Joined March 2022

- Tweets 7,728

- Following 78

- Followers 16,186

- Likes 252

4,624 Photos and videos

Pinned Tweet

Jun 2

Big milestone 🚀

SignalPlus has officially closed our latest US$50M Series B1 funding round at a US$500M post-money valuation.

The round was led by our long-term supporters at HashKey Capital @HashKey_Capital, with strategic participation from BlockBooster @0xBlockBooster and AppWorks @AppWorks.

Deeply grateful to the Goldman Sachs team @GoldmanSachs for acting as our sole financial advisor.

We extend our deepest gratitude to our clients, partners, investors, and team members for their unwavering trust and support over the years.

The Next Chapter: TradFi Expansion & SignalPlus 2.0

Onwards and upwards!

prnewswire.com/news-releases…

12

11

54

6,361

Jun 12

Quick weekly comment:

Volatile week in macro markets as the liquidity drain ahead of upcoming IPOs was compounded initially by fears of accelerating inflation ahead of Wednesday’s CPI print, before re-escalation of rhetoric on the US/Israel - Iran war pushed equity markets another leg lower. However Trump quickly U-turned once more on Thursday before risk-off sentiment could materially extend, calling off strikes and promising a deal (for almost the 40th time in the past 6 weeks …).

For crypto, BTC price action was actually constructive this week ahead of the psychological support level of $60k, confirming our view that it was the first asset class to suffer the liquidity drain given its ongoing underperformance in the past 12-18 months. With positioning clearly lighter and some real demand seen around the $60k, spot was able to find a base and rally back above $63k despite the backdrop. Vols inflated significantly across the curve this week after the high realised of the prior 2 weeks fed through, but realised this week has already dropped back into the high 30s/ low 40s on a high frequency basis, again indicative of lighter positioning and flows out there. Skews have attempted to normalise (less bid for puts) as the worries of a liquidity event below 55-50k have eased , though spot vol correlation remains clear with implied vols softening to end the week with spot back above $63k. Barring any material re escalation on the geopolitical front, we anticipate cross asset markets will quieten down in the coming weeks as we approach the heart of summer and the World Cup kicks off, and this should see implied vols in the <3m expiries soften materially to price this seasonality. However given the broader macro landscape and the midterm elections, we are expecting Q4 to bring some volatility once more.

142

Jun 12

📢 More Bybit Altcoin Options Now Available on SignalPlus

🚀 Newly Supported Options Products: DOGE, XRP, MNT, and XAUT

👉 Connect your Bybit API at t.signalplus.com to trade options, spot, and futures.

2

125

Jun 10

⚽️ SignalPlus World Cup Event Has Successfully Concluded!

🎉 Congratulations to all our winners!

🥉 Warm-up: 32 participants won a Tetris Game Console

🥈 Group Stage: 22 participants won a 2-Player Tabletop Soccer

🏅 Round of 32: 16 participants won a Pac-Man Mini Arcade

🏆 Final: Gold won a 26-inch Dual Joystick Arcade

📬 Please check your email for details on how to claim your prize.

👾 Stay tuned for more exciting events: t.signalplus.com/nuwa/rank

3

310

Jun 8

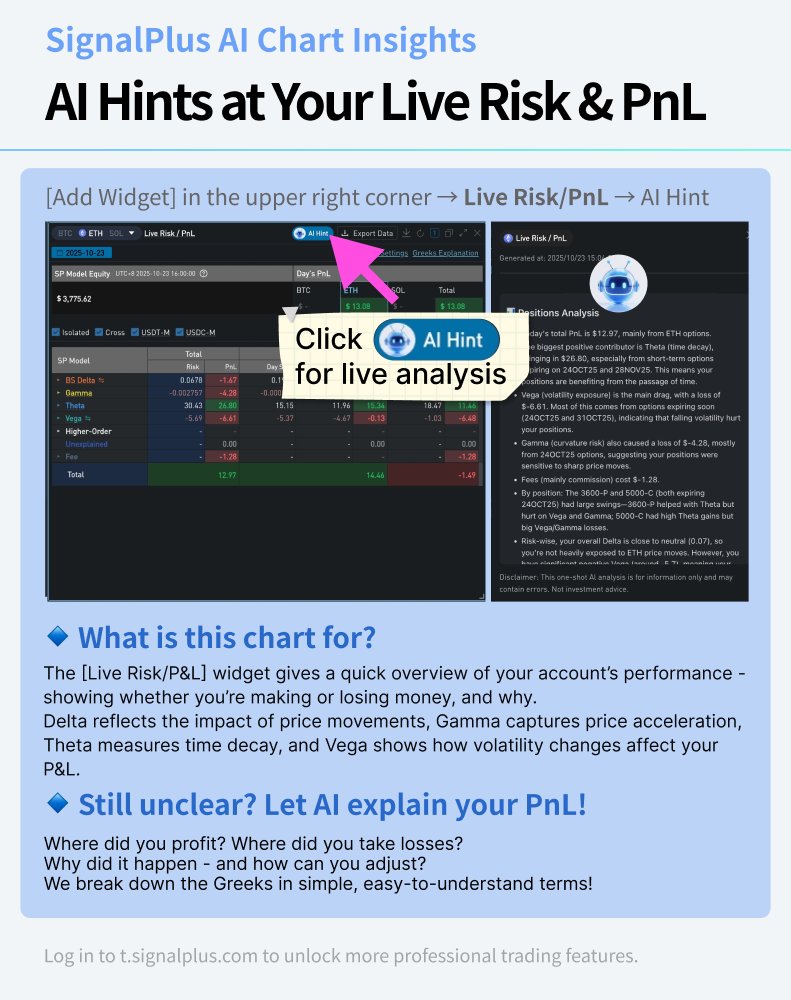

Stop being confused about your P&L!

Let AI instantly interpret your live risk and P&L:

💡 See where you made money, where you lost it - and why.

AI automatically attributes your P&L so you can understand it at a glance.

📖 Greeks in plain language.

Did you earn from time decay (Theta) or lose to volatility (Vega)?

🧭 AI scans all your positions to identify your biggest risk exposures and help you defuse potential landmines.

4

253

Jun 8

🎮 SignalPlus football event winners will be announced this Wednesday at 8:00 UTC

⚽ Haven't joined the action yet? There's still time! Jump in now and compete for a chance to win before the event ends.

👾 t.signalplus.com/nuwa/rank

2

4

426

Jun 5

📢 New Widget | OI by Expiration & Strike

Where is the market positioned?

Track open interest across expiries and strikes to identify positioning concentration, key expiry dates, and important market levels.

🔍 Positioning concentration

📅 Key expiries

🎯 Important strike levels

👉 t.signalplus.com

1

4

332

SignalPlus retweeted

Jun 3

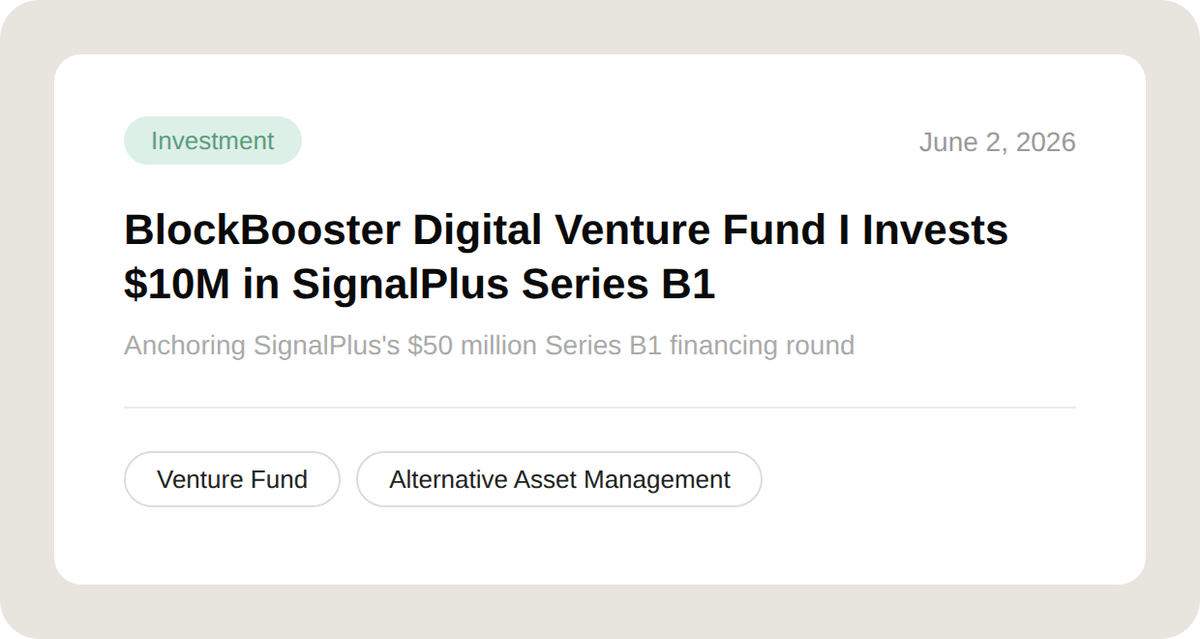

BlockBooster Fund I has made its first investment.

$10M anchor commitment to @SignalPlus_Web3, in its $50M Series B1 round, advised by @GoldmanSachs.

SignalPlus runs the leading derivatives terminal for institutions in digital assets, now extending into traditional finance. We are committed to staying an active partner as SignalPlus continues to expand.

Read the full announcement → blockbooster.io/news/block-b…

9

39

56

1,880,388

Read our latest edition of Leaders in Crypto with @SignalPlus_Web3 Partner & CFO Augustine Fan @tangpingnomics.

Augustine shares his insights on the convergence of Crypto, TradFi, and agentic AI, the current bear market challenges, and more.

Read below:

medium.com/@lvrgpr/signalplu…

1

1

3

1,338

Jun 4

👀 Do any of these sound familiar?

💭 You lost money today, but don’t know where it went?

💭 Your strategy felt solid—so why aren’t you making money?

💭 Wondering how to make smarter, data-driven trading decisions?

🔑 The answer lies in SignalPlus’ powerful features: Real-Time Risk/P&L and P&L Attribution.

From daily PnL breakdowns to insights by Greek letter, position, expiry date, and even weekly and monthly performance - everything is covered.

📊 All data is fully customizable, supporting both crypto and USDT denominations, with flexible Greek parameter settings tailored to your trading style.

⭐ Try it free now: t.signalplus.com (Or download the app: signalplus.com/#/app)

1

1

299

Jun 3

BTC Vol — week in review 18May–1Jun 2026

The momentum higher in spot has waned over the last couple of weeks, retracing back through some local support levels...

Read more 👇

🔗 medium.com/signalplus-offici…

#BTC #Crypto #options #macro #stock #volatility

1

4

409

May 27

🚨 TODAY’S X SPACE

Building a 24/7 AI Trading Assistant

SignalPlus × @0xEvinho

Join us live 👇x.com/i/spaces/1qKVmmyYQOAxB

We’re diving into:

OpenClaw / Hermes / n8n

AI-native crypto trading

The future of AI trading infrastructure

What actually happens when AI starts interacting with real trading workflows? 👀

Scan to join our SignalPlus AI Trader Hub Community

We’ll randomly select 3 listeners to win 10 USDT each 🚀

6

7

21

2,871

May 27

6

10

16

1,223

May 26

🤯 Still stuck using Excel for manual bookkeeping?

😵💫 Tired of constantly switching between exchange apps?

Say goodbye to the hassle! Create cross-exchange portfolios and view your total assets and overall profit/loss at a glance.

8

1,094

May 25

Stop being confused about your P&L!

Let AI instantly interpret your live risk and P&L:

💡 See where you made money, where you lost it - and why.

AI automatically attributes your P&L so you can understand it at a glance.

📖 Greeks in plain language.

Did you earn from time decay (Theta) or lose to volatility (Vega)?

🧭 AI scans all your positions to identify your biggest risk exposures and help you defuse potential landmines.

4

937

May 21

💡 One-click selection of basic standard strategies

SignalPlus offers 10 basic options strategies, allowing you to quickly switch strategies for more convenient operations!

1

4

827

May 19

BTC Vol — week in review 11–18 May 2026

Price action remains reasonably consistent with a broad consolidation phase, noting decent support below at $76-75k and then again at $74k...

Read more 👇

🔗 medium.com/signalplus-offici…

#BTC #Crypto #options #macro #stock #volatility

2

733