Speculator 🔮🧞

Joined October 2025

- Tweets 353

- Following 16

- Followers 129

- Likes 290

43 Photos and videos

Pinned Tweet

24 Oct 2025

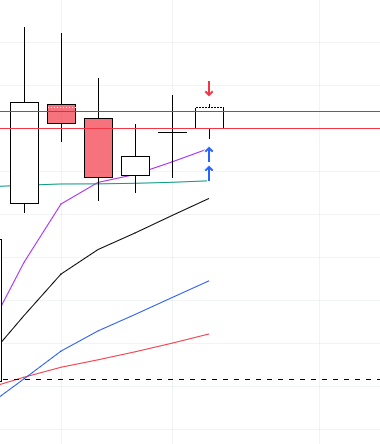

it's not about pattern what make money , it's always flow of liquidity which make money

study where money is flowing --kq

theme / hot group / earning > tight pattern >relative strength > position size > entry > trade management tactic

3

6

1,877

i think india have its bigger theme now

datacable & datacentre stock -AI proxy

energy -- future crises prepareation

finance -- fii ko kiase laaye vaapas

this is i think theme is now for india

in mean time there will be sector will come and go but it is theme now

2

2

167

Recnt FM interview tell clearly inida is finally wake up

and it will make all necessery step in urgent to catch the next wave even we miss first wave of some trend

which is clearly very very good sign now

1

61

This is key to growth

if you see oportunity bet big

man contra bet many time test your pateince

but you have to bet when you see extraordinary opportunity regardless of result

result are in hand of god and elder blessing --RJ

3

92

Jun 13

anticipation give best R:R but at cost of low win rate

where breakout give high win rate

i am willing to sacrifice some part of both to find sweet spot

it rquire SA & A setup

still working on this

i am very good at mean reversion

but if i find sweet spot then 🔥🚀

1

1

155

Jun 12

time for this week top 100 stock study post mortem

this is now tonight plan

let see what this week teach

1

1

8

684

Jun 12

look if you take leverege

remeber it work both side

always hedge your leverege position

i have seen many people go bankcoroupt beacuse they take leverege without hedge

never risk more then what you earn in any trade

single double is key to finance few big risky trade

1

165

Jun 12

is it exact time for swing start

time to press gas pedal now

time will tell

79

Jun 12

don't rush at open to buy seeing gap-up

wait few minute like first 15/30 min

then take ORB as entry

gap-up kill risk reward

7

280

Jun 11

world best trader investor

still no body come close to his compounding return

1

119

Jun 11

never excited for book but exited for this one

just because of @Qullamaggie story is present

Market Wizards new book

night is set for this 😄

1

121

Hari retweeted

With the IPO of SpaceX set to hit the market tomorrow, this would be a good time to take a look at some of the largest IPOs in prior massive bull markets. Though nothing in history other than maybe Saudi Aramco’s 2019 IPO can even come close to the relative size of the SpaceX IPO, there are still lessons to be learned from the market’s history.

NCR

100 years, six months, and six days ago, the largest IPO of the Roaring Twenties hit the market. National Cash Register, a manufacturer of cash registers and other accounting and business machines, sold its shares to the public at $50/share, valuing the company around $75M. The largest company at the time, AT&T, was worth a little under $3B.

NCR was most similar to IBM at the time as both companies manufactured and sold business machines. Both companies grew during the decade primarily due to the general growth in business and the growing need for accounting and money management solutions.

The timing of the IPO was classic. The market had been running hot for months. NCR listed right as the automobile group was going parabolic, and just before the Federal reserve raised the rediscount rate by 50 bps. The entire market took a nose dive. High-flying stocks like Chrysler and Hudson Motors cratered. Chrysler fell over 50% from its late 1925 peak. Hudson imploded 70%. The baking stocks, which had experienced their own boom in the prior year, began their long, inglorious demise. General Baking Company went down 75% in a straight line. Continental Baking followed suit.

NCR immediately began to sink within hours of its listing. It fell in lock step with the rest of the market, losing about 30% between January and May of 1926. It ended up trading in a large IPO base for its first two years on the exchange, mostly on low volume. After breaking out of its base in early 1928, it became one of the more liquid speculative favorites in early 1929.

Although its trough to peak move was only about 350%, that was at a time when most traders were using up to 10-1 margin. For a trader who captured just a 10% gain in a stock, it could have been equivalent to a 100% position gain. But after reaching a high of over $140 in 1929, it would fall to just $5 in 1933 — a loss of over 95%. However, by the time of the computer revolution in the 1960s, NCR would be a manufacturer of computers, and one of the “seven dwarves” that competed with IBM in the early commercial computing industry. Between 1950-1961, it would rise 2,500% amid the boom in computing.

LU

70 years after NCR went public, one of the largest IPOs of the dotcom era hit the market. Lucent Technologies, LU, came onto the stock exchange valued at around $15B in April of 1996 after raising, a then record amount, of $3B. It was, at the time of listing, the largest IPO in history. For reference, General Electric was the largest company in the market with a market cap of roughly $200B. LU was a large company, but nowhere near one of the largest. At its peak a few years later, it was the world’s largest telecommunications company.

It was spun out of AT&T’s telecom infrastructure business. It sold optical/fiber gear, wireless infrastructure, corporate networking and communications equipment, and it even had a semiconductor arm. It was a retail favorite internet infrastructure play throughout the dotcom bubble.

LU’s entrance into the market was very different than that of NCR 70 years earlier. LU rose steadily through early 1998 when it fell vertically by about 50% amid the Russian ruble crisis and fallout from the Asian Financial Crisis.

The trough to peak move on LU was about 1,000% between 1996 and 1999, before imploding 99% to just $0.60 by 2002.

X

While not technically an IPO, US Steel made its debut in 1901 after being organized as a consolidation between several leading steel companies. When it began trading on the NYSE, it had a market capitalization of around $1B, making it the largest company in the world, and the first to reach a billion-dollar valuation.

Again, X had classic timing. When it debuted, the market had been in the largest raging bull market in its history for the prior four years. Steel, iron, railroads, and other industrial stocks were making huge gains. Brooklyn Rapid Transit, nearly 2,000%. New York Air Brake, 1,500%. Missouri Pacific, 1,100%. Atchison, Topeka, & Santa Fe, 1,000%. Colorado Fuel & Iron, 700%.

X began trading just 33 trading days before the Panic of 1901 effectively brought a close to the great bull market that began in 1897. After rising less than 30% from its debut to its high, it had a complete unwind of 55% into the panic before quickly recovering, making a false breakout and breaking down once more. It would continue to decline until it reached $8 in 1904 when it would finally make its first real move of 360% into 1905 amid increased demand from the Russo-Japanese War.

$SPCX shares some similarities with these stocks, but it’s also a completely unique situation we’ve never really seen before. Many companies in the late 1890s were formed as giant trusts to consolidate entire industries just like US Steel was. The majority of those companies didn't make great moves until years later.

Only about 5% of SPCX will be floated on the exchange. Demand will likely be high. Supply will be low. Even at such a high valuation, it could be more volatile than the average trillion-dollar stock. It could rip out the gate. But the most likely scenario is that it will need to let out some air before it's really ready to make a tradeable move. But if there’s one thing the market has to teach us, it’s that anything could happen.

“The stock market is never obvious. It is designed to fool most of the people, most of the time.”

—Jesse Livermore

5

8

50

4,667

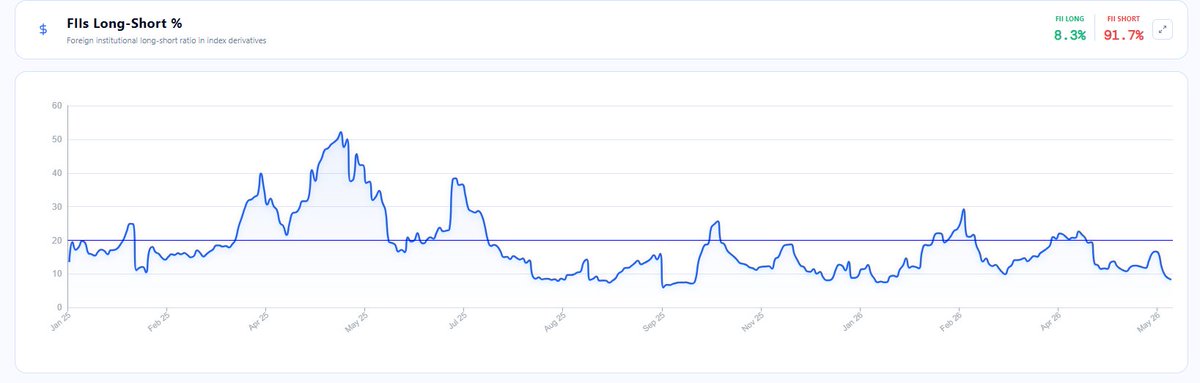

Jun 10

finally someone has spoken what i am thinking

clear fact no emotion

fii was almost 92.3 % short --extreme

why history will not repeat

Jun 10

FIIs are sitting with one of the highest index short positions in Indian market history ...nearly 2.7lakh contracts. History clearly shows that FIIs rarely continue aggressive shorting once positions reach this extreme zone. Whenever such stretched positioning appeared earlier, the market either consolidated for a few sessions or triggered sharp short-covering rallies.Previously, FIIs covered around 1.5 lakh contracts, and later across other index futures expiries (Midcap & Sensex) they again pushed shorts toward the 2.7 lakh zone for June series . Now Index again standing near an extreme short positioning level.

Remember: Markets don’t reverse when everyone is bullish. They reverse when positions become crowded and stretched.The chart is already speaking. Watch the marking carefully ... every time FII shorts peaked, Nifty moved up soon after. Alert: When positioning reaches extremes, the move that follows is usually fast and unexpected. Stay alert. The market may be preparing for something many are not ready for. #NIFTY #NIFTY50 #JustSaying

Chart Source @strike_ic

145

Jun 10

In investing, you need conviction. Your patience will be tested, but your conviction will be rewarded.

---RJ

sometime you are so contra in current situation

but you need to bet on what you think is right not other think what is right now

2

85

Hari retweeted

BREAKING: May CPI inflation rises to 4.2%, the highest level since April 2023.

Core CPI inflation also rises to 2.9%, the highest since September 2025.

Inflation in the US is officially back above 4% and more than double the Fed's target.

Odds of Fed rate hikes are rising.

494

1,472

8,060

2,772,681

Jun 10

short covering

what a beutiful concept

---8 out of 10 time it happen and end in similar way

history is very good guide

59

Hari retweeted

“Buy the first pullback after a new high, sell the first rally after a new low.” Linda Raschke:

9

119

887

62,888