A new private forum for credit investors to exchange views on the most topical names. Lifetime FREE access for first 250 members.

Joined January 2026

- Tweets 240

- Following 156

- Followers 150

- Likes 230

20 Photos and videos

Pinned Tweet

What is The Credit Stack? 🧵 A private forum for professional credit investors to discuss the most topical names and situations in credit.

1

896

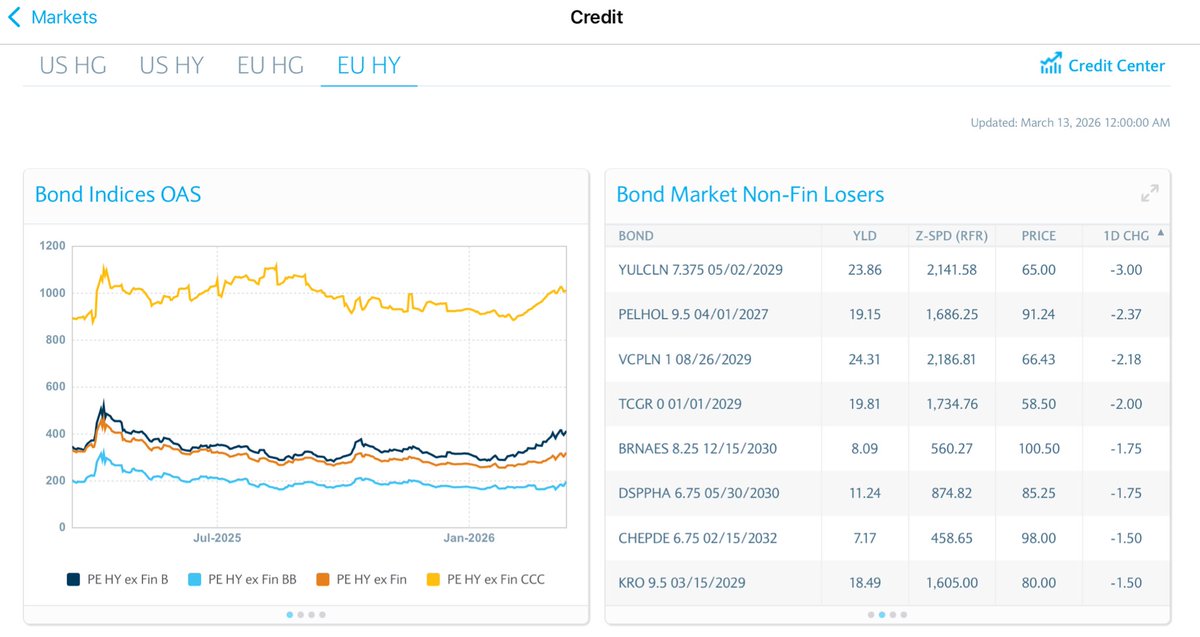

📆Earnings season is here for European HY Chemicals 🧪

We are building consensus for:

🔵 Arxada (LNZING) — 14 Apr

🔵 INEOS Group (INEGRP) — 23 Apr

🔵 INEOS Quattro (STYRO) — 24 Apr

Submit your EBITDA estimates up to COB 3 days prior → see Credit Stack Consensus 48hrs before earnings drop ⬇️

1

352

🚀 Introducing Credit Stack Consensus — private company HY earnings estimates, crowdsourced from buy-side and sell-side credit professionals.

Submit your estimate → unlock the consensus.

No Bloomberg. No broker. Just the market’s actual view.

We’ve started small with some upcoming EUR HY Chems. Check it out ⬇️

1

2

4

958

🔥🔥🔥Free access to The Credit Stack 🔥🔥🔥

A private forum for HY/distressed/special sits investors

Sign up, post one 5 line thread, you’re in for life.

Link in bio 🫡

1

1

511

🚨The Credit Stack is now offering FREE lifetime memberships to the first 250 sign-ups 🚨

Sign-up ➡️ start one new company thread (as little as 5 lines) ➡️ join the conversation ➡️ FREE LIFETIME ACCESS

1

188

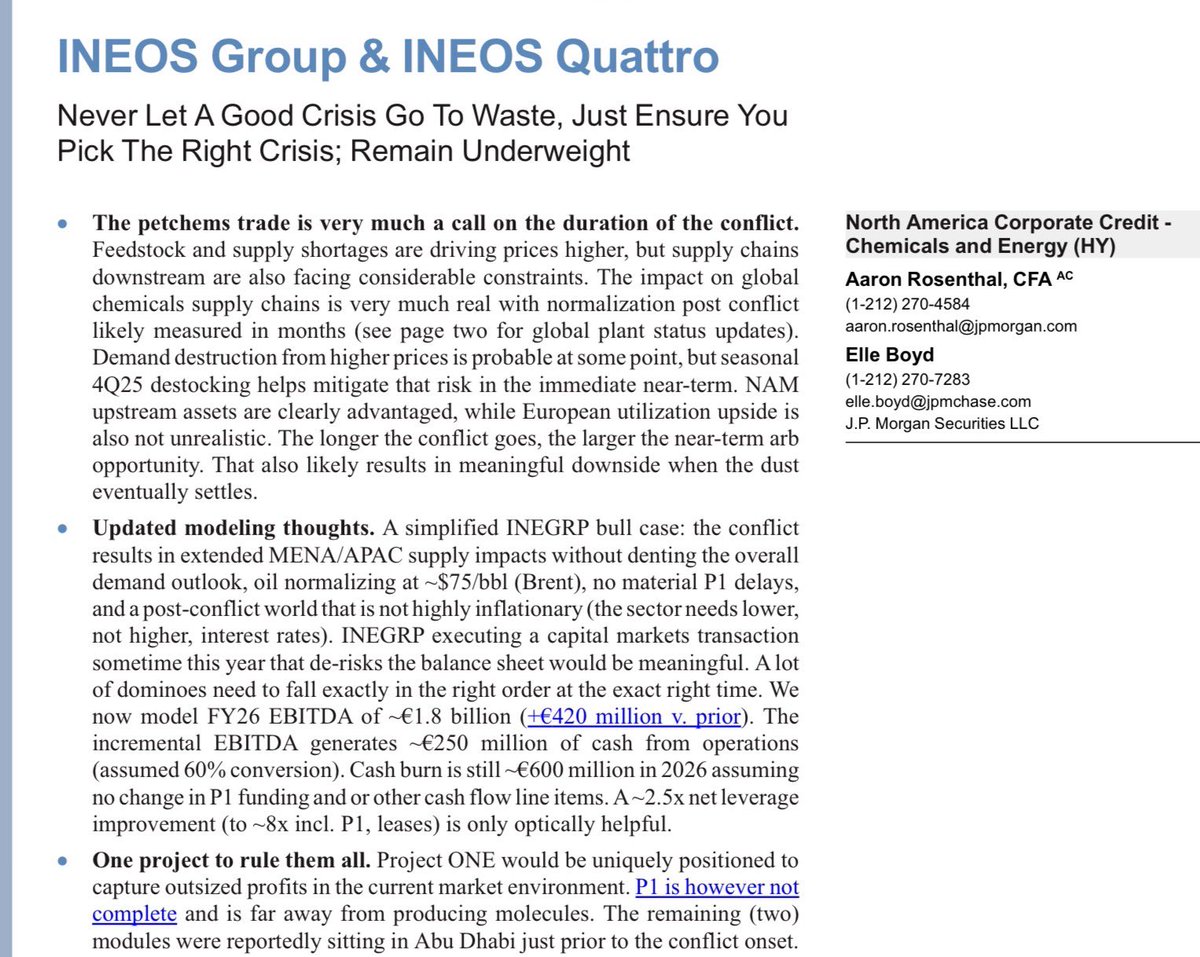

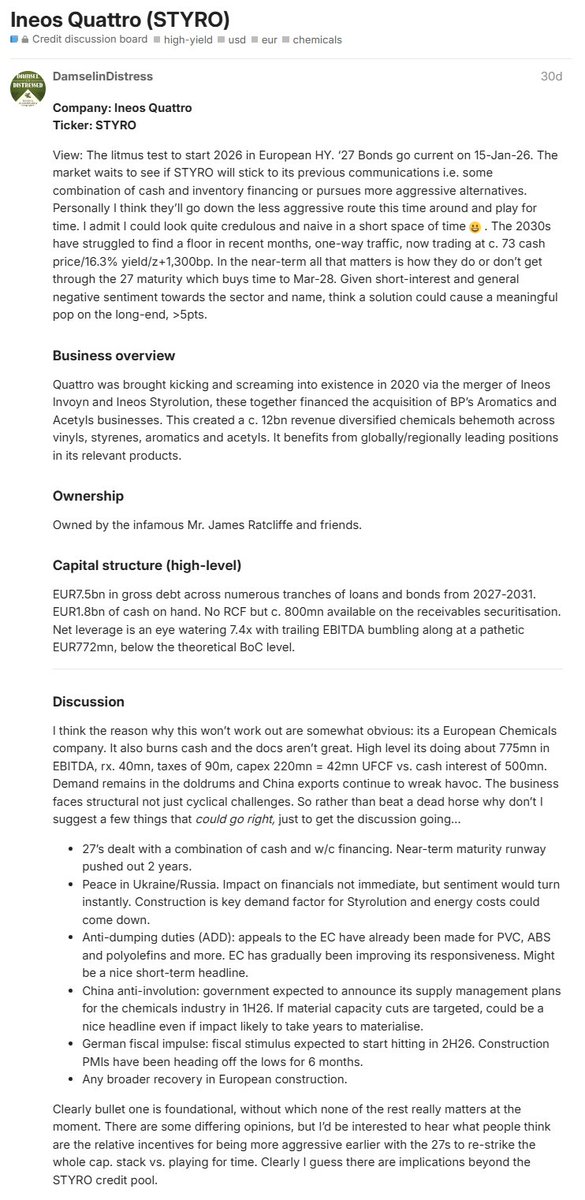

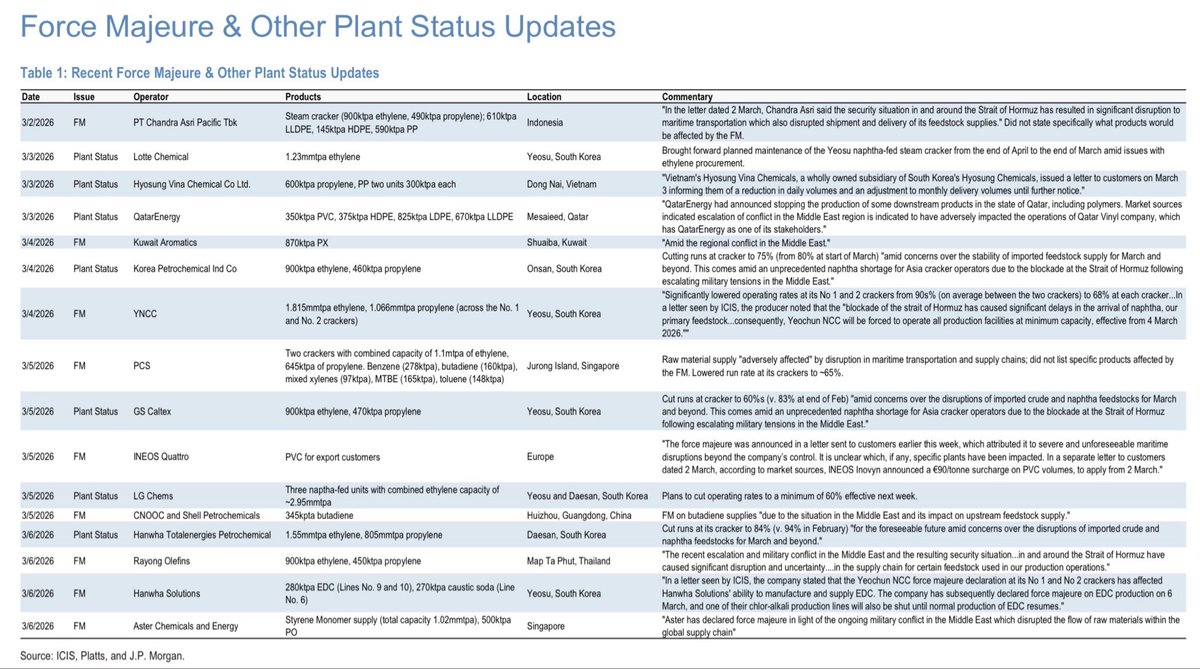

European Chemicals, already on the brink, could be pushed over the edge by the Iran conflict. Energy costs will rocket but the impact is more nuanced than at first glance. Disruptions to cheap ME & Asian supply could provide a near-term boost.

[credit: JPM & Aaron Rosenthal]

2

4

768

The Credit Stack retweeted

Mar 13

Private Credit: The Moment of Truth

andromedainvestors.com/

1

4

23

5,538

The Credit Stack retweeted

Mar 14

There are at least 6 problems in no particular order:

-mislabeling or intentionally disguising the amount SaaS exposure in some porfolios

-no concept of portfolio construction for some of the direct lending managers

-mismarking and/or marking inconsistencies across funds

-other uses of leverage away from the basic bank/bond/clo financing of direct lending - 2nd outs, jv’s, direct clo equity investments to juice returns and mask the real underlying leverage of the portfolio

-250bln of the direct lending market is in “semi-liquid” products where underlying isn’t liquid at all

-prisoners dilemma for LP’s of that last bucket - if you don’t redeem do you just get left with the turds?

Everyone has to make their own opinion on the SaaS and AI disruptions threatened loans. I think there will be a very interesting secondary opportunity as entities look to sell to meet redemptions or reduce exposure to areas they are too overweight. Right now though to your point Boaz the public BDC’s at .85 -.95 GAV - I look at GAV not EQUITY NAV bc the latter ignores the ultimate downside risk - are cheap to where these secondary private portfolios are offered/trading - I think there will be a convergence in the near future given the amount likely to come for sale.

16

50

622

389,627

The Credit Stack retweeted

Mar 12

My take: The best opportunity in the market is setting up a fund/vehicle to buy dislocated private credit loans from forced sellers.

My credentials: I run the leading information and data provider on the global credit markets (@OctusCredit). I was buying bank debt in the 60s in the fall of 2008 that eventually refi'd at par, including from the Lehman desk auction. I am very bullish on software and think the Citrini thesis is flawed. I reached out to them to debate me on our podcast.

Two quotes from Seth Klarman have guided my investing for over 20 years:

1) "My experience is that when people want to give something away at a ridiculous price because they have to, not because they want to, that’s a good time to buy."

2) "The best opportunities for value investors often arise when other investors are forced to sell, regardless of price."

Over the past couple of weeks, headlines have rolled in about redemptions coming from public and private credit funds:

""Morgan Stanley Limits Redemptions at $7.6B North Haven Fund After Withdrawal Requests Hit 11%" (March 12, 2026)"

"Cliffwater Limits Repurchases to 7% After Record 14% of Investors Seek Exit From $33B Flagship"

"Blue Owl Gates OBDC II as Hedge Funds Circle With 35% Discount Buyout Offers" (March 10, 2026)

Another headline: "Private Credit ETFs Plunge 18% in Two Weeks as 'Gating' Fears Spread to Publicly Traded Vehicles"

I believe these headlines will continue. Investors should get used to them. Or as George Soros' concept of reflexivity: our perceptions of reality don’t just reflect reality—they actively change it.

Or in steps...

1. The Bias

Investors believe private credit is a "magic" asset class: high yields with low volatility. They assume "semi-liquid" funds mean they can always get their cash back quarterly.

2. The Action

A $1.7 trillion wall of cash pours in. This massive liquidity makes the underlying borrowers (software companies) look healthier than they are, "validating" the initial bias.

3. The Pivot

AI threats / Citrini thesis emerge. A few "smart money" investors doubt the fund valuations and submit redemption requests to test the exit.

4. The Spiral

Funds hit their 5% withdrawal caps and "gate" the doors. This act of self-preservation signals "danger" to the rest of the herd, turning a small exit into a mass panic.

5. The New Reality

The perception of a "safe haven" has been reflexively destroyed. The asset is now a liquidity trap, creating the "forced sellers" that Seth Klarman waits for.

Soros once wrote: "Financial markets, far from accurately reflecting all the available knowledge, always provide a distorted view of reality. The degree of distortion may vary from time to time; sometimes it’s quite negligible, at other times it is quite pronounced."

If redemptions still continue and private credit is considered an asset to avoid, more investors will ask for their money back. And more funds will be forced to sell assets inside these funds.

The underlying businesses haven't changed. The huge cash equity checks beneath these loans haven't changed (Yes LTV has changed because multiples have compressed but cash is still there). The maturity profile hasn't changed. Revolvers are still available.

The one thing that has changed is the reflexivity of the new reality and people are rushing for the doors in an illiquid market = buying opportunity.

Here is some simple math:

If you buy a loan at 90, with a SOFR 500 floating rate coupon that matures/refis at par in 3 years your return is ~13%.

If you buy a loan at 80, with a SOFR 500 floating rate coupon that matures at par/refis in 3 years your return is ~18%.

If you buy a loan at 75, with a SOFR 500 floating rate coupon that matures/refis at par in 3 years your return is ~21%.

I view these as the absolute LOW returns. I believe returns will be materially higher for 2 reasons:

1) The AI/Citrini thesis will be proven wrong shortly throughout this year as software companies report good numbers in Q1, Q2 and Q3

2) In the very off-chance you get to own the keys of these companies, buying a software company through a restructuring has the chance of MOICs over 2.0x taking into effect rights and equity discounts.

All told: As I said on our podcast, I think this could be a once in a generation opportunity to buy assets with MINIMUM mid teen returns, very little chance of capital loss with potential huge upsides.

I do not think an investor should BLINDLY buy everything being force sold by a private credit fund or BLINDLY buy every software company out there. But this is so overblown its creating an opportunity for the best credit investors in the world to set up vehicles to absolutely crush it. An alpha, not a beta trade.

The table is being set. The smart funds are already setting up to capitalize on this opportunity as it plays out over the rest of the year.

7

10

104

55,984

🚨New Credit Stack Hack Just Dropped🚨

Problem: ⏳ No time to login type up my thoughts.

Solution: 🎤 Quick voice message ➡️ @openclaw 🦞 ➡️ post live on TCS ✅ 🫡

I think this is called “AI enabled” 👀

#highyield #credit #AIenabled

166

🔥 What's being discussed on The Credit Stack this month?

Here's what's generating the most heat 🧵👇

#highyield #credit

1

1

2

532

🇺🇸 US HY

📌 Tronox (TROX)

📌 BORR Drilling (BORRNO)

📌 PetSmart (PETM)

📌 Innophos (IPHS)

📌 Organon (OGN)

📌 Celanese (CE)

1

230

💬

The Credit Stack is a private forum for professional credit investors.

👉 thecreditstack.co

149

ION Platform bonds down 20 points in a month, one of the most shorted names in European credit. But founder Andrea Pignataro just broke his silence with a contrarian take on the SaaSpocalypse worth reading.

🧵

#highyield #credit

Pignataro's core argument: there's a "substitution fallacy" at work. Just because AI can perform a cognitive task that software facilitates doesn't mean it can replace the software. Enterprise software isn't a task tool — it's a coordination layer. You don't just use Salesforce, you speak it.

1

361

Hebbia founder George Sivulka put it well: 90% of any finance job is routine. The other 10% — the preferences of a particular MD, the way a specific desk formats things — is where deals get done. "90% right is the same as 100% wrong."

1

151

Back to the credit: ION Platform has no immediate triggers post-September refi, strong recurring revenues with long-term contracts and good cash generation. The question is whether the subscription model and margins face a real AI threat — or whether the moat holds.

For signs of stress in the Pignataro empire, watch the Italian businesses — Cerved and Cedacri.

Source: Octus, EMEA Special Sits Weekly (Feb 2026)

104