Enable crypto investment for the global masses. Cut the noise, find true value. Join SoDEX sodex.com 🌲 linktr.ee/SoSoValueCrypto

Joined April 2022

- Tweets 4,743

- Following 21

- Followers 1,001,125

- Likes 3,209

1,609 Photos and videos

Pinned Tweet

Feb 3

10,173

7,405

29,707

1,023,181

Jun 13

Big day for Space X.

See views from our research community and check out the brand new RWA Research Hub. 👇

5,050

111

462

58,496

SoSoValue retweeted

Jun 12

By community request, you can now Trade SpaceX ($SPCX) with up to 20x leverage. 🚀

RWA Trading Tournament is LIVE on SoDEX with $1,000,000 total prize.

Round 1 (June 12 - June 19)

Trade $SPCX to win the first $100,000 prize pool. More rounds to be unlocked if the $SPCX volume breaks $150M.

The first 3,000 traders who achieve $5,000 volume will receive $10 each.

Multi-asset margin feature is now LIVE on SoDEX: use $SOSO as collateral for your $SPCX trading to boost your share of the $100,000 prize pool.

👉Trade now:SoDEX.com/trade/futures/SPCX…

#SoDEX #SpaceX #RWA

379

57

274

52,673

Jun 12

$SOSO EXP S2 Airdrop Claim is now live. Congrats!

We're excited to announce two new utilities for $SOSO:

1️⃣ RWA Research Hub is live

Tech is shaping the world and Valuechain makes it accessible to everyone Stake $SOSO to vote and onboard top tech assets to ValueChain.

2️⃣ Multi-Asset Margin is enabled on SoDEX

Trade with $SOSO as collateral in your margin account, alongside $BTC, $ETH and $XAUT.

Now, claim your $SOSO, explore the RWA Research Hub, trade $SPCX and share the $100,000 prize pool.

Claim now: sosovalue.com/exp

Research Hub: sodex.com/research

2,655

285

1,452

332,521

Jun 12

Update on EXP Season 2 Airdrop Checker EXP Season 2 has been an incredible journey!

Participation and data metrics have far blown past Season 1, and our team is currently running final checks on the full dataset.

Because we’re still processing a massive amount of data, the opening of Airdrop Checker (initially set for 12:00 UTC today) will need just a bit more time.

We are grinding hard to push this out and expect the page will go live within the next 8 hours.

We’ll drop the official link here once it's ready. 🔔

Huge thanks for your patience and stay tuned! 🤝

— SoSoValue Team

2,348

913

4,565

190,580

Jun 12

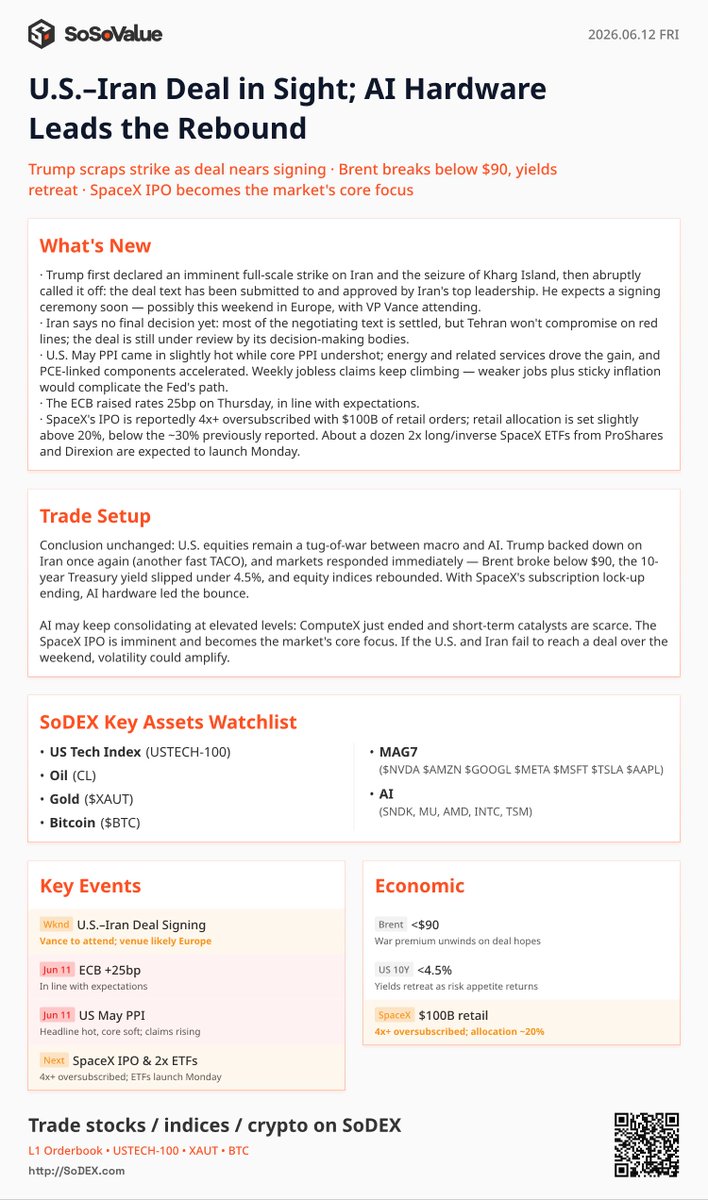

SoSoValue Flash: Trump Brinkmanship De-escalates to Lift Sentiment, SpaceX Capital Unlock Triggers Hardware Rebound

💥 Core Catalyst:

The Middle East geopolitical theater experienced a sudden u-turn. Trump initially declared an imminent full-scale strike on Iran and the immediate seizure of Kharg Island, only to abruptly stand down as the framework text was finalized and approved by Iran's senior leadership. Trump expects a formal signing ceremony shortly in Europe, with VP Vance attending. However, Iran noted that "no final decision has been made" yet; while most of the text is settled, Tehran refuses to compromise on its core red lines, and the draft remains under structural review.

🔍 Key Logic Shifts:

1️⃣ Macro & Yields: Trump's abrupt policy pivot (another rapid TACO) triggered a rapid decompression in risk premiums. Brent crude broke below $90 and the 10Y Treasury yield slipped under 4.5%. However, underlying macro signals remain mixed: the May PPI print arrived slightly hot while core PPI undershot, driven by sticky energy services. Concurrently, weekly jobless claims continue to climb, leaving the Fed stuck in a complex stagflationary "weaker jobs sticky inflation" bottleneck.

2️⃣ Liquidity & SpaceX: The historic SpaceX IPO is materializing with overwhelming demand. Reports indicate the deal is over 4x oversubscribed with a staggering $100B in retail orders alone, forcing the retail allocation to compress slightly above 20%. Crucially, the expiration of this massive subscription capital lock-up has released vast amounts of idle cash back into the financial system, instantly alleviating the secondary market's recent liquidity drain.

3️⃣ Sector Rotation: Seizing on the newly unlocked dry powder, the highly crowded AI hardware clusters (Memory, CPU, and Foundries) spearheaded a broad-based index rebound. With the broader technology sector in a near-term catalyst vacuum following the conclusion of ComputeX, AI is expected to continue its high-altitude consolidation, while attention swings to the Monday launch of over a dozen 2x leveraged long/inverse SpaceX ETFs from ProShares and Direxion. Additionally, the ECB delivered a well-anticipated 25bp rate hike on Thursday.

📊 Trade Setup (SoDEX Assets to Watch):

Core: $USTECH-100 | $CL (Crude) | $XAUT | $BTC

MAG7: $NVDA | $AMZN | $GOOGL | $META | $MSFT | $TSLA | $AAPL

AI Hardware: $SNDK | $MU | $AMD | $INTC | $TSM

7,874

255

976

65,808

Jun 12

13

54

223

15,404

Jun 12

Oracle, Broadcom, Ciena — solid earnings across the board, and the market didn't care.

How do you trade AI infrastructure from here? Join the SoSoValue research community and let's talk 👇

Jun 11

Oracle reported earnings today. I opened its chart on SoDEX — the stock was down nearly 12% in pre-market trading.

sodex.com/join/JELLYZ

This is not an isolated case. Over the past week, three key companies across the AI infrastructure chain reported earnings, and the market reaction was surprisingly consistent:

- June 3: Broadcom reported FY2026 Q2. Results beat — the stock sold off sharply.

- June 4: Ciena reported FY2026 Q2. Results beat — the stock also fell sharply.

- June 10, after the close: Oracle reported FY2026 Q4. Results beat — the stock dropped anyway.

Three earnings reports. None of them were bad. Three stock reactions. None of them went up.

So what went wrong?

First, Oracle: strong demand, but heavy financing pressure.

The numbers were solid: Q4 revenue of $19.18B, up 21% YoY; adjusted EPS of $2.11; OCI cloud infrastructure revenue up 93% YoY.

The problem is not demand. The problem is investment. In FY2026, Oracle's CapEx reached $55.66B while free cash flow was -$23.69B. FY2027 CapEx could reach as high as $95B, funded by continued debt and equity financing for AI data center construction.

Oracle's central tension is clear: AI cloud orders are strong, but fulfilling them requires massive upfront spending on data centers, GPUs, networking, power, and land. The market isn't worried about whether demand exists — it's worried about whether these orders can generate a high enough return on capital, and when free cash flow will turn positive again.

Then Broadcom: the business is strong, but expectations are too high.

Revenue was $22.19B, up 48% YoY; AI semiconductor revenue was $10.8B, up 143% YoY. Very strong — yet the stock still fell.

Expectations for core AI suppliers have become extreme. Broadcom guided Q3 AI chip revenue to around $16B — strong, but not enough for the market's more aggressive hopes. Broadcom didn't fall because AI ASIC and networking demand is weak. It fell because the stock had already priced in too much of the future.

Finally, Ciena: revenue beat, but the trade was too crowded.

Revenue was $1.57B, up 40% YoY; adjusted EPS was $1.64, up 290%; full-year revenue guidance was raised to around $6.3B. Again, not a bad report.

Ciena's problem: the market had long been trading it as a core beneficiary of AI optical networking — AI data centers need higher-bandwidth, lower-latency optical connections, and Ciena sits directly in that part of the chain. But after a sharp year-to-date rally, the bar for another positive surprise was simply too high.

Three companies, one signal.

Oracle provides cloud and databases. Broadcom provides ASICs, AI networking chips, and infrastructure software. Ciena provides optical networking and data center interconnects. Placed inside the AI infrastructure chain, they are links in the same chain:

AI data center construction → AI ASICs / networking chips → optical networking / interconnects → cloud revenue and compute monetization

Look at all three together and the signal is clear: AI infrastructure trading is moving from phase one to phase two.

In phase one, the market bought the narrative: who has AI orders, who is in the chain, who benefits from data center expansion.

In phase two, the market buys verification: can orders turn into revenue, revenue into profit, profit into free cash flow? Can CapEx generate enough ROIC? Is valuation already stretched? Can guidance keep moving higher?

The selloffs across all three companies show that the market will keep trading AI — but it will no longer blindly reward every AI infrastructure company.

Going forward, the real upside may belong to two types of companies: the surest recipients of AI CapEx dollars — GPU, ASIC, HBM, networking, and power chain companies — and the operators that can prove CapEx returns by turning orders into revenue, profit, and free cash flow.

If you also follow U.S. AI stocks, you can view and trade related U.S. equity contracts on SoDEX, including $ORCL, $MU, and other AI infrastructure names.

3,700

292

969

49,400

Jun 11

SoSoValue Flash: Severe Geopolitical Reignited, CPI Holds Steady, Heavy Capex Warnings Trigger Tech Volatility

💥 Core Catalyst:

The Middle East situation has sharply re-escalated. Dissatisfied with slow talks, Trump threatened to target Iran's power plants and bridges if a deal isn't signed. Following the downing of a U.S. Apache helicopter, the U.S. launched nearly 4 hours of retaliatory airstrikes, claiming Iran's control capability in the strait was eliminated (which Iran denies). In response, Iran issued stern warnings and the Strait of Hormuz has been fully closed. Iran fired dozens of ballistic missiles and drones at 21 key strategic Gulf targets, including a U.S. base in Jordan.

🔍 Key Logic Shifts:

1️⃣ Macro Risks: Trump's hawkish military threats have fundamentally disrupted the market’s prior baseline assumption that he would avoid reopening active hostilities. However, the macro front received some insulation as the May CPI print arrived broadly in line (with core slightly below expectations). Feared second-round effects from oil pass-through, World Cup distortions, and endogenous inflation failed to materialize.

2️⃣ Liquidity Drain: U.S. equities remain locked in a tug-of-war between macro anxiety and secular AI momentum. On the capital front, the ongoing SpaceX IPO continues to absorb significant institutional liquidity. The trading desk notes a broader decline in secondary market depth, which is amplifying short-term volatility across major indices.

3️⃣ Capex Concerns: AI momentum continues to consolidate at elevated levels during a post-ComputeX catalyst vacuum. While Oracle's post-close earnings and guidance matched consensus, its massive $40 billion equity and debt fundraising blueprint for the next fiscal year reignited fierce market anxieties over over-extended capex. Shares plunged 11% after-hours, acting as a direct drag on tech sentiment.

📊 Trade Setup (SoDEX Assets to Watch):

Core: $USTECH-100 | $CL (Crude) | $XAUT | $BTC

MAG7: $NVDA | $AMZN | $GOOGL | $META | $MSFT | $TSLA | $AAPL

AI Hardware: $SNDK | $MU | $AMD | $INTC | $TSM

15,555

451

1,242

64,798

Jun 11

16

151

321

11,687

Jun 10

🚀 Claude just dropped Fable 5 & Mythos 5 — and we want YOUR take.

Reply with your honest experience 👇

💬 Share your Fable 5 / Mythos 5 experience below — pros, cons, anything real.

📸 Must include screenshots or video — text-only replies won't qualify.

⏰ Deadline: Friday 18:00 (UTC 8) 🏆 Top 10 by likes bookmarks = 100 $SOSO each

Your signal matters. Let's hear it. 👇

Introducing Claude Fable 5: a Mythos-class model that we’ve made safe for general use.

Its capabilities exceed those of any model we’ve ever made generally available.

8,107

429

1,262

49,139

Jun 10

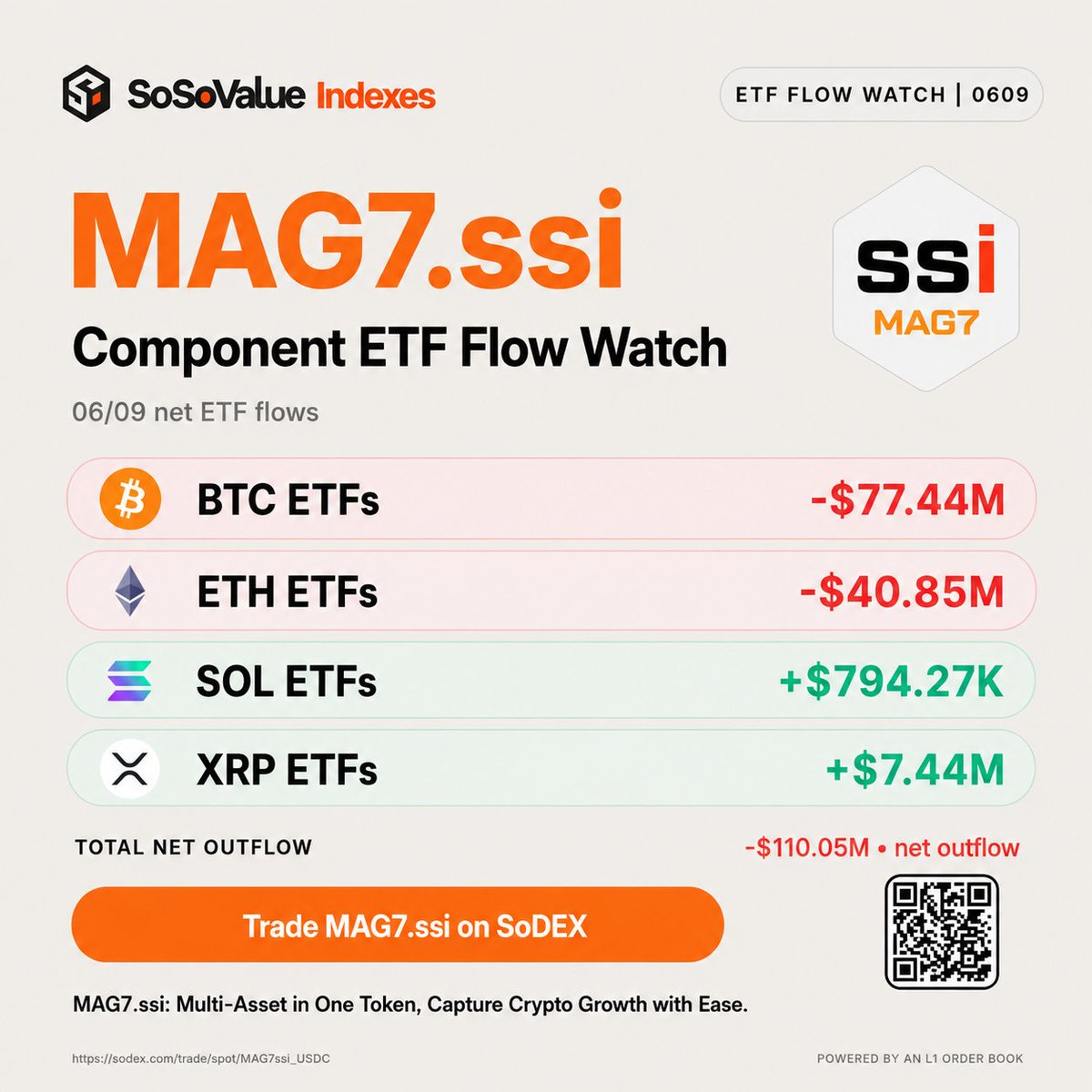

MAG7.ssi Component ETF Flow Watch | 0609

BTC ETFs: -$77.44M Net Inflow

ETH ETFs: -$40.85M Net Inflow

SOL ETFs: $794.27K Net Inflow

XRP ETFs: $7.44M Net Inflow

MAG7.ssi:

Multi-Asset in One Token, Capture Crypto Growth with Ease.

Trade MAG7.ssi on SoDEX — powered by an L1 order book:

sodex.com/trade/spot/MAG7ssi…

#BTC #ETH #SOL #XRP #ETF #Crypto #MAG7ssi #SoDEX

6,634

475

1,338

45,492

Jun 9

A useful read on why AI CapEx matters beyond Nvidia. 👇

Jun 9

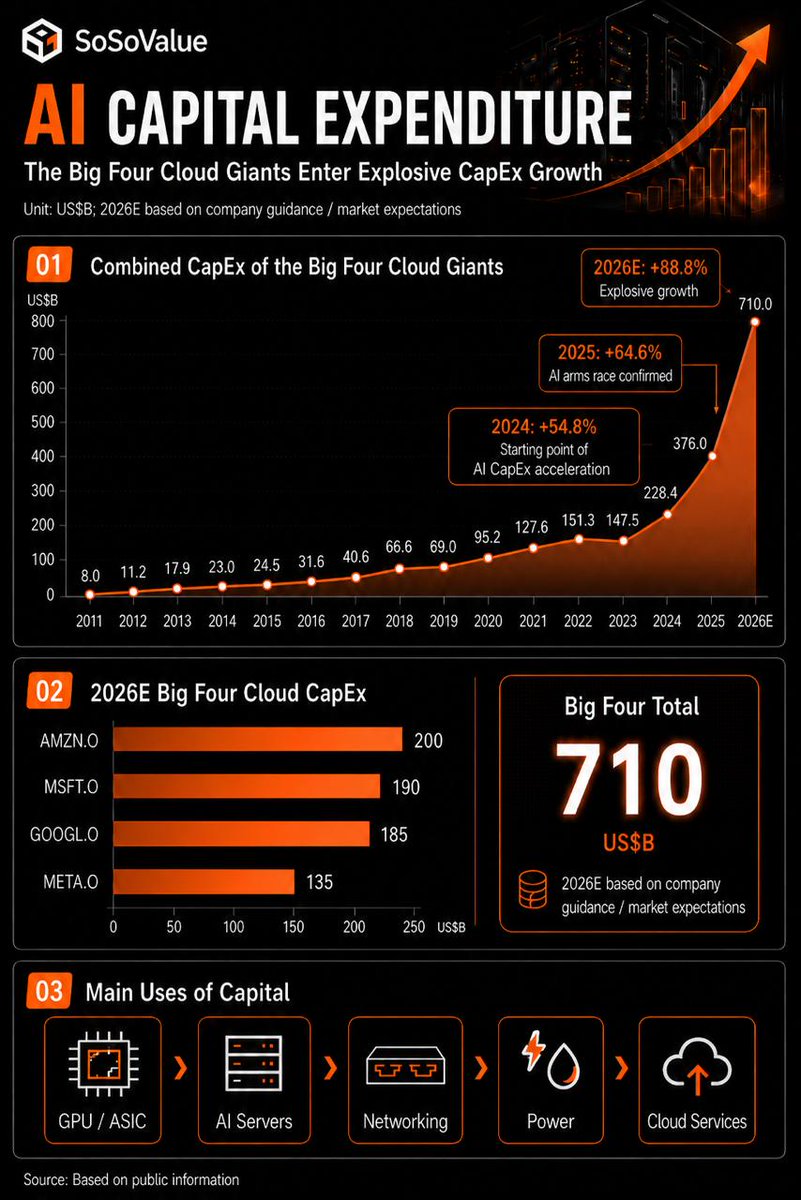

Why should AI stock investors pay attention to AI CapEx?

AI capital expenditure refers to the fixed-asset investments cloud giants like Amazon, Microsoft, Google and Meta — plus some vertical AI players — make in GPU clusters, data centers, networking, storage and power infrastructure. In essence, it's the starting point of the entire AI supply chain.

Once hyperscalers raise CapEx, capital flows down the chain:

GPU / ASIC → HBM → AI servers → networking equipment → data centers → power infrastructure → cloud revenue

That's why the pace of AI CapEx directly reflects compute demand, supply-chain orders, application innovation and the ability of AI products to scale.

Looking at the data, the CapEx cycle of the four major cloud giants (Amazon, Microsoft, Google, Meta) splits into four stages:

2011–2023: Traditional cloud expansion. CapEx was driven by enterprise cloud migration, SaaS, video, advertising, e-commerce and storage.

2024: An extraordinary acceleration begins. After being down 2.5% YoY in 2023, combined CapEx jumped 54.8% to $228.4 billion. Post-ChatGPT and GPT-4, AI infrastructure had firmly entered the tech giants' budgets.

2025: The arms race confirmed. CapEx grew a further 64.6% to $376 billion — proof that 2024 wasn't a one-off rebound, but the start of sustained expansion in AI compute demand.

2026: Explosive growth. On current guidance, combined CapEx could reach $710 billion, up nearly 89% YoY. This is no longer an extension of the cloud cycle — it's a massive buildout as tech giants race to secure the next generation of compute.

And the expansion is far from over. As free cash flow gets consumed by CapEx, the giants are leaning more on external financing: Alphabet recently moved forward with an equity raise of around $80–85 billion, and Meta is exploring more options to fund its data center buildout.

So where is the money going?

1. AI chips and accelerators — Nvidia and AMD GPUs, Google TPUs, Amazon Trainium, Microsoft Maia. The most visible part of the spend.

2. HBM, DRAM and enterprise SSDs — model parameters, training data and inference cache all need high-speed memory; the stronger the GPU, the greater the demand.

3. AI servers and rack-scale systems — hyperscalers buy full servers and, increasingly, rack-scale systems like GB200 and GB300, not individual GPUs.

4. Networking and optical modules — training spans thousands of GPUs, so switches, NICs, optical modules and interconnects become critical.

5. Data centers and power — land, buildings, liquid cooling, transformers, grid connections and long-term power agreements, all built for high power density.

So AI CapEx isn't just about buying GPUs — it's about building an entire "compute factory." That's why the AI trade has widened from Nvidia to HBM, memory, servers, optical modules, data centers, power equipment and liquid cooling.

For investors, the real question isn't how much the giants spend — it's whether that spending converts into large, sustainable AI revenue. Short term, CapEx means supply-chain orders; medium term, cloud compute capacity; long term, the winner won't be whoever spends the most, but whoever turns each dollar of CapEx into the most revenue and profit.

This cycle may look like a model race on the surface. Underneath, it's a race for compute, power, memory and data center capacity.

Therefore, the Big Four cloud giants — along with the core suppliers capturing the largest share of AI CapEx — are the key players in this AI infrastructure cycle.

If you want to invest in this theme, you can trade them on @sodex_official such as $GOOGL, $MSFT, $MU and $SNDK.

sodex.com/join/JELLYZ

#SoDEX #SoSoValue #AI

9,317

487

1,308

72,061

Jun 9

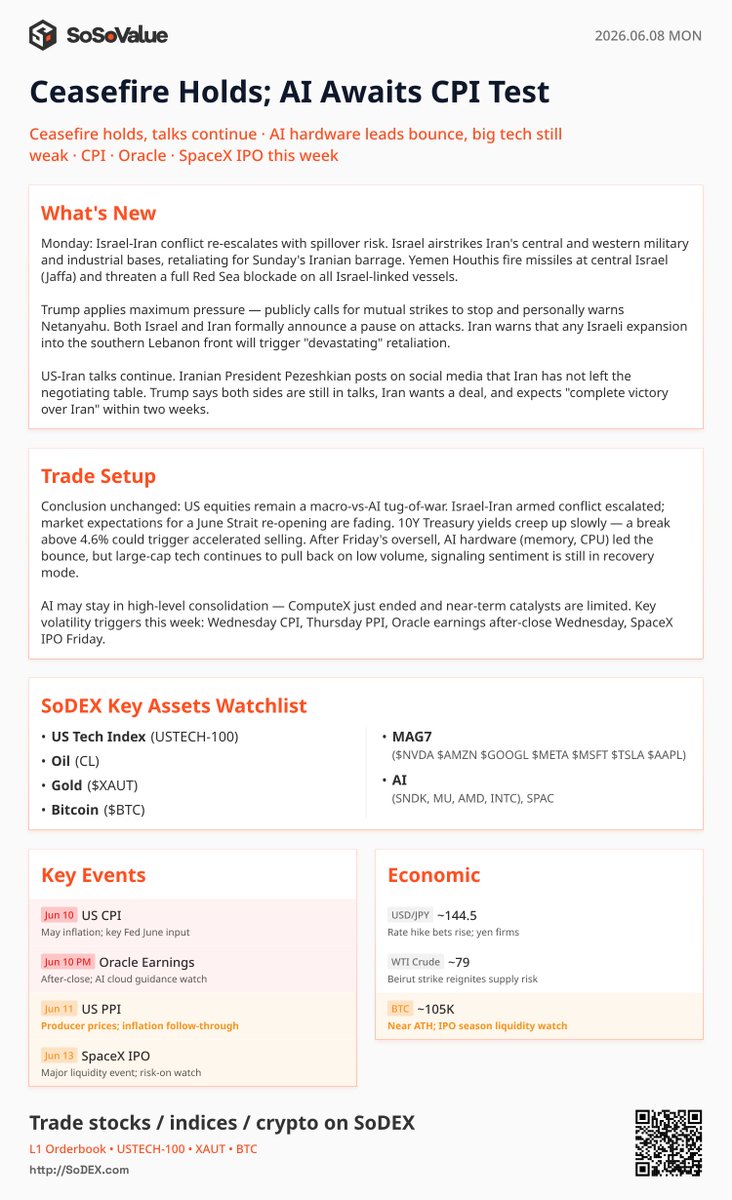

SoSoValue Flash: Israel-Iran Conflict Pauses Under Maximum Pressure, Markets Face Catalyst Vacuum Ahead of Volatility Week

💥 Core Catalyst:

The Israel-Iran conflict re-escalated on Monday as Israel struck central and western Iranian targets in retaliation for Sunday's strikes, while Houthi rebels launched missiles at central Israel and threatened a full Red Sea blockade. Following Trump's maximum pressure and a call to Netanyahu, both sides formally announced a suspension of mutual attacks. Meanwhile, U.S.-Iran talks continue; Iran's President stated they remain at the table, and Trump claimed negotiations are ongoing with a path to "total victory" within two weeks.

🔍 Key Logic Shifts:

1️⃣ Macro & Yields: The military escalation has weakened market expectations for a June strait reopening. The 10Y Treasury yield is slowly edging higher, building macro pressure; a clean break above 4.6% could trigger accelerated selling. Overall, U.S. equities remain locked in a tactical tug-of-war between macro and AI forces.

2️⃣ Sector Rotation: Following Friday's oversold conditions, the most tightly crowded AI hardware clusters—memory and CPU—staged the earliest rebound. Conversely, mega-cap tech stocks continue their orderly pullback on thin overall market volume, indicating that broader risk appetite is still in a recovery phase.

3️⃣ AI & Volatility: With ComputeX now concluded, the AI sector has entered a short-term catalyst vacuum, favoring a high-altitude consolidation pattern. Volatility is expected to spike later this week, driven sequentially by Wednesday's CPI, Thursday's PPI, Wednesday's post-close Oracle earnings, and Friday's highly anticipated SpaceX (SPCX) IPO.

📊 Trade Setup (SoDEX Assets to Watch):

Core: $USTECH-100 | $CL (Crude) | $XAUT | $BTC

MAG7: $NVDA | $AMZN | $GOOGL | $META | $MSFT | $TSLA | $AAPL

AI & SPCX: $SNDK | $MU | $AMD | $INTC | $SPCX

9,601

419

1,142

49,971

Jun 9

7

126

285

8,042

Jun 8

Timely analysis from our SoSoValue researcher community.

Fellow researchers, share your investment views for a chance to be featured. 👇

Jun 8

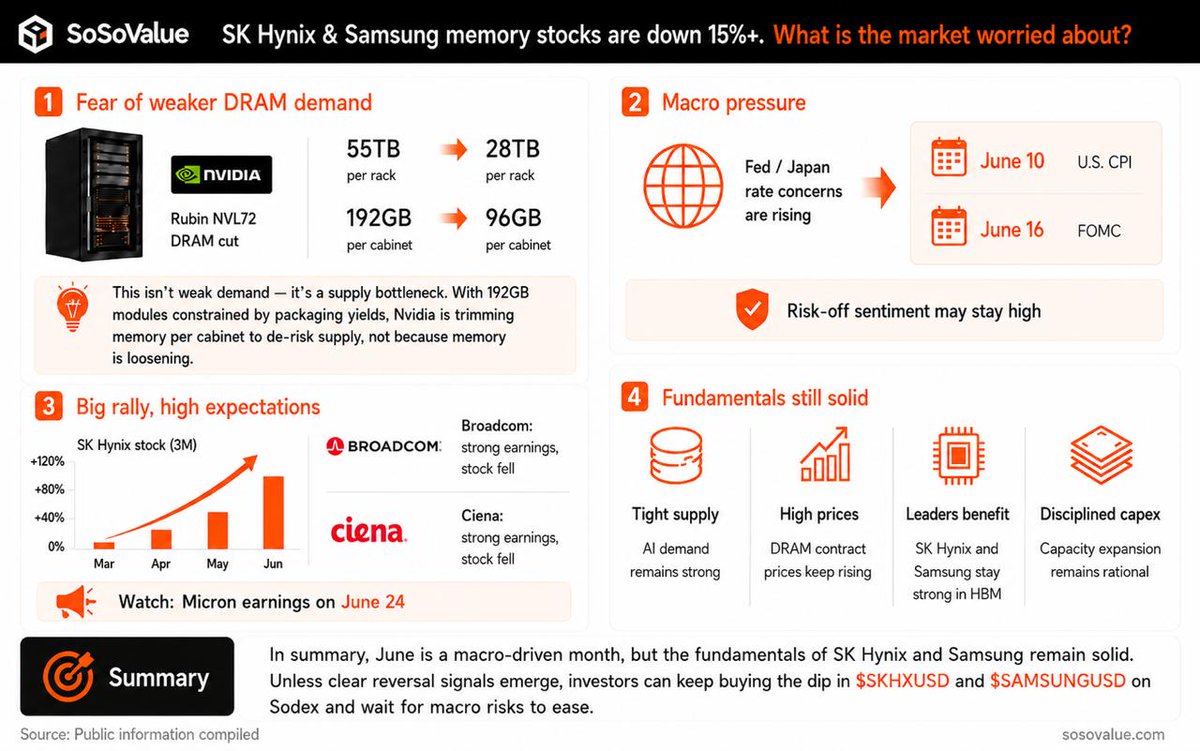

Memory stocks like SK Hynix and Samsung have recently pulled back more than 15%. What is the market worried about?

1. Fear of weaker DRAM demand from customers like Nvidia.

Nvidia's Rubin NVL72 is reportedly set to cut total DRAM capacity per rack from an originally planned 55TB to 28TB, while memory per cabinet may drop from 192GB to 96GB. The market has read this as a sign of weaker memory demand, triggering fears that the expected "volume and price upcycle" in memory may fail to materialize.

But in our view, the market has overreacted. The reason for this adjustment is not weak demand — it's supply bottlenecks.

First, due to tight allocation and extremely low packaging yields, SK Hynix and Samsung cannot supply enough 192GB memory modules to meet demand. To ensure every Rubin GPU has sufficient DRAM, Nvidia is proactively managing supply-chain risk by lowering memory per cabinet.

Second, Nvidia's original reference specification was already very high, and the new architecture is highly flexible. Even with a reduced factory-shipped configuration, end users can still provision additional memory capacity through cloud providers if needed.

So this adjustment does not materially change the reality of tight supply or the growth trajectory of memory demand.

2. Macro pressure: Fed / BoJ rate concerns and a heavy data calendar.

Concerns are rising that the Fed may stay restrictive for longer and that the Bank of Japan may keep hiking. The remarks and policy stance of the new Fed Chair, Kevin Warsh, are worth watching closely.

The upcoming U.S. CPI release on June 10 and the FOMC meeting on June 16–17 could further fuel risk-off sentiment.

3. A big prior rally, high expectations, and a market waiting for fresh catalysts.

Memory stocks delivered a blistering rally in April and May. The market now needs fresh industry-specific catalysts to support further upside. The sharp sell-offs in Broadcom and Ciena after strong earnings reports are a case in point — which makes Micron's earnings on June 24 worth watching closely.

In summary, June is a macro-driven month, but the fundamentals of SK Hynix and Samsung remain solid.

Unless clear reversal signals emerge, investors can keep buying the dip in $SKHXUSD and $SAMSUNGUSD on @sodex_official and wait for macro risks to ease.

sodex.com/join/JELLYZ

#SoDEX #SoSoValue

790

339

975

43,174

Jun 8

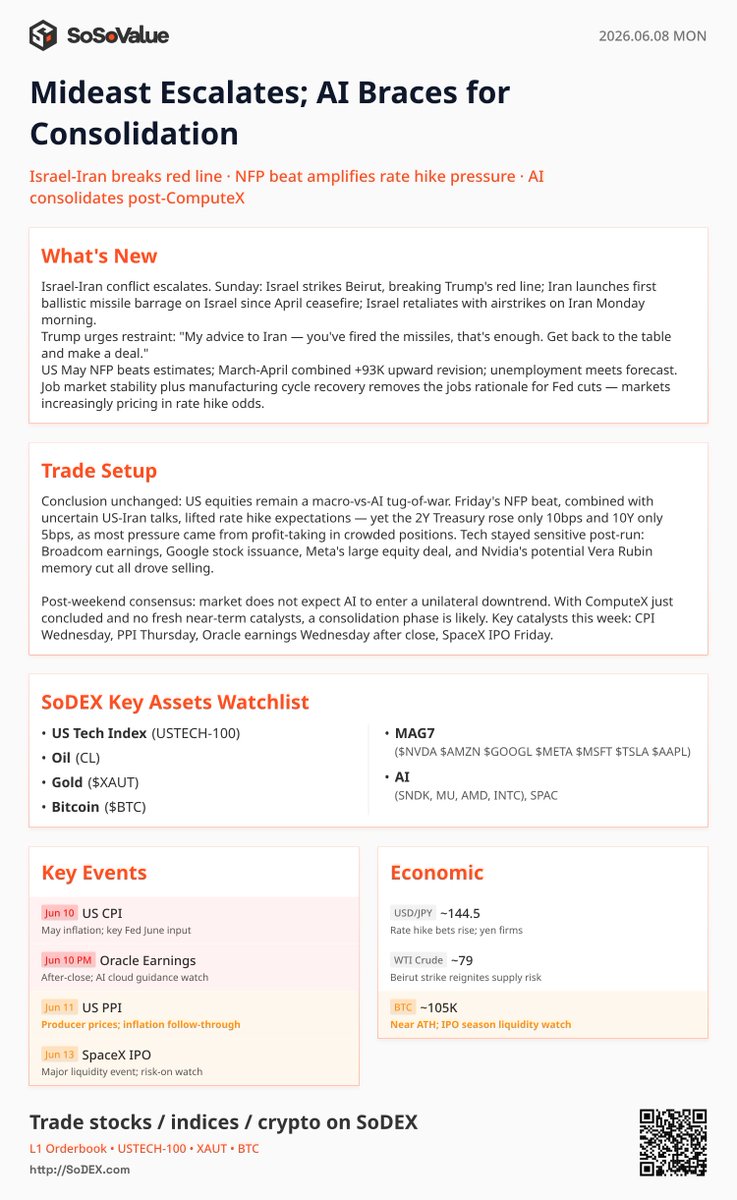

SoSoValue Flash: Geopolitical Escalation Shocks Markets, Strong NFP Elevates Hike Pricing, Tech Crowding Liquidates

💥 Core Catalyst:

Israel's strike on Beirut breached Trump's red line, triggering the most severe exchange of ballistic missiles and retaliatory airstrikes between the U.S. and Iran since the April ceasefire. Trump called for restraint and a return to talks. Concurrently, the massive May NFP beat paired with uncertain negotiation speed lifted market rate-hike expectations.

🔍 Key Logic Shifts:

1️⃣ Macro & Fed: Strong employment data deflated Fed rate-cut justifications, pushing Treasury yields higher and forcing the market to price in hike possibilities. The Fed is expected to hold in June, but a Q4 pivot to tightening remains on the table if oil stays elevated.

2️⃣ Crowded Outflows: Following excessive gains, the tech sector suffered from overcrowded profit-taking. A series of headlines—including softer Broadcom sentiment, Google's completed issuance, Meta's debt plans, and potential memory cuts in NVIDIA's Rubin chips—triggered the selloff.

3️⃣ AI & Volatility: With ComputeX concluded, AI is entering a range-bound consolidation period due to a near-term catalyst vacuum. This week's core volatility drivers include Wednesday's CPI, Thursday's PPI, Oracle's earnings, and Friday's SpaceX IPO.

Trade Setup (SoDEX Assets to Watch):

Core: $USTECH-100 | $CL (Crude) | $XAUT | $BTC

MAG7: $NVDA | $AMZN | $GOOGL | $META | $MSFT | $TSLA | $AAPL

AI & SPAC: $SNDK | $MU | $AMD | $INTC | $SPAC

9,394

412

1,146

50,431

Jun 8

8

130

322

8,737

Jun 6

🚨 Last Call for Wave 2 Builders

Wave 2 of the SoSoValue AI Buildathon is almost closing.

Our 8 Wave 2 Product Reviewers are now ready and excited to dive into your submissions — including 4 returning reviewers from Wave 1 and 4 new reviewers joining this round.

Updated products, new ideas, stronger demos — we’re ready to see them.

Submit before the deadline 👇

app.akindo.io/wave-hacks/JBE…

#SoSoValue #SoDEX #Buildathon #AI #AIAgents #OnChainFinance #Web3 #Builder

19,792

721

2,228

107,859