286 Photos and videos

Pinned Tweet

I sold $META at $150. It hit $800.

I’ve held $MSFT since 2013. 400 shares at $28.16. Up 14x. Still holding.

Same investor. One difference.

I sold $AAPL at $142 too. Both ran. I missed both.

Same mistake twice. I owned great compounders, then let price noise talk me out of the business.

The difference was not luck. The two I sold, I never wrote down. The one I kept, I underwrote.

No written thesis. No IRR. No holding period. No journal.

So I built the thing I wish I had in 2013.

A fully transparent underwriting journal. $500 a week into hated, cash-rich businesses I can hold for 3, 5, 10 years. Before I buy: six gates, a written thesis, an IRR above my 18% hurdle. Posted before the outcome, not after.

Good or bad. Right or wrong. No hindsight edits.

I can’t delete the scoreboard.

The goal is not to call the next 500% move. It is to buy durable businesses, underwrite them well enough to hold through the pain, and make “never sell” the default until the business breaks.

Week 19 of 52 is live. The receipts are public.

1

990

I'll give you the part of my own thesis I'm least sure about. $BABA

The high margin is still a claim. Management says the intelligence layer earns more than the box, and honestly my whole valuation leans on that being true. But they haven't published the standalone number yet, and segment margin is still about 9%.

If that margin never shows up, this is a revenue story dressed as a profit story, and I overpaid in my model. So I watch cloud gross margin every single quarter. That's the line that settles it.

2

153

$NFLX has nearly round-tripped from the February lows. Back to ~$80 on a business that prints FCF, dominates global streaming, and has barely scratched advertising revenue.

Best entertainment compounder on the planet. Watching patiently.

1

2

132

Late 2020: $BABA at $320. Oct 2022: $BABA at $58.

80% drawdown from peak to trough.

At the bottom, the market was valuing the entire company at $140B with $40B in net cash and the #1 position in cloud, AI, and e-commerce in China.

The business kept generating cash the whole way down. FCF didn't break. The stock did.

The drop is what creates the IRR. No drop, no setup.

Gate 5: Pass. 9/10.

1

147

A Venmo user who routes a paycheck in earns $PYPL roughly 6x the revenue of a user who just splits dinner tabs.

Less than 5% of 100 million accounts have set up recurring funds-in.

The thesis is not adding users. It is the users they already own climbing the ladder.

2

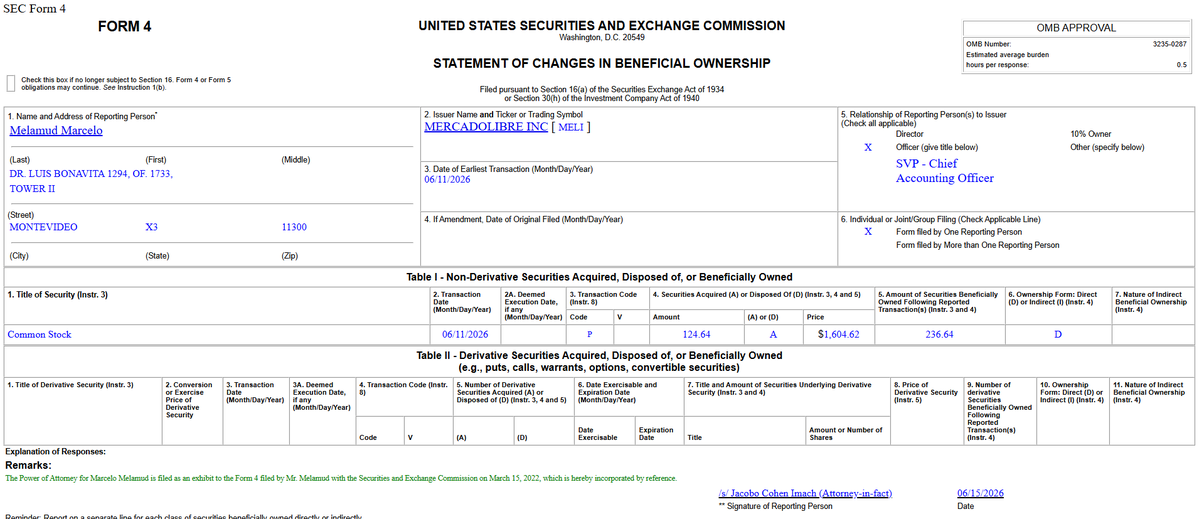

135

This is the line that made me sit up. On the May call management said they raised per-token prices and demand kept climbing. Customers are literally in a queue for access. $BABA

Raise the price, line gets longer. Commodities don't behave like that. Foreign frontier chips can't get into China reliably, the cost to build a new server has doubled in a year, and once an enterprise is on Alibaba Cloud there's nowhere obvious to go. That's pricing power hiding behind a growth headline.

8

174

$BABA is not a trade. Every time I've tried to trade it or buy options against it, it has punished me.

$70 to $90, then back to $80. $117, then back to $80. $145, then back to $95. $190, then back to $109.

The stock hands you unrealized gains, then takes them back. That's the filter if you want to be a long-term $BABA shareholder. It shakes out everyone who needs the return to be linear.

The arc it's drawing right now maps almost exactly to 2016 to 2020. After the $190 high in fall 2025, we entered the sideways chop phase. Two years of range-bound movement while the underlying business compounds in the background.

40% cloud growth. T-Head chips scaling inside the cloud infrastructure. MaaS margins beginning to appear on the income statement. Wu and Tsai are buying back stock and building the business simultaneously.

I'm not underwriting a price target. I'm underwriting a business that is building all five layers of China's AI stack, trading at half the multiple of its US comparable, with management that thinks in decades.

1

1

8

255

This is the tension I sit with on $DLO

The bear case isn't complicated. NFLX and AMZN move enormous volume. DLO needs them more than they need DLO, and that asymmetry shows up every time a contract renews. Take rates compress. Management is already on record saying the general trend is down. If that pressure compounds over ten years and the customer base never diversifies enough to change the dynamic, free cash flow never takes off the way the thesis requires.

That's the scenario that kills the return.

The bull case requires a different picture. Sixty countries. Existing local relationships. Compliance infrastructure built over years in markets where you can't just show up and process payments. Pedro Arnt said it plainly on the Q1 call: the bearish repricing thesis has been eliminated. What's left is a slow erosion managed through frontier market expansion and new product mix.

But the real question isn't whether take rates compress. They will. The question is whether DLO's customer base diversifies faster than the compression compounds.

I don't know the answer. Nobody does yet. If five years from now the top three merchants still represent the majority of TPV and none of the frontier market pipeline has materialized, the leverage never flips. The free cash flow story stalls.

What I believe: to replicate what DLO has built in 60 emerging markets, you don't just need capital. You need years of local banking relationships, regulatory licenses, FX infrastructure, and compliance frameworks built country by country. You cannot buy that overnight. Time is the real moat, not the technology.

Whether that's enough to flip the leverage equation is the grey area. I own the position. I'm watching the customer concentration numbers every quarter. That's the metric that settles the debate.

1

116

$BABA is sitting around $112. The 52-week range is $103 to $192.

So the stock is near its lows in the same stretch the cloud accelerated to 40% and management disclosed a new revenue line growing 10x. Read that twice.

And they're buying. Roughly 7 million shares repurchased for $815 million in a single quarter, management on record calling it undervalued. When the people with the most information are buying their own stock near the bottom of the range, I pay attention.

1

6

242

Week 20 of 52: this week's $500 goes to $BABA.

Cloud revenue: 26%, then 34%, then 35%, then 40%. Four consecutive quarters.

AI revenue posted triple-digit growth for 11 straight quarters. It now makes up 30% of external cloud revenue. Annualized run rate: $5.3 billion.

Margins held through all of it and are ready to move higher.

That’s the setup. The full Substack math write-up is below.

open.substack.com/pub/swissk…

4

204

Five words from the December call have been rattling around my head since. $BABA

"Shifting from selling resources to selling intelligence."

Renting a server means charging for the box. Capital heavy, price grinds to the floor, margins sit in the 30s. Serving a token means charging for the answer, and the answer is worth a lot more than what it costs to produce. The market is looking at 40% growth on a 9% margin and calling 9% the ceiling. It's the floor.

1

1

177

Server costs doubled at $BABA. Cloud margins were flat.

That's the setup. Stock is sitting at $112 after backfilling the July gap.

I've purchased it four times over three months. Adding again Monday.

4

230

The question everyone asks about $BABA Cloud is whether 40% growth can hold. Wrong question.

What matters is what's growing inside that 40%. AI product revenue is at a $5.3 billion run rate now, about 30% of external cloud, and management thinks it crosses half within a year. The low-margin box business is getting replaced by something that prices like software. That's the whole story and the headline number doesn't show it.

4

214

Most investors see the cloud number. The real money is a layer deeper.

$BABA just reported 40% cloud growth. Triple digit AI revenue for the 11th straight quarter. $5.3B annualized run rate.

That's not the thesis.

The MaaS layer compounding inside that growth is. I put a per-share number on it using management's own targets and showed exactly what the market is missing.

Full Substack write-up below: swissknifeinvestor.substack.…

9

289

Venmo looks like a way to pay your roommate.

It is actually how $PYPL acquires the next generation of high-income users without spending a dollar.

100 million young, affluent accounts. The most expensive problem in fintech, solved.

At $40 you are getting the customer acquisition machine for free.

1

3

211

People can’t get enough of the SpaceX IPO. I can’t get enough of $META below $560.

30% revenue growth. 17x earnings. A decade of ROIC in the high 20s. Zuckerberg is 42 and just getting started.

I’m investing for tomorrow, and tomorrow is 2030.

Ever tried to quit Instagram? My wife has deleted and re-downloaded the app more times than I care to count. That’s not a product. That’s a consumer habit. That habit creates the power of the network and the compounding machine.

While everyone chases SpaceX allocations, I’m digging through 10 years of $META earnings transcripts and hundreds of billions in free cash flow. Investors are paying $2.2T for a company that isn’t profitable yet. You’re pricing in asteroid belt mining on Day 1.

I’ll take the proven winner.

$META prints cash. SpaceX $SPCX prints hype.

1

144

Investors asking how $PYPL makes money on free money transfers is thinking about Venmo wrong.

P2P was never the business. P2P was distribution. The wedge that put 100 million people inside a PayPal-owned financial app and trained them to open it without thinking.

The habit is the asset. The monetization comes after.

3

159

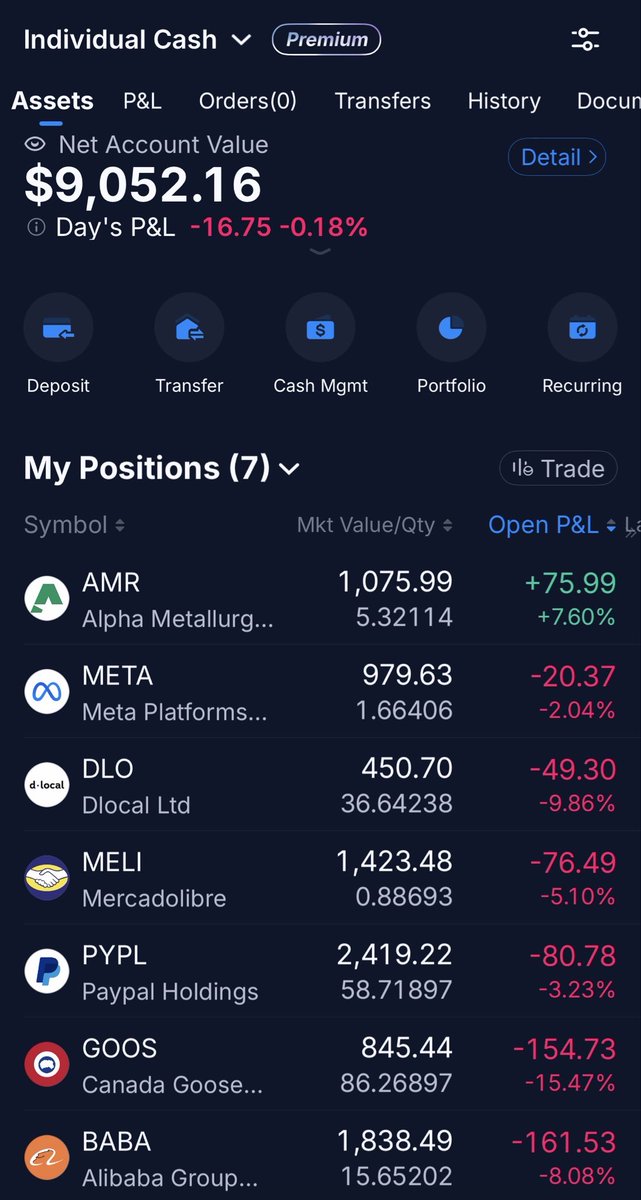

I’m down on 6 of 7 positions right now.

The one that’s green: $AMR. 6.8%.

Coal. Hated. Left for dead. Up while everything else bleeds.

The gates don’t promise you’ll be right immediately. They promise you’ll still be in the trade when you are.

Week 19. Scoreboard stays public.

158