In-depth research on quality public companies 📖 Free content on Substack 🎧 Podcast: The Synopsis 👇 All Linked below 🔸— @DrewCohenMoney & @kevg1412

Joined September 2022

- Tweets 6,014

- Following 263

- Followers 11,987

- Likes 6,622

1,867 Photos and videos

Pinned Tweet

1 Feb 2023

Starting at GS research and migrating to the buy-side was a first hand experience in how lacking 3rd party research is.

Speedwell just released a short piece on how we differ.

speedwellsnippets.substack.c…

2

11

76

78,537

Speedwell Research retweeted

$MU and homebuilders are more similar than you might think.

Everything about a home builder is basically a commodity product.

It is often taught that commodity products cannot maintain high returns, but if you look at the ROE of many home builders you’ll see many in the 20% range. Sometimes much, much higher.

These businesses have a product that anyone can produce, but the reason why their economics are maintained is because demand outstrips supply.

There is more demand for (moderately/ low priced) homes than we create. Thus virtually every home that gets built gets sold—and at a price that provides ample margin for the builder.

When these businesses do poorly is when demand temporary sags and the carrying cost of inventory (construction loan interest expense) weighs on returns. Aggressive financing on the builders parts, could result in bankruptcy in such situations.

Generally though, demand for homes is only going to go up overtime and will continue to outstrip the pace of building—at least in the U.S.

The situation is different in China for instance where supply increases has resulted in very soft home prices and phantom cities.

The point I wish to make is that competitive moats are only pertinent to a business when supply outstrips demand.

If you can differentiate your product sufficiently, the consumer preferences you are fulfilling are unique enough that the business itself is the sole supplier.

They have escaped the rat race of commodity competition where any business can build what they build. If you want an iPhone, there is only one seller. If you want fast delivery on millions of items through a high trust seller, there is only Amazon (in the U.S.)

The less emphasized point though is that even if your product is undifferentiated, so long as supply runs below demand, you can have a strong business.

We are seeing this phenomenon in memory chips, energy supply, and data centers. The demand is overwhelming and so many business that fit the bill of being a commodity product can reap stellar margins and returns on capital—for now.

Micron posted 68% operating margins. 3 years ago they were as low as -63%.

With capacity constraints and capital flooding into the data center build out, they certainly have strong tailwinds to continue to post such stellar margins.

However, the problem with such businesses comes from the fact that these high returns draw in incremental capital and eventually growth in supply will overshoot demand.

While a cycle can take years, it doesn’t change the fact that memory is not a differentiated product the same way a Nvidia GPU chip or Arista network switch is. (That doesn’t mean they can’t also have their own cyclically though—just that by and large the market for Nvidia GPUs, is different than the market for “GPUs”)

Investing in such businesses becomes a bet on the capital cycle duration and a bet on the rationality of multiple players. It works so long as demand is higher than supply, but when the situation reverses, the commodity-like returns of an undifferentiated product returns. (Memory investors are basically betting that AI demand has resulted in a paradigm shift where demand will continue to outpace supply for many years—perhaps a decade… but Wall Street only tends to model 3-5 years out).

Building constraints in the U.S. has prevented economic deterioration in the home building industry. (Even in a weak year like 2021 a small home builder— Dream Finders Homes had a 12% ROIC, higher than most businesses). The time it takes to build new fabs has prevented this from immediately correcting in the memory industry, but it is inherently a more precarious competitive position to be in because the businesses do not control their destiny. Apple can control the production of iPhones, but Micron cannot control the supply of HBM.

This is not to say this is a “wrong” way to invest—there are many ways to make money. But just that the timing of such investments are much more critical than say investing in a Red Bull or Monster. The customers of those business’s only want a “Red Bull” and alternatives (by and large) will not do. Thus the vectors of competition move from trying to create a better Red Bull rather than simply supplying an energy drink.

The history of businesses that do not have moats is brutal. Capitalism will eventually compete down those returns. But that doesn’t mean an investor can’t make money if they time the capital cycle right—they should just be aware that is the bet they are making.

5

2

16

1,255

Speedwell Research retweeted

Should I do an Adobe update video?

71%

Yes

13%

No

16%

I'm Scared

31 votes • 20 hours

12

1

11

2,355

Jun 12

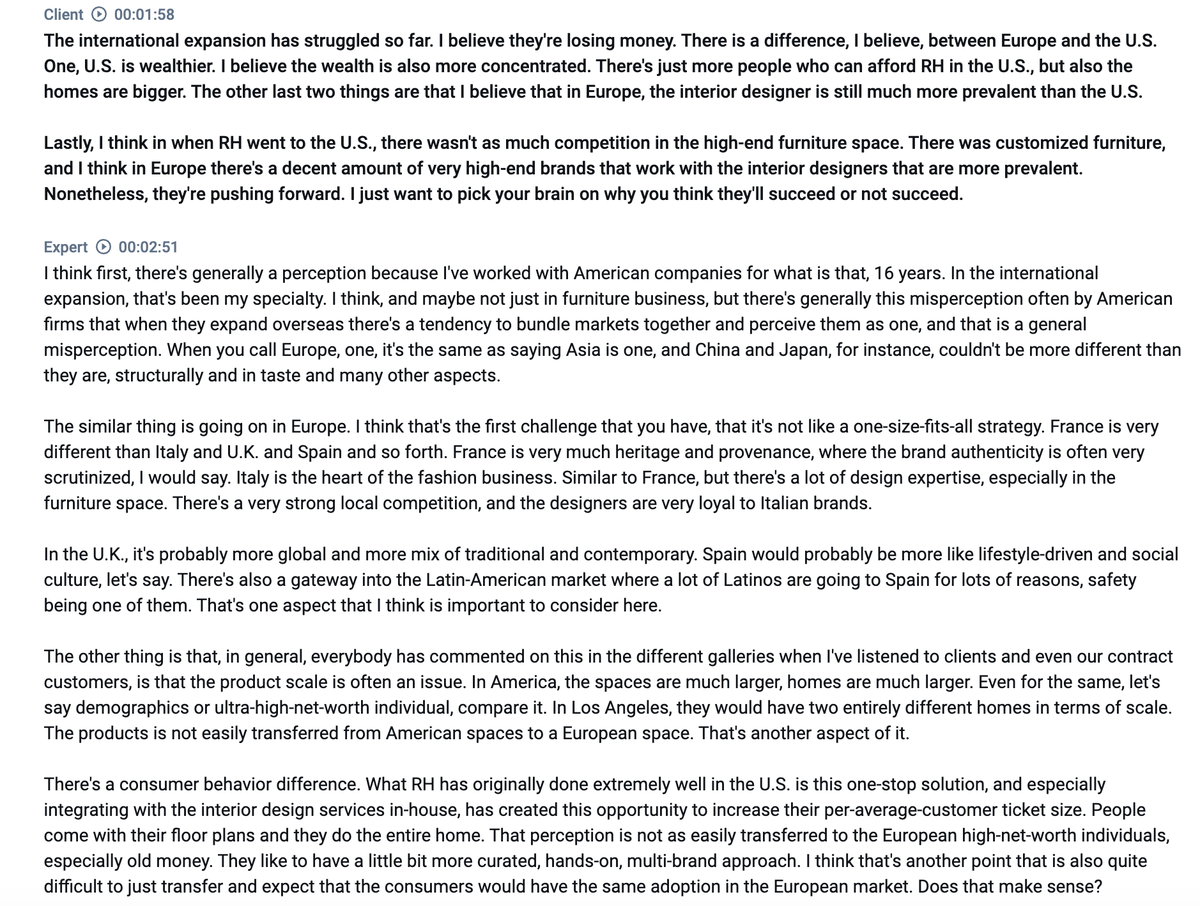

Former senior financial analyst at $FND on mom and pop competition

"At the end of the day, the biggest competitor that Floor & Decor or any of the major companies see in the flooring space are your local mom-and-pop stores because of the loyalty that they have from their customers.

Our big focus at the time, and I am sure it still is, they did not have a desire to put mom-and-pop stores out of business...

They looked for opportunities to partner with mom-and-pop stores, and there were times where we would even just become the supplier for those stores in certain products that were hard to find."

@AlphaSenseInc

1

17

2,522

Speedwell Research retweeted

Jun 12

One of the best cover up out there! @DrewCohenMoney

2

2

10

2,247

Speedwell Research retweeted

Jun 11

$ADBE ARR growth inflected to 12.5% from 10.9%, but they continue to expect total year ARR at 10.2%

The CFO also announced a departure.

Not a great look with both CEO and CFO slots now open.

18

5

125

19,391

Jun 11

Former creative director at $ADBE on their focus on workflow over having the "best" model

"They're focused now more on integrating the workflow and the full experience than trying to focus on having the best Midjourney competitor.

Their strength is really on the workflow."

@AlphaSenseInc

1

10

2,427

Speedwell Research retweeted

Jun 10

Just dropped a new Dialogue

We talk about:

- chip stocks

- AI

- capital cycles

- what’s different from ‘99

Jun 10

🎙️ New Dialogue Podcast Released!

In this dialogue, we discuss:

🔹 Are we in an AI bubble or not?

🔹 How reflexivity affects outcomes

🔹 What you can do as an investor

Listen below 👇

1

3

11

4,518

Jun 10

Jun 10

I think $YELP is a one of the greatest lost opportunities in consumer internet.

The app has been underinvested in (search is broken), their advertising has always been ineffective, and they missed multiple move into adjacencies before competitors (OpenTable, DoorDash, Angi, Mindbody, and other SMB services). They were early enough to have a real shot of becoming a SuperApp like Meituan, instead they floundered for years not changing much and bleeding capital.

Today though, it still represents a strategic asset that I cannot fathom why no one has tried to acquire

$ABNB could use Yelp to buttress their Services business giving them instant access to hundred of millions of reviews, >60mn MAUs, and tens of millions of business profiles.

It also solves Airbnb's key issue: frequency. People DO NOT open the Airbnb app often enough for it to be a strong foundation to cross-sell services. Looking up restauraunts/ local businesses is a high frequency activity for tens of millions of users. And if they improve the app, I venture to say they could easily increase that as their strong suit is UI. This is exactly what they would need in order to spin-up the services business.

OpenAI or xAI could absorb them to improve their local search results to compete against Google Reviews and they would also get a new customer touch point. The access to their ~10mn businesses is also PERFECT for a business that needs to build advertiser density in order to grow their ads business.

Meta could do the same to improve search results in their apps and have a new "business profile" page that is more comprehensive to a FB account (although more likely to be blocked).

At a 50% premium, that is a CAC of only $33 a user and you get access to ~10mn businesses, hundreds of millions of reviews, and other meta data.

Why not bet ~$2 bil on acquiring Yelp?

6

5,330

Jun 10

🎙️ New Dialogue Podcast Released!

In this dialogue, we discuss:

🔹 Are we in an AI bubble or not?

🔹 How reflexivity affects outcomes

🔹 What you can do as an investor

Listen below 👇

2

4

6,267

Jun 10

Former creative director at $ADBE on how gen AI is expanding Adobe's ecosystem and retaining enterprise clients

@AlphaSenseInc

2

2

17

2,517

Speedwell Research retweeted

Jun 9

Most people miss that there is a speculative element in buying a cheap stock

"If you're buying a mediocre business just because it's cheap, time is against you because you need it to very quickly realize to its market value in order for you to sell it and make your return.

Otherwise, if you're stuck in it, you're stuck in a business that's investing at a low ROIC, and so the longer it takes in order to realize that return, the worse your investment is going to be."

May 26

🎙️ New Dialogue Podcast Released!

In this dialogue, we discuss:

🔹 S&P 500 valuation concerns

🔹 Thoughts on $CSU and $INTU earnings

🔹 Update on $SE and $MELI

Listen below 👇

5

3

37

6,959

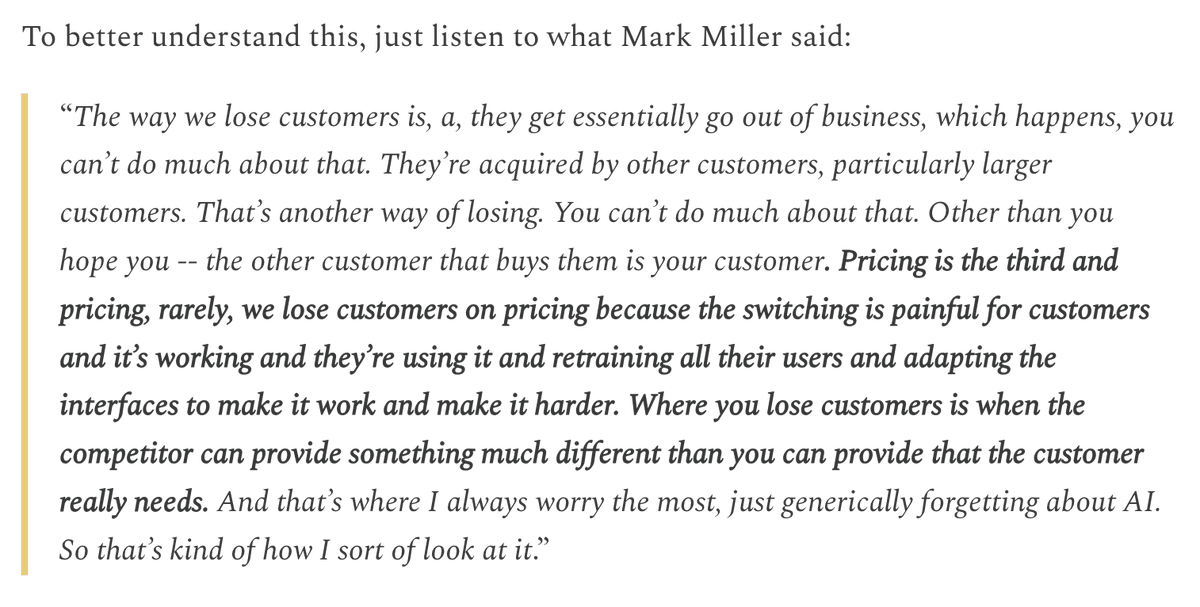

Former senior financial analyst at $FND on market share gains from new vs existing stores

"They were gaining market share but almost at a quicker pace on their existing stores because the new stores that were beginning to open, they were starting to get into areas that were less familiar with Floor & Decor.

Newer stores were having slightly slower openings, whereas existing stores were growing both sales and market share at a greater pace for a period of time."

@AlphaSenseInc

1

12

2,314

Speedwell Research retweeted

Jun 8

4

4

20

4,658

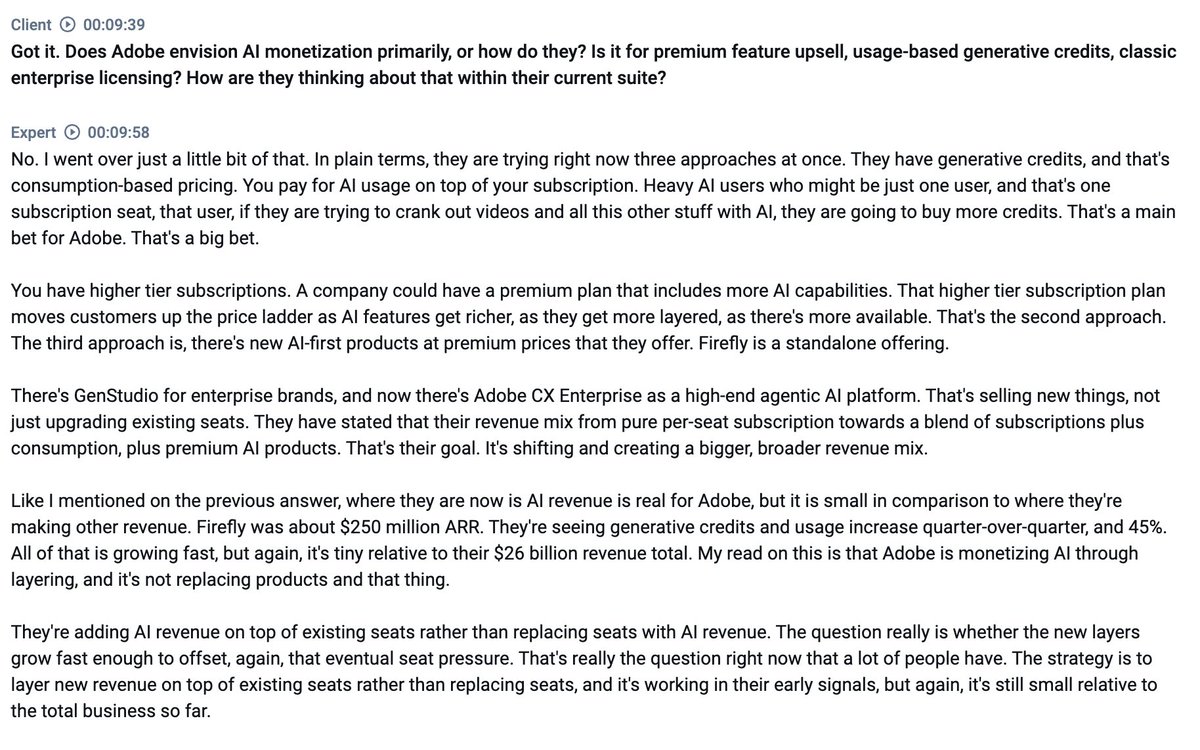

Former creative director at $ADBE on AI pricing

"They're adding AI revenue on top of existing seats rather than replacing seats with AI revenue.

The question really is whether the new layers grow fast enough to offset that eventual seat pressure.

That's really the question right now that a lot of people have.

The strategy is to layer new revenue on top of existing seats rather than replacing seats, and it's working in their early signals, but again, it's still small relative to the total business so far.

@AlphaSenseInc

2

1

20

3,516

Speed of development, in and off itself, isn’t beneficial to the customer.

This is part of the reason why software companies are somewhat insulated from the growing ease of creating software.

AI does mean creating software is easier, which is a benefit to the software company creator, and they may be able to reduce their costs as a result.

However, passing off a portion of this cost savings to customers with a price decrease is not that value additive to customers.

This means not only that it is hard to win new business just based off of price, but also that it is not that simple creating new products with AI to upsell customers, there needs to be a real value add.

$CSU

2

1

18

2,689

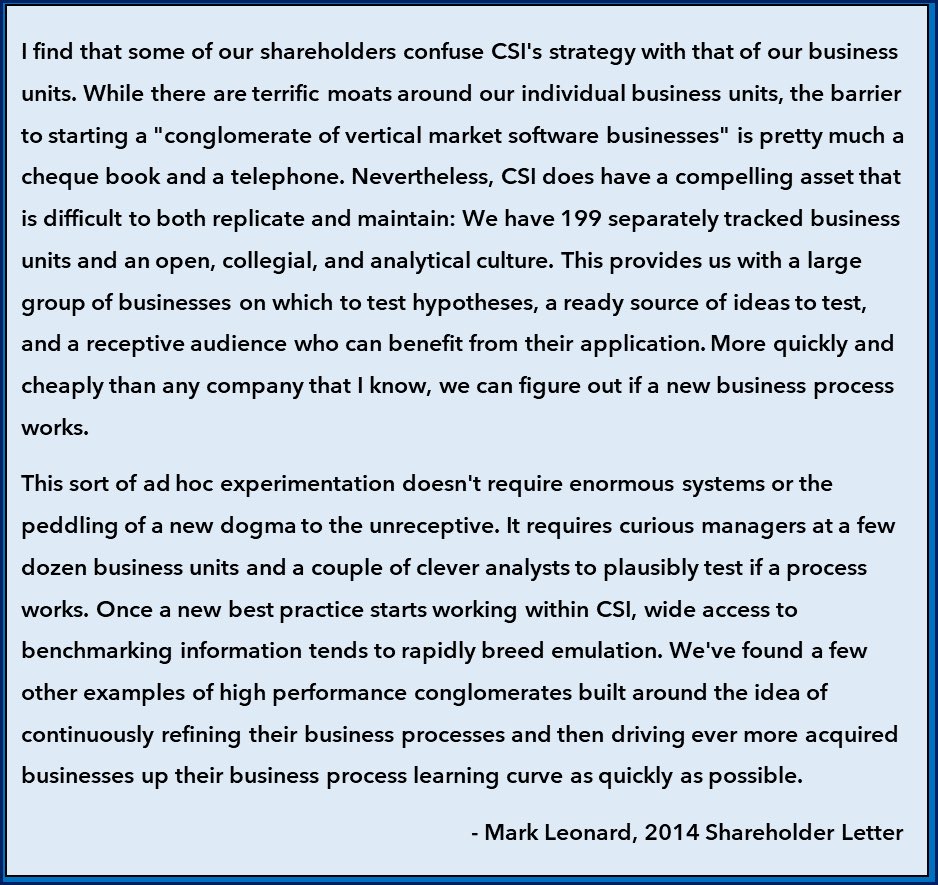

There is our businesses’ moats and then there is our moat—most investors confuse the two.

In 2014 Mark Leonard clarifies Constellation’s competitive advantage.

$CSU

15

2,402

It's always about the capital cycle.

Jun 5

AI stocks are down a lot today

$NBIS -14%

$MU -11%

$SNDK -10%

$AMD -10%

$ORCL -10%

$INTC -9%

$NVDA -5%

But what if we are still far from AI being in a bubble?

The capital flows into the semiconductor sector and AI beneficiaries doesn’t seem likely to slow for several years.

Unlike during the tech bubble where 95% of Fiber was dark (never used), virtually every GPU made is being utilized.

And there are still several capacity constraints that prevent a full supply side expansion—which is typically the precondition to a bubble forming.

Read this weeks Five Minute Money for the 5 arguments for and against us bring in an AI Bubble.

1

7

3,258

Speedwell Research retweeted

Jun 5

AI stocks are down a lot today

$NBIS -14%

$MU -11%

$SNDK -10%

$AMD -10%

$ORCL -10%

$INTC -9%

$NVDA -5%

But what if we are still far from AI being in a bubble?

The capital flows into the semiconductor sector and AI beneficiaries doesn’t seem likely to slow for several years.

Unlike during the tech bubble where 95% of Fiber was dark (never used), virtually every GPU made is being utilized.

And there are still several capacity constraints that prevent a full supply side expansion—which is typically the precondition to a bubble forming.

Read this weeks Five Minute Money for the 5 arguments for and against us bring in an AI Bubble.

7

4

79

20,142