Joined April 2011

- Tweets 9,356

- Following 652

- Followers 6,084

- Likes 44,937

1,116 Photos and videos

Pinned Tweet

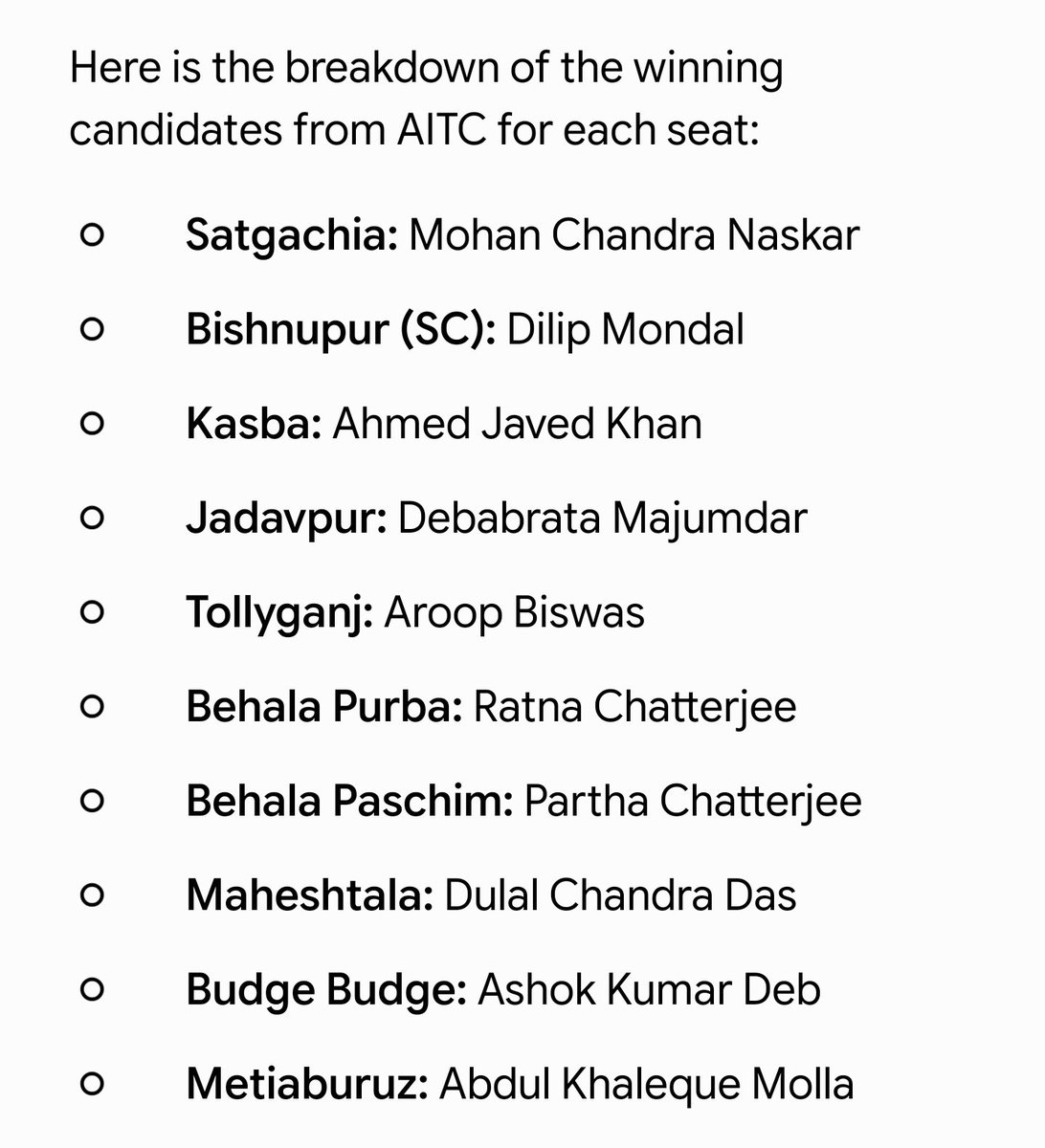

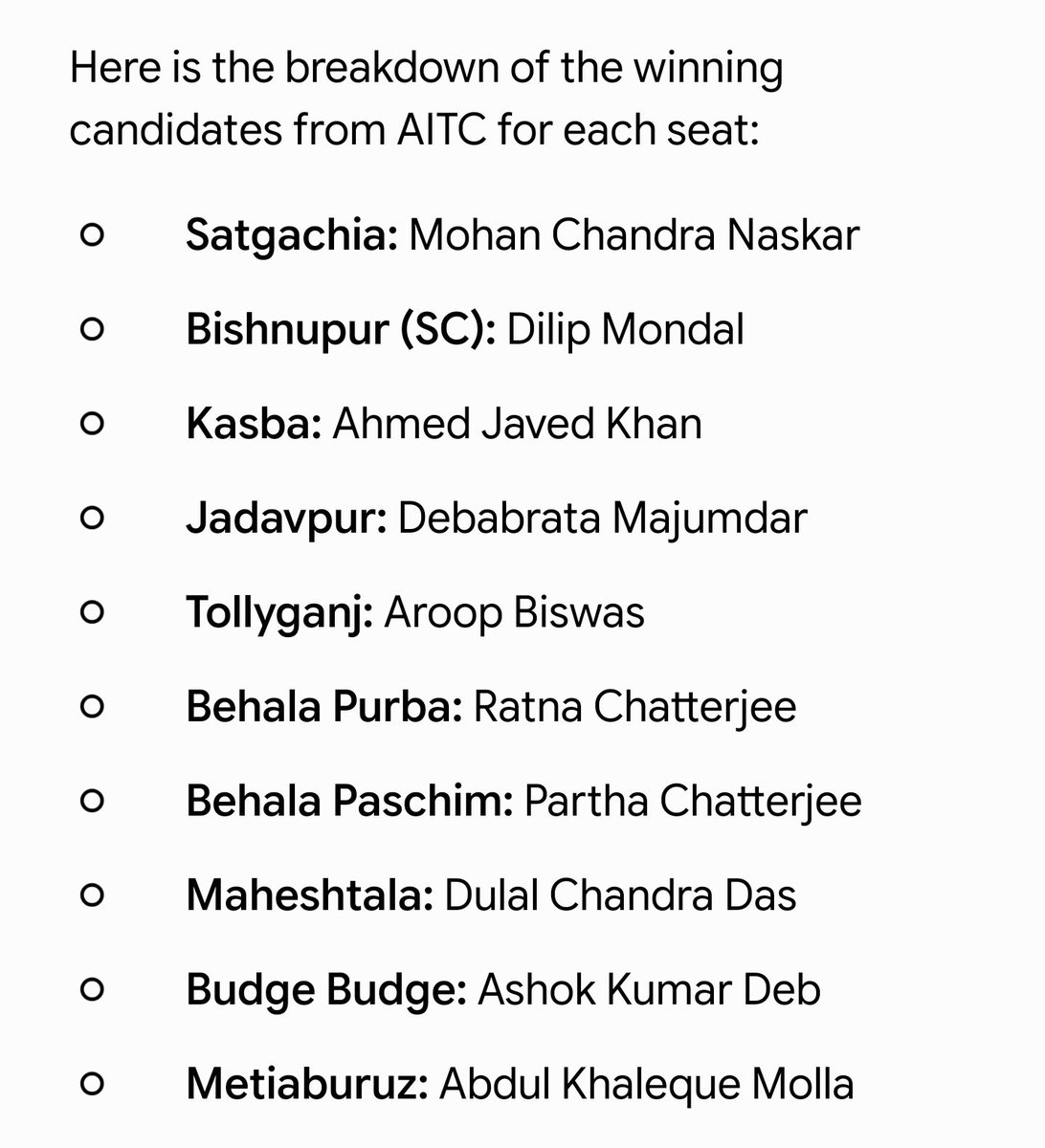

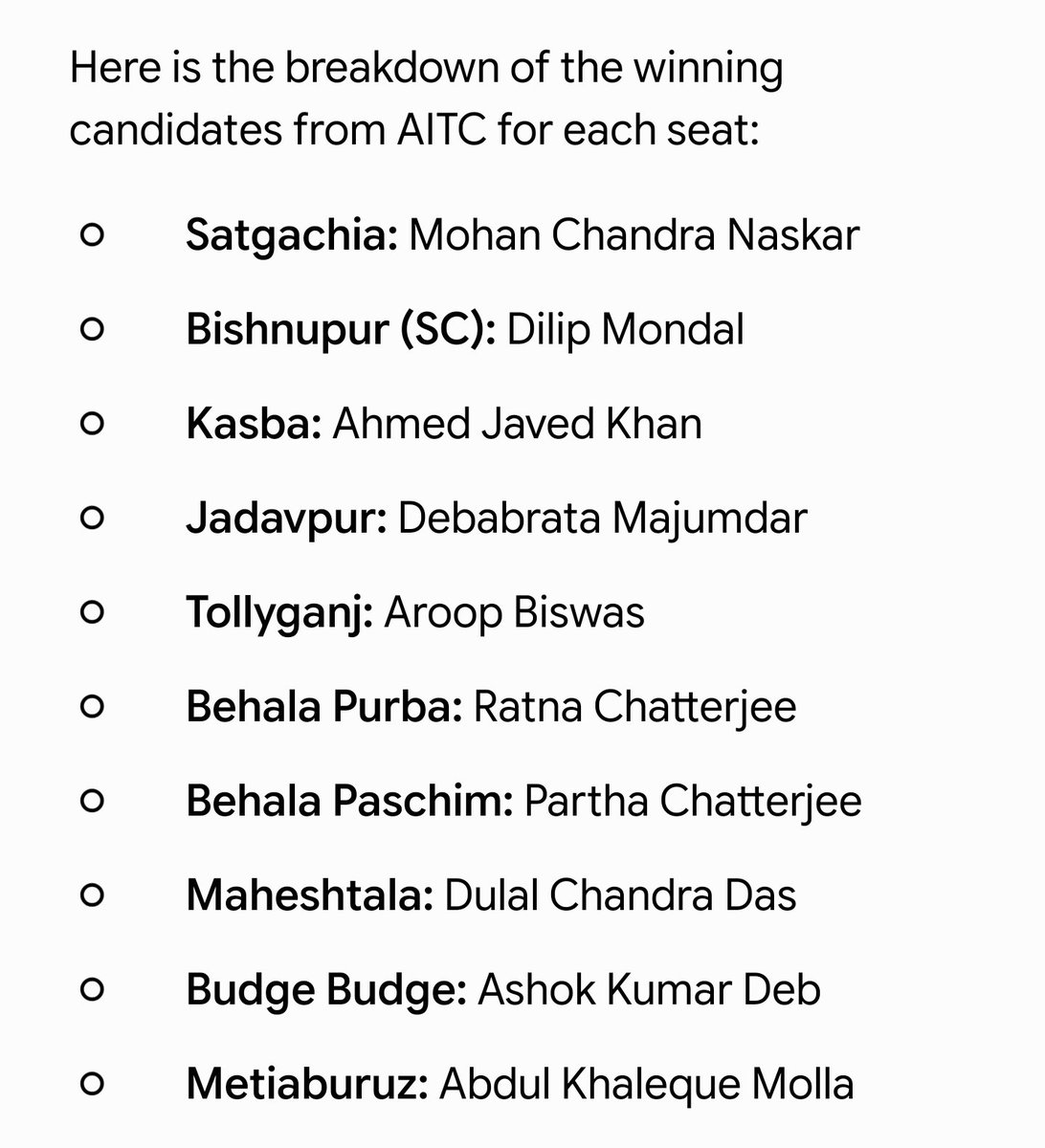

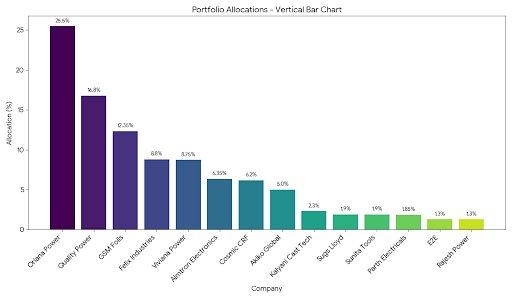

🍕 Portfolio Update: May'2026

(Mainboard 23.5%, SME 76.5%)

-

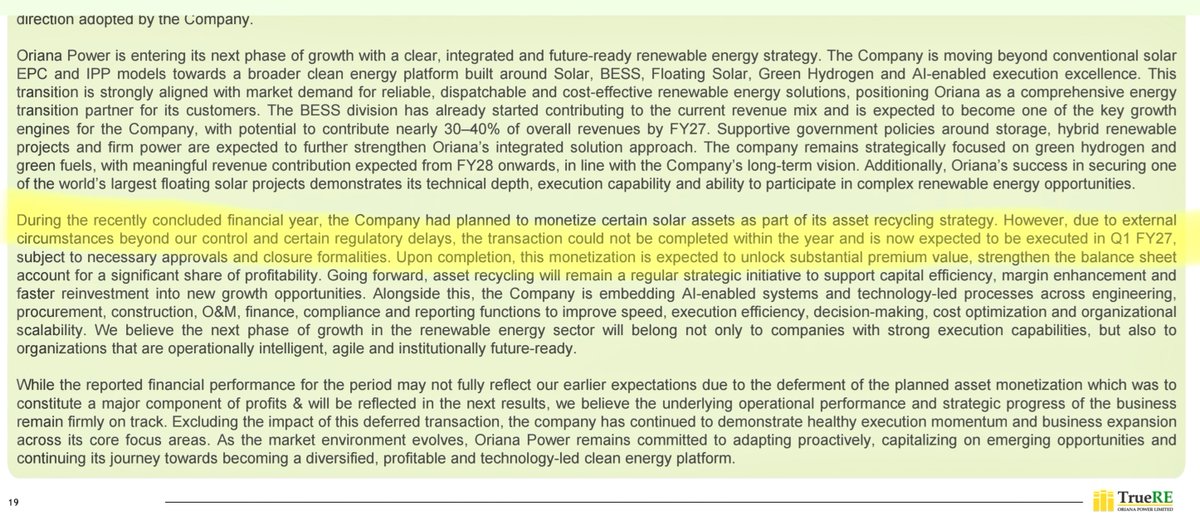

1️⃣ Oriana Power - 16.85%

2️⃣ GSM Foils - 12.45%

3️⃣ Quality Power - 12.40%

4️⃣ Cosmic CRF - 11.35%

5️⃣ Aimtron Electronics- 10.30%

-

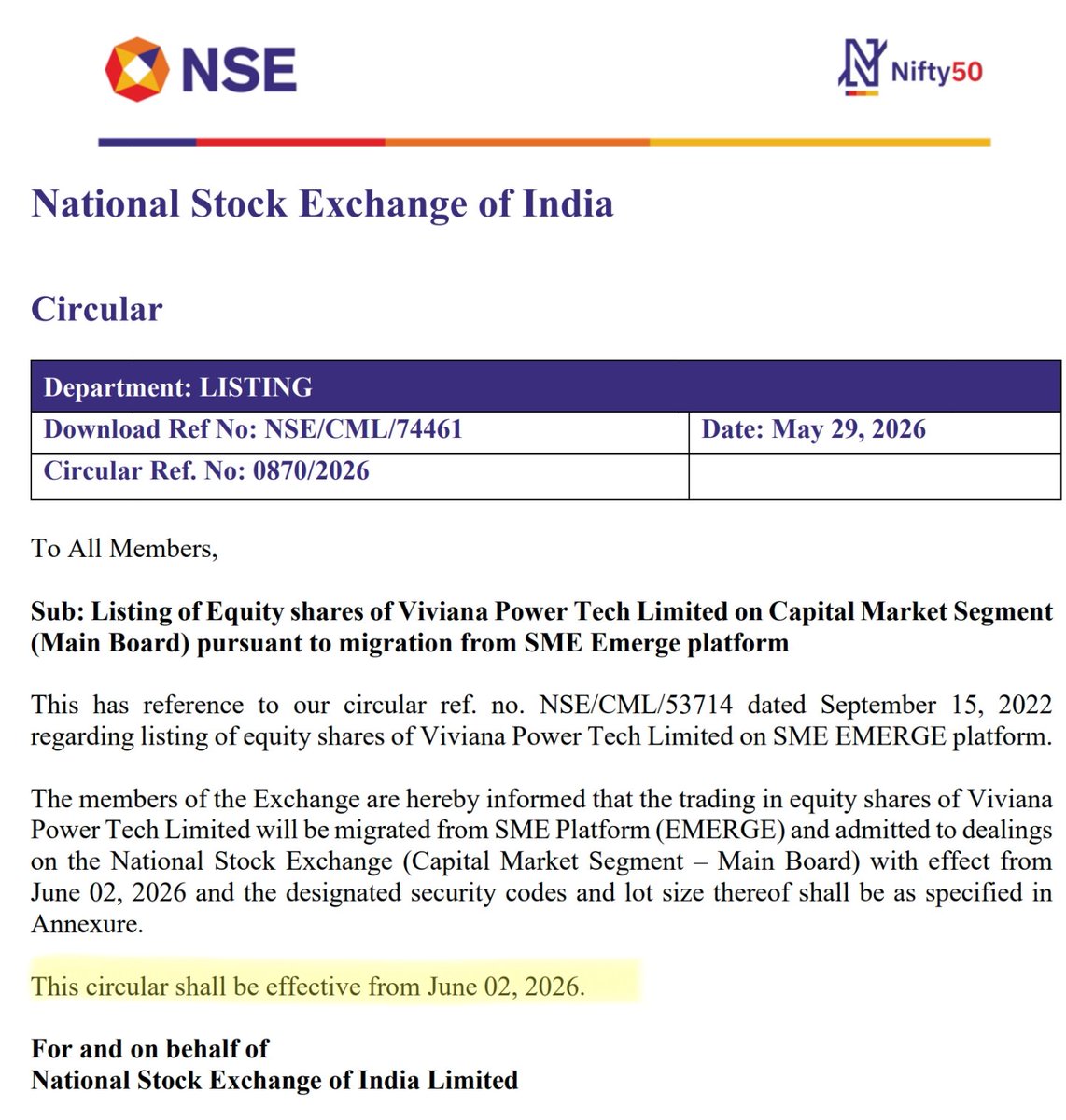

6. Viviana Power - 9.63%

7. Akiko Global - 8.50%

8. Felix Industries - 7.40%

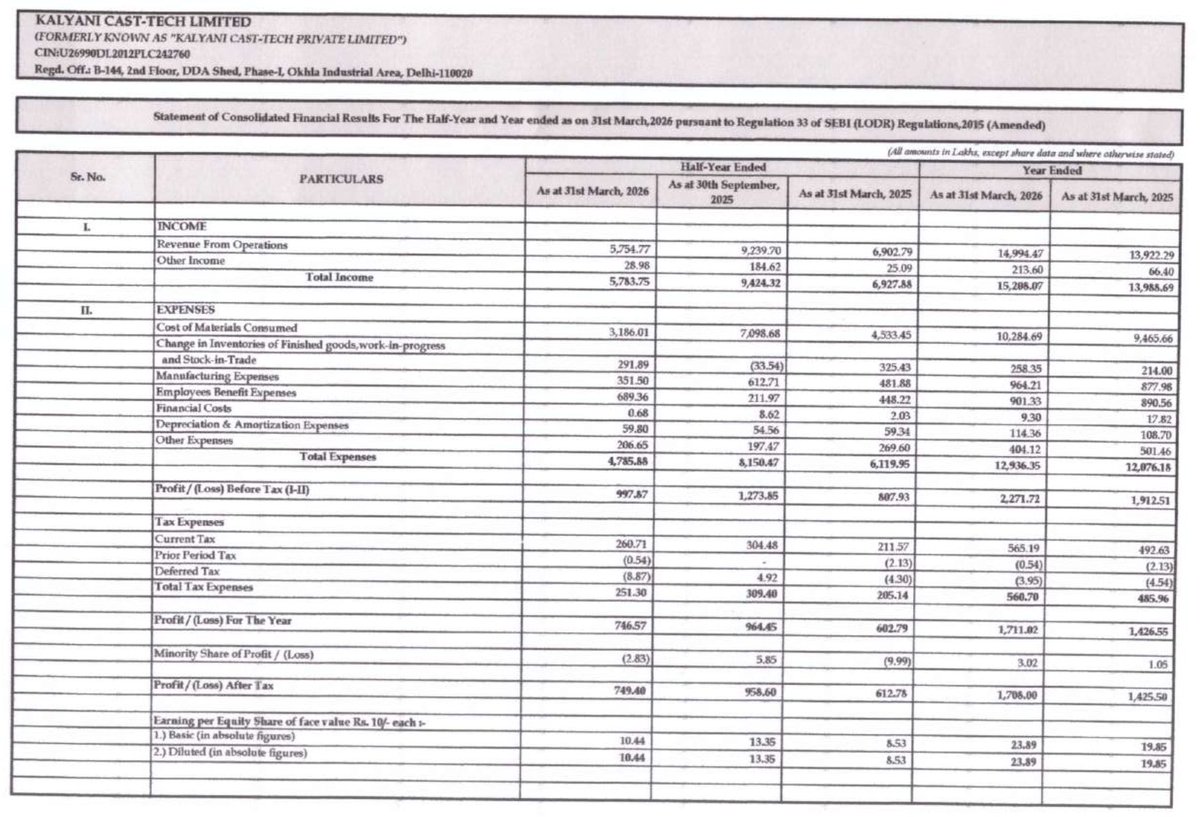

9. Kalyani Cast Tech- 5.75%

-

10. Parth Electricals- 2.30%

11. Sugs Lloyd - 1.64%

12. Kernex Microsystems - 1.30%

-

😵💫Regretting of selling E2E to buy more Cosmic CRF. I wanted to buy it again next day but couldn't do it because of continued UC. Missed opportunity despite having strong biases.

⚡I want to add Parth Electricals but despite of mediocre results, the stock is rising continuously. Couldn't add more.

🚂Very bullish on Kalyani Cast-Tech and Cosmic CRF. Kalyani might not do so well in H1 but it should do well H2 onwards. Happy to hold on. Looking forward to participation of both in the upcoming wagon tenders.

◻️GSM Foils, Akiko - both are giving fantastic sales numbers every month. Expecting a great year for both, in terms of topline growth.

🤖 Expecting, Oriana should do well in both H1 and H2.

-

Will read these businesses- Blue water, CFF fluid, Knowledge Marine, Omnitex.

-

⚠️ Disclaimer: This is personal portfolio journal shared for transparency only. It is not a buy/sell recommendation or investment advice. My holdings and views might change after this post.

📊 Portfolio Update: April'2026

(Mainboard 18%, SME 82%)

-

1️⃣ Oriana Power - 25.50%

2️⃣ Quality Power - 16.80%

3️⃣ GSM Foils - 12.35%

4️⃣ Felix Industries - 8.80%

5️⃣ Viviana Power - 8.75%

-

6. Aimtron Electronics- 6.35%

7. Cosmic CRF - 6.20%

8. Akiko Global - 5.00%

9. Kalyani Cast Tech- 2.30%

-

10. Sugs Lloyd - 1.90%

11. Sunita Tools - 1.90%

12. Parth Electricals- 1.85%

13. E2E - 1.30%

14. Rajesh Power - 1.30%

-

➕Added more Aimtron post results. Will buy more if the stock price falls below ₹1100 level. The growth projection, sector tailwind, below 1 PEG valuation make it attractive at that level.

➕Added E2E for long term holding. Valuation seems good. Not so expensive on forward EV/EBITDA basis.

-

⚠️Disclaimer: Please don't buy or sell shares based on my portfolio stocks. Please do your due diligence before investing.

4

5

43

8,907

Sunit | Stock market kid retweeted

Very Few Leaders in India have such scriptural clarity!

111

3,520

12,455

104,767

Re-rating of Viviana Power will be a rewarding journey🤞🏻

3

22

2,170

#E2ERAIL #SME 🧵 Why did Mukul Agrawal take 13.94% in this Rail engineering system integrator company?

This isn't a random SME bet. Here's the full thesis 👇

NOVA's RDSO CCA Approval (May 15, 2026)

E2E's subsidiary NOVA Control Tecnologix just received Concept Clearance from RDSO for Kavach development.

This makes NOVA eligible for:

→ Prototype submission

→ Field trial orders (expected H1 FY27)

→ Full commercialisation from FY29

Kavach revenue guided: ₹150–200cr in FY29 at 30–40% product margins.

This is not an EPC stock. It's becoming an OEM.

3

9

29

3,277

Sunit | Stock market kid retweeted

Jun 11

To understand the depth and breadth of what Prime Minister Modi has achieved, we must remember what he inherited.

The Congress Party had a disastrous flirtation with Soviet style socialism (and the word "socialist" is still there in our Constitution, thanks to Indira Gandhi). With the Soviet collapse, India faced bankruptcy and the Congress switched to the Washington consensus, Davos-style globalism. To be fair to them, it looked reasonable in 1991, and people like me supported it, but far deeper thinkers like Gurumurthy saw that Davos globalism also as a dead-end. It met its end in the Global Financial Crisis 2008-9.

Modi's Swadeshi philosophy has achieved the balance of building up our capability while also earning the respect of the world. Like all great transformations, it takes time.

My prayers for his good health because so much work lies ahead 🙏

504

1,700

8,241

223,838

Sunit | Stock market kid retweeted

Jun 10

The Indian Air Force congratulates the entire team behind the successful maiden flight of the first India-made C-295.

The achievement reinforces India's growing aerospace capabilities and underscores the Indian Air Force commitment to fostering indigenous defence capability under the vision of Atmanirbhar Bharat.

#C295 #MakeInIndia #AtmanirbharBharat #IAF #IndianAirForce

@PMOIndia

@rajnathsingh

@DefenceMinIndia

@SpokespersonMoD

@HQ_IDS_India

@adgpi

@CareerinIAF

@Indiannavy

58

502

3,483

83,075

Sunit | Stock market kid retweeted

Jun 10

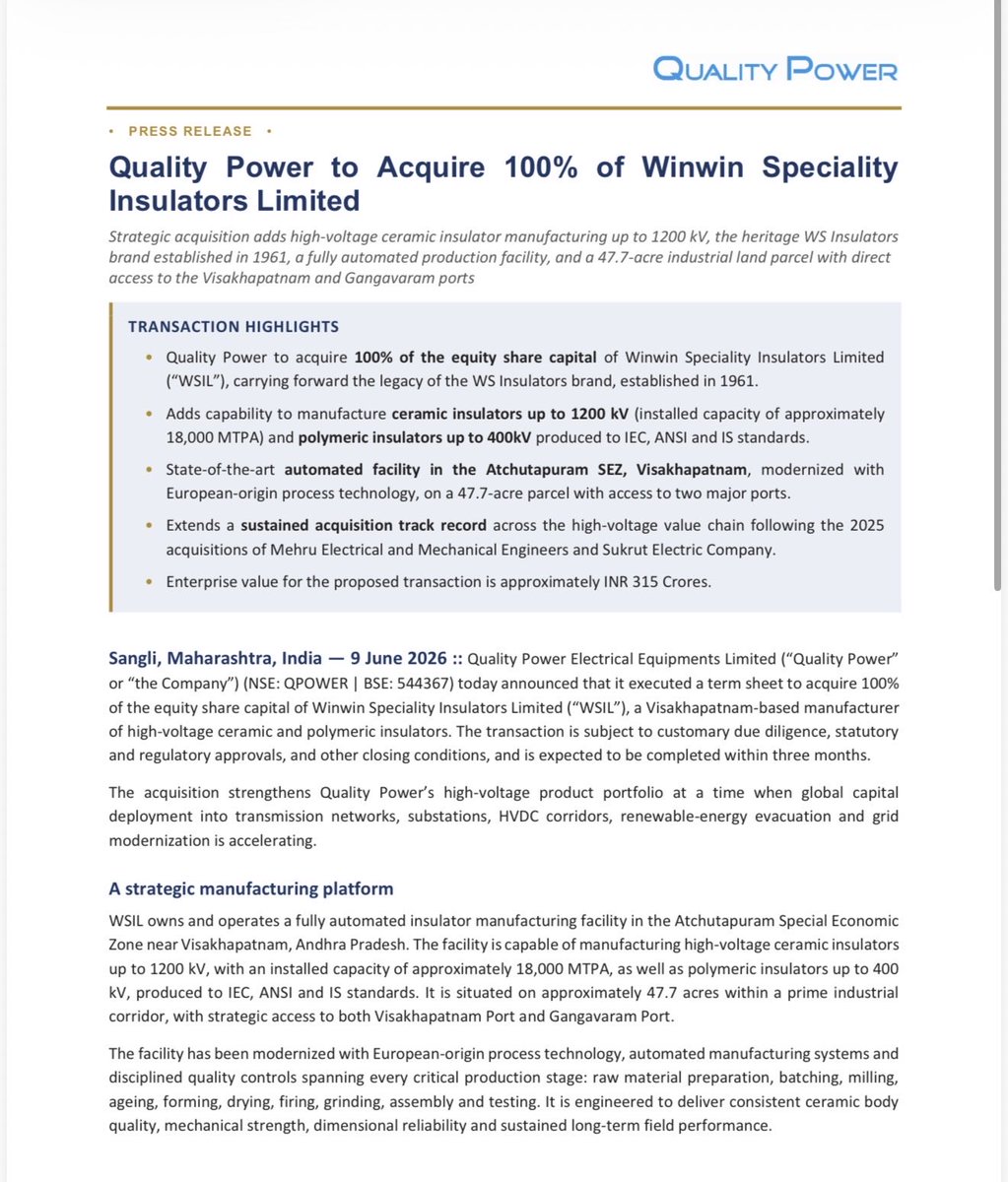

Quality Power to Acquire 100% of Winwin Speciality Insulators Limited for a consideration of 315 Crores

Transaction Highlights:

▪︎ Capability to manufacture ceramic insulators up to 1200 kV (installed capacity of ~18,000 MTPA) and Polymeric insulators up to 400kV produced to IEC, ANSI and IS standards.

▪︎ Fully automated facility in the Atchutapuram SEZ, Visakhapatnam, modernized with European-origin process technology, on a 47.7-acre parcel with access to two major ports.

The acquisition strengthens Quality Power’s high-voltage product portfolio at a time when global capital deployment into transmission networks, substations, HVDC corridors, renewable-energy evacuation and grid modernization is accelerating

This development comes at the times when whole industry is struggling to get Insulators and there’s a shortage globally!

Long way to go 🚀

The 4th (last) image attached below has link for the corporate video and factory tour of WinWin

Disc: Invested and Biased

2

9

116

11,490

Sunit | Stock market kid retweeted

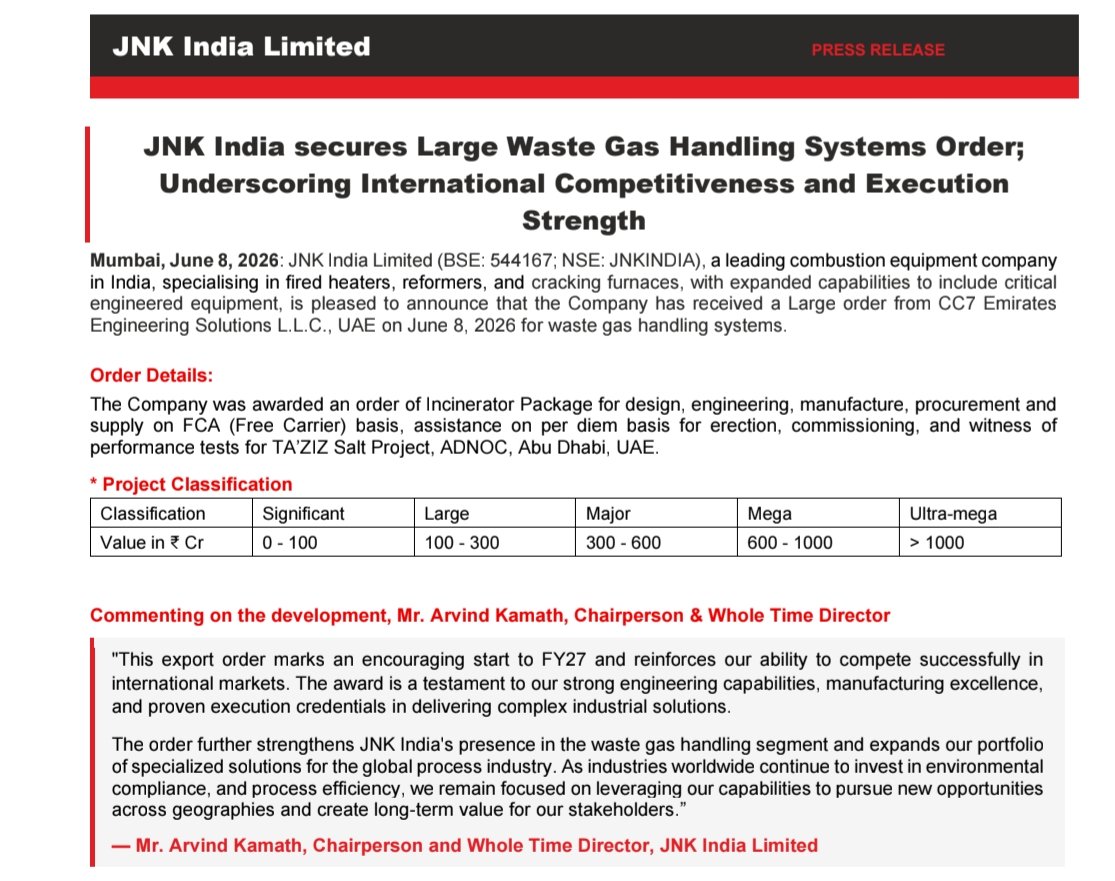

Jun 8

JNK India

#JNKIndia

100-300cr order(Large)

Large waste gas handling systems from CC7 Emirates Engineering Solutions,UAE

International order

Orderbook reaches 2100-2200cr now with this addition providing good visibility for FY27 and FY28

Additional orders from the bid pipeline, if gets converted provides upside visibility to the numbers

4

20

226

22,882

India have zero economic leverage against China in case of any military conflict.

Around 75% of oil import and 60% of total export of China go through Strait of Malacca.

Having a strong military and surveillance in the Nicobar would force China to rethink hundred time before doing any military misadventures.

Plus the 14.2 m TEU transshipment terminal, greenfield international airport, 450 MVA gas-solar power plant, and township- would give India economic boost.

-

Undeniably there will be big ecological disaster in that particular area. But, let's be honest, did USA, Russia, Israel, China ever think about ecology before attacking any country? This is the bitter truth.

India have never been and will never be an aggressor. All military measures we take are solely to defend ourselves.

This project is the only chance for India putting China in a massive strategic disadvantage.

-

HOPE WE BUILD IT ASAP. Jai Hind 🇮🇳

Under the Great Nicobar Islands development projects, India has plans to invest Rs 13,000 crore to build an airport and runway for use by both the Indian Navy and civilians. The project is expected to be completed in five years, and the budget will be shared by both the Defence Ministry and the Ministry of Civil Aviation: Defence Ministry Sources

9

1,126

Amazing 🤩

Jun 8

Look at this beauty of Indian Railways!

One double-stack container train can replace around 200 trucks on the road.

Cheaper, cleaner, and far more efficient.

1

15

2,562

Sunit | Stock market kid retweeted

Jun 6

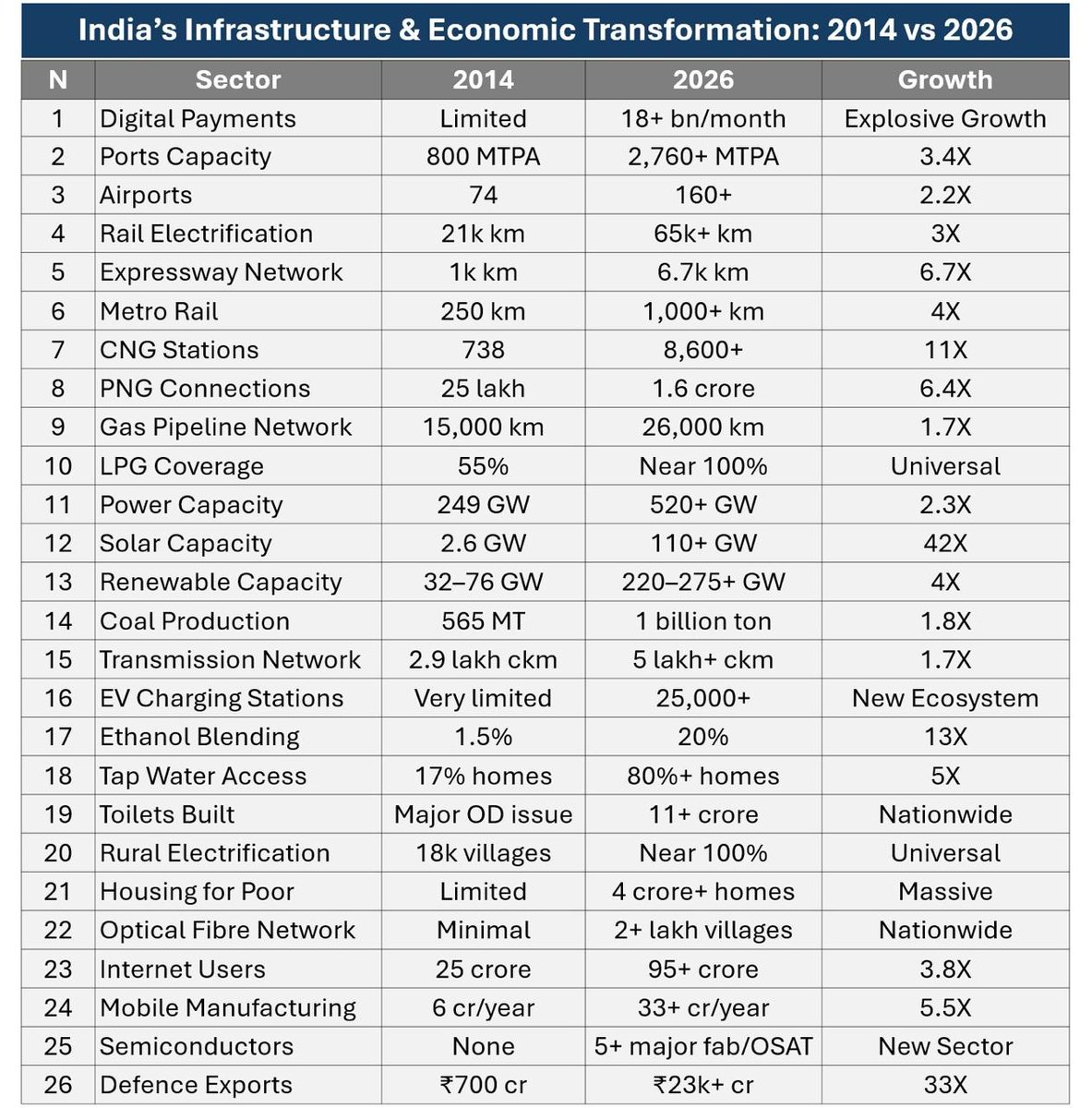

What has changed in India in last 12 years.....

550

4,308

12,340

1,000,696

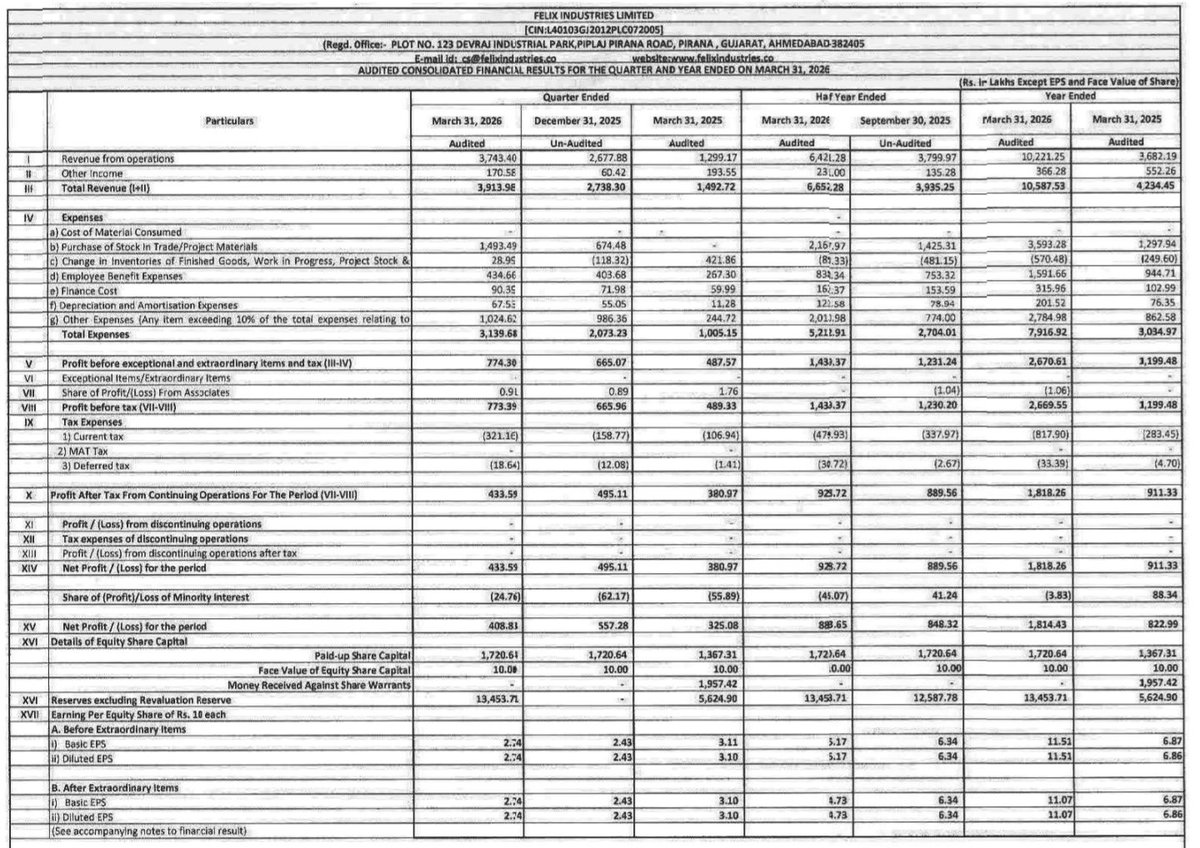

♻️Detailed summary of the concall of #Felix Industries.

Jun 6

#SME #Felix #FelixIndustries

Felix Industries Q4 & FY26 Earnings Call Highlights

👉 FY27 & Future Outlook:

▫️ Consolidated revenue guidance for FY27 maintained at ~180-200 Cr (standalone subsidiaries including Oman, WMC, Rivita, metal recycling & others)

💠Driven by full utilization of existing capacities, new recurring contracts and ramp-up across verticals.

💠 Oil processing (Oman India) expected at 60-70 Cr this year with current 40 TPD capacity at near 100% utilization in next 3-6 months; longer-term target 100 TPD via incremental expansions as feedstock improves.

💠 Metal recycling to contribute 40-50 Cr in FY27, scaling to 100-125 Cr with 20-25 Cr additional capex; acid reclamation and plastic recycling to add further momentum.

💠 EBITDA margins stable at 30-31% (including other income)

💠PAT margins 17-20%.

💠Q4 margin dip (to ~12% PAT) attributed to manpower expansion, project overheads (CETP) and higher interest on working capital utilization — not a structural shift

💠Oil ramp-up, utilization & revenue math (40 TPD → 60-70 Cr FY27, then 100 TPD)

💠Metal recycling scale, margins (15-20% EBITDA, 12-14% PAT) & expansion capex

💠 Recurring revenue (O&M, BOO, BOOT) mix to rise sharply

💠EPC to shrink proportionally over next few years as projects convert to long-term annuity models.

💠 Oman normalization post geo-political slowdown; Middle East (Saudi/UAE refineries) discussions ongoing but focus remains on maximizing current facilities first.

💠 Medium-term (FY28-FY30) aspirational trajectory: next “landmark” year post-FY27 growth

👉 Current Order Book / Projects and Future Pipeline:

▫️ Visibility from secured long-duration BOO/BOOT/O&M contracts (up to 10 years) across industrial, food, steel, oil & gas sectors.

💠 Oil processing: existing orders already ensure 100% utilization of 40 TPD in FY27; additional sizable contracts expected to trigger capacity addition toward 100 TPD target.

💠 Metal recycling: unit acquired, retrofits complete by month-end; commercial operations from next month; 4 TPD processing capacity for zinc/copper sulphate (magnesium also possible); one PO-stage order of ~15 Cr 15-20 Cr under discussion.

💠 CETP project (common effluent treatment plant with equity stake): ~70% complete, balance 20 Cr EPC revenue in FY27; O&M to start post-September at ~1 Cr/month (~12 Cr annualized).

💠 Plastic recycling & water verticals: current Gujarat facilities fully loaded with feedstock; focus on debottlenecking and utilization before new geographies.

💠 Pipeline: multiple under-discussion orders (water, waste oil, metal); Rivita Solutions approvals now in place for water recycle projects; acid reclamation MOUs advancing; more than enough demand but selective intake to protect execution quality.

💠 International: Oman operations back on track with orders in hand; incremental Middle East opportunities being evaluated only after current facilities hit peak performance.

👉 Other Notable Points:

▫️ Balance sheet insights:

💠Debt-equity comfortable; working capital cycle optimization targeted in FY27 via better subsidiary alignment, LC-backed corporate orders and mobilization advances (government projects remain 90-120 days).

💠Current bank debt ~21 Cr (India) expected to rise to 35-40 Cr 20-25 Cr in Oman for growth — total addition ~40 Cr, fully serviceable via operating cash flows.

💠 Promoter pledge to be reduced progressively; authorized capital increased to 40 Cr as preparatory step for mainboard migration (no equity raise planned).

💠 Business Model Shift: Continued emphasis on converting EPC → BOO/BOOT/O&M for recurring, high-visibility cash flows and optimized working capital. Zero Liquid Discharge (ZLD), circular economy and resource recovery remain core.

▫️ ESG & Capacity Snapshot:

💠17 MLD wastewater, 40 TPD waste oil (target 100 TPD), 50 TPD hazardous waste, 100 projects delivered; operations in India & Oman; subsidiaries driving metal recycling, oil & gas tech, acid reclamation.

▫️Migration to NSE Mainboard: Targeted in next 5-6 months; enhancing visibility, liquidity and institutional participation.

▫️Manpower & Risks:

💠Headcount scaling with fresh engineers and vertical-specific teams; skilled manpower remains industry-wide challenge but not a current bottleneck.

💠No major risks flagged; liquidity and geo-political normalization being actively managed.

1

7

1,539

#Railway Wagons

Railway wagons current capacity 3 lakh wagons, government expansion plan to 6 lakh wagons.

Tenders for 1 lakh wagons order to be floated in next 2-3 months🚂

I found some video on wagons opportunity,

youtu.be/_ob1j_tCdfI?si=9_ar…

1

17

2,347

Sunit | Stock market kid retweeted

Real GDP has been estimated to grow by 7.7% in FY 2025-26 (PE)

Real GVA has grown by 7.9% in FY 2025-26. (PE)

Real GDP and Real GVA have been estimated to grow by 7.8% and 7.9%, respectively, in Q4 of FY 2025-26. (PE)

Notably, Manufacturing, Trade, Repair, Hotels, Transport, Communication & Services related to Broadcasting, Storage and Financial, Real Estate & Professional Services sectors have attained double-digit growth at both Constant and Current Prices in FY 2025-26.

Our government led by Hon'ble PM Shri @narendramodi is committed to further drive the 'Reform Express' with decisive policy measures to ensure positive economic momentum amidst the global challenges.

Read more: pib.gov.in/PressReleasePage.…

459

456

1,883

94,240

Curiously looking forward to see how this huge development on Green Hydrogen unfolds.

Oriana Power- starting from FY27, is targeting an overall capacity of 100 KTPA of green hydrogen and 1 Million Tons per annum of e-fuels ( G. Ammonia) by 2030.

-

Dis: invested

Jun 5

8,000 tonnes. That's India's total green hydrogen production right now. Target is 5 million tonnes by 2030. We're 0.16% of the way there with 4 years left.

Every project review I've sat in, there's a moment where someone puts the real numbers on a whiteboard and the room goes quiet. Green hydrogen is at that moment nationally. The ambition is right. The math is terrifying.

2

12

2,415

Sunit | Stock market kid retweeted

Jun 5

FY26 GDP: 7.7%. Q4 alone: 7.8%.

Against genuine global headwinds, the Indian economy outperformed every cautious forecast.

That’s true resilience.

But the RBI, just this morning projected 6.6% for FY27. That’s not pessimism. Only a realistic reading of what crude prices, monsoon uncertainty, and West Asia tensions could do to momentum.

So in summary, we’ve earned the right to feel good about last year.

But the danger is in being complacent.

Because the world isn’t getting any less complicated.

Back to work…

234

948

4,422

98,531

Sunit | Stock market kid retweeted

What you see behind PM Modi is a 700 MW nuclear steam generator, indigenously manufactured in India.

Only a handful of countries can manufacture these at scale.

For a nuclear engineer, this photograph is actually more impressive than most missile or aircraft photos. It represents industrial capability at its finest. ⚛️

84

2,024

9,714

185,493

Sunit | Stock market kid retweeted

Jun 5

vTitan medical equipment update: we have been shipping steadily and a big shipment of syringe pumps is getting ready at the factory!

We also have an affordable pump for Thalassemia (vTitan AccuFlow Thala pump) and over a thousand patients have benefited from it.

Our R&D team is working hard on many more products. Our particular focus is on affordability.

vTitan is teaching us a lot about hardware design and manufacturing.

100

590

3,378

127,597

Kalyani Cast-Tech started despatching containers from their new factory-

11

1,481

Sunit | Stock market kid retweeted

Jun 4

You want the young officer to sacrifice his life for the love of the Nation, but you don’t want him to express his love for his fiancée.

In the Army we say ‘Youngster nahi karega, toh kaun karega’.

If you can not find a fault in his professional capabilities, don’t do this nuktachini for such a pure gesture of love and belonging.

Military equipment has been on display during many ‘Know your Army’ exhibitions around the country. The students and non military personnel have clicked pics with it showing pride and love for the Army. So, please don’t bring in the national security angle into this.

Let the young soldier do his national duty with pride and honour 👍

Jai Hind 🇮🇳

1,410

4,857

30,435

850,938