- Tweets 15,594

- Following 5

- Followers 6,936

- Likes 11,003

ALT Weekly watchlist of top 10 institutional setups highlighting key stocks, strategies, and ratings in various sectors.

ALT Weekly watchlist of top 10 institutional setups highlighting key stocks, strategies, and ratings in various sectors.

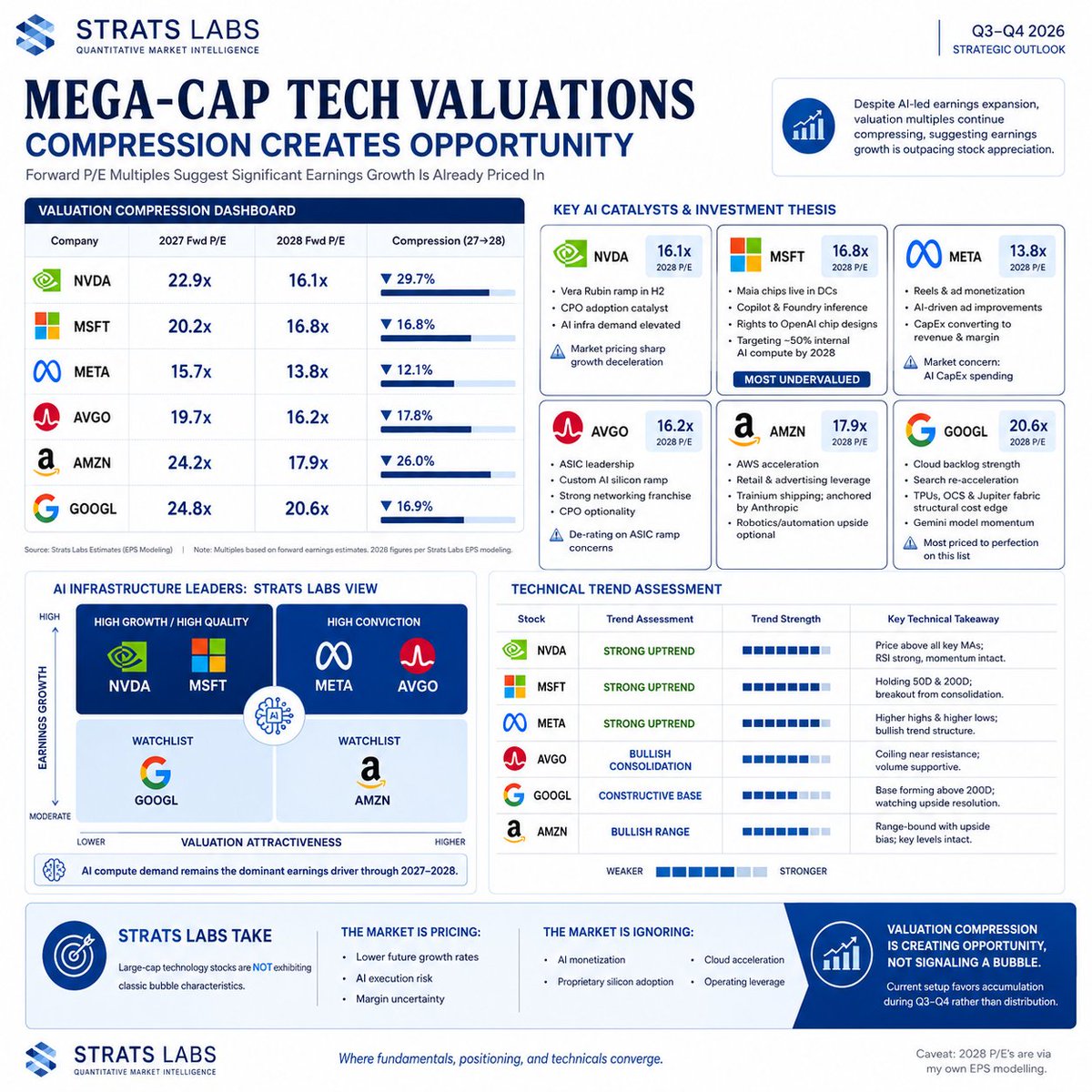

ALT Valuation dashboard of major tech companies showing forward P/E estimates for 2028, illustrating investment opportunities in compressed valuations.

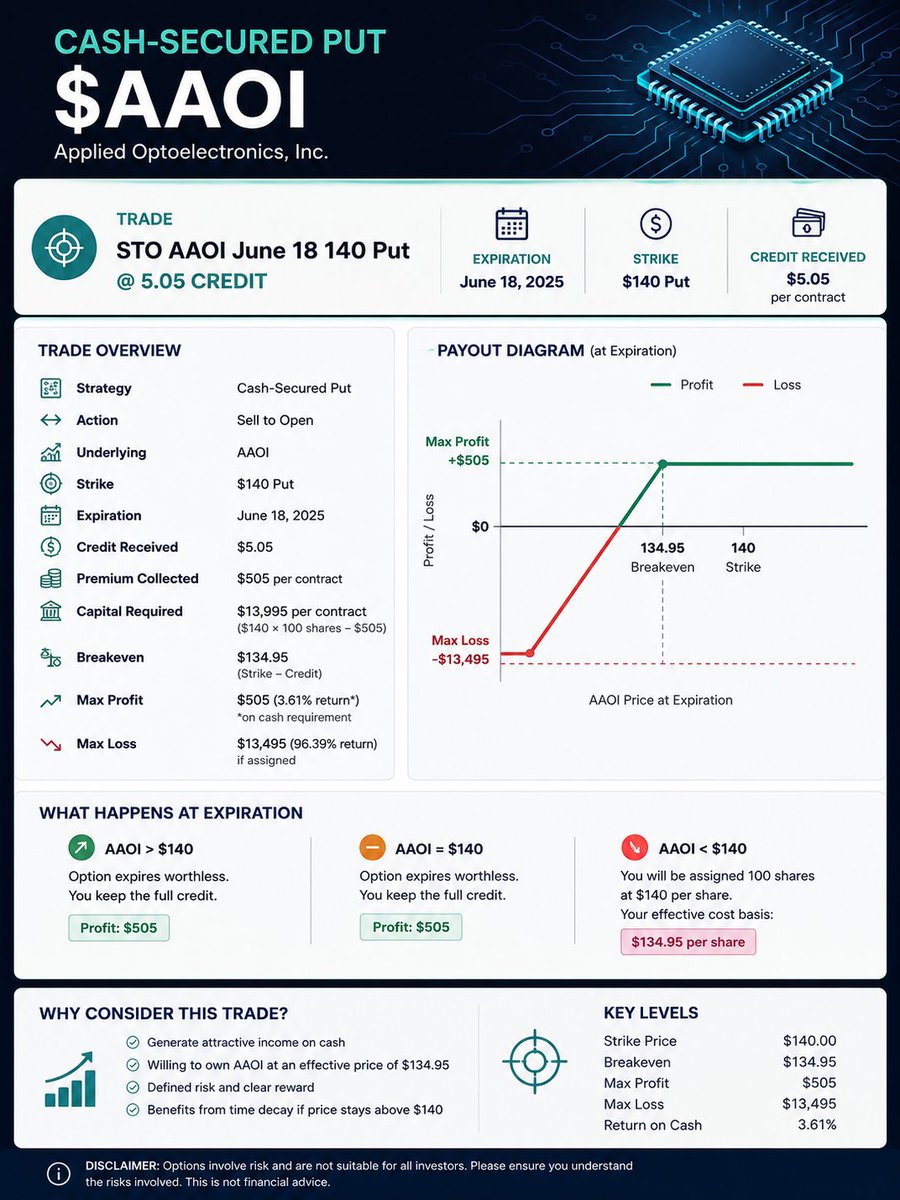

ALT The chart shows implied volatility trends for Applied Optoelectronics options, highlighting a significant rise for short-term calls.

ALT AAOI cash-secured put trade closed, showing a profit of $145 with a return of 54.19% over 13 days, detailing trade specifics.

ALT Stock charts displaying a daily and four-hour view of Nebius, highlighting a target price of 250 and market indicators with divergence noted.

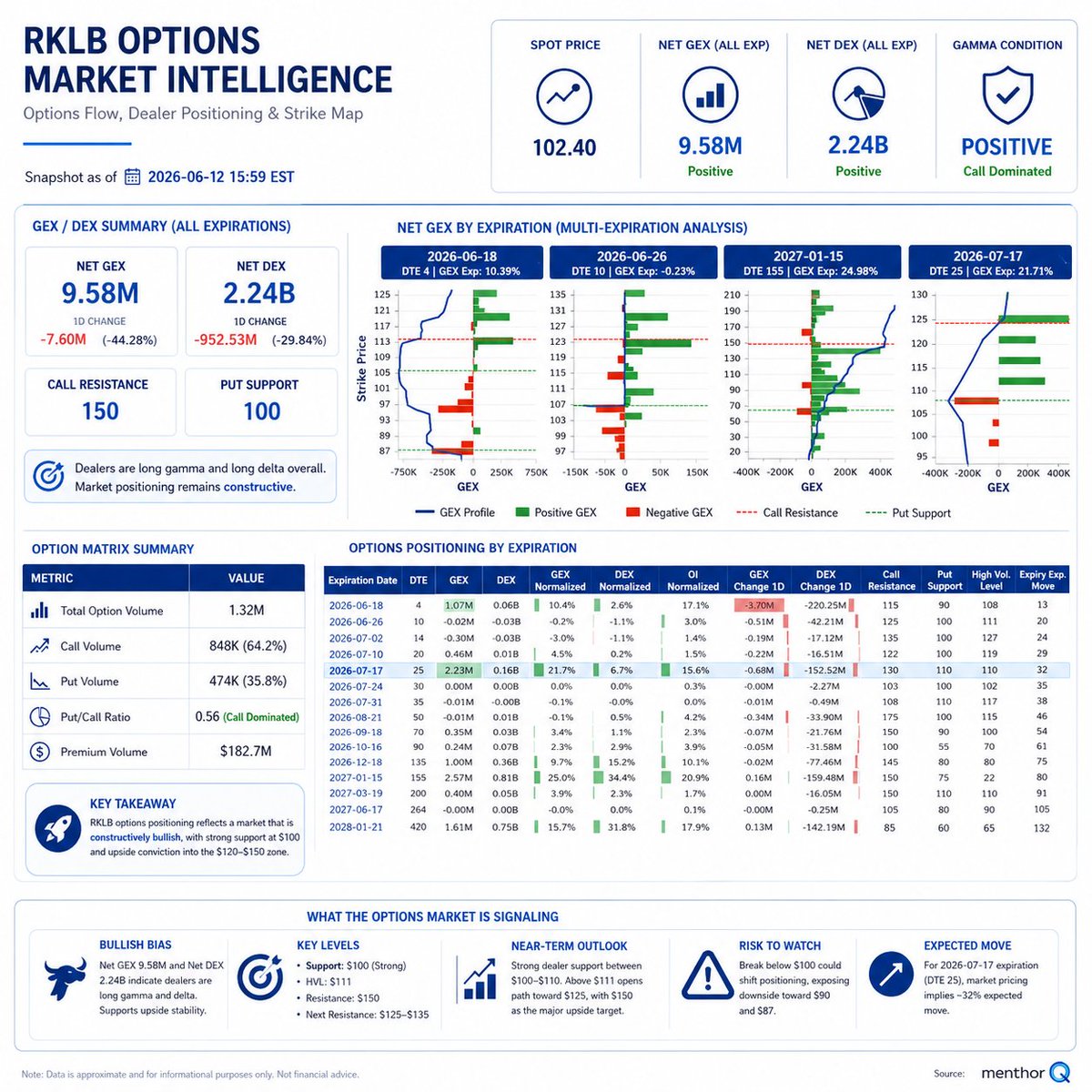

ALT Options data for $RKLB shows positive net gamma, with key resistance at 150 and support at 100. Market sentiment leans bullish.

ALT Stock chart for IREN shows a respected trading channel, featuring a recent breakout and bullish flag pattern, with noted divergence indicators.

ALT Two stock charts for IREN and NEBIUS show price trends and patterns, including resistance levels and potential target prices.

ALT Five-minute candlestick chart for SPCX shows fluctuating stock prices, peaking above 176 and currently around 169.20.

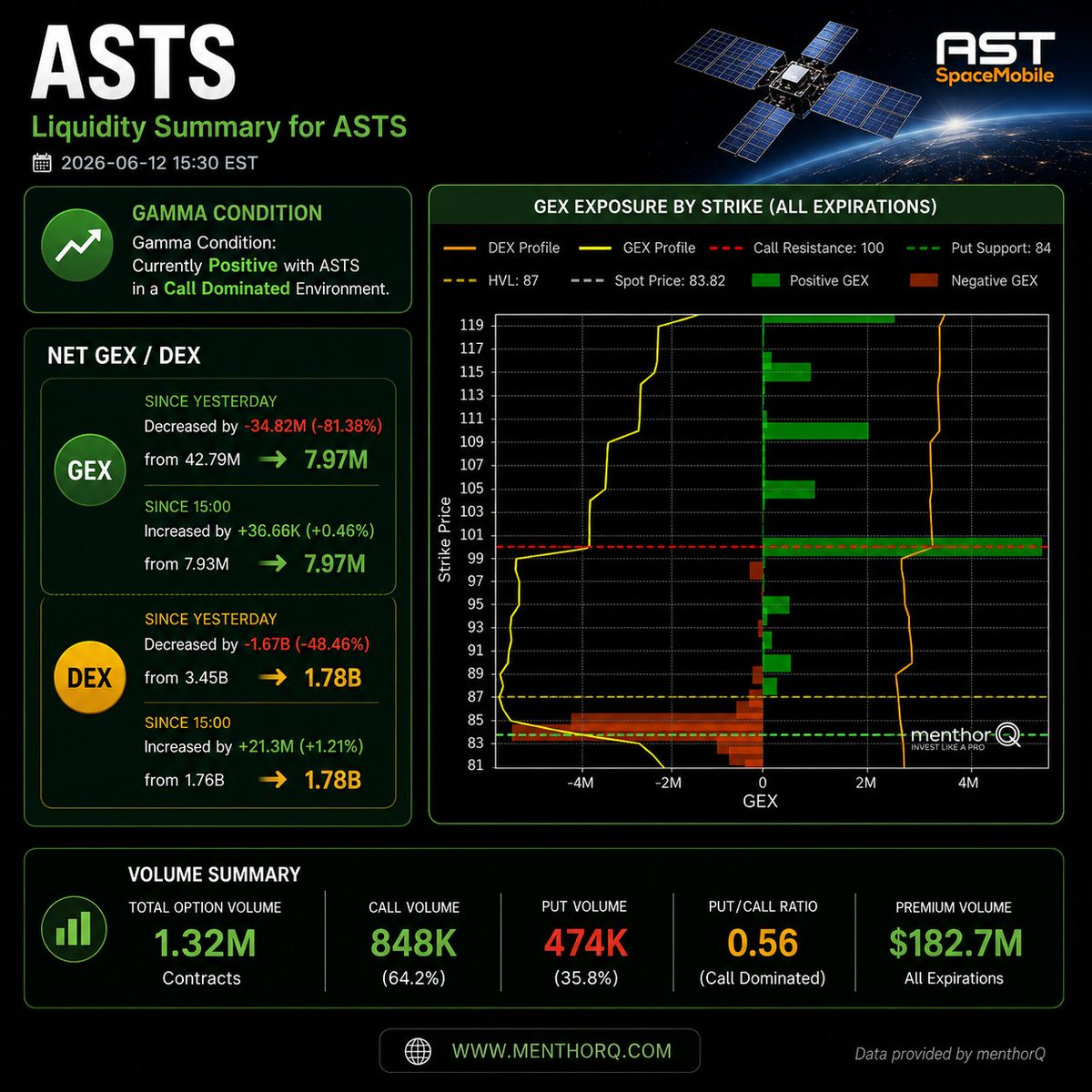

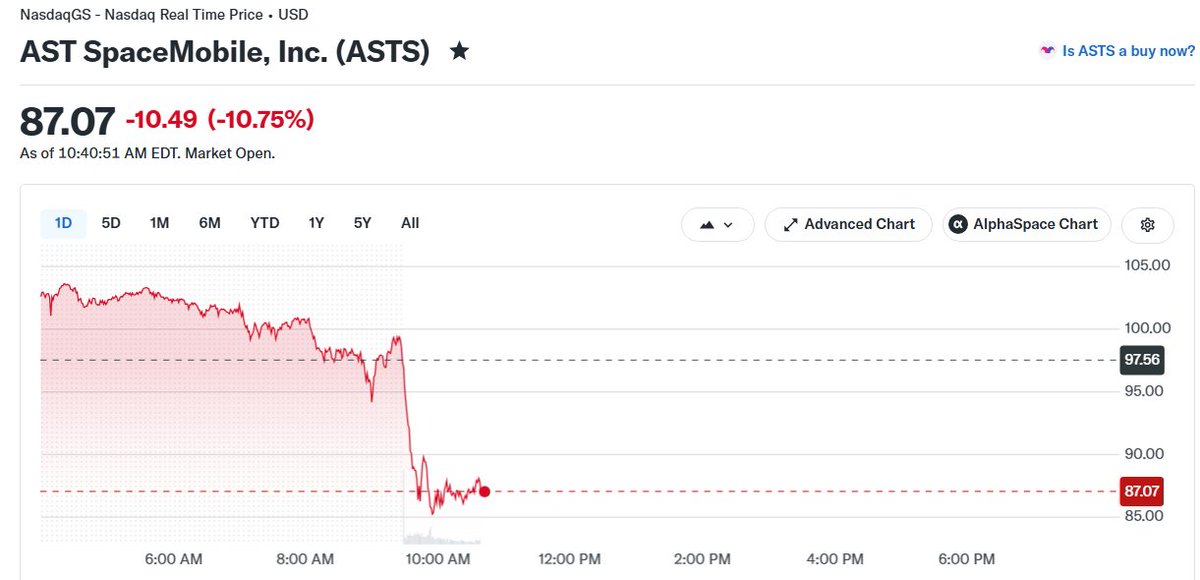

ALT A financial trading interface displaying trades related to $ASTS, showing realized P&L and details of options trades.

ALT A smiling man with light hair, born June 14, 1946, is featured, possibly indicating a public figure in a digital profile format.

ALT A smiling man with light hair, born June 14, 1946, is featured, possibly indicating a public figure in a digital profile format.