Published 500,000 words on how to analyze, value, and manage your stock portfolio at stablebread.com. Follow for write-ups, models, and guides!

Joined August 2020

- Tweets 3,428

- Following 308

- Followers 2,263

- Likes 2,105

552 Photos and videos

Pinned Tweet

May 29

I've published 500,000 words on how to analyze, value, and manage stocks.

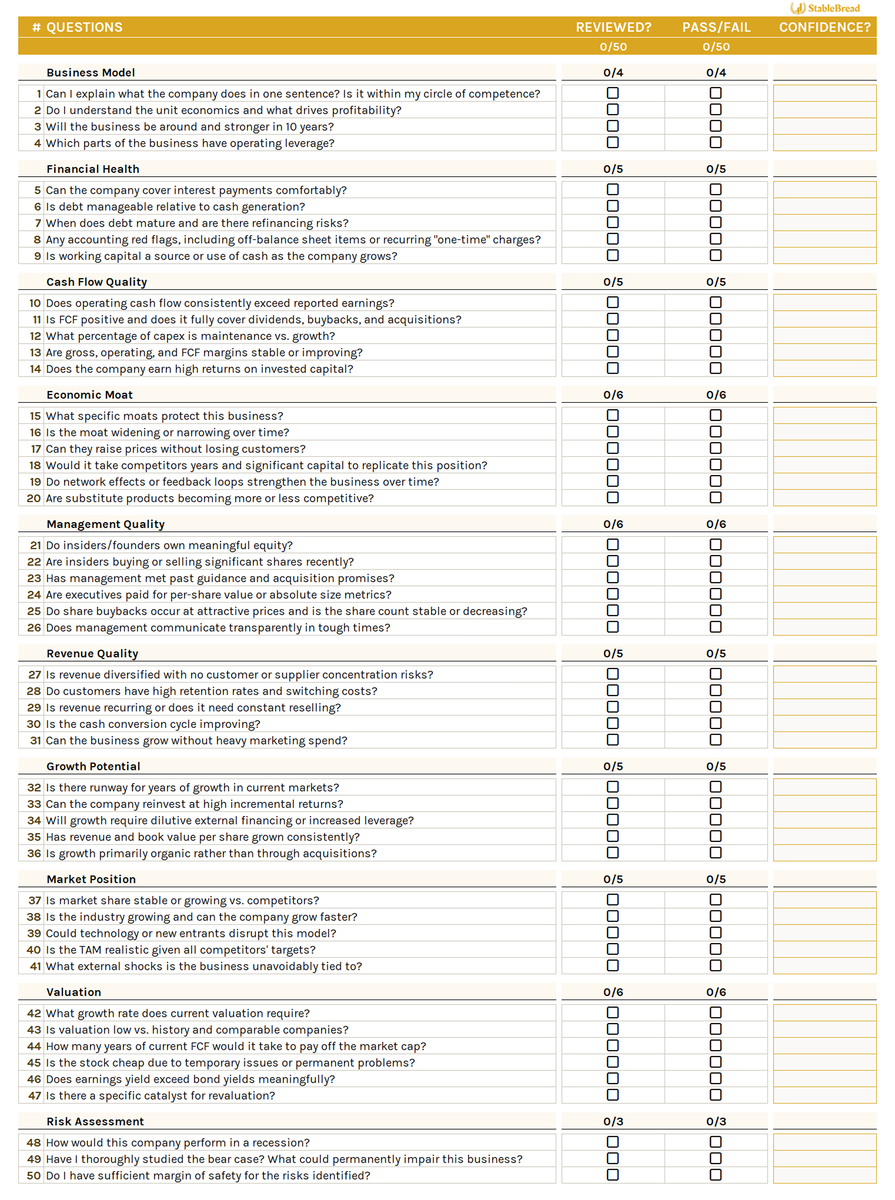

Here's the 50-question checklist I run through when evaluating a business (free Excel version included): ↓

1️⃣ Business Model

1. Can I explain what the company does in one sentence? Is it within my circle of competence?

2. Do I understand the unit economics and what drives profitability?

3. Will the business be around and stronger in 10 years?

4. Which parts of the business have operating leverage?

2️⃣ Financial Health

5. Can the company cover interest payments comfortably?

6. Is debt manageable relative to cash generation?

7. When does debt mature and are there refinancing risks?

8. Any accounting red flags, including off-balance sheet items or recurring "one-time" charges?

9. Is working capital a source or use of cash as the company grows?

3️⃣ Cash Flow Quality

10. Does operating cash flow consistently exceed reported earnings?

11. Is FCF positive and does it fully cover dividends, buybacks, and acquisitions?

12. What percentage of capex is maintenance vs. growth?

13. Are gross, operating, and FCF margins stable or improving?

14. Does the company earn high returns on invested capital?

4️⃣ Economic Moat

15. What specific moats protect this business?

16. Is the moat widening or narrowing over time?

17. Can they raise prices without losing customers?

18. Would it take competitors years and significant capital to replicate this position?

19. Do network effects or feedback loops strengthen the business over time?

20. Are substitute products becoming more or less competitive?

5️⃣ Management Quality

21. Do insiders/founders own meaningful equity?

22. Are insiders buying or selling significant shares recently?

23. Has management met past guidance and acquisition promises?

24. Are executives paid for per-share value or absolute size metrics?

25. Do share buybacks occur at attractive prices and is the share count stable or decreasing?

26. Does management communicate transparently in tough times?

6️⃣ Revenue Quality

27. Is revenue diversified with no customer or supplier concentration risks?

28. Do customers have high retention rates and switching costs?

29. Is revenue recurring or does it need constant reselling?

30. Is the cash conversion cycle improving?

31. Can the business grow without heavy marketing spend?

7️⃣ Growth Potential

32. Is there runway for years of growth in current markets?

33. Can the company reinvest at high incremental returns?

34. Will growth require dilutive external financing or increased leverage?

35. Has revenue and book value per share grown consistently?

36. Is growth primarily organic rather than through acquisitions?

8️⃣ Market Position

37. Is market share stable or growing vs. competitors?

38. Is the industry growing and can the company grow faster?

39. Could technology or new entrants disrupt this model?

40. Is the TAM realistic given all competitors' targets?

41. What external shocks is the business unavoidably tied to?

9️⃣ Valuation

42. What growth rate does current valuation require?

43. Is valuation low vs. history and comparable companies?

44. How many years of current FCF would it take to pay off the market cap?

45. Is the stock cheap due to temporary issues or permanent problems?

46. Does earnings yield exceed bond yields meaningfully?

47. Is there a specific catalyst for revaluation?

🔟 Risk Assessment

48. How would this company perform in a recession?

49. Have I thoroughly studied the bear case? What could permanently impair this business?

50. Do I have sufficient margin of safety for the risks identified?

2

9

2,839

Jun 13

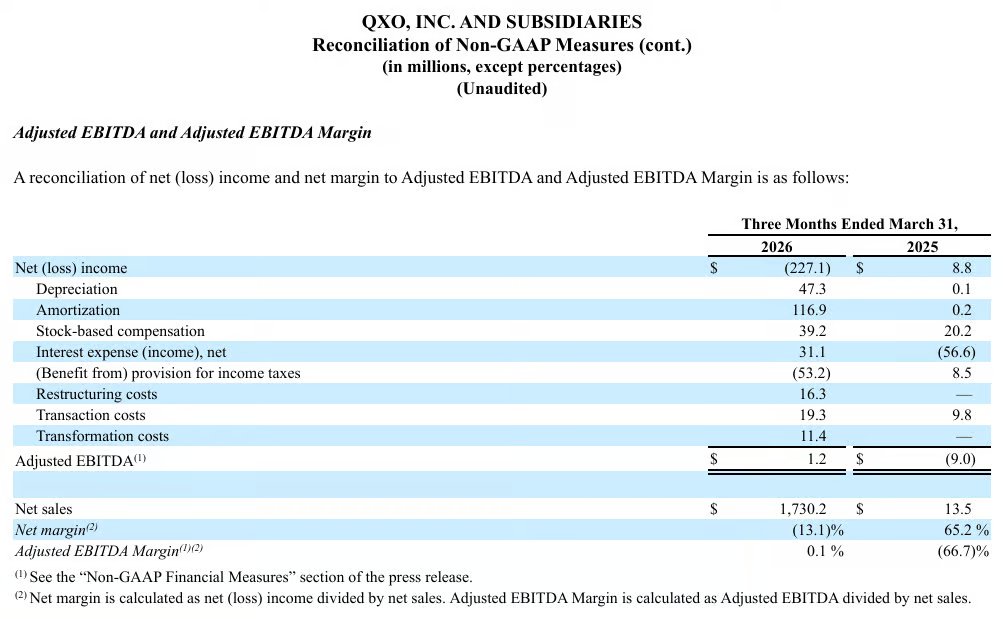

$QXO lost $227M last quarter. Strip out the deal accounting and the real business is near break even.

Q1 2026:

→ Net sales: $1,730.2M

→ Gross profit: $409.3M (23.7% margin)

→ Net loss: $(227.1)M

→ Adjusted EBITDA: $1.2M

→ Loss per share: $(0.35)

The gap between the $227M GAAP loss and near-zero EBITDA is the whole story of an early-stage roll-up.

Most of it's amortization ($116.9M, mostly acquired intangibles), plus depreciation, stock comp, interest, and one-time deal costs. Non-cash or deal-related.

What's left is a core roofing business that's barely EBITDA-positive right now, because integration spending and a soft housing market are landing at the same time. And Kodiak and TopBuild aren't in the numbers yet.

One real signal underneath: gross margin has climbed every quarter since the Beacon close, 21.1% --> 23.3% --> 24.2% --> 23.7%. Some is accounting noise, but on $8.6B of revenue each point is ~$86M.

Don't grade QXO on this income statement. Grade it once Kodiak and TopBuild hit the P&L.

3

5

492

Jun 12

$BCAR is trading even closer to its trust value floor since my writeup on May 8th.

Next best opp to $BRUN (prev $WLAC) pre-merger if you understand the mechanics and have the risk appetite: newsletter.stablebread.com/p…

Jun 12

We're growing fast:

5.3x revenue in FY2025 vs FY2024 (~$7M)

22 enterprise customers across 12 countries

92% retention

95.5% GPU utilization

Recurring GPU-as-a-Service revenue today massive upside from infrastructure solutions. $300M qualified pipeline. Momentum is real.

4

937

Jun 12

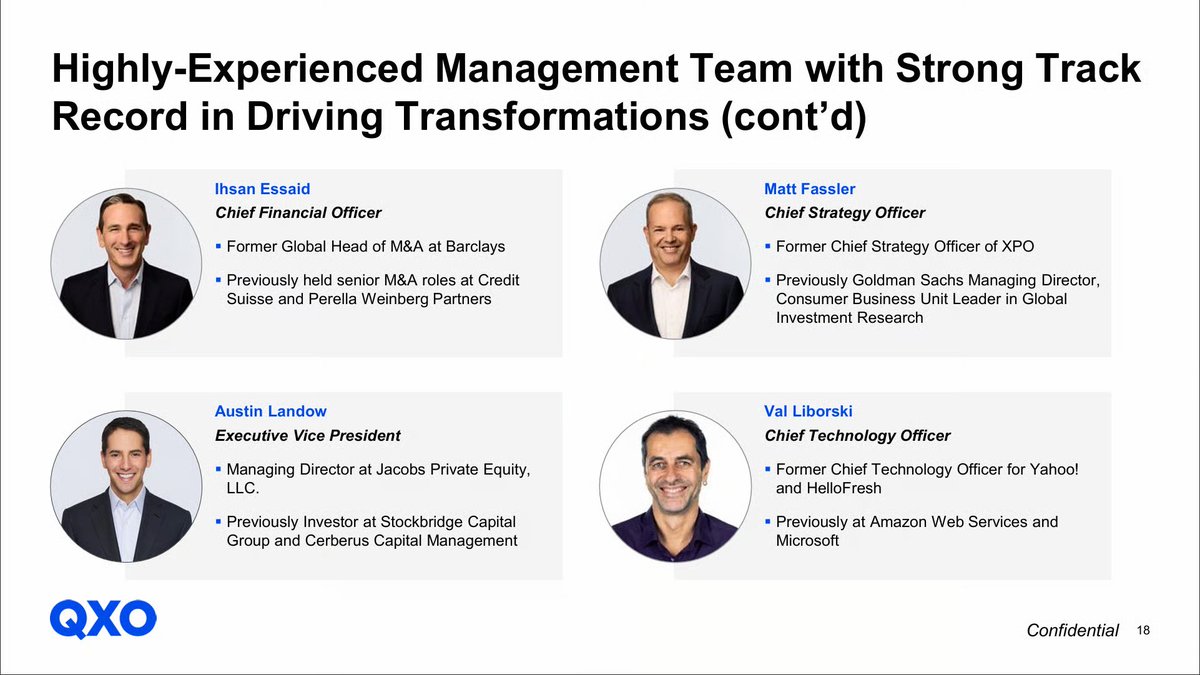

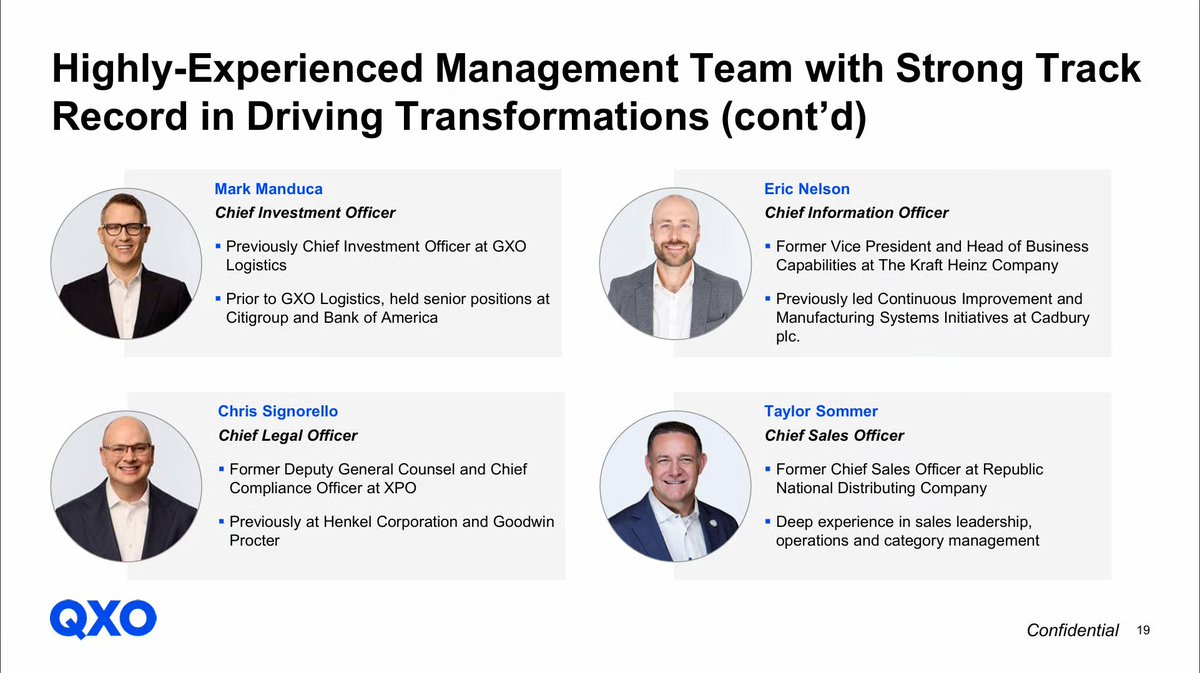

In under two years, QXO $QXO went from a tiny software shell to $8.6B in revenue. It didn't grow there. It bought its way there.

It raised $5B at launch, which Bloomberg called the largest equity offering the building products sector had ever seen, then went shopping:

→ Beacon Roofing: $11B (April 2025), the platform that made $QXO the largest publicly traded roofing and waterproofing distributor in North America.

→ Kodiak: $2.25B (April 2026), a $2.4B-revenue distributor of lumber, trusses, windows, and doors.

→ TopBuild $BLD: $17B (announced April 2026), set to roughly double EBITDA.

TopBuild is the largest insulation distributor and installer in North America, an 18% EBITDA margin business versus the 8% QXO's roofing runs.

Combined, the company is $18.1B of revenue, $2B of EBITDA, ~1,150 branches, and 28,000 employees, with #1 or #2 positions across insulation, roofing, waterproofing, and lumber.

And the two he walked away from say as much as the wins:

→ Rexel: $9.4B hostile bid the board rejected as too low. He walked.

→ GMS: $5B bid, then he stepped aside when Home Depot outbid him at $110/share.

Fast and aggressive, but he won't chase a deal past his number.

The TopBuild deal still has to close in Q3, and it's already drawn the usual merger-objection lawsuits, including a Delaware suit seeking to delay the QXO shareholder vote.

These almost always settle for added disclosure, but the close is the catalyst to watch.

P.S. I wrote a 5k word deep dive on $QXO last week. Link in bio!

1

1

5

484

Jun 12

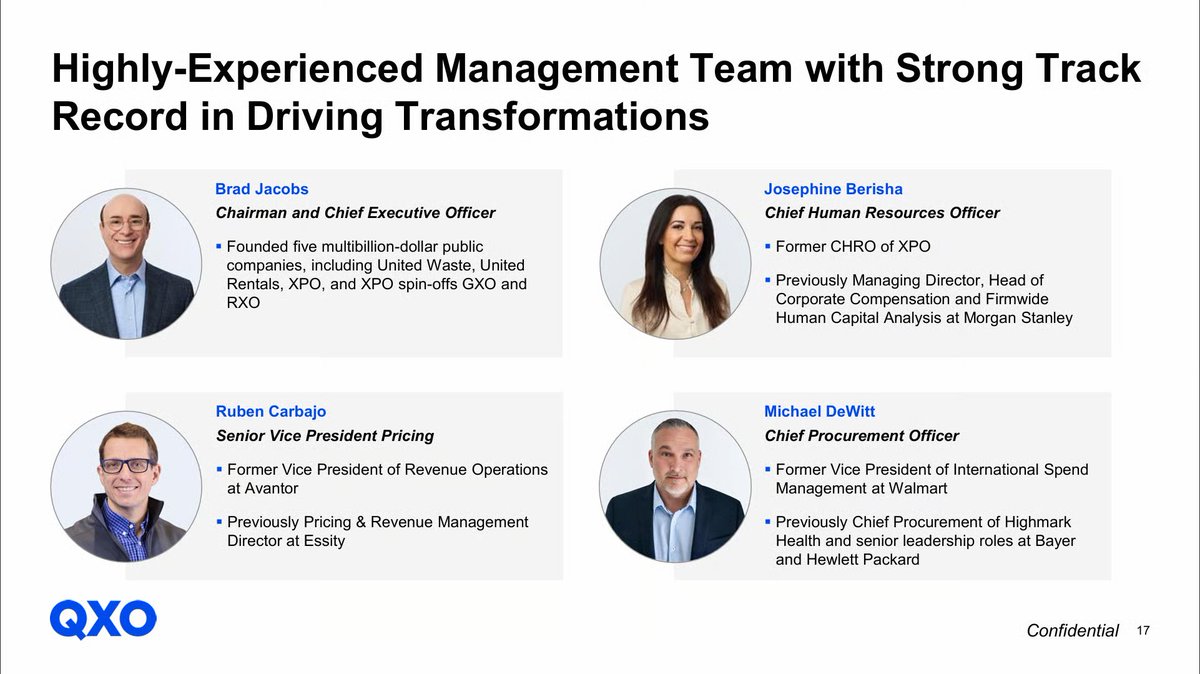

What if I told you the operator who built five separate multibillion-dollar public companies is running his playbook again, this time on an $800B industry?

The name is Brad Jacobs.

He built United Waste, United Rentals, XPO, and the XPO spin-offs GXO and RXO. His new vehicle is QXO $QXO, which distributes roofing, waterproofing, and building products across the U.S.

His model is the same every time:

→ Pick a large, fragmented, unglamorous industry.

→ Buy a platform company.

→ Apply a transformation playbook: procurement, data-driven pricing, network optimization, technology.

→ Use cash and stock to buy more companies.

→ Repeat until the industry looks different.

He's run that exact sequence three times:

→ United Waste: compounded 55%/yr to its 1997 sale, beating the S&P by 5.6x.

→ United Rentals $URI: ~250 acquisitions, ~200x for early backers.

→ XPO $XPO: $150M built into a top-10 logistics company, ~50x, later split into XPO, GXO, and RXO

Across all of it: ~500 acquisitions and $50B raised. Building products is roll-up #4.

Why this industry? Jacobs called it old and durable, the kind of business AI can't disrupt but can enable.

U.S. houses average 40 years old, commercial buildings 50 , and much of the infrastructure beneath them is a century old. The demand doesn't disappear, and it's never been professionalized at scale.

The target: $50B in revenue and $7.5B in EBITDA, a 15% margin against the 8% the core runs today. And the bench chasing it is stacked with his old XPO and GXO operators.

1

1

4

431

Jun 12

👉 I published a 5k word deep dive on the company last week. You can read most of it for free here: newsletter.stablebread.com/p…

1

199

Jun 11

The bottleneck isn't entirely chips anymore. It's electricity.

A 100 MW AI data center needs the entire electrical infrastructure--transformers, busways, and switchgear.

Every component has multi-year backlogs.

Transformer lead times stretched from under a year in 2019 to 3-5 years today. Switchgear reportedly sold out through 2028.

And 30-50% of AI data centers planned to open in 2026 are expected to be delayed or cancelled.

Eaton $ETN and Schneider Electric $SU.PA benefit at the building level (alongside Vertiv $VRT from the cooling layer).

Monolithic Power $MPWR makes the voltage regulators that feed the chips.

Behind them sit gas turbines, on-site fuel cells (Bloom Energy $BE), and small modular nuclear reactors.

Today this industry is arguably the cleanest supply-constraint story in tech.

1

1

1

210

Jun 11

Bottlenecks move. That's the whole point.

2023 was GPU chips.

Early 2024 was HBM memory.

Late 2024 and most of 2025 was CoWoS packaging.

2025 into 2026 is power and grid capacity.

From here, the bottlenecks get less obvious. Cooling chemicals facing new regulation, rare-earth magnets for cooling pumps, fiber optic supply, and electricity generation itself.

The right investing question isn't "buy NVIDIA" or "buy SK Hynix." It's which layer of the stack holds pricing power for the longest, and which name at that layer is best positioned to defend it as supply catches up.

Each new bottleneck creates a pocket of unusual margins. Each one eventually attracts capital that compresses them.

Buy the next bottleneck, not the last one.

1

1

87

Jun 11

Feeling behind on the AI compute stack and the bottlenecks driving it?

Whoever sits at the bottleneck has pricing power. When supply catches up, the bottleneck moves up the stack (every 12-18 months) and the pricing power moves with it.

Here's how the AI compute stack works, layer by layer, with the names making money at each layer. ↓

1

1

2

316

Jun 11

Each modern AI chip dissipates 700-1,000 watts of heat. Air can't extract that economically.

Direct-to-chip liquid cooling runs coolant right across the chip, then back to a CDU (cooling distribution unit) sitting at the end of each row of racks.

Vertiv $VRT ended Q1 2026 with a $15B backlog and a book-to-bill ratio near 2.9x (meaning $2.90 of new orders for every $1 of revenue).

Vertiv supplies most of the CDUs. Modine $MOD and nVent $NVT are smaller specialists. Boyd and Aavid own the cold-plate niche but are private.

1

1

2

230

Jun 11

Once data needs to travel between server racks (which hold multiple servers), copper wires can't keep up.

Copper signals only carry about a meter at AI speeds before they degrade. Past that, you need fiber optic cables.

Optical transceivers convert the electrical signal into light, send it through the fiber, then convert it back at the far end.

Every ~18 months, transceiver speeds double. 400G → 800G → 1.6T → 3.2T. Each new generation grows the total market because data volumes grow faster than prices fall.

Coherent $COHR and Lumentum $LITE supply the photonic components.

Fabrinet $FN does the high-precision assembly. As of 2025, Fabrinet held 100% share of 1.6T transceivers for NVIDIA's Blackwell platform.

Innolight $300308.SZ is the Chinese leader.

1

1

1

174

Jun 11

Once you have the chip, you need to make 8 GPUs act like 1.

Each chip in a server only works on part of the AI training problem. They share data constantly at terabit speeds.

$NVDA's solution is called NVLink NVSwitch. It's a high-speed communication fabric (essentially the highway between chips) that lets 8 GPUs work as a unified system.

This is one of NVIDIA's quieter moats. Whoever owns the communication protocol gets to price the silicon that plugs into it.

Broadcom $AVGO and Marvell $MRVL sell competing networking chips that hyperscalers can use to build their own fabric.

Astera Labs $ALAB makes connectivity chips that keep signals clean at the speeds AI requires.

If these alternatives gain ground, NVIDIA's networking advantage erodes even if it keeps GPU share.

1

1

1

134

Jun 11

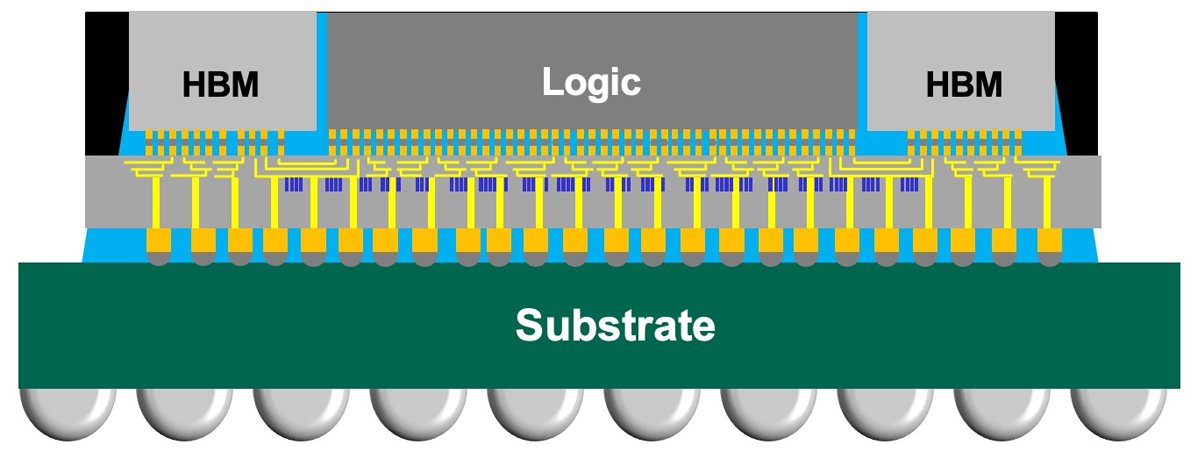

You've got the chips. You've got the memory. But connecting them at the speeds required is its own manufacturing challenge.

The dominant technology is $TSM's CoWoS (Chip-on-Wafer-on-Substrate). Think of it as the manufacturing process that physically wires the chip and memory together into one finished product.

Through most of 2024 and 2025 this was the actual bottleneck on AI chip output. Wafer supply existed, but CoWoS capacity didn't.

$TSM is scaling CoWoS from ~35K wafers/month in late 2024 to ~130K/month by end of 2026. Still sold out through 2026, with $NVDA reportedly reserving most of the available capacity.

Samsung Foundry and Intel Foundry are coming up as second sources.

ASE $ASX and Amkor $AMKR handle older-generation packaging.

1

1

1

128

Jun 11

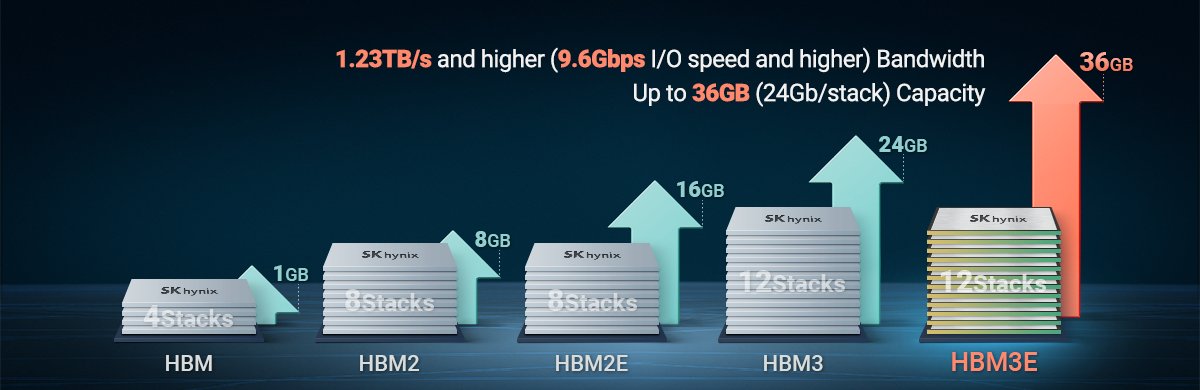

Next, the memory wall.

Compute is useless without fast memory right next to it. Modern AI chips are bonded to 4-8 stacks of high-speed memory called HBM (High Bandwidth Memory).

Without enough memory bandwidth, the chip sits idle waiting for data. This became the binding constraint in late 2023.

SK Hynix $000660.KS qualified HBM3 with $NVDA first and ran with it. Q1 2026: 72% operating margin (all-time high) on ~$38B in revenue.

Management said cumulative HBM commitments now cover more than three years of supply.

Samsung $005930.KS spent two years improving manufacturing quality after falling behind on HBM3. Their next-generation memory (HBM4) is ramping for NVIDIA's Vera Rubin platform in H2 2026.

Micron $MU is the third entrant and the only US-based supplier.

Memory has always been a cyclical business in semis. Margins this high will eventually attract enough new capacity to bring prices back down.

1

1

198

Jun 11

Start with the chips themselves.

An AI training server is built around 8 accelerator chips (basically GPUs designed for AI math) wired together on one board.

$NVDA owns this layer. They've dominated for two years, but that's starting to change.

Hyperscalers (AWS, Google, Meta, Microsoft) got tired of paying NVIDIA's premium and started designing their own chips.

They partner with Broadcom $AVGO and Marvell $MRVL to manufacture them.

$GOOGL's Ironwood TPU, $META's MTIA, Anthropic's training chips, and OpenAI's chip are all on Broadcom's roster.

$AMD ships MI300/MI400 and has emerged as the credible #2 to NVIDIA. $MSFT, $META, and $ORCL have deployed it for inference workloads and some training.

$INTC ships Gaudi but has struggled to gain hyperscaler adoption.

1

1

262

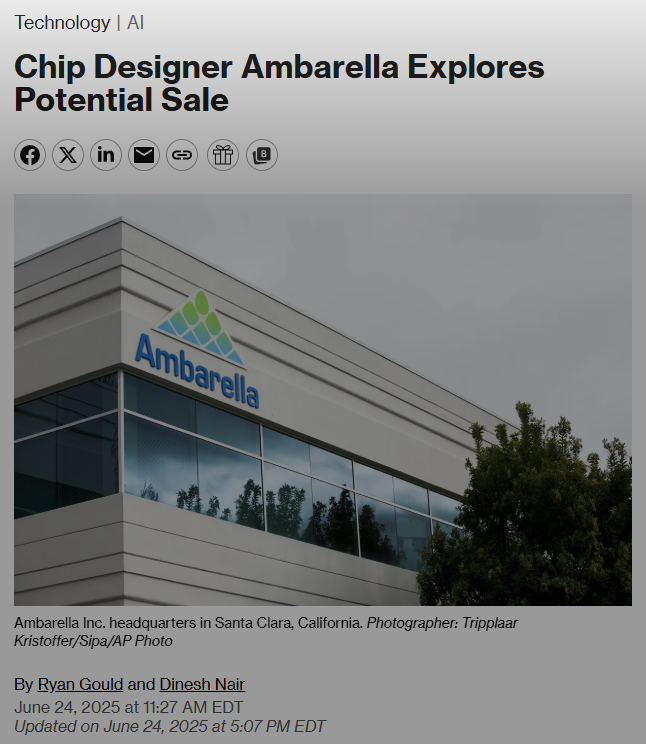

Jun 10

$AMBA investors shouldn't forget the company tried to sell itself less than a year ago.

The stock jumped 21% on the news, then the sale process went quiet.

On June 24, 2025, Bloomberg reported $AMBA had hired bankers to explore a sale and was already talking to potential buyers.

The report flagged two buyer types: (1) chip rivals looking to fill out an automotive or physical-AI portfolio, and (2) private equity firms.

$QCOM and $NXPI are the cleanest fits. PE seems unlikely given $AMBA's growth-stock profile and minimal EBITDA.

$QCOM has been actively building Snapdragon Ride and bought Veoneer's Arriver ADAS software in 2022, so $AMBA's CV3 Cooper platform would accelerate that roadmap with transformer-native silicon and robotics/security exposure.

$NXPI leads in auto processing and networking but is weak in AI vision, which is exactly $AMBA's strength.

$RNECY is a third option given how aggressive they've been on deals (IDT $6.7B, Dialog $5.9B, Altium $5.9B).

11 months later, no deal has been announced.

That silence could mean it's dead, or it could be the normal pace of a complex deal.

Either way, the underlying setup hasn't changed. $AMBA is the rare public, pure-play edge AI chip company small enough for a larger player to absorb (<$3B market cap).

What an acquirer wants is slow and expensive to build alone:

→ CVflow architecture, proven across 46M shipped chips.

→ Cooper software platform, with 200 model architectures running on it.

→ Radar IP.

→ Automotive design pipeline.

The Hanwha LTA strengthens the standalone case and reduces pressure on the board to sell.

But it also makes the franchise more valuable to a strategic acquirer. A signed $800M customer commitment across multiple chip generations is exactly what acquirers pay premiums for.

1

1

4

1,443

Jun 10

I published my full write-up on $AMBA late last month. With prices falling recently I think it's worth a read: newsletter.stablebread.com/p…

1

434

Jun 10

AI data centers, CPOs, memory, and chips are cool and all… but what about the eggs you had for breakfast? 🥚

Cal-Maine Foods $CALM is the largest egg producer in the U.S., selling about one in four eggs Americans eat.

At ~$77/share, it trades at 5x trailing earnings, with a ~14% distribution yield (divs buybacks), $1.15B net cash, and no debt.

That's a net cash floor of $24/share, ~31% of the market cap.

Plus the company keeps on acquiring smaller producers, and is now pushing into prepared foods, egg patties, omelets, waffles, and pancakes, to become more than just an egg company.

And with the company down 34% from recent highs, is the market punishing it too harshly just because egg prices came back down?

Publishing a full writeup on the topic in 2 hours. Link in bio!

2

461

Jun 9

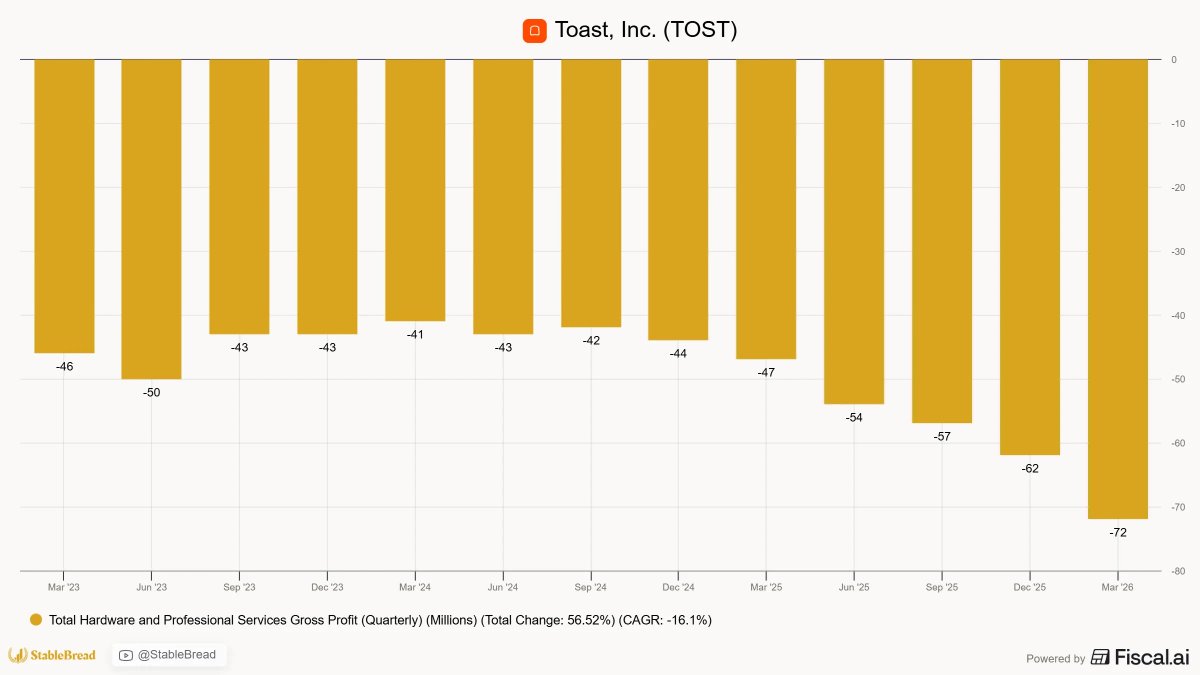

Toast $TOST beat Q1 2026, raised full-year guidance, and still fell ~15%.

UBS cut its price target to $34, Citi to $36, DA Davidson to $28. One of the reasons was the Q2 margin guide, which came in soft on hardware costs.

Toast sells terminals and handhelds below cost to win the location. That segment lost $220M in FY2025 and another $72M in Q1 2026, by design.

The problem is what's inside the devices.

Memory contract prices are up 80-95% in recent quarters, with DRAM and NAND supply dominated by Samsung $SSNLF, SK Hynix $HXSCL, and Micron $MU, and AI data centers absorbing their output.

IDC expects the shortage to run through 2026 and well into 2027. That's a multi-year cost pressure on a below-cost hardware model.

On the earnings call, CFO Elena Gomez addressed it directly:

"The impact to the 2027 P&L will be larger than the impact to 2026... we're gonna have healthy margins in both 2026 and 2027... we don't anticipate this will have any structural impact to our P&L over the long term."

In numbers: roughly 1.5 points of adjusted EBITDA margin in 2026, more in 2027, against a ~34% margin on recurring gross profit today and a 40% long-term target.

Toast is buying memory ahead of need to protect supply. Inventories rose to $136M from $114M at year-end.

The market is pricing a structural problem. So either Gomez is wrong about 2027 being the peak, or the market is punishing $TOST permanently for a temporary cost hit.

1

6

729

Jun 10

Found this post helpful? Consider checking out the full 4k word $TOST deep dive here: newsletter.stablebread.com/p…

239

Jun 9

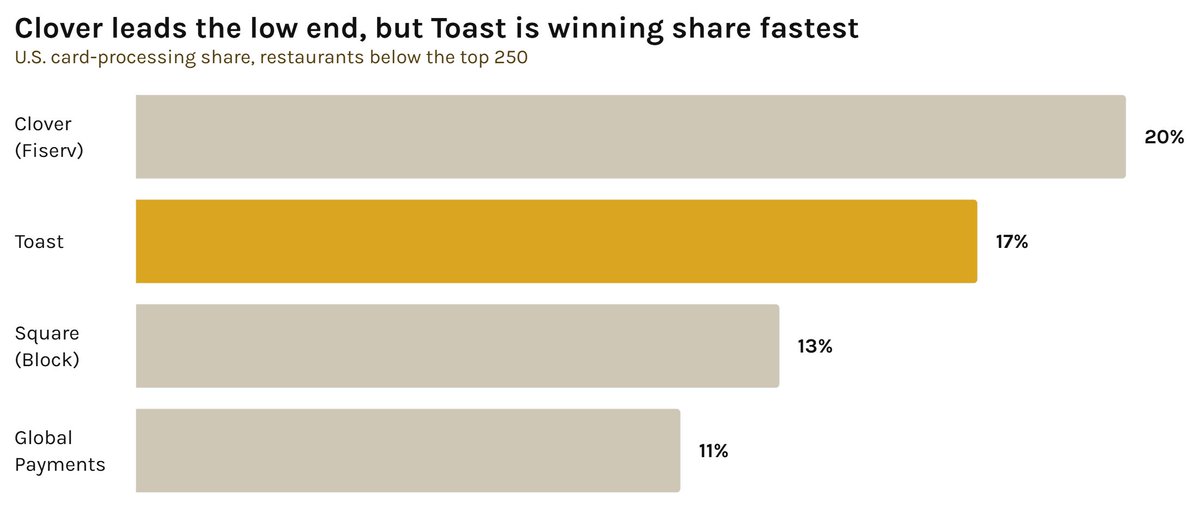

Clover, not Toast $TOST, is the share leader in small-restaurant POS.

Toast's "roughly 1 in 5 U.S. restaurants" stat is real. But it measures Toast against every restaurant in the country, not the smaller-restaurant pool where Toast, Clover, and Square actually compete.

A January 2026 Baird report estimated card-processing share for U.S. restaurants below the top 250 chains, ~75% of a ~$1.1T market:

→ Clover (Fiserv): 20%, 175,000 locations.

→ $TOST: 17%, 145,000.

→ Square (Block): 13%.

→ Global Payments: 11%.

The ~171K locations $TOST reports is its total across all segments, enterprise included.

In the below-top-250 slice, Baird credits it with ~145K. Clover is ahead by ~30K.

Square is the one moving. Its food-and-beverage GPV grew 16% y/y in Q4 2025, slower than $TOST's 22%, but its parent Block said fine-dining and other full-service operators (sit-down restaurants) are increasingly switching to Square.

Full-service is the segment $TOST leads.

Then there's DoorDash. It hasn't launched a POS, but analysts report it's testing one in San Francisco, Phoenix, and New York.

A projection reported by PYMNTS has DoorDash reaching 20% of U.S. restaurants by 2035 if it launches. Small restaurants already lean on DoorDash for delivery, so a combined POS-and-delivery offer would be hard to ignore.

However, these threats are unlikely to impact $TOST's numbers in the near term. $TOST's win rates rose y/y in FY2025, and it's adding 30,000 net locations a year.

Baird also surveyed 37 restaurateurs, and most said they liked their vendor and planned to expand with it, with no talk of leaving.

So bulls aren't wrong that $TOST scaled. They're wrong if they think SMB leadership is settled. Clover is ahead in the SMB slice by Baird's count, and Square is pushing into full-service, where $TOST leads.

2

417