Ex-Investment Banker | A Curious Learner | Views are personal and not recos.

Joined March 2026

- Tweets 128

- Following 271

- Followers 141

- Likes 226

59 Photos and videos

Pinned Tweet

Jun 1

HFCL ALL TGTs HIT - Up 130% since posted.

Apr 9

HFCL - TechnoFunda (TF) Playbook

Preform foray: HFCL has now approved a ₹580 crore preform manufacturing plant via subsidiary HFCL Technologies Pvt. Ltd.; planned capacity is ~300–310 MTPA, with commissioning targeted by July 2029.

Management had earlier said preform was a strategic backward-integration move to secure raw material for its fast-expanding optical fibre/OFC business.

Co. is targeting ₹3,500 cr OFC revenue in FY27.

Market size: The global fiber-optic preform market is estimated at US$12.4 billion by 2032.

Note: This is only for educational purposes and is not a buy/hold/sell recommendation.

6

816

13h

MOTISONS JEWELLERS - TF PLAYBOOK

The biggest trigger here is the ₹150 crore QIP allotment.

Motisons has allotted 13.57 crore equity shares at ₹11.05/share, raising ₹149.99 crore from qualified institutional buyers. The issue was priced at a 4.57% discount to the floor price of ₹11.58/share.

The interesting part is the investor mix.

Key allottees above 5% of the issue:

Pine Oak Global Fund - 2.26 crore shares, 16.67% of issue

Mint Focused Growth Fund PCC - Cell 1 - 2.26 crore shares, 16.67%

Saint Capital Fund - 2.26 crore shares / 16.67%

Nova Global Opportunities Fund PCC - Touchstone - 1.86 crore shares / 13.67%

Compact Structure Fund - 1.36 crore shares / 10.00%

Tiger Strategies Fund-I - 90.50 lakh shares / 6.67%

Together, these six investors took 80.33% of the entire QIP, which means the raise was highly concentrated among a few large institutional buyers.

ADD THIS TO YOUR WATCHLIST!

Note: This is only for educational purposes and is not a buy/hold/sell recommendation.

2

62

Jun 13

Commentary on Global Water treatment and Wastewater treatment Market opportunity from @vatechwabag Chairman & MD - Rajiv Mittal:

"This is the region which we are operating. And if you put all this together, this is almost 75 billion to 100 billion in next five to seven years is the opportunity"

1

17

Jun 13

A bit intrusive and controversial thought: This looks more like a marketing stunt to me at a broader level because if I think from the first principles or second order - Why would Anthropic release such a model which is so powerful such that it questions the national security of a geography, of course they would know the implications and consequences of such a model then why release only to get banned later?

And I’m sure that these guys would obviously be doing the basic sanity check before releasing model to the world.

Jun 13

The US government, citing national security authorities, has issued an export control directive to suspend all access to Fable 5 and Mythos 5 by any foreign national, whether inside or outside the United States, including foreign national Anthropic employees.

The net effect of this order is that we must abruptly disable Fable 5 and Mythos 5 for all our customers to ensure compliance.

Access to all other Claude models is not affected.

We apologize for this disruption to our customers. We believe this is a misunderstanding and are working to restore access as soon as possible.

Read our full statement: anthropic.com/news/fable-myt…

3

47

Harsh Pathak retweeted

Jun 12

World's First Trillionaire

962

1,747

12,501

489,012

Jun 12

Strong reversal in the markets today.

Let's see what the weekend brings us :)

Jun 11

The 2nd week of June has been worser than the certain weeks of Apr and May with the broader market showing clear signs of weakness as selling pressure continues.

Let's see how this week ends.

Data courtesy: @itsTarH

1

4

63

Jun 12

JAY BHARAT MARUTI - TF PLAYBOOK

Solid Q4FY26 Good QoQ and YoY uptick across all parameters

Rev at 766cr vs 610cr, Q3 at 645cr

PBT at 55cr vs 29cr, Q3 at 28cr

PAT at 80cr vs 21cr, Q3 at 18cr

The stock is not moving in isolation. One of the clearest fundamental triggers is the sharp recovery in Maruti Suzuki sales, which matters because this company sits directly in the Maruti ecosystem.

Maruti’s monthly sales trend has been strong:

Jan 2026: 236,963 units ( 11.6% YoY)

Feb 2026: 213,995 units ( 7.3% YoY)

Mar 2026: 225,251 units ( 16.7% YoY)

Apr 2026: 239,646 units ( 33.3% YoY)

May 2026: 242,688 units ( 34.8% YoY)

ADD THIS TO YOUR WATCHLIST!

Note: This is only for educational purposes and is not a buy/hold/sell recommendation.

3

181

Jun 11

Middle East – Leading the Global Desalination Movement

The Middle East is becoming the centre of the global desalination theme.

The reason is simple:

>> High water stress.

>> Limited freshwater availability.

>> Rising population and industrial demand.

>> Heavy dependence on desalinated water.

Regional desalination demand is expected to grow by ~62% by 2025. Today, ~63% of the region’s water demand is already met through desalination, while only ~31% of treated wastewater is reused.

That gap creates a major infrastructure opportunity.

>> Saudi Arabia is leading with a planned investment of USD 32 billion by 2027, including USD 12 billion through PPPs under Vision 2030.

>> UAE plans to invest USD 2.08 billion by 2027, focusing on ZLD and integrated water management under its Water Security Strategy 2036.

>> Qatar is targeting 70% reuse of treated water by 2030.

>> Kuwait already sources over 90% of freshwater through desalination and is allocating USD 1.5 billion for asset upgrades and reuse.

>> Bahrain aims to double desalination capacity by 2035.

>> Oman is expanding Independent Water Projects with a focus on renewables and brine management.

1

2

3

65

Jun 11

The 2nd week of June has been worser than the certain weeks of Apr and May with the broader market showing clear signs of weakness as selling pressure continues.

Let's see how this week ends.

Data courtesy: @itsTarH

2

148

Jun 11

BCL IND - TECHNOFUNDA PLAYBOOK

BCL Industries is quietly building a biofuel distillery growth story.

FY26 numbers were decent:

Revenue: ₹2,913 cr

EBITDA: ₹251 cr, up 18% YoY

PAT: ₹126 cr, up 23% YoY

EBITDA margin: 8.6%, up 130 bps

The real trigger is capacity.

BCL has commissioned its new 150 KLPD grain-based distillery at Rajpura, taking total distillery capacity to 900 KLPD.

Management expects ~75% utilization from Q2 and sees potential incremental revenue of ~₹300 cr at full utilization.

Another 250 KLPD expansion in Haryana is planned over the next ~2 years.

Now comes the strategic margin expansion....BCL meets 100% of steam and power needs through paddy straw boilers, giving it a structural cost advantage versus fuel-dependent peers.

Policy tailwinds also remain strong - India is moving beyond E20, with discussions around E30, E85, E100 and flex-fuel adoption.

ADD THIS TO YOUR WATCHLIST!

Note: This is only for educational purposes and is not a buy/hold/sell recommendation.

7

365

Jun 9

SOUTH INDIAN BANK - A STRONG PEAD AND PSU INDEX BREAKOUT CANDIDATE

NIFTY PSU BANK INDEX looks V V strong with respect to other indices.

Bank posted record profitability and stronger return ratios: FY26 net profit at INR 1,455cr ( 12% YoY). Profitability translated into RoA 1.03% / RoE 12.76% for FY26; Q4 RoA 1.17% / RoE 14.49%.

Management noted NIMs have improved ~15 bps over the last two quarters.

Deposits 15% YoY to INR1,23,346cr

CASA 17.5% YoY to INR39,621cr

Advances 14.5% YoY to INR1,00,274cr

GNPA down 177 bps from 3.2% to 1.43%

NNPA down 63 bps from 0.92% to 0.29%

ADD THIS TO YOUR WATCHLIST!

Note: This is only for educational purposes and is not a buy/hold/sell recommendation.

1

4

284

Jun 8

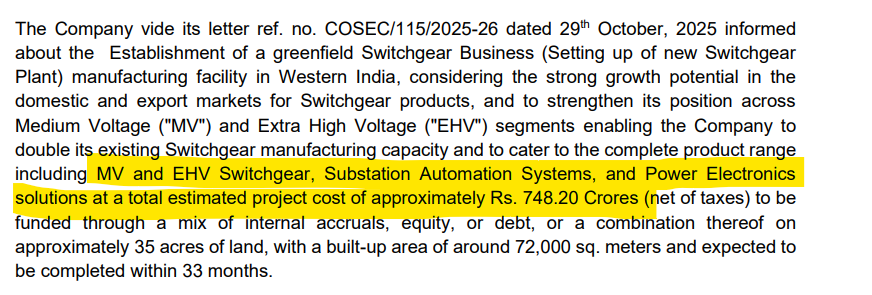

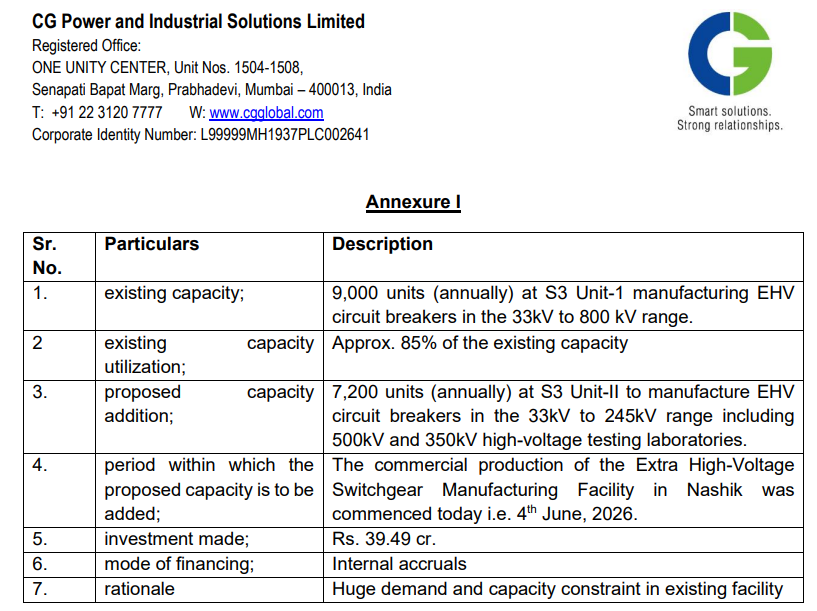

The Power Upcycle and grid capex is coming for real.

CG’s existing EHV circuit breaker capacity was 9,000 units annually and already running at ~85% utilisation.

It has now commissioned a new Nashik EHV unit adding 7,200 units annually, with ₹39.49 crore invested.

This is not a standalone expansion.

It sits inside a much larger ₹748.2 crore greenfield capex plan announced earlier.

The broader project is meant to double switchgear capacity across MV EHV, and also add substation automation and power electronics capabilities.

1

2

5

467

Jun 4

AVALON TECH - TECHNOFUNDA PLAYBOOK

Management stated: Best year to date; 7th consecutive quarter of growth.

FY26 revenue 46% YoY (vs 40% guidance) to ₹1,603 cr

Q4 revenue ₹480 cr ( 40% YoY, 14.9% QoQ)

Gross margin (GM): Q4 33.7%; FY26 34.3% (upper end of 33–35% guided)

EBITDA: Q4 ₹57 cr, 11.8% (vs 11.5% in Q3); FY26 ₹173 cr, 10.8% ( 50.9% YoY)

PAT: Q4 ₹41 cr, 8.4%; FY26 ₹113 cr, 6.9% ( 78% YoY)

ROCE 20.6% (vs 15.7% last year; “10% two years ago”)

Order book (near-term): ₹2,196 cr, 24.7% YoY, average execution ~14 months

Long-term contracted revenue: additional ₹1,245 cr with execution 15–36 months

Management guiding FY27 revenue growth guidance: 24–27%. They also doubled their guidance from ₹1,603 cr (FY26) to ~₹3,200 cr by FY29.

ADD THIS TO YOUR WATCHLIST!

Note: This is only for educational purposes and is not a buy/hold/sell recommendation.

2

132

Jun 4

SKM EGG PRODUCTS - TECHNOFUNDA PLAYBOOK

Management characterized FY26 as a record year driven by exports, mix, and operating leverage leading to outstanding results.

FY26 (YoY) financials (as stated):

Revenue: ₹767 Cr (vs ₹493 Cr, 58% YoY)

Operating profit: ₹162–163 Cr (vs ₹71 Cr)

PBT: ₹136 Cr (vs ₹47 Cr)

PAT: ₹102 Cr (vs ₹33 Cr) - “Management cited First time… crossing 100 crores"

Q4 FY26 (sequential comparison given vs prior year quarter):

Revenue: ₹197 Cr (vs ₹180 Cr) Operating profit: ~₹48 Cr PBT: ₹41 Cr (vs ₹9.7 Cr) PAT: ₹32 Cr (vs ₹6.22 Cr)

Margin Expansion:

Operating margin increased from ~14% to ~21% YoY

PAT margin shown improving from ~7% to ~13% YoY

TECHNICAL OUTLOOK:

Stock has recently entered stage 2 with explosive weekly volumes of Rs. 53.96 Cr and is a strong PEAD candidate.

ADD THIS TO YOUR WATCHLIST!

Note: This is only for educational purposes and is not a buy/hold/sell recommendation.

2

211

Jun 2

FCL TGT 1 HIT - 25%

May 19

Specialty Chemicals Stock - TechnoFunda Playbook

MCap: ~3845 Cr

PE: ~35.4

ROCE: ~18.3%

ROE: ~13.5%

This is not a normal re-rating setup.

A listed company that the market still mostly buckets as a small textile chemical player is trying to become something much bigger:

A global specialty chemicals platform with direct US oilfield exposure.

Management commentary has turned unusually aggressive.

“₹3,000 crore topline in 3–4 years would not surprise us.”

Against a current revenue base of around ₹772 crore, that is effectively a 4x growth ambition.

And the interesting part is this:

current utilization is still only around 60–62%.

Yet the numbers are already moving fast:

Revenue growth: 162% YoY

PAT growth: 118% YoY

Management has also repeatedly said:

“Q4 is the base.”

Because the current CCT run-rate is already around $90–100 million annualized.

The earlier target was $200 million by 2030.

Now management is saying that number can be achieved before FY28.

Guess the stock in the comments below👇 I know many of you will get it right :)

ADD THIS TO YOUR WATCHLIST!

Note: This is only for educational purposes and is not a buy/hold/sell recommendation.

3

263

May 27

MAX ESTATES - TECHNOFUNDA PLAYBOOK

MAX INDIA: ANTARA SENIOR CARE RECEIVES OCCUPANCY CERTIFICATE FOR NOIDA PROJECT

Antara Senior Care received partial Occupancy Certificate (OC) for Phase 1 of Noida Sector 150 senior living community

OC (OCCUPANCY CERTIFICATE) covers 3 towers and 340 residential units, paving way for resident possession

Around 340 senior families expected to receive possession of homes

OC unlocks nearly Rs. 150 Cr receivables linked to possession milestones

Entire project spans ~12 lakh sq ft, with Phase 1 accounting for ~7.45 lakh sq ft

Total revenue potential estimated at Rs. ~550 Cr for Phase 1 and Rs. ~800 Cr for Phase 2.

Due to the above news MAXINDIA (the company which looks after the Senior Care & living) was up 14% today!

ADD THIS TO YOUR WATCHLIST!

Note: This is only for educational purposes and is not a buy/hold/sell recommendation.

4

277

May 25

RAIN IND - TECHNOFUNDA PLAYBOOK

Rain Industries Limited (RAIN) is a leading vertically integrated producer of carbon, cement and Advanced materials products.

It is:

>> world's largest producer of CTP

>> world's second largest manufacturer of CPC

>> global leader in advanced materials

>> one of the leading grey cement manufacturers

Solid Q4FY26 result leading to strong PEAD:

>> Big QoQ and YoY uptick across all parameters

>> Rev at 4520cr vs 3768cr, last qtr at 4300cr

>> EBITDA at 690cr vs 380cr with OPM at 15.4% vs 10.1%

>> PBT at 256cr vs loss, last qtr at 66cr

>> PAT at 158cr vs loss,last qtr at 38cr

Led by volumes improvements in Calcination due to strong demand & higher production as compared to ramping up of Capacity utilization during Q1 2025 and Increased prices of CPC & CTP across all major products supported with appreciation of Euro and USD against Indian Rupee.

ADD THIS TO YOUR WATCHLIST!

Note: This is only for educational purposes and is not a buy/hold/sell recommendation.

9

1,685

May 22

RATEGAIN TECH - TECHNOFUNDA PLAYBOOK

Mcap: ~ 8551 Cr | PE: ~38.7 | ROCE ~13.7%C | ROE ~ 12%

VERY STRONG PEAD CANDIDATE DUE TO RESULTS:

YoY Performance (Mar ’26 vs Mar ’25):

Sales: ₹716 Cr (vs ₹261 Cr) ⇡ 174%

EBITDA: ₹147 Cr (vs ₹60.6 Cr) ⇡ 143%

Net Profit: ₹70.0 Cr (vs ₹54.8 Cr) ⇡ 28%

EPS: ₹5.92 (vs ₹4.64) ⇡ 28%

QoQ Performance (Mar ’26 vs Dec ’25):

Sales: ₹716 Cr (vs ₹540 Cr) ⇡ 33%

EBITDA: ₹147 Cr (vs ₹87.1 Cr) ⇡ 69%

Net Profit: ₹70.0 Cr (vs ₹26.4 Cr) ⇡ 165%

EPS: ₹5.92 (vs ₹2.24) ⇡ 164%

ADD THIS TO YOUR WATCHLIST!

Note: This is only for educational purposes and is not a buy/hold/sell recommendation.

5

589

Harsh Pathak retweeted

May 20

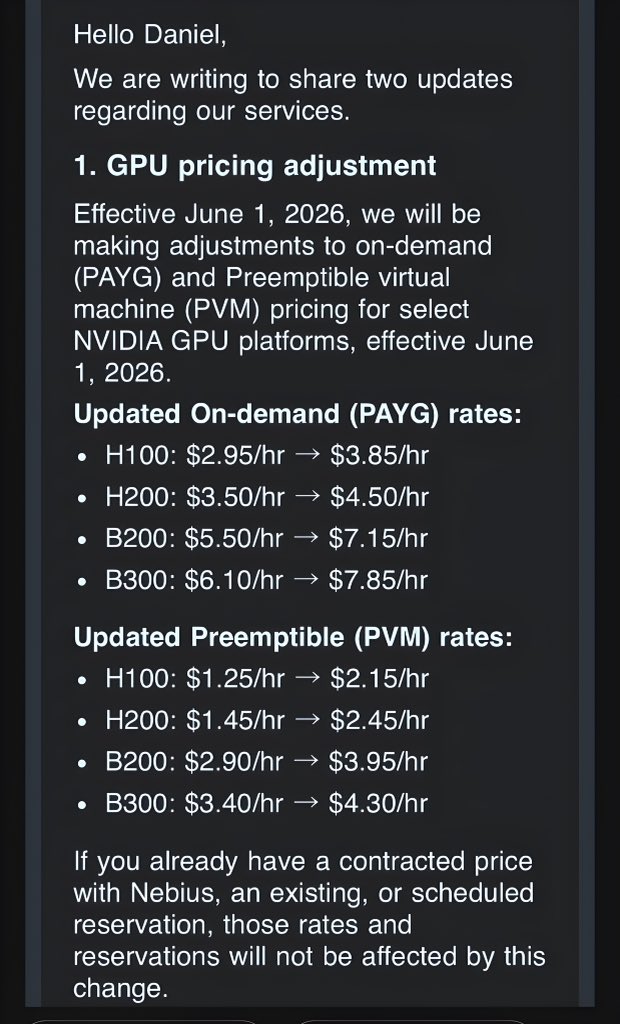

$NBIS increased GPU rental prices across the board starting in June

Blended price increase: 34%

The biggest increase was in H100 preemptible pricing, up 72%

7

13

171

47,481

May 21

Balaji Amines - TechnoFunda Playbook

Balaji Amines has commenced commercial production at its Dimethyl Ether (DME) plant in Solapur with 1,00,000 TPA capacity.

That matters because it makes the company the first DME manufacturer in India, in a product that can directly support import substitution and reduce dependence on LPG imports.

The second layer is the battery-chemicals optionality - Balaji has already upgraded its electronic-grade DMC plant, and DMC is a key electrolyte solvent used in EV batteries.

The company is currently the only DMC manufacturer in India, with 15,000 MTPA installed capacity.

Alongside that, it also makes electronic-grade TEA and electronic-grade NMP, both relevant to battery and electronic chemical applications.

Management’s pitch is clear: not just participate in future EV chemical demand, but become an early domestic supplier before the market scales up.

If the DME ramp-up starts showing numbers, the reversion-to-mean may happen in no time.

ADD THIS TO YOUR WATCHLIST!

Note: This is only for educational purposes and is not a buy/hold/sell recommendation.

2

7

545