Joined April 2022

- Tweets 981

- Following 9

- Followers 17,440

- Likes 444

517 Photos and videos

Pinned Tweet

9 Sep 2025

Follow our new X account. 👇

Note that @StriveFunds will remain active and be the source for all things related to our asset management business.

The "at Strive" will keep you up to date on all things related to $ASST and our Bitcoin treasury strategy.

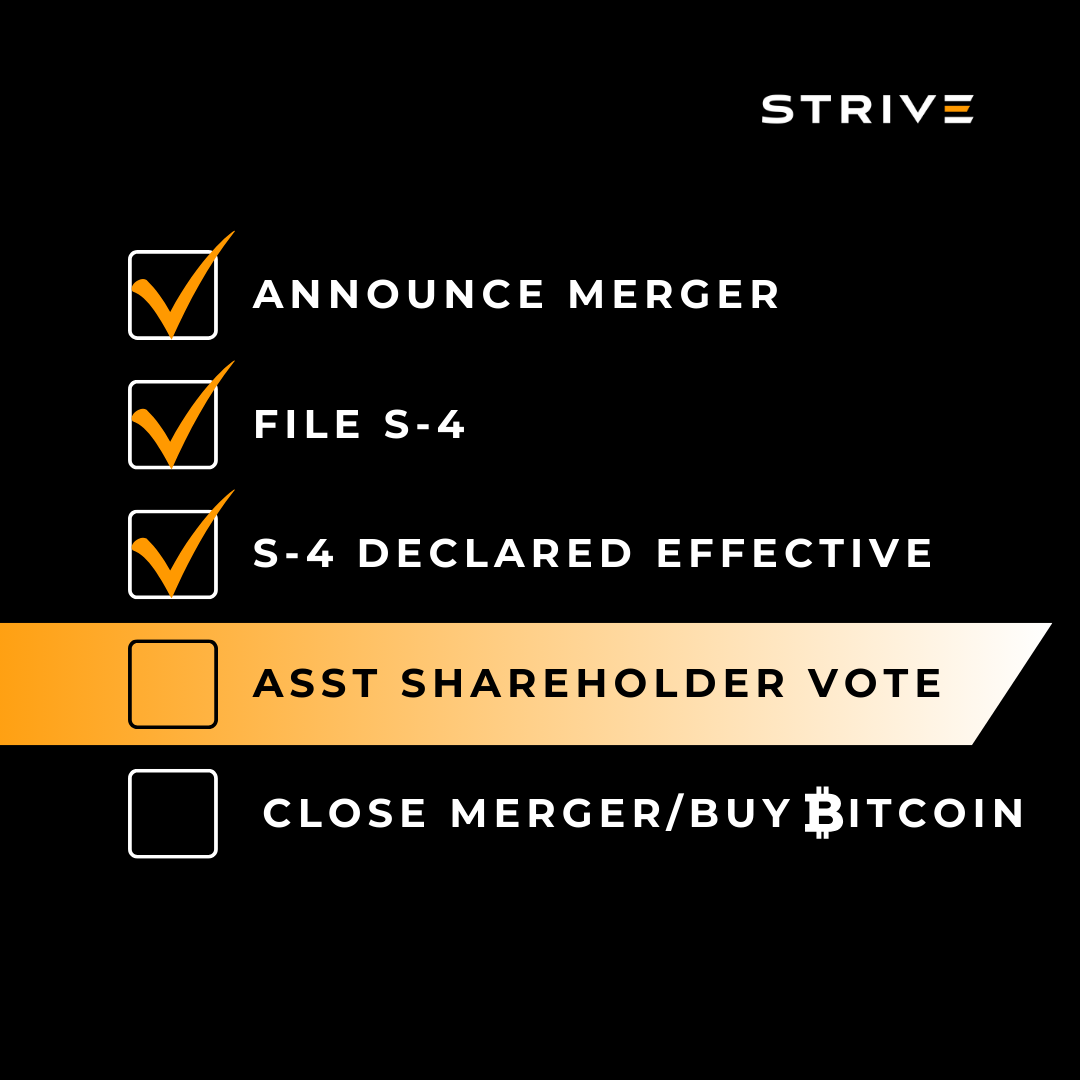

Asset Entities - $ASST - shareholders approved the merger with Strive this afternoon.

Next up: close the merger and buy Bitcoin.

15

6

63

27,526

RT @ColeMacro: Strive filed a registration statement with the SEC for the T-Strive Digital Credit ETF.

Please read the prospectus for deta…

162

12 Nov 2025

97

Strive updates:

1. SATA listed on Nasdaq following oversubscribed & upsized IPO.

2. Strive acquired 1,567 BTC for ~$162M at ~$103,315 per Bitcoin. As of 11/10/25, we hodl 7,525 Bitcoin.

3. New $ASST & $SATA investor presentation released.

4. $SATA dividends expected to be ROC (Return Of Capital).

88

223

1,444

542,675

Strive Asset Management retweeted

17 Sep 2025

With Strive, it is important to recognize both the near-term technicals and the long-term fundamentals and business plans.

On the technical side, we just closed a $750M PIPE, and those investors will be receiving shares at any time within 30 days of the merger close, expanding the float in a major way. It is also worth noting that the PIPE was raised above the $1.02 merger price between Asset Entities and Strive, which was a strong outcome for the company but one that naturally creates near-term technical considerations and nuances.

On the fundamental side, the picture is very different. We have raised substantial permanent capital to launch our Bitcoin treasury. We immediately filed a WKSI shelf & both an ATM and a repurchase program, giving us substantial optionality to accrete additional Bitcoin and increase Bitcoin per share. We have no debt, announced our ambitions to launch a perpetual preferred security in 2025, and have assembled a highly experienced leadership team and board to navigate these waters. Management’s shares are locked up and no one has sold.

I strongly suggest people do their own research and invest accordingly as the institutionally complex technicals work through and the strong fundamentals begin to shine. Our team is laser focused on building a perpetual engine for shareholder growth powered by Bitcoin.

57

36

247

99,203

STRIVE (NASDAQ: $ASST) ANNOUNCES BOARD OF DIRECTORS & INITIAL BITCOIN STRATEGY DETAILS

BOARD OF DIRECTORS

- Chairman @ColeMacro CEO @Strive

- @shirishjajodia Corporate Treasurer @Strategy

- @werkman Chief Investment Officer @Swan

- @BitcoinPierre CEO of The Bitcoin Bond Company

- @jameslavish Co-Founder @BTCOppFund

- @Avik Chairman @FREOPP

- @BenPhiat CFO @Strive

- @LoganBeirne CLO @Strive

- @shiasark CMO @Strive

- @MoneroMahesh Co-Founder @EV3ventures

- @JonathanMacey Corporate & Securities Law @Yale

- Observer @PunterJeff VP of Bitcoin Strategy. @Strive

INITIAL BITCOIN TREASURY STRATEGY DETAILS

- 69 Bitcoin starting balance sheet (351 Exchange)

- $750 million cash from PIPE

- $750 million potential additional cash from warrants

- $450 million at-the-market (ATM) offering

- $500 million stock repurchase program

- 2025 publicly registered perpetual preferred equity offering ambitions

- Zero debt from convertible bonds or other offerings

Link to full press release in comments.

133

133

988

468,491

Strive Asset Management retweeted

9 Sep 2025

Follow our new X account. 👇

Note that @StriveFunds will remain active and be the source for all things related to our asset management business.

The "at Strive" will keep you up to date on all things related to $ASST and our Bitcoin treasury strategy.

Asset Entities - $ASST - shareholders approved the merger with Strive this afternoon.

Next up: close the merger and buy Bitcoin.

15

6

63

27,526

5 Sep 2025

Vote YES!

Voting for the $ASST merger with Strive is now enabled on ALL platforms, including Charles Schwab, Fidelity, E*Trade, and Robinhood, and the IProxy Direct site!

If you are having issues voting, please contact your brokerage or vote directly here: iproxydirect.com/index.php/a…

$ASST Shareholders: Voting is now enabled on ALL platforms, including Charles Schwab!

Over the past week, $ASST & Strive have been working hard behind the scenes with our proxy solicitor, Broadridge, and a proxy printer to ensure the delivery of all voting information. All brokerages and shareholders of record as of 7/21 should have received a communication.

Please vote YES now before the 9/8 midnight deadline! While we expect the vote to pass, we will be forced to delay the merger close if there are not enough votes by the shareholder meeting on 9/9.

4

5

39

10,149

5 Sep 2025

For more information, read ASST’s press release: prnewswire.com/news-releases…

2

16

2,914

29 Aug 2025

A Bitcoin Order You Can Bank On

Earlier this month, President Trump issued an executive order guaranteeing fair access to banking services for all Americans, including Bitcoin-related firms that have long been denied services simply for operating in a disfavored industry.

This isn't Trump's first move against debanking. Federal banking agencies have already removed "reputational risk" from their assessments—the buzzword that allowed regulators to pressure banks into shunning digital asset firms, firearms manufacturers, and other politically unpopular industries.

But the August order goes further. It not only requires banks to accept Bitcoin clients going forward, it forces them to make amends for past refusals. Specifically, the order requires banks to "identify and reinstate any previous clients" that were previously "denied services through a politicized or unlawful debanking."

That's important. Under the rules invoked by the previous administration, the government could pressure banks to drop clients, but banks couldn't inform clients why they were being dropped. That secrecy might make sense when cutting off terrorist networks or foreign spy cells, but it makes far less sense when we're talking about Coinbase. Even crypto-skeptic JP Morgan CEO Jamie Dimon complained, "we should be allowed to tell you" what's going on.

Now his wish has been granted. Regulators are making clear they plan to hold banks accountable. Comptroller of the Currency Jonathan Gould has vowed to “commence a review to assess the extent to which the institutions it supervises have or are engaged in politicized or unlawful debanking and take remedial actions if appropriate.” Acting FDIC Chair Travis Hill said he'll do the same.

That's welcome news for digital asset firms, which continue to be debanked despite earlier reforms. Alex Konanykhin, CEO of Unicoin, told Cointelegraph that his company and its subsidiaries "have been de-banked, without explanations, by several banks" including Citibank, Chase, Wells Fargo, City National Bank of Florida and TD Bank. Konanykhin claimed that Unicoin was debanked by four banks this year alone, highlighting how deeply these practices are embedded in compliance culture.

The irony, of course, is that Bitcoin was designed to prevent the very kind of financial censorship to which these firms have been subjected.

But that doesn't mean that Bitcoin is ready to fully replace the fiat system just yet. Miners and node operators will still need to tap electricity grids to power operations, and fiat cash to pay those bills. Bitcoin Treasury Companies still largely need to meet payroll and settle taxes in dollars. And Bitcoin exchanges' raison d'etre is, well, the ability to exchange Bitcoin for other forms of currency, like cash. For now, participation in the Bitcoin economy still requires access to the U.S. banking system.

It's not hard to see why the banks bowed to pressure: blocking Bitcoin wasn't their choice so much as Washington's. But today, the pressure runs the other way, and it comes from the President himself. That doesn't necessarily mean they'll comply, but if they don't, the risks will be a lot more than "reputational."

2

4

22

2,748

Strive Asset Management retweeted

28 Aug 2025

Off zero before deal close, and into the Bitcoin 100, with 69 BTC 😏

Wheels in motion 🏃♂️

18

5

156

19,996

All, thank you for making us aware of various $ASST voting issues across brokerages, including Charles Schwab.

We’re working with $ASST’s proxy solicitor on a daily basis to ensure the delivery of voting information to brokerages and other institutional shareholders to enable voting.

We are encouraged that many of you have already been able to vote and we are hopeful that many of the remaining issues will be resolved by next week post-Labor Day.

Strive is looking forward to a successful YES vote on 9/9 so that we can close the merger and begin our Bitcoin strategy.

7

4

28

7,065

Just to clarify as I’ve been getting a lot of questions about our potential $1.5 billion of dry powder once Strive completes its merger with $ASST:

- We will not receive the first $750mm of USD proceeds until the close (shortly after the 9/9 $ASST vote).

- Once we have USD, then we will start buying Bitcoin.

Another day closer to our pending merger with $ASST & unlocking the first $750 million to begin executing on our Bitcoin strategy as a public company.

We may have an additional $750 million (up to $1.5 billion of total proceeds) within 1 year of the merger close.

7

9

55

35,558

Strive Asset Management retweeted

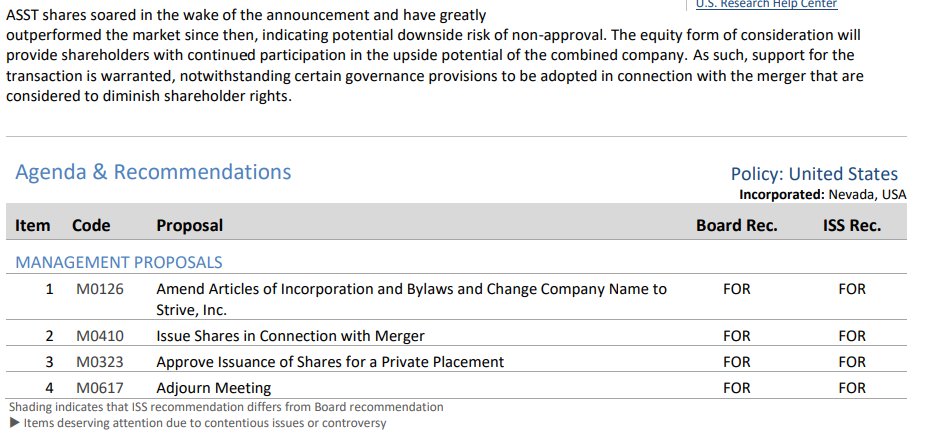

28 Aug 2025

ASST SHAREHOLDER VOTE UPDATE:

ISS recommends $ASST shareholders vote YES for all Management Proposals regarding the merger with Strive to pursue our Bitcoin treasury strategy.

13

15

95

13,593