Joined February 2024

- Tweets 612

- Following 18

- Followers 897

- Likes 1,611

153 Photos and videos

Pinned Tweet

Jun 9

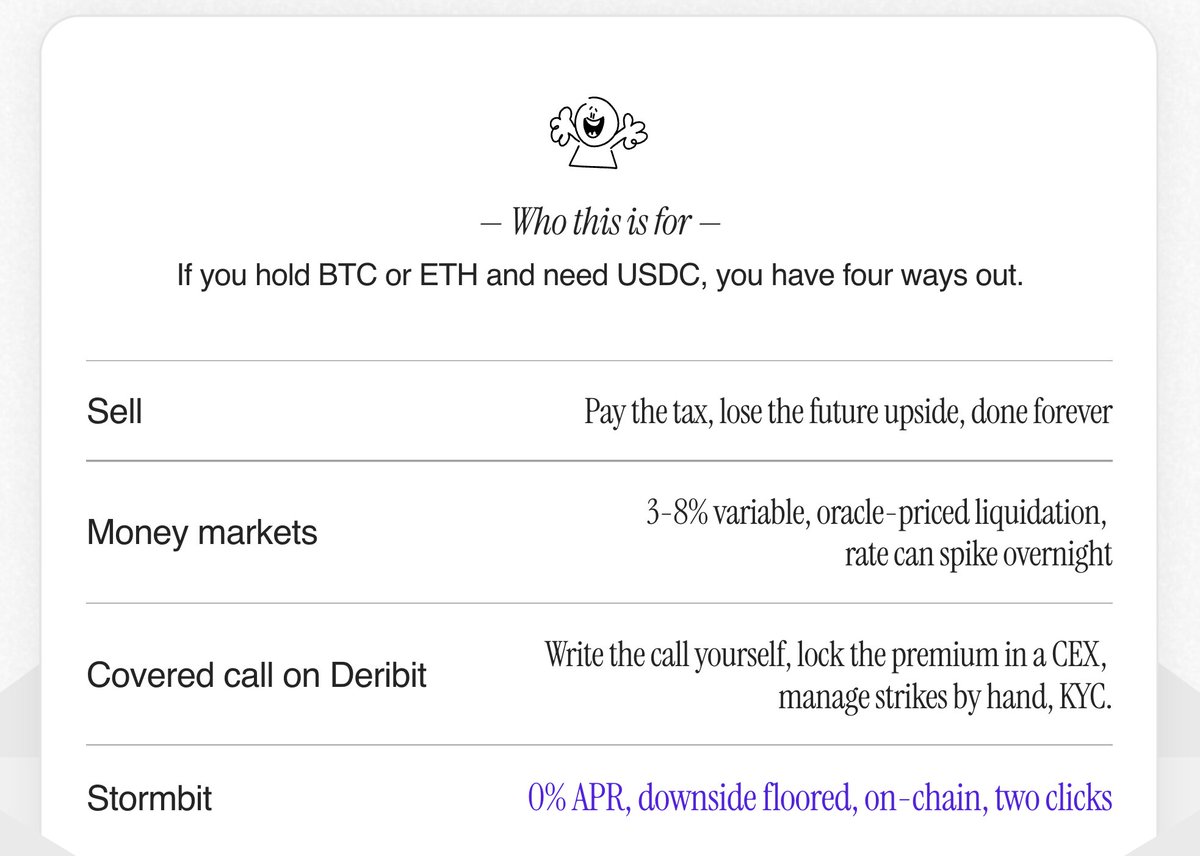

Earn extra income on your ETH and BTC.

Available right now.

DM for exclusive access to the best rates.

1

1

2

91

Jun 9

DeFi credit has one shape: borrow, pay interest, get liquidated.

Goldman has run a second category for 30 years: collar-backed credit. 0% interest, no liquidations, maturity-only settlement. $138B book.

That category doesn't exist on-chain yet. We're building it. It has to be unbreakable from day one.

Grateful to do that work with @ethereumfndn @nethermind @chainlinklabs and the rest of this cohort.

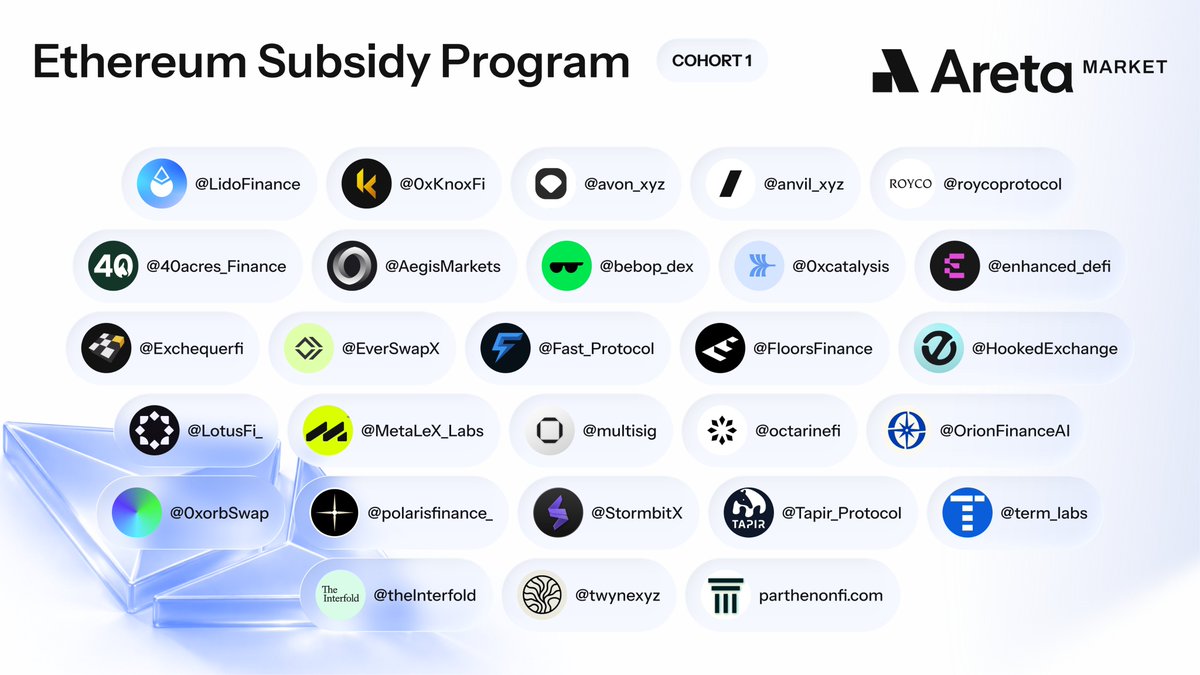

1/ World, meet Cohort I of the Ethereum Security Subsidy Program. Out of 100 applicants, here are the 30 projects selected for our first of many cohorts.

Proudly securing @ethereum mainnet together with @ethereumfndn, @nethermind and @chainlinklabs.

108

1/ World, meet Cohort I of the Ethereum Security Subsidy Program. Out of 100 applicants, here are the 30 projects selected for our first of many cohorts.

Proudly securing @ethereum mainnet together with @ethereumfndn, @nethermind and @chainlinklabs.

25

46

190

32,208

Loans w/o liquidations @StormbitX 🤝

Jun 2

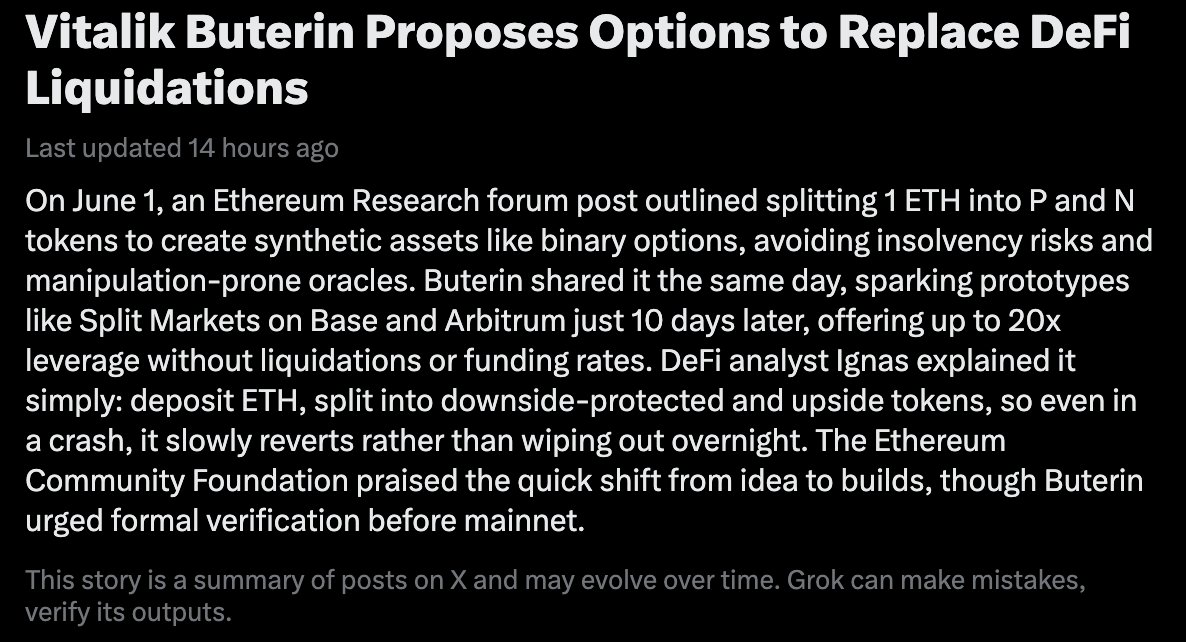

LATEST: ⚡ Vitalik Buterin has proposed building synthetic assets with options instead of debt, a shift he says could make algorithmic stablecoins less vulnerable to forced selloffs.

1

1

144

May 28

0%

Top 3 lending markets: 5.29% to borrow WETH/USDC. Rates are spiking.

0% at @StormbitX.

DM for beta access. Onboarding 1-on-1.

141

May 14

Stormbit is not a money market.

It is not a yield farm.

It is the oldest credit primitive in finance, rebuilt as code, opened to anyone with a wallet and a thesis.

We think it is the only honest way to lend money on a blockchain. We think the rails get written once.

We think it is us.

2

2

214

May 13

Only on stormbit.finance

Gated access. OPEN NOW.

Cohort 3 last seats.

Cohort 4 open for registrations.

2

124

Yes, very well said.

Velocity was about managing risk after origination.

(I liquidate)

Robustness is about pricing it before.

(I don't liquidate).

Stormbit prices risk.

@StormbitX

Apr 21

for the last few years, velocity was your edge in DeFi.

it's increasingly becoming robustness now.

what that means:

- risk controls that hold up

- incentives that attract durable liquidity

- systems that behave predictably under stress

- and security that assumes constant adversarial pressure.

^these are the differentiators now and going forward imo

1

1

2

240

. @LucaProsperi nails the diagnosis. DeFi is brutal for borrowers. Liquidation risk is structural and no protocol has fixed it at the source.

Lenders unknowingly underwrite risk they don't understand. Borrowers get liquidated. Nobody solved both sides.

The math was always there. Someone just had to build it.

@StormbitX is right now the only protocol where lenders and borrowers are EQUALLY protected.

VCs looking for the next DeFi primitive, DMs open.

@LucaProsperi @adcv_ @theempirepod - give us 30 min. If we're wrong, we're wrong (i doubt :) ). If we're right, you have your story.

@Mehdi96_

@jrcarlos2000

@StormbitX

Apr 13

DeFi is not great at lending

DeFi today is optimized for trading and arbitrage. Not lending to corporates, mortgages or private credit

"How big actually is the target market / addressable market of DeFi lending? It remains to be proven. If it's as big as credit we are very, very far away" @LucaProsperi @m0

1

3

9

1,055

Apr 1

Stormbit will be in the room. Come say hi.

Tomorrow during EthCC Cannes 🇫🇷

A curated gathering of vault curators, infra, LPs, and RWA issuers shaping the future of onchain yield.

11:00–15:00

Thanks to our event partners @TradingProtocol @ipor_io @1deltaDAO

Apply: luma.com/b9ieeqyb

1

1

194

Interesting thread.

The $6.2M isn't really about curators being slow. It's about a deeper architectural assumption — that risk management can be a role instead of a primitive.

When you step back, institutional DeFi needs three risk layers solved at the protocol level:

1. Depeg risk — does the peg hold?

2. Price risk — does the collateral hold?

3. Credit risk — does the borrower hold?

Most of what exists today solves these with people and permissions. The interesting question is what happens when you solve them with math.

When you're originating hundreds of loans a day across multiple collateral types, you can't have humans in the loop deciding if the market is dangerous. The pricing model already knows.

We're closer to this than most people think.

Mar 22

1/ Millions in bad debt, at the time of writing, were created across Gauntlet's Morpho vaults from the Resolv USR exploit.

Almost all of it was supplied ** after ** the exploit.

So why would curators supply millions in USDC to a broken market?

Let’s dive in.

1

5

357

Mar 13

Fixed rates will take DeFi beyond crypto — and we agree.

That's why we built from day one as fixed-rate, fixed-term, with insurance on every loan.

The future of onchain lending is predictable, bounded, and institutional-ready.

See you in Cannes 🏖️🩴

1

1

11

835

I can't agree more.

The vision I had since we started building @StormbitX is exactly this — lending only scales when both sides know their terms upfront and the downside is bounded.

We believe every loan should be insured. No liquidation cascades. No oracle surprises. Borrower pays the hedge cost, LP gets real yield from real interest.

Fixed-term. Hedged.

That's the hill we're building on.

1

4

9

619

Feb 28

late night at stormbit hq and someone needs to say this:

stop building smarter agents. start insuring the dumb ones.

every loan on stormbit ships with an insurance. defined downside. no liquidation. ever.

when agents arrive at scale they won't need 99% accuracy. they'll need insurance.

that's us. anyway back to code.

**intern taking control of the main account**

2

138

Feb 26

In other terms,

Redefining Yield through Insured Credit.

$1T in cumulative loans is proof that the world is ready for on-chain credit.

But as the market matures, the question shifts from 'Where can I borrow?' to 'Where is my yield protected?

Aave built the foundation for the $1T era 👏

@StormbitX is building for the next era by evolving the model—shifting from pure lending to insured yield products.

We are de-risking it.

Together, let's bring credit on-chain.

1

200