Co-founder/CEO @Numeral (YC 23), the fastest, easiest way to stay compliant with US sales tax and global VAT. Trusted by 3,000 ecommerce and SaaS businesses.

Joined March 2010

- Tweets 2,465

- Following 976

- Followers 3,211

- Likes 15,003

306 Photos and videos

I’m thrilled to share that @numeral has raised a $35M Series B, led by Mayfield, at a $350M valuation!

Turns out, sales tax and VAT have gotten so complex that we need AI and millions of dollars in VC funding to make it simple again.

This brings us to $57M in funding, including our $18 million Series A led by Benchmark Capital in March of this year.

We are 1,057 days into building Numeral, and I’m humbled to say that we’ve processed over $5 billion in transaction volume, filed 150,000 sales tax returns for 2,000 paying customers, and achieved 3.5x year-over-year revenue growth.

Numeral is the end-to-end platform for sales tax and VAT compliance.

I couldn't be prouder of what we’ve accomplished… but there's still a lot left to build, many new customers to serve, and a heck of a lot more sales tax filings to, well, file.

So what’s next?

Global coverage: Growing internationally? Our in-house platform currently covers 60 countries, and we are expanding to many more by the end of the year.

Integrations: As you may have noticed, we’ve launched several new integrations over the last few months, including with Orb, Sequence, Tabs, and others. Some exciting integrations to come!

Automation: Could Numeral be the most boring AI company? Our AI may not be the flashiest, but our automations mean you'll never have to log into a government portal or listen to hold music again.

Our team: We are currently hiring for multiple roles across our organization. Ready to join us?

Matt and I are incredibly grateful to our customers and team. Thank you for making this milestone possible.

And a special thank you to our wonderful investors: @MayfieldFund, @SPangulur, @benchmark, @chetanp, @ycombinator, @gustaf, @uncorkcap, @susanwliu, @FundersClub, @mittal, @mantisVC, @AlexPallNY, @ShaanVP, @lennysan, @moizali, @mrsharma, @ringmybeller, @khency6, @asturnerr, @maariabajwa, and so many others.

64

47

546

638,581

This is funny. And also the clearest explanation of tax infrastructure I've ever seen.

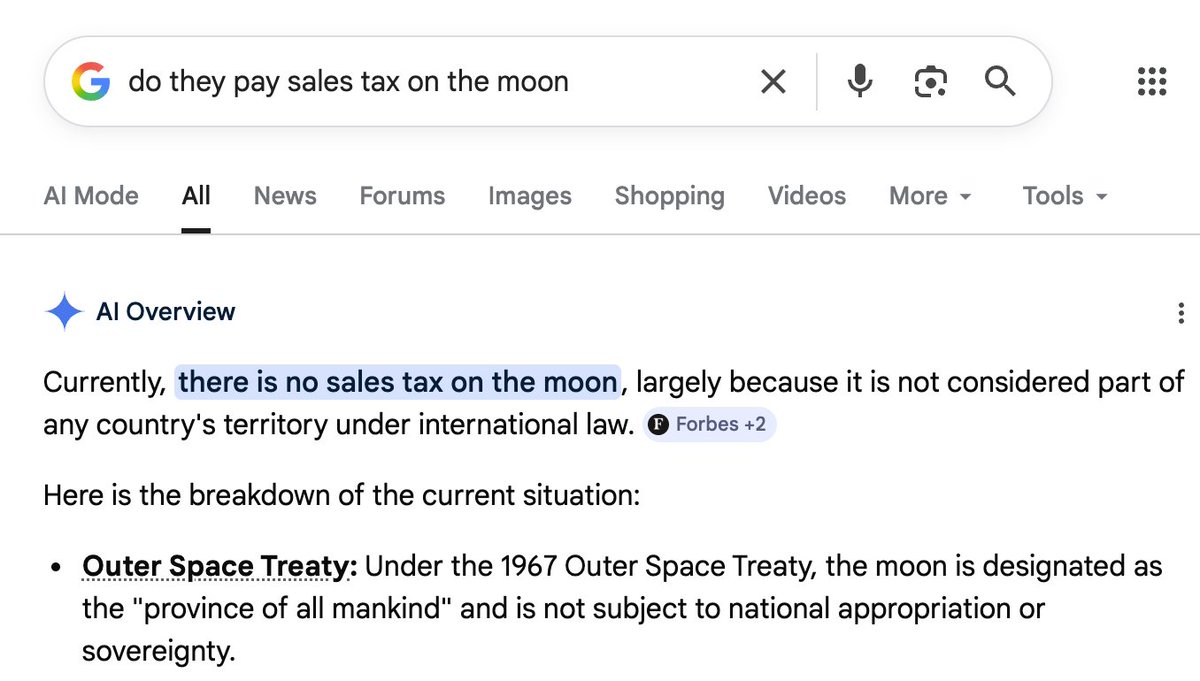

Japan's PM won an election promising to cut food sales tax to 0%.

In a cost of living crisis, cutting food tax looked like an easy political win.

Then she tried to implement it.

Point-of-sale systems at major retail chains were never built to process a 0% rate. A full overhaul takes up to a year. The PM called it "an embarrassment for Japan" in parliament. The press gave it a name: reji-kabe, register wall.

The OECD flagged the plan as too costly. Fiscal hawks raised alarms about Japan's 230% debt-to-GDP ratio. Political opponents pushed back.

None of it changed the policy.

A cash register did.

Because… get this, 1% is what the software can handle :)

83

was walking through a park in sf and saw a guy pushing a high-end uppababy stroller.

i peeked inside expecting to see a newborn.

no baby.

four NVIDIA H100s buckled into the stroller, getting some fresh air.

i nodded at the dad.

he nodded back.

“keeping them cool,” he whispered.

“nature is healing,” i replied.

i love this city.

2

11

811

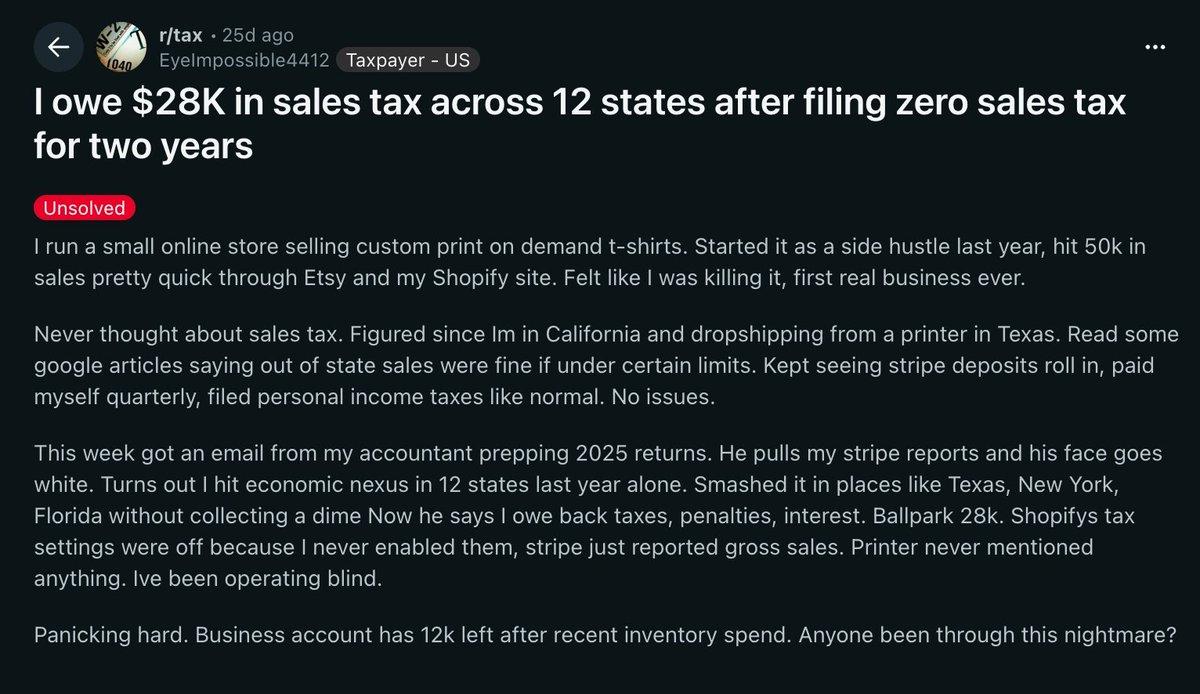

Saw this on Reddit this week. $28k in back taxes across 12 states. Business account has $12k left.

This person was selling custom t-shirts, doing well, paying himself, and had no idea he may have created sales tax exposure across multiple states.

His accountant only caught it while prepping 2025 returns.

By then: back taxes, penalties, interest. $28k across states he’d barely thought about.

Now, the comments pointed out a few important wrinkles.

Maybe the Etsy sales should have been carved out because marketplace facilitators usually collect and remit. Maybe the Texas printer created physical nexus. Maybe the accountant counted some thresholds wrong.

But that’s the thing about sales tax.

One question turns into MANY:

Which sales channel? Which state? Which threshold? Revenue or transactions? Marketplace or direct? Economic nexus or physical nexus? When did the obligation start?

You keep depositing checks until someone runs the numbers and tells you the answer is less obvious than you thought.

The Wayfair ruling in 2018 meant crossing certain revenue or order thresholds in a state can create an obligation, even if you’ve never been there, never had a warehouse there, and never thought about it.

A lot of founders find out the same way this guy did. Too late.

If you're doing decent volume online and haven't checked your nexus exposure, that's worth 10 minutes of your time today.

And if you’d rather get someone else look at it, check out @Numeral.

3

1

7

1,436

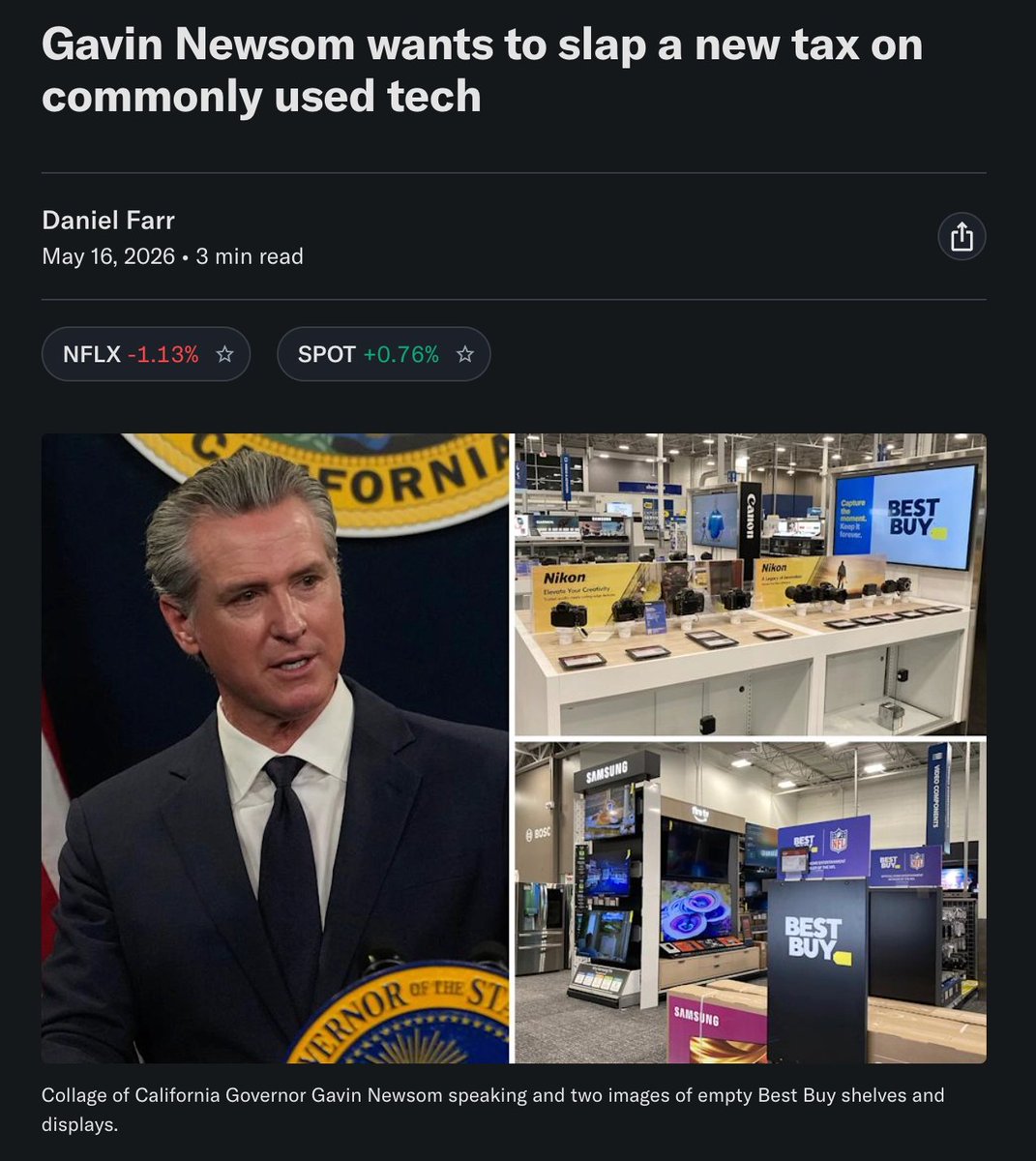

California might tax SaaS.

Governor Newsom's proposal would expand state sales tax to cloud software, SaaS, and some AI platforms. Base rate is 7.25%, higher with local add-ons, projected to generate $1.1 billion in year one and roughly $2 billion annually.

California's been one of the big exceptions for SaaS - software companies could often sell into the state without the same treatment as physical products. That may change.

The more interesting point is the direction of travel. Sales tax started with physical goods, then caught ecommerce after Wayfair in 2018, then marketplaces became collectors, now it's reaching software and cloud tools. The tax code lags the business model, then catches up all at once.

A lot of DTC brands kept operating under old assumptions after Wayfair until sales tax showed up in audits, fundraises, or acquisitions. At @Numeral, we watched that happen to founder after founder.

SaaS and AI may be entering that same moment.

The proposal still needs to pass the legislature. But when one of the biggest SaaS markets in the country moves this direction, it's worth paying attention.

Sales tax feels boring until it becomes a diligence issue.

2

4

526

Always proud to see the Numeral team combining remote and in-person work outside

Jun 1

omg this team brought their remote coworker to lunch with a hardware device LOL

then they said BYE

only in sf lol

2

11

2,038

Two great teams coming together. Excited to see what they build. Keypo is lucky to have @dblumenfeld!

Jun 1

Keypo is joining Multifactor!

I’ve been working on cryptography products at the intersection of AI Agents since 2024. It’s a problem very few are working on but is the biggest roadblock to agents reaching critical mass. Put it this way: your parents aren’t gonna trust AI with their bank account without knowing there is ZERO ways it can do something malicious.

Then one day, I’m watching @tbpn and I hear “Multifactor is building a password manager for AI agents.”

Fast forward to meeting @viveknair_1, and I was blown away by his background in cybersecurity. An ex-CIA agent, author of 10 patents in cryptography and most importantly: equally obsessed with building agent security solutions.

I’m extremely excited to work with Vivek and the very talented Multifactor team as founding engineer. Together, we will build novel cryptography products that make zero- trust account sharing with agents possible.

6

566

I run a tax compliance company. The Germany e-invoicing rollout is a masterclass in how operators get caught by a rule they weren’t tracking.

From 2025, domestic B2B e-invoicing became the standard. But the rollout was phased - some businesses still had transition time before they had to send the new structured invoice format.

Receiving was a different story.

Even if you didn’t have to send structured e-invoices yet, your systems still had to be ready to receive them.

Which created a strange gap: your own invoicing process could still look familiar, while your AP workflow, ERP, and archiving all needed to handle a new format coming in.

There’s one important caveat: foreign businesses without a German fixed establishment are outside the domestic e-invoicing scope.

But for businesses in scope, a lot of teams were watching the outbound deadline. The inbound one snuck up on them.

The broader point for operators: when a government changes a document standard, the compliance date on paper rarely captures the actual scope of work.

By the time your legal deadline arrives, you’ve already got an ops project on your hands.

80

The billing mistake that turns 30% of a Texas deal into 100% taxable.

Texas has a rule most founders never see coming. If you bundle taxable and non-taxable services on a single lump-sum invoice, and the taxable portion exceeds 5% of the total, the state presumes the entire charge is taxable.

Picture a $10,000 deal: $3,000 in taxable services bundled with $7,000 in non-taxable work, written as one line item. Texas can treat all $10,000 as taxable. At a combined state and local rate up to 8.25%, that's hundreds of dollars in liability on revenue that was never supposed to be in the tax base.

A few things worth knowing:

1. It's a presumption. You can rebut it with documentation showing the actual breakdown, but that's an audit-time fight you don't want to have. Clean invoices prevent it entirely.

2. Service type matters. This applies to Texas's enumerated taxable services: data processing, information services, and similar categories. If your work doesn't touch these, the rule may not apply the same way.

3. If you do data processing work, Texas already carves out 20% as non-taxable by statute. That exemption only works if your invoice line items are separated.

The fix is the same in every case: break out your line items. Taxable services on one line, non-taxable on the next, expenses called out separately.

Nothing about the actual work changes. Just the quote template.

Pull up your last few Texas invoices and check how they're structured.

1

147

In Australian GST, everyone assumes the merchant carries the liability. BUT sometimes it ends up with the company that just moved the box.

Say an Australian customer buys low-value goods from an overseas merchant. The merchant doesn’t ship directly - a redeliverer steps in, forwarding the package into Australia.

If the merchant or marketplace has already handled GST, that’s the end of it.

But when neither has, the obligation can move downstream to the redeliverer.

Not the merchant or the marketplace. The forwarding company.

The part that catches operators off guard is where the liability can end up. You’d expect it to sit with whoever sold the goods. But if the seller/platform isn’t the one handling GST, the obligation can follow the fulfillment flow.

Worth keeping in mind as more ecommerce brands experiment with fulfillment setups, forwarding flows, and cross-border logistics.

1

2

125

Nothing has made software feel more alive than watching people develop loyalty, resentment, and emotional dependency toward specific models.

People talk about Claude and ChatGPT the way previous generations talked about coworkers.

“This used to be really good.”

“It’s still useful, but I need to phrase things carefully.”

“I don’t trust it with anything high stakes.”

“It was incredible last month. No idea what happened.”

6

287

Fishwife got named one of Time’s Most Influential Food and Drink Companies of 2026.

Very deserved.

They took tinned fish and made it feel like something you’d bring to a dinner party.

Beautiful tins, great flavors, a cookbook, the whole thing.

The funny thing with good brands is that once they work, the idea feels obvious.

Of course tinned fish could be premium.

Of course it could be giftable.

Of course it could sit next to wine and nice bread and not feel like emergency food.

But someone had to actually make it feel that way.

Very cool to see.

Proud they’re a Numeral customer.

Also the cookbook is great.

1

21

2,846

I’ve been using miso.com for months - it’s amazing and I can’t imagine not having it

Frontier models like @OpenAI publicly avoided booking travel for a reason.

I founded miso.com - $2,000,000 booked. 200 founders, athletes, and creators. 1 thread in iMessage.

All in beta.

Here’s what’s different:

• We actually know you, from avoiding flights at 8 AM to finding Starlink flights, down to what breed your service dog is. We weigh out the options between points and cash, making sure every loyalty, credit, and reward is working for you.

• 24/7 support. No random fees, no charges for changes. We're the first to integrate legacy infrastructure with LLMs to deliver concierge-grade service at scale. Modify, rebook, or cancel at any time.

• We literally give you back money for hotels, referrals, and every milestone you hit.

Search is the wrong abstraction. We built a tool to just do it for you.

We're now opening it up to the public.

join.miso.com

1

16

15,824