share of the total 2026 market.

smmt.co.uk/vehicle-data/car-…

3

553

Jun 3

Ramsdens #RFX H1 Results:

- Revenue up 62% to £83.7m

- Gross profit up 48% to £40.1m

- Profit before tax up 173% growth to a record £16.7m

- Interim special dividend of 3p (FY25: 0.5p).

- Total interim dividend is therefore 9p (FY25: 5p).

- The Board currently anticipates that profit before tax for FY26 is expected to be in a range of £30m to £33m, ahead of current market expectations

- All time high.

1

1

869

Justin Waite retweeted

May 21

Solar in 2025 grew 19x faster than experts at the International Energy Agency predicted in 2015.

Solar is now the fastest growing electricity source in human history.

78

345

1,262

129,978

May 21

Along with the dire unemployment figures here’s another set of figures @RachelReevesMP will not mention today:

The Purchase Managers Index (PMI) numbers.

The service sector makes up over 80% of the UK economy. It just collapsed to 47.9. Below 50 means it's in contraction.

Excluding the COVID-19 pandemic lockdowns, this represents the sharpest decline in service sector activity for nearly a decade (since July 2016).

PMI’s monthly economic indicator that tracks prevailing business conditions and sentiment within a specific country or sector.

Unlike official government data (like GDP or employment figures), which looks backward at what already happened, PMIs are forward-looking leading indicators. They offer an immediate, real-time snapshot of the private sector's health right now.

According to Chris Williamson, Chief Business Economist at S&P Global Market Intelligence he describes it as the "perfect storm" hitting the UK economy.

Specifically, he noted that this combination is forcing businesses to battle multiple fronts simultaneously, resulting in:

1. Surging inflation and supply shortages: Spurred by the Middle East conflict, which has driven up energy costs, triggered shipping delays, and added fuel surcharges.

2. Falling output and client hesitancy: Amplified by domestic political uncertainty (with firms highlighting questions over Prime Minister Keir Starmer and leadership succession), which has heavily dented investment sentiment and paused corporate spending.

3. Job cuts: As businesses trim headcount to cope with thinning sales pipelines and sticky overheads.

Note, two of these three problems were created by the government. They have long since dropped their “growth” mantra as every policy they have introduced has had the opposite effect.

Rachel Reeves talked about an IMF growth upgrade recently but they have been upgraded from a series of downgrades since Labour came to power.

IMF Forecasts for 2026:

Mid-2024: 1.5%

Late 2025: 1.2%

April 2026: 0.8%

This shows Labour haven’t a clue what they are doing and worse still they are being disingenous about the numbers they shout about.

The truth is, they are actively damaging businesses with their policies. Enabling and empowering business is the key to growth in the UK, Labour do not understand this.

2

3

7

848

Justin Waite retweeted

May 20

A must read.

We called for a National Emergency Plan for jet fuel to be published, they ignored us.

Ed Miliband has not done the work and is ideology opposed to British oil and gas.

The consequence is that we will now be funding Putin’s war machine.

Disgrace.

May 20

EXCLUSIVE with @EllenAMilligan: UK government officials are blaming each other for the extraordinary situation that has seen Britain loosen sanctions on Russian oil.

The EU will NOT waive sanctions. It means the UK has departed from the EU’s approach and now has looser sanctions on refined Russian oil products than Europe.

UK officials privately concede it weakens the Britain’s case for its G7 allies to maintain and bolster sanctions against Russia.

One says it’s the fault of Keir Starmer and No10 for not taking the lead on measures sooner to prepare for limitations on jet supply.

One says Ed Miliband’s restrictions on expanding energy supply have left the UK in a more vulnerable position. The sanctions waiver highlights how Britain has become more reliant on fuel imports than other major European nations.

Others say the Treasury and Foreign Office have wavered at the first sign of strain. The Foreign Office is unable to explain its position this morning and remarkably DESNZ is declining to comment.

Foreign Affairs Committee chair Emily Thornberry says the people of Ukraine have been "very let down" by the decision to relax sanctions.

“They don’t understand, given that we promised that we would stop this loophole in October, and we still haven’t done it. In fact, it seems to have got worse," Thornberry tells the BBC.

bloomberg.com/news/articles/…

47

282

1,107

67,380

May 20

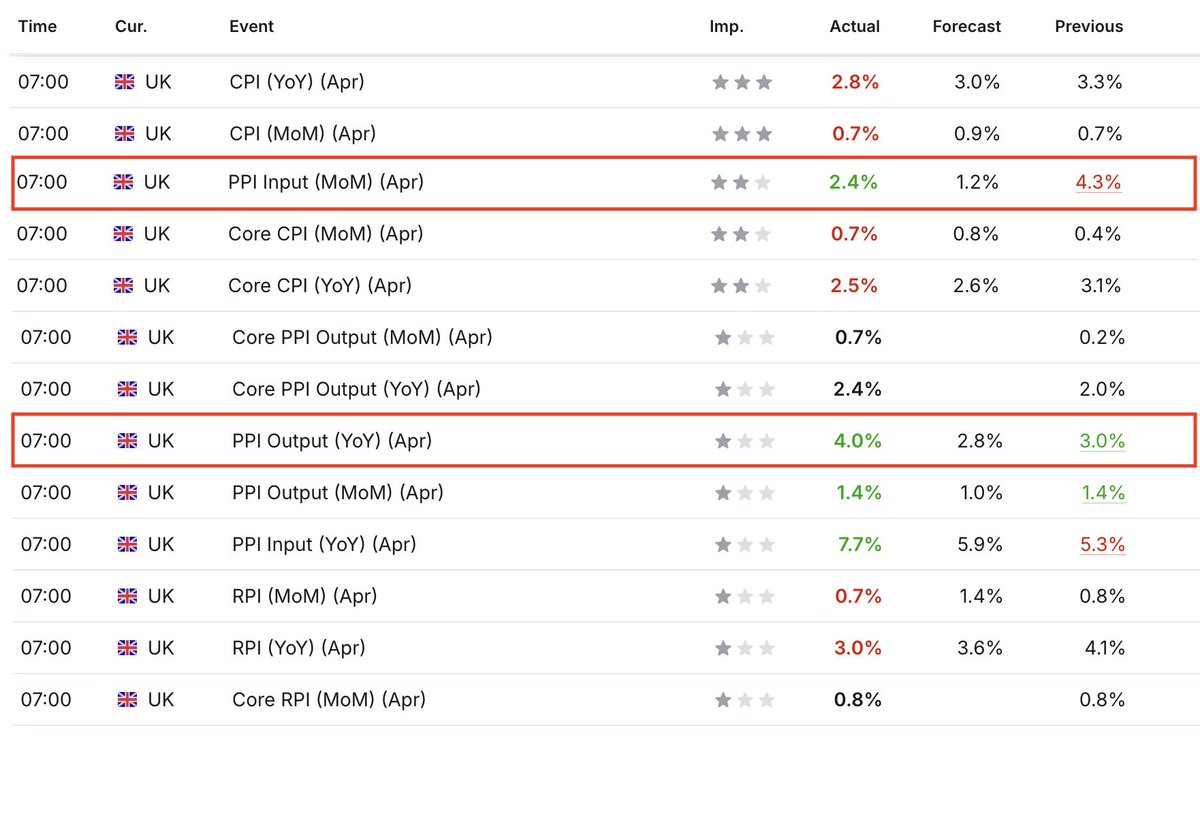

This is why you were trounced in the local elections. You pick and choose the figures that suit you and not the ones that mean the most to the people of this country. Inflation is down to the energy cap. This will go up by 13% in July.

PPI is up above expectations. That is what we can expect in the next set of inflation numbers.

I see you didn’t mention yesterday’s employment numbers because the unemployment rate rose to 5.0%

Payrolled employees in April 2026 showed a monthly drop of 100,000 roles, one of the steepest single-month contractions outside of the pandemic.

Youth Unemployment climbed sharply to 16.2% up significantly from 14.2% a year ago and represents the highest level of youth joblessness in over a decade.

Interest rates are nothing to do with you, the Bank of England would have lowered them earlier if you hadn’t increased pay and taxes on business. They are now forecast to go up but they were lowered due to weak growth.

Back in December the BoE stated: "Consistent with evidence of subdued economic growth and building slack in the labour market, pay growth and services price inflation have continued to ease"

The cost of UK debt is the highest amongst the G7 countries because we are a high risk unstable environment exposed to high energy costs and yet your government ban North Sea Oil & Gas but imports it from Norway who get it from the same place!

The public are not as stupid as you think they are and you will find out this when you are given the boot at the next elections.

May 20

Growth higher than forecast, borrowing down, and now inflation falling further than expected.

This Labour government has the right economic plan.

4

3

15

2,245

Justin Waite retweeted

May 20

After 18 months of “standing up to Putin” the Labour govt quietly issued a licence allowing imports of Russian oil refined in third countries.

Yesterday Labour MPs voted AGAINST UK oil and gas licences.

We are now importing from Russia instead of drilling in the North Sea.

Insane.

May 19

BREAKING: UK waives some Russian oil sanctions, allowing imports of diesel and jet fuel processed in third countries from Russian crude

(most likely supply chain: imports of Indian refined products produced by processing Russian crude).

gov.uk/government/publicatio…

984

5,251

19,927

809,624

May 20

Inflation comes in below expectations due to energy price cap but look at PPI.

PPI is a leading indicator of Inflation.

If the costs of raw materials, energy, and manufacturing rise, factories generally do one of two things: absorb the costs (hurting profit margins) or pass them down the supply chain. Because of this, a rising PPI often signals that a rise in the CPI is coming a few months later.

2

2

9

1,066

May 18

In the next few weeks we could experience a Global Arbitrage Domino Effect.

Around the world different regions are feeling the effects of the Strait of Hormuz being closed at different rates.

May – June 2026: The Far East

Developing economies in the Far East (such as Bangladesh and parts of Southeast Asia) that lack deep strategic oil reserves are already hitting critical threshold limits by April and May. This has already triggered strict energy rationing, early commercial shutdowns, and sharp contractions in industrial output.

June – July 2026: Europe

European jet fuel and middle distillate tightness began escalating sharply through late April. Europe is running dangerously low on specific product categories because it cannot easily replace the highly sophisticated mega-refineries of the Persian Gulf, which specialize in processing heavy, sour Middle Eastern crudes into diesel.

You might think that the two biggest economies of the world, the U.S. & China has plenty of reserves so it shouldn’t be a problem.

The issue is in the physical commodities markets, a shortage in one region cannot be contained. It triggers a frantic, borderless bidding war that rapidly exports price inflation and physical scarcity to every corner of the globe.

So far the markets are shrugging this off.

Right now, the Magnificent 7 are operating like an economic shield. Their stellar earnings reports and the staggering capital expenditure (CapEx) boom into AI data centres are acting as a powerful narrative machine, blinding broader stock markets to the gathering physical supply shocks.

But AI data centres and tech giants are not virtual entities living in a frictionless "cloud." They are massive consumer engines of physical steel, concrete, silicon, copper, and—above all else—electricity.

If commodity costs continue to rise due to the Middle Eastern domino effect, the tech sector's AI ambitions are going to run head-first into a physical brick wall.

Jeff Currie, the former long-time head of commodities research at Goldman Sachs who recently stepped into an executive role at Abaxx Markets says, “Equity markets are operating in 'la la land' regarding the Middle East. They are overlooking structural shortages and treating a massive physical supply disruption as a temporary blip. The real cost of crude and refined products is completely detached from what paper benchmarks are showing. I just don't understand how people can just ignore the severity of what is coming their direction.” 👇👇👇

x.com/CommodMkt/status/20563…

May 18

Thank you to @SquawkBoxEurope for inviting me on this morning to discuss the structural shifts reshaping commodities and energy markets, as well as a deeper dive into AI and the problems we face with the commodities that fuel it.

A lot covered off but a pleasure as always Steve Sedgwick and co: cnb.cx/4fpHZsb

1

9

1,411