Visionary investing in growth and dividend stocks plus traveling for fun. Over 1 million views on Google Maps of my travel photos. I'm not a financial adviser

Joined August 2018

- Tweets 213,213

- Following 5,656

- Followers 2,190

- Likes 164,205

253 Photos and videos

Growth Stocks Traveler retweeted

Jun 14

It’s National Strawberry Shortcake Day!

#NationalStrawberryShortcakeDay #Shortcake #StrawberryShortcakeDay

3

41

60

1,078

Growth Stocks Traveler retweeted

Jun 14

4

34

60

825

Growth Stocks Traveler retweeted

It's National New Mexico Day! I went to Santa Fe once, loved it and can't wait to go back! cozymystery.com/themes/trave…

5

9

212

Growth Stocks Traveler retweeted

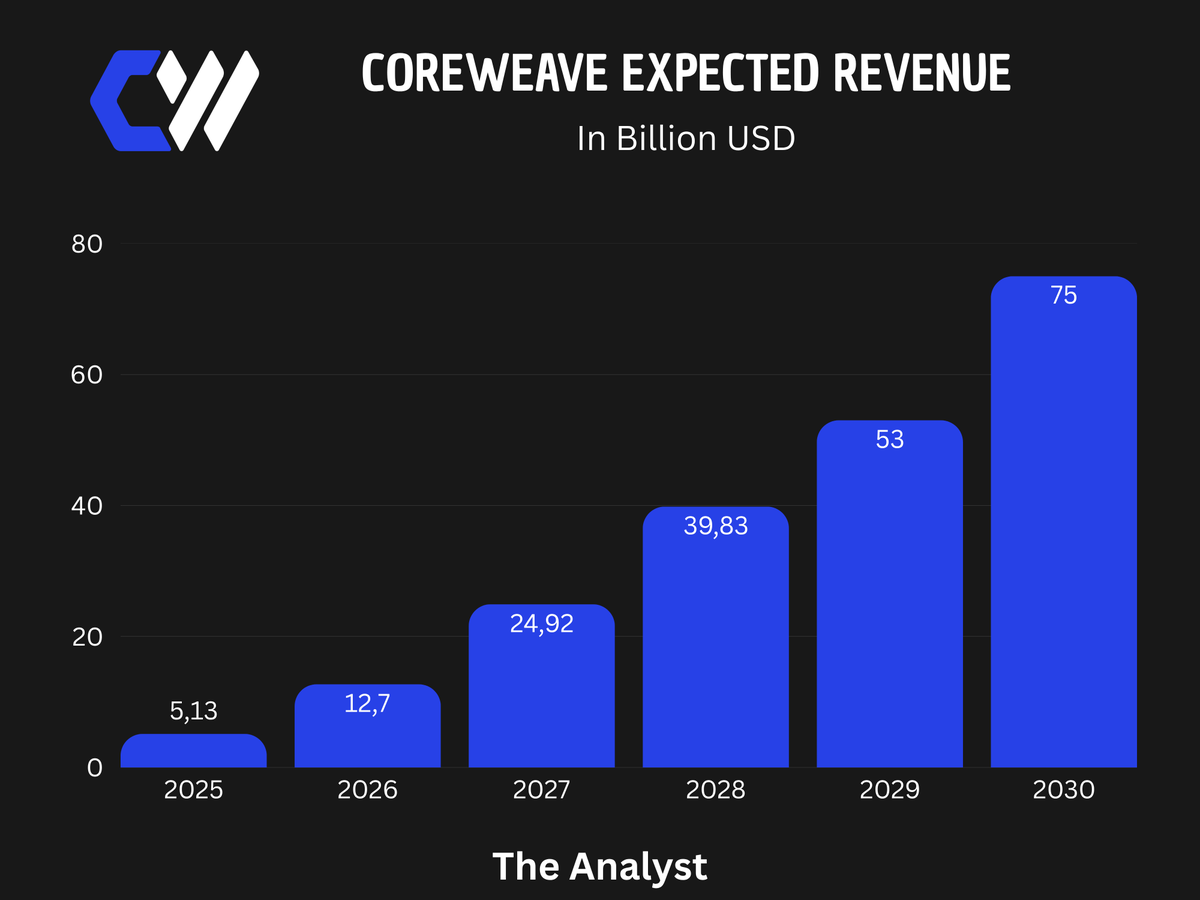

Jun 14

$CRWV is the most attractive buy amongst AI-Infrastructure companies.

And the math makes this reaally obvious:

Currently valued at $55B

Company expects to do $53B in revenue 2029 alone.

The demand remains huge.

Interest expenses will decline strongly over the next years.

The $NVDA partnership is making this a whole lot more attractive.

The reason this is so cheap now is most likely that $NBIS for a long time just seemed like the more attractive bet.

But $NBIS being valued more than $CRWV is just ridiculous.

To justify this valuation gap, $NBIS margins would need to remain more than twice of $CRWV's over the long-term.

Most likely not going to happen.

29

44

309

21,723

Growth Stocks Traveler retweeted

Largest Tech Companies in the world

29

93

3,637

Growth Stocks Traveler retweeted

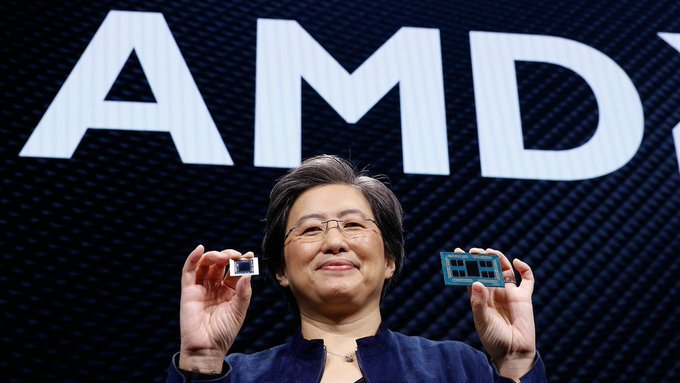

$AMD IS NOW WORTH OVER $900B FOR THE FIRST TIME EVER

May 6

$AMD is up over 15% today because this was the quarter where the market started reframing AMD from “the cheaper $NVDA alternative” into a true beneficiary of the next AI infrastructure phase where CPUs & GPUs both matter.

AMD has real shot at becoming a $1T company this year.

30

32

442

49,097

Growth Stocks Traveler retweeted

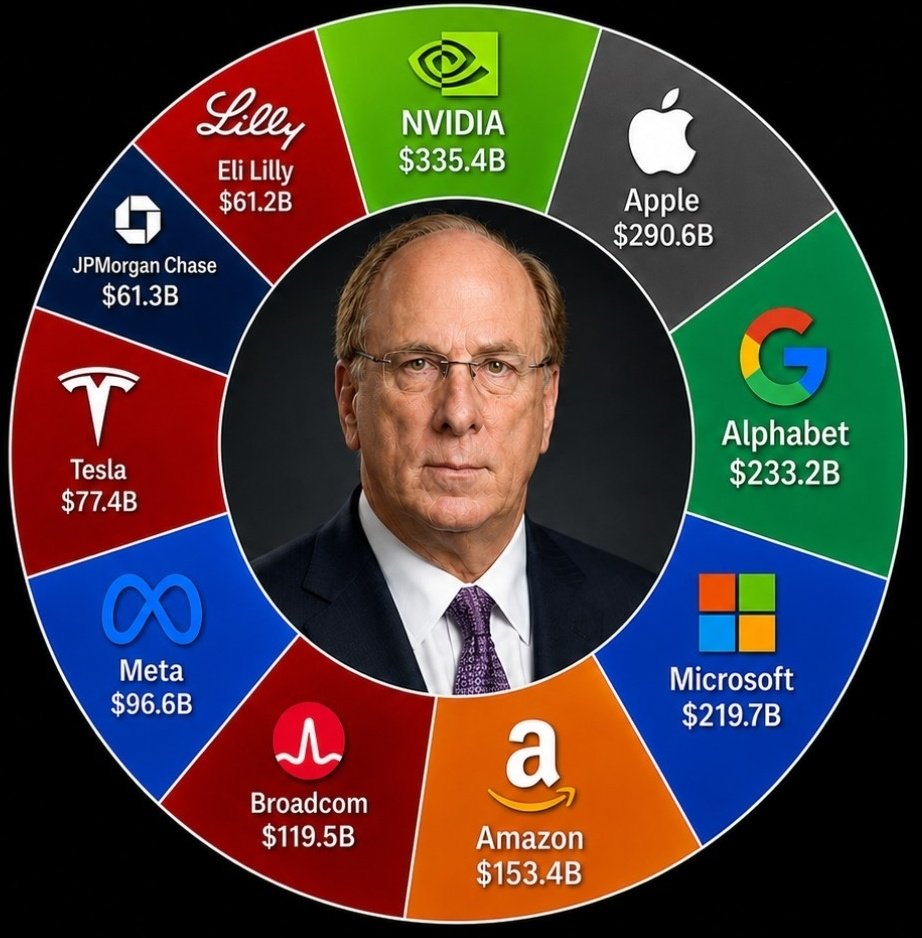

BlackRock's Stock Portfolio:

5

65

520

20,456

Growth Stocks Traveler retweeted

Barack and I were so honored to have @AkunyiliCrosby create our portrait for the Obama Presidential Center. Her artistic brilliance shines through — and the way she infused such life and joy into the piece is truly extraordinary. We love it, and we think everyone who visits the Center will too!

1,740

5,660

28,839

675,610

Growth Stocks Traveler retweeted

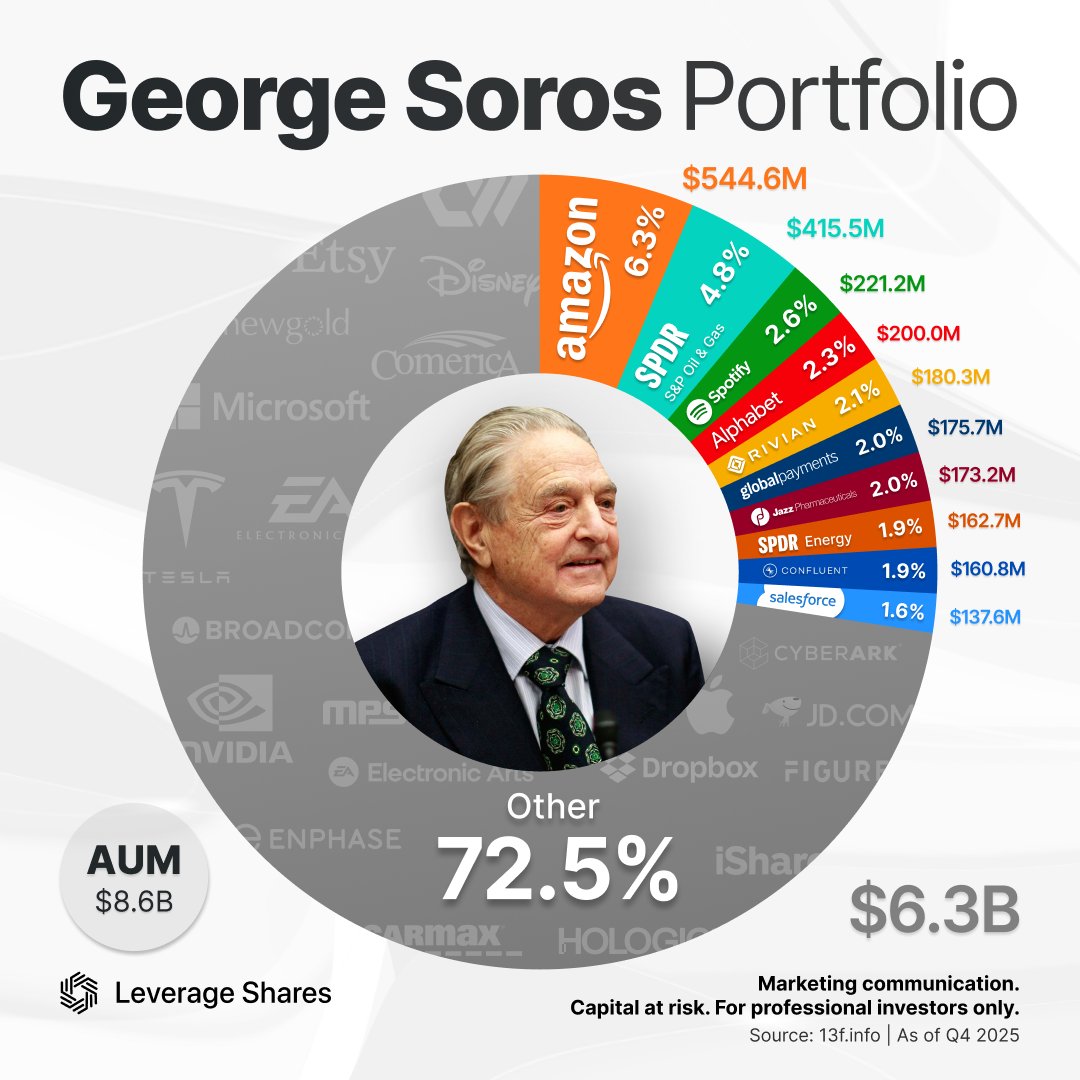

George Soros Portfolio

2

38

240

15,444

Growth Stocks Traveler retweeted

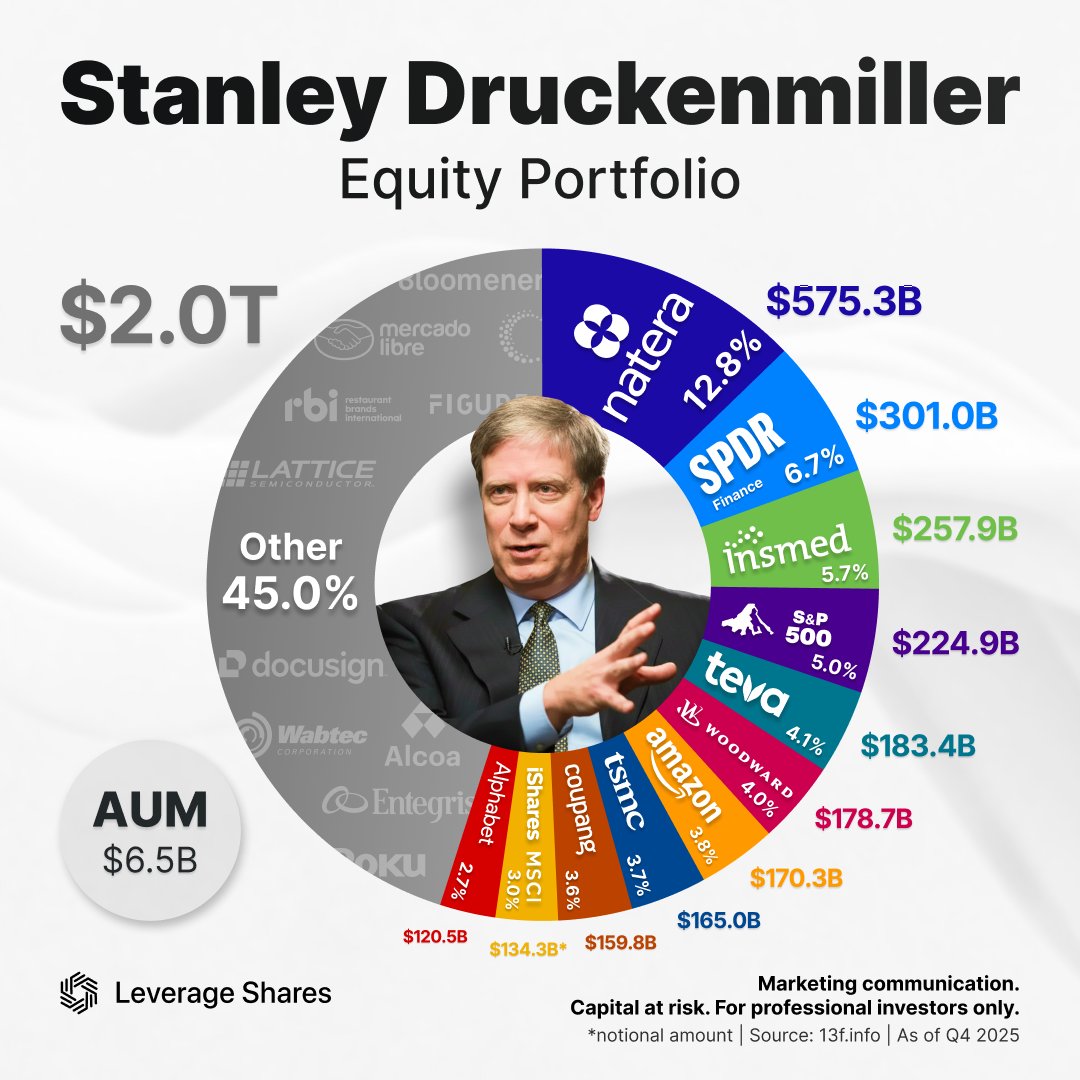

Stanley Druckenmiller Portfolio

12

54

3,449

Growth Stocks Traveler retweeted

🚨 14 Quality Stocks Trading Near Their 52-Week Lows

Some stocks are under pressure, but the underlying businesses continue to show resilience.

$PLTR | Palantir

$MSFT | Microsoft

$META | Meta

$SOFI | SoFi

$MELI | MercadoLibre

$SE | Sea Limited

$UBER | Uber

$NFLX | Netflix

$MA | Mastercard

$GRAB | Grab

$RBLX | Roblox

$CELH | Celsius Holdings

$DOCU | DocuSign

$KVYO | Klaviyo

7

29

3,151

Growth Stocks Traveler retweeted

🔥 THE WORLD’S MOST VALUABLE SEMICONDUCTOR COMPANIES 🤖💾

AI infrastructure is now creating trillion-dollar chip giants.

🥇 NVIDIA $NVDA — $4.97T

🥈 TSMC $TSM — $2.20T

🥉 Broadcom $AVGO — $1.82T

4️⃣ Samsung $005930.KS — $1.46T

5️⃣ Micron $MU — $1.11T

6️⃣ SK Hynix $000660.KS — $1.07T

7️⃣ AMD $AMD — $834B

8️⃣ ASML $ASML — $718B

9️⃣ Intel $INTC — $626B

🔟 Lam Research $LRCX — $459B

🎯 Key Takeaways

🤖 AI chips dominate the list

NVIDIA

AMD

Broadcom

TSMC

💾 Memory is back in a massive way

Micron

SK Hynix

Samsung

🏭 The AI supply chain is global

USA

Taiwan

South Korea

Netherlands

⚙️ Semicap equipment remains critical

ASML

Lam Research

💡 Bottom Line

The AI boom is not just lifting software companies.

It is creating a new semiconductor supercycle across:

✅ GPUs

✅ HBM memory

✅ Foundries

✅ Networking chips

✅ Lithography

✅ Wafer equipment

🚀 AI infrastructure is now the most valuable trade in global markets.

2

2

180

Growth Stocks Traveler retweeted

11

11

153

54,166

Growth Stocks Traveler retweeted

Jun 14

Here's the most ridiculous yearly chart you'll see today:

$STX

30

47

587

74,985